Key Insights

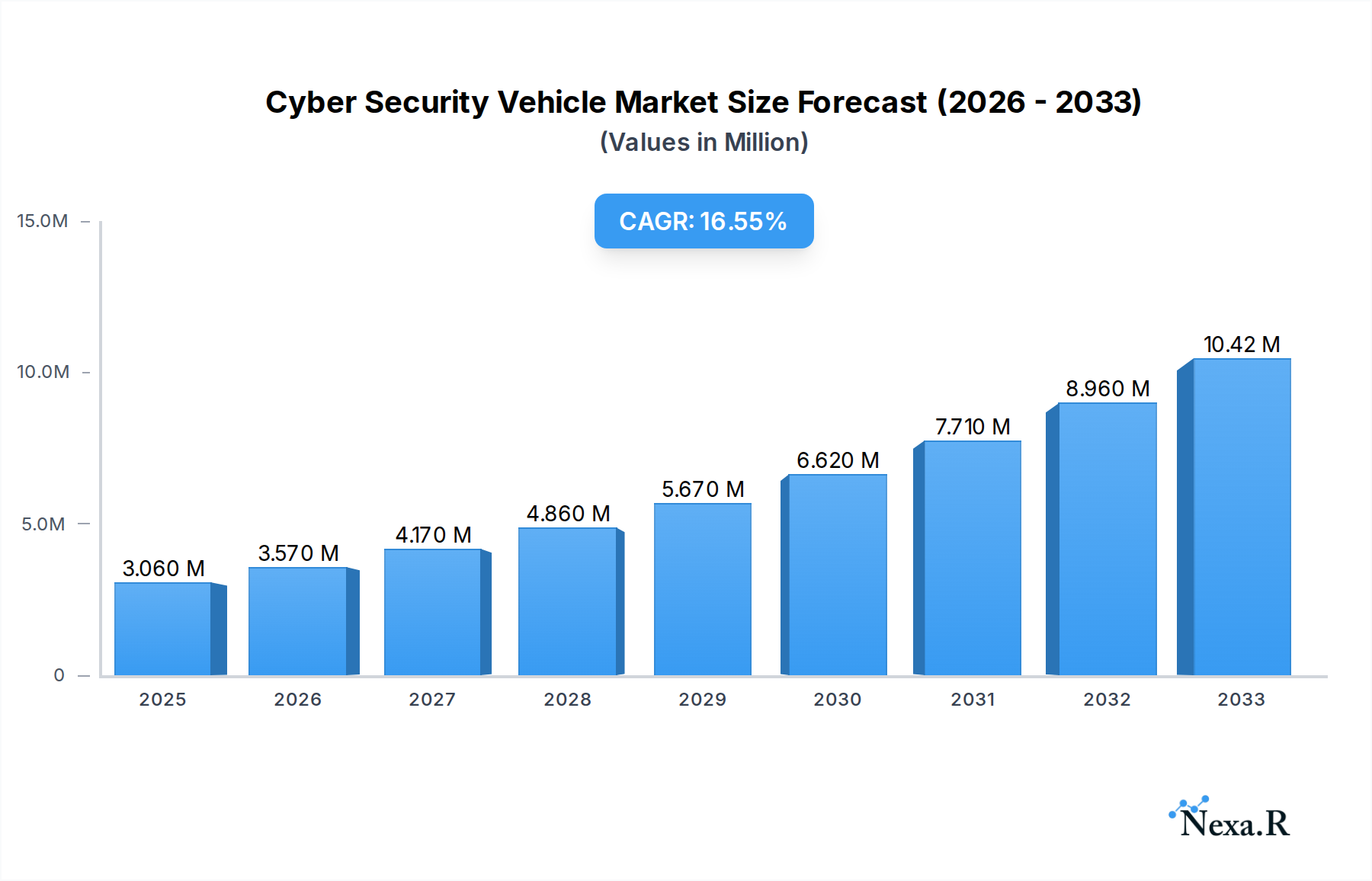

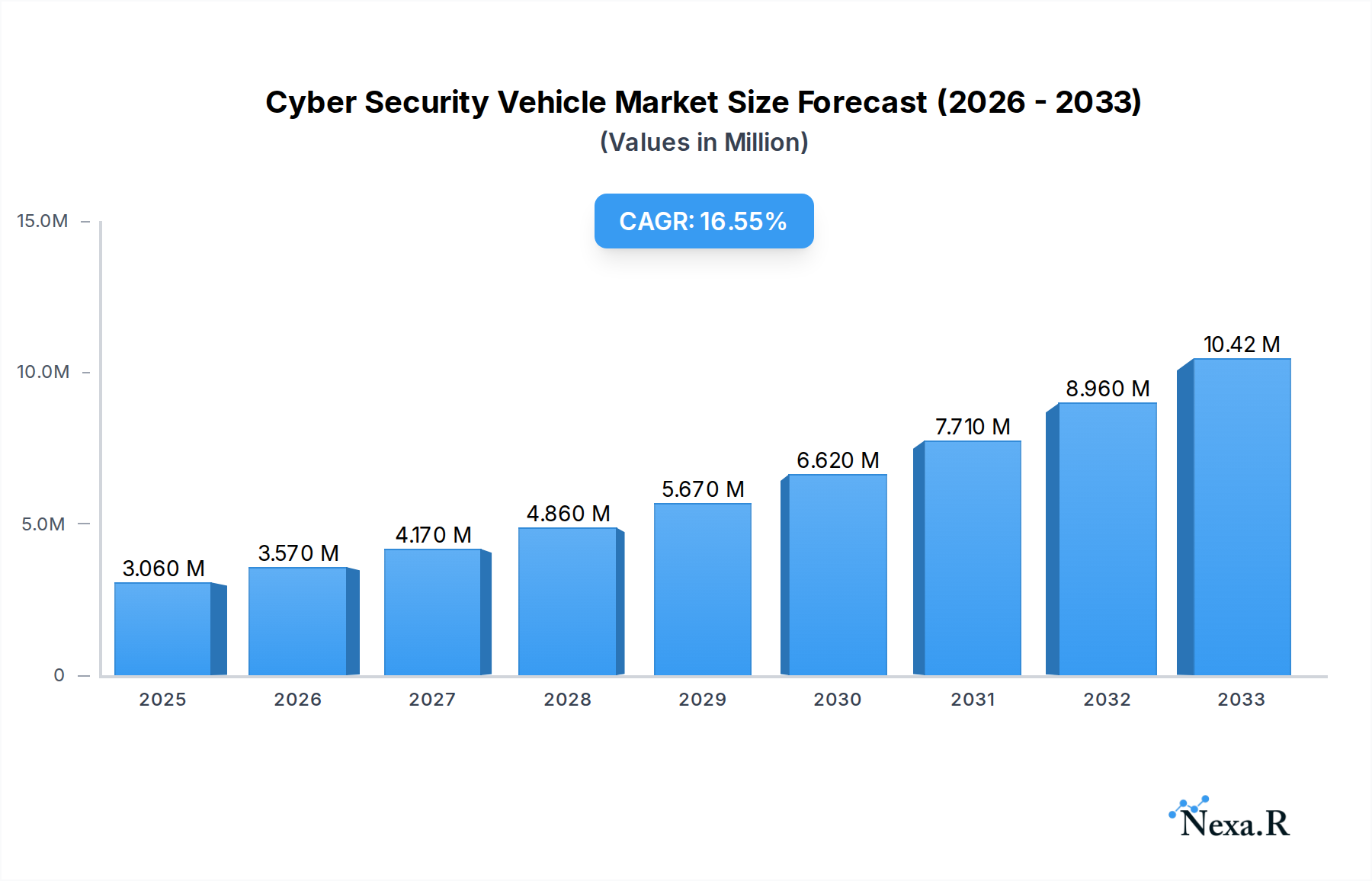

The global Cyber Security Vehicle Market is poised for substantial expansion, projected to reach a market size of 3.06 Million by 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 16.66%. This significant growth is fueled by the escalating sophistication of cyber threats targeting connected and autonomous vehicles, necessitating advanced security solutions to protect sensitive data and ensure operational integrity. Key market drivers include the increasing adoption of connected car technologies, the proliferation of in-vehicle infotainment systems, and the growing demand for advanced driver-assistance systems (ADAS), all of which present expanded attack surfaces for cyber adversaries. Furthermore, stringent regulatory frameworks and automotive industry standards emphasizing vehicle cybersecurity are compelling manufacturers to invest heavily in robust security architectures. The market is segmented across various solution types, with Software-Based solutions leading due to their adaptability and ease of integration, followed by Hardware-Based solutions offering foundational protection. Professional Services are also gaining prominence as automakers seek expert guidance in implementing and managing complex cybersecurity strategies. Network Security and Application Security are critical security types, addressing the vulnerabilities inherent in vehicle communication networks and the software applications running within them. Leading companies like Karamba Security Ltd, Harman International Industries Inc (Samsung), and Continental AG are at the forefront, innovating and competing to offer comprehensive cybersecurity portfolios.

Cyber Security Vehicle Market Market Size (In Million)

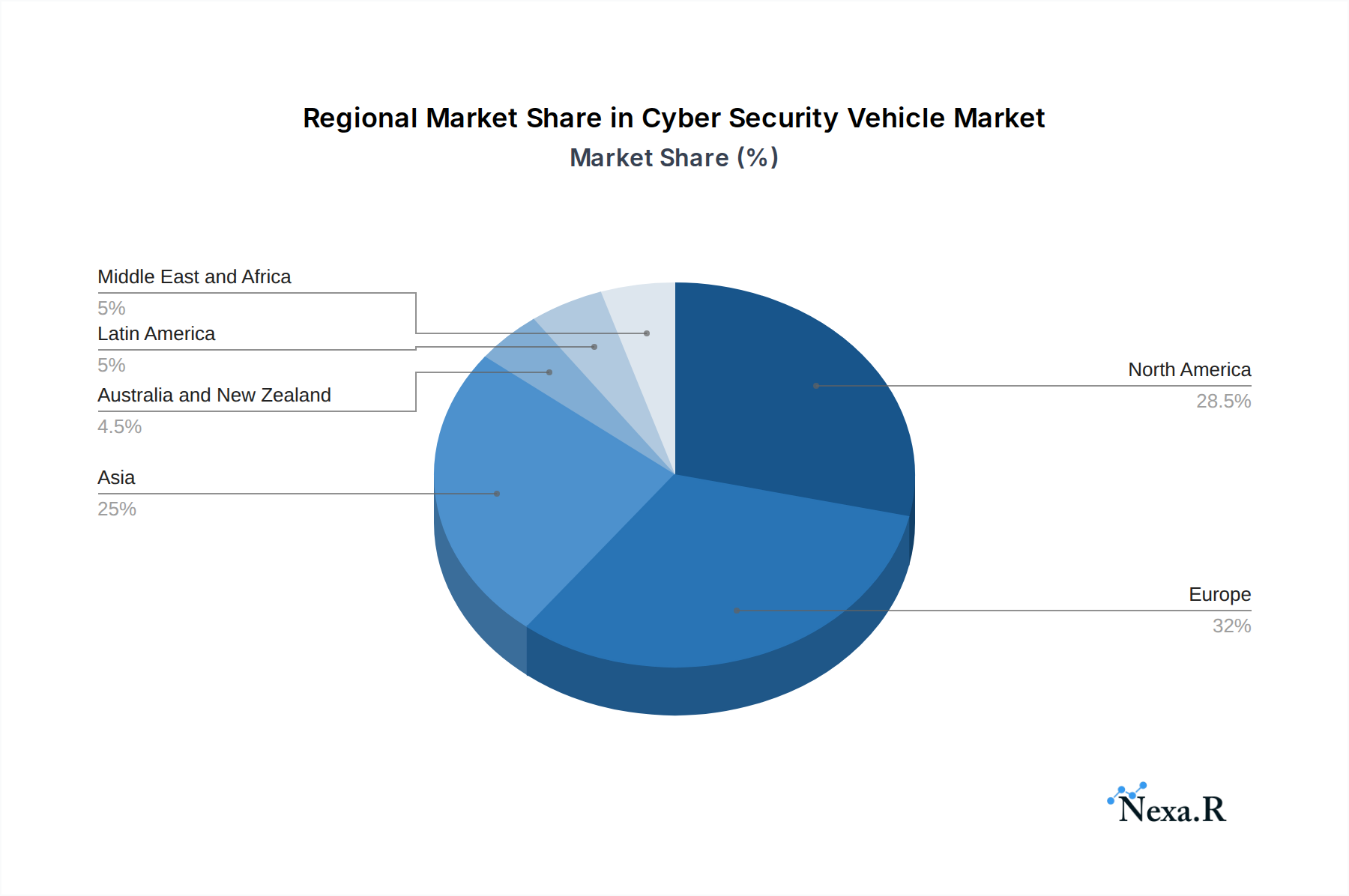

The forecast period from 2025 to 2033 anticipates continued dynamism, with the market size expected to grow exponentially. Emerging trends such as the integration of AI and machine learning for threat detection and prevention, the development of secure over-the-air (OTA) updates, and the establishment of end-to-end cybersecurity frameworks for vehicle lifecycles are shaping the competitive landscape. However, the market also faces restraints, including the high cost of implementing advanced cybersecurity measures, the complexity of securing legacy vehicle systems, and the shortage of skilled cybersecurity professionals within the automotive sector. Geographically, North America and Europe are expected to dominate the market share due to early adoption of connected vehicle technologies and stringent regulatory environments. The Asia-Pacific region is anticipated to witness the fastest growth, driven by increasing automotive production and a rising awareness of cybersecurity risks. Investments in research and development by major players, alongside strategic partnerships and collaborations, will be crucial in overcoming these challenges and capitalizing on the immense opportunities within this rapidly evolving market.

Cyber Security Vehicle Market Company Market Share

This in-depth report provides a definitive analysis of the global Cyber Security Vehicle Market, examining its intricate dynamics, growth trajectories, and the strategic landscape from 2019 to 2033. With a base year of 2025, this report offers invaluable insights for automotive manufacturers, cybersecurity providers, technology integrators, and investors seeking to capitalize on the rapidly evolving connected vehicle ecosystem. Explore the segmentation by solution type (Software-Based, Hardware-Based, Professional Service, Integration, Other Types of Solution) and security type (Network Security, Application Security, Cloud Security, Other Types of Security), understanding the market's structure and demand drivers. Dive into parent market and child market analyses to grasp the broader industry context and specific sub-segment opportunities within the automotive cybersecurity market.

Cyber Security Vehicle Market Dynamics & Structure

The Cyber Security Vehicle Market is characterized by a moderately concentrated structure, with key players investing heavily in research and development to address escalating threats. Technological innovation is the primary driver, fueled by the increasing complexity of vehicle architectures and the proliferation of connected features. Regulatory frameworks, such as UNECE WP.29 and ISO/SAE 21434, are becoming more stringent, compelling manufacturers to prioritize robust cybersecurity solutions. Competitive product substitutes are emerging, ranging from integrated OEM solutions to specialized third-party offerings, creating a dynamic competitive landscape. End-user demographics are shifting towards early adopters of advanced automotive technologies, demanding enhanced safety and data privacy. Mergers and acquisitions (M&A) are a significant trend, with larger players acquiring specialized cybersecurity firms to bolster their capabilities. For instance, in July 2022, Infineon Technologies acquired NoBug Consulting SRL and NoBug d.o.o., enhancing its Connected Secure Systems (CSS) Division for complex IoT product development.

- Market Concentration: Moderate, with leading automotive and technology giants holding significant market share.

- Technological Innovation Drivers: Advanced driver-assistance systems (ADAS), autonomous driving, over-the-air (OTA) updates, and in-car infotainment systems.

- Regulatory Frameworks: UNECE WP.29, ISO/SAE 21434, GDPR, and regional data privacy laws.

- Competitive Product Substitutes: In-vehicle network security, end-to-end encryption, intrusion detection and prevention systems.

- End-User Demographics: Tech-savvy consumers, fleet operators, and commercial vehicle providers.

- M&A Trends: Strategic acquisitions of specialized cybersecurity firms by Tier-1 suppliers and OEMs.

- M&A Deal Volumes: xx million units in the historical period, projected to reach xx million units by 2028.

Cyber Security Vehicle Market Growth Trends & Insights

The Cyber Security Vehicle Market is poised for substantial growth, driven by the exponential rise in connected vehicles and the increasing sophistication of cyber threats. The market size is projected to expand from an estimated xx million units in the base year 2025 to xx million units by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of xx% during the forecast period. Adoption rates for advanced cybersecurity solutions are accelerating as automakers recognize the critical need to protect vehicle systems and sensitive user data. Technological disruptions, including the integration of AI and machine learning for threat detection and the evolution of secure software development practices, are reshaping the market. Consumer behavior is shifting, with a growing emphasis on data privacy and security as purchase decision factors. The market penetration of dedicated cybersecurity solutions in new vehicle sales is expected to rise from xx% in 2025 to xx% by 2033. This growth is underpinned by an increasing awareness of the financial and reputational risks associated with cyber breaches in the automotive sector.

The increasing reliance on interconnected systems within modern vehicles creates a vast attack surface, making robust cybersecurity no longer an optional feature but a fundamental requirement. The proliferation of IoT devices and sensors within the vehicle, coupled with external connectivity for services like telematics, navigation, and infotainment, necessitates comprehensive security measures. Over-the-air (OTA) updates, while offering convenience and efficiency, also present a potential vulnerability if not secured properly, further emphasizing the need for secure software-based solutions. The demand for secure communication protocols, secure boot processes, and tamper-proof hardware components is on the rise. Furthermore, the development of autonomous driving capabilities amplifies the stakes, as any compromise could have severe safety implications. This escalating complexity and risk profile directly translate into a sustained demand for advanced cybersecurity solutions across the entire automotive value chain.

The market is also witnessing a paradigm shift in how cybersecurity is approached. Previously viewed as a peripheral concern, it is now being integrated into the core design and development phases of vehicles. This proactive approach, often termed "security by design," involves embedding security considerations from the earliest stages of concept and architecture to final deployment and maintenance. This shift is driven by both internal pressures from R&D departments and external pressures from regulatory bodies and consumer expectations. The growing trend of software-defined vehicles further underscores the importance of cybersecurity, as software increasingly dictates vehicle functionality and performance. Securing these software layers against malicious attacks, unauthorized access, and data breaches is paramount.

Dominant Regions, Countries, or Segments in Cyber Security Vehicle Market

The Cyber Security Vehicle Market is experiencing significant growth across various regions and segments, with North America and Europe currently leading in adoption and development. In North America, the high penetration of connected vehicles, coupled with stringent data privacy regulations and a strong emphasis on consumer safety, propels the demand for advanced Network Security and Application Security solutions. The region benefits from a mature automotive industry and a significant presence of leading cybersecurity technology providers.

Europe follows closely, driven by the proactive regulatory environment, particularly the General Data Protection Regulation (GDPR), which necessitates robust data protection measures for connected vehicle data. The region's commitment to innovation in automotive technology and the increasing deployment of ADAS features further fuel the market for Hardware-Based and Software-Based cybersecurity solutions.

Asia Pacific, particularly China and South Korea, represents a rapidly growing market. The swift adoption of connected car technologies, burgeoning electric vehicle (EV) market, and government initiatives supporting automotive innovation are key drivers. The demand for Cloud Security solutions is also escalating as more vehicle data is processed and stored in cloud platforms.

From a segment perspective, Software-Based solutions currently dominate the market, owing to their flexibility, scalability, and ability to address complex threat landscapes. This segment includes intrusion detection and prevention systems, secure operating systems, and threat intelligence platforms. Hardware-Based solutions, such as secure microcontrollers and hardware security modules (HSMs), are also gaining traction due to their inherent security and performance advantages. Professional Services, including risk assessment, penetration testing, and incident response, are crucial for ensuring comprehensive cybersecurity strategies and are witnessing steady growth. The Integration segment, focused on seamlessly embedding cybersecurity solutions into vehicle architectures, is also vital.

- Dominant Regions:

- North America: High adoption of connected vehicles, stringent regulations, strong R&D.

- Europe: Proactive regulatory environment (GDPR), commitment to automotive innovation.

- Asia Pacific: Rapidly growing EV market, government support for automotive tech.

- Dominant Segments by Type of Solution:

- Software-Based: Currently leading due to flexibility and scalability.

- Hardware-Based: Growing rapidly for enhanced security and performance.

- Professional Service: Essential for comprehensive strategy and support.

- Dominant Segments by Type of Security:

- Network Security: Critical for protecting vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communications.

- Application Security: Essential for securing in-vehicle software and infotainment systems.

- Cloud Security: Increasingly important with the rise of cloud-based automotive services.

Cyber Security Vehicle Market Product Landscape

The product landscape of the Cyber Security Vehicle Market is characterized by a sophisticated array of solutions designed to protect vehicles from an evolving threat matrix. Innovations include next-generation firewalls, intrusion detection and prevention systems (IDPS) specifically tuned for automotive networks, and secure gateways that act as critical choke points for data flow. Software-based solutions are increasingly leveraging AI and machine learning for real-time anomaly detection and predictive threat intelligence, enabling proactive defense against emerging cyberattacks. Hardware-based security modules (HSMs) and secure element chips are being integrated to provide tamper-proof storage for critical cryptographic keys and secure execution environments for sensitive operations. Furthermore, advancements in secure over-the-air (OTA) update mechanisms ensure the integrity and authenticity of software patches, a crucial aspect for maintaining long-term vehicle security.

Key Drivers, Barriers & Challenges in Cyber Security Vehicle Market

Key Drivers:

- Increasing Connectivity: The proliferation of connected features in vehicles creates new attack vectors, driving the need for robust cybersecurity.

- Evolving Threat Landscape: Sophisticated cyberattacks targeting vehicles are becoming more frequent and complex, necessitating advanced defense mechanisms.

- Regulatory Mandates: Stringent automotive cybersecurity regulations are compelling manufacturers to prioritize security.

- Data Privacy Concerns: Growing awareness of data privacy issues among consumers is pushing for enhanced protection of personal information.

- Autonomous Driving Development: The safety-critical nature of autonomous systems demands uncompromising cybersecurity.

Barriers & Challenges:

- High Development Costs: Implementing comprehensive cybersecurity solutions can be expensive, impacting vehicle pricing.

- Complexity of Vehicle Architectures: Integrating cybersecurity across diverse and complex vehicle systems is challenging.

- Talent Shortage: A lack of skilled cybersecurity professionals in the automotive sector hinders effective implementation.

- Supply Chain Vulnerabilities: Security risks within the automotive supply chain can compromise vehicle security.

- Legacy Systems: Integrating cybersecurity into older vehicle platforms presents significant hurdles.

- Rapid Technological Evolution: The fast pace of technological advancement requires continuous adaptation of cybersecurity strategies.

Emerging Opportunities in Cyber Security Vehicle Market

Emerging opportunities in the Cyber Security Vehicle Market lie in the development of AI-powered predictive cybersecurity solutions that can anticipate and neutralize threats before they materialize. The growing demand for secure mobility-as-a-service (MaaS) platforms presents a significant avenue for providers of end-to-end vehicle security and data protection. Furthermore, the expansion of vehicle-to-everything (V2X) communication technologies necessitates robust cybersecurity frameworks to ensure the integrity and safety of inter-vehicle and infrastructure communication. Untapped markets in developing regions with rapidly growing automotive sectors also represent significant growth potential for affordable and scalable cybersecurity solutions. The increasing adoption of blockchain technology for secure data logging and identity management within vehicles also opens new avenues for innovation and market expansion.

Growth Accelerators in the Cyber Security Vehicle Market Industry

Key catalysts driving long-term growth in the Cyber Security Vehicle Market include breakthroughs in quantum-resistant cryptography, which will safeguard vehicles against future quantum computing threats. Strategic partnerships between automotive OEMs, Tier-1 suppliers, and specialized cybersecurity firms are accelerating the development and deployment of integrated security solutions. The increasing focus on cybersecurity in electric vehicle (EV) charging infrastructure also presents a significant growth opportunity, ensuring the security of energy networks and user data. Furthermore, the standardization of cybersecurity protocols and best practices across the industry will foster greater interoperability and accelerate market adoption. The continued evolution of automotive software, especially in the context of software-defined vehicles, will consistently drive demand for advanced cybersecurity measures.

Key Players Shaping the Cyber Security Vehicle Market Market

- Karamba Security Ltd

- Harman International Industries Inc (Samsung)

- Escrypt GmbH

- Infineon Technologies AG

- Honeywell International Inc

- Denso Corporation

- Visteon Corporation

- Delphi Automotive PLC

- NXP Semiconductors NV

- Arilou Technologies Ltd

- Cisco Systems Inc

- Continental AG

- Argus Cybersecurity Ltd

- Secunet AG

Notable Milestones in Cyber Security Vehicle Market Sector

- July 2022: Infineon Technologies acquired NoBug Consulting SRL (Romania) and NoBug d.o.o. (Serbia) to enhance its Connected Secure Systems (CSS) Division's capacity for complex IoT product development, including cybersecurity and AI for future IoT infrastructure.

- July 2022: NXP Semiconductors announced a collaboration agreement with Hon Hai Technology Group ("Foxconn") to develop platforms for a new generation of intelligently connected automobiles, leveraging NXP's automotive technology and expertise in safety and security.

In-Depth Cyber Security Vehicle Market Market Outlook

The Cyber Security Vehicle Market is set for sustained and significant growth, fueled by an unwavering commitment to vehicle safety, data privacy, and the rapid advancement of automotive technology. Growth accelerators such as AI-driven threat detection, secure V2X communication protocols, and the development of quantum-resistant cybersecurity measures will define the future landscape. Strategic collaborations and regulatory advancements will further solidify the market's expansion. The increasing demand for secure software-defined vehicles and the burgeoning electric vehicle sector present substantial opportunities for innovation and market penetration. The industry is moving towards a proactive, integrated approach to cybersecurity, ensuring that future mobility is not only intelligent and efficient but also inherently secure, creating a robust and trustworthy automotive ecosystem for years to come.

Cyber Security Vehicle Market Segmentation

-

1. Type of Solution

- 1.1. Software-Based

- 1.2. Hardware-Based

- 1.3. Professional Service

- 1.4. Integration

- 1.5. Other Types of Solution

-

2. Type of Security

- 2.1. Network Security

- 2.2. Application Security

- 2.3. Cloud Security

- 2.4. Other Types of Security

Cyber Security Vehicle Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Cyber Security Vehicle Market Regional Market Share

Geographic Coverage of Cyber Security Vehicle Market

Cyber Security Vehicle Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.66% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type of Solution

- 5.1.1. Software-Based

- 5.1.2. Hardware-Based

- 5.1.3. Professional Service

- 5.1.4. Integration

- 5.1.5. Other Types of Solution

- 5.2. Market Analysis, Insights and Forecast - by Type of Security

- 5.2.1. Network Security

- 5.2.2. Application Security

- 5.2.3. Cloud Security

- 5.2.4. Other Types of Security

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Australia and New Zealand

- 5.3.5. Latin America

- 5.3.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type of Solution

- 6. Global Cyber Security Vehicle Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type of Solution

- 6.1.1. Software-Based

- 6.1.2. Hardware-Based

- 6.1.3. Professional Service

- 6.1.4. Integration

- 6.1.5. Other Types of Solution

- 6.2. Market Analysis, Insights and Forecast - by Type of Security

- 6.2.1. Network Security

- 6.2.2. Application Security

- 6.2.3. Cloud Security

- 6.2.4. Other Types of Security

- 6.1. Market Analysis, Insights and Forecast - by Type of Solution

- 7. North America Cyber Security Vehicle Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type of Solution

- 7.1.1. Software-Based

- 7.1.2. Hardware-Based

- 7.1.3. Professional Service

- 7.1.4. Integration

- 7.1.5. Other Types of Solution

- 7.2. Market Analysis, Insights and Forecast - by Type of Security

- 7.2.1. Network Security

- 7.2.2. Application Security

- 7.2.3. Cloud Security

- 7.2.4. Other Types of Security

- 7.1. Market Analysis, Insights and Forecast - by Type of Solution

- 8. Europe Cyber Security Vehicle Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type of Solution

- 8.1.1. Software-Based

- 8.1.2. Hardware-Based

- 8.1.3. Professional Service

- 8.1.4. Integration

- 8.1.5. Other Types of Solution

- 8.2. Market Analysis, Insights and Forecast - by Type of Security

- 8.2.1. Network Security

- 8.2.2. Application Security

- 8.2.3. Cloud Security

- 8.2.4. Other Types of Security

- 8.1. Market Analysis, Insights and Forecast - by Type of Solution

- 9. Asia Cyber Security Vehicle Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type of Solution

- 9.1.1. Software-Based

- 9.1.2. Hardware-Based

- 9.1.3. Professional Service

- 9.1.4. Integration

- 9.1.5. Other Types of Solution

- 9.2. Market Analysis, Insights and Forecast - by Type of Security

- 9.2.1. Network Security

- 9.2.2. Application Security

- 9.2.3. Cloud Security

- 9.2.4. Other Types of Security

- 9.1. Market Analysis, Insights and Forecast - by Type of Solution

- 10. Australia and New Zealand Cyber Security Vehicle Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type of Solution

- 10.1.1. Software-Based

- 10.1.2. Hardware-Based

- 10.1.3. Professional Service

- 10.1.4. Integration

- 10.1.5. Other Types of Solution

- 10.2. Market Analysis, Insights and Forecast - by Type of Security

- 10.2.1. Network Security

- 10.2.2. Application Security

- 10.2.3. Cloud Security

- 10.2.4. Other Types of Security

- 10.1. Market Analysis, Insights and Forecast - by Type of Solution

- 11. Latin America Cyber Security Vehicle Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type of Solution

- 11.1.1. Software-Based

- 11.1.2. Hardware-Based

- 11.1.3. Professional Service

- 11.1.4. Integration

- 11.1.5. Other Types of Solution

- 11.2. Market Analysis, Insights and Forecast - by Type of Security

- 11.2.1. Network Security

- 11.2.2. Application Security

- 11.2.3. Cloud Security

- 11.2.4. Other Types of Security

- 11.1. Market Analysis, Insights and Forecast - by Type of Solution

- 12. Middle East and Africa Cyber Security Vehicle Market Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Type of Solution

- 12.1.1. Software-Based

- 12.1.2. Hardware-Based

- 12.1.3. Professional Service

- 12.1.4. Integration

- 12.1.5. Other Types of Solution

- 12.2. Market Analysis, Insights and Forecast - by Type of Security

- 12.2.1. Network Security

- 12.2.2. Application Security

- 12.2.3. Cloud Security

- 12.2.4. Other Types of Security

- 12.1. Market Analysis, Insights and Forecast - by Type of Solution

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Karamba Security Ltd

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Harman International Industries Inc (Samsung)

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Escrypt GmbH

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Infineon Technologies AG

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Honeywell International Inc

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Denso Corporation

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Visteon Corporation

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Delphi Automotive PLC

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 NXP Semiconductors NV

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Arilou Technologies Ltd

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Cisco Systems Inc

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Continental AG

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 Argus Cybersecurity Ltd

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.14 Secunet AG

- 13.1.14.1. Company Overview

- 13.1.14.2. Products

- 13.1.14.3. Company Financials

- 13.1.14.4. SWOT Analysis

- 13.1.1 Karamba Security Ltd

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Cyber Security Vehicle Market Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Cyber Security Vehicle Market Revenue (Million), by Type of Solution 2025 & 2033

- Figure 3: North America Cyber Security Vehicle Market Revenue Share (%), by Type of Solution 2025 & 2033

- Figure 4: North America Cyber Security Vehicle Market Revenue (Million), by Type of Security 2025 & 2033

- Figure 5: North America Cyber Security Vehicle Market Revenue Share (%), by Type of Security 2025 & 2033

- Figure 6: North America Cyber Security Vehicle Market Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Cyber Security Vehicle Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Cyber Security Vehicle Market Revenue (Million), by Type of Solution 2025 & 2033

- Figure 9: Europe Cyber Security Vehicle Market Revenue Share (%), by Type of Solution 2025 & 2033

- Figure 10: Europe Cyber Security Vehicle Market Revenue (Million), by Type of Security 2025 & 2033

- Figure 11: Europe Cyber Security Vehicle Market Revenue Share (%), by Type of Security 2025 & 2033

- Figure 12: Europe Cyber Security Vehicle Market Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Cyber Security Vehicle Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Cyber Security Vehicle Market Revenue (Million), by Type of Solution 2025 & 2033

- Figure 15: Asia Cyber Security Vehicle Market Revenue Share (%), by Type of Solution 2025 & 2033

- Figure 16: Asia Cyber Security Vehicle Market Revenue (Million), by Type of Security 2025 & 2033

- Figure 17: Asia Cyber Security Vehicle Market Revenue Share (%), by Type of Security 2025 & 2033

- Figure 18: Asia Cyber Security Vehicle Market Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Cyber Security Vehicle Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: Australia and New Zealand Cyber Security Vehicle Market Revenue (Million), by Type of Solution 2025 & 2033

- Figure 21: Australia and New Zealand Cyber Security Vehicle Market Revenue Share (%), by Type of Solution 2025 & 2033

- Figure 22: Australia and New Zealand Cyber Security Vehicle Market Revenue (Million), by Type of Security 2025 & 2033

- Figure 23: Australia and New Zealand Cyber Security Vehicle Market Revenue Share (%), by Type of Security 2025 & 2033

- Figure 24: Australia and New Zealand Cyber Security Vehicle Market Revenue (Million), by Country 2025 & 2033

- Figure 25: Australia and New Zealand Cyber Security Vehicle Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Cyber Security Vehicle Market Revenue (Million), by Type of Solution 2025 & 2033

- Figure 27: Latin America Cyber Security Vehicle Market Revenue Share (%), by Type of Solution 2025 & 2033

- Figure 28: Latin America Cyber Security Vehicle Market Revenue (Million), by Type of Security 2025 & 2033

- Figure 29: Latin America Cyber Security Vehicle Market Revenue Share (%), by Type of Security 2025 & 2033

- Figure 30: Latin America Cyber Security Vehicle Market Revenue (Million), by Country 2025 & 2033

- Figure 31: Latin America Cyber Security Vehicle Market Revenue Share (%), by Country 2025 & 2033

- Figure 32: Middle East and Africa Cyber Security Vehicle Market Revenue (Million), by Type of Solution 2025 & 2033

- Figure 33: Middle East and Africa Cyber Security Vehicle Market Revenue Share (%), by Type of Solution 2025 & 2033

- Figure 34: Middle East and Africa Cyber Security Vehicle Market Revenue (Million), by Type of Security 2025 & 2033

- Figure 35: Middle East and Africa Cyber Security Vehicle Market Revenue Share (%), by Type of Security 2025 & 2033

- Figure 36: Middle East and Africa Cyber Security Vehicle Market Revenue (Million), by Country 2025 & 2033

- Figure 37: Middle East and Africa Cyber Security Vehicle Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cyber Security Vehicle Market Revenue Million Forecast, by Type of Solution 2020 & 2033

- Table 2: Global Cyber Security Vehicle Market Revenue Million Forecast, by Type of Security 2020 & 2033

- Table 3: Global Cyber Security Vehicle Market Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Cyber Security Vehicle Market Revenue Million Forecast, by Type of Solution 2020 & 2033

- Table 5: Global Cyber Security Vehicle Market Revenue Million Forecast, by Type of Security 2020 & 2033

- Table 6: Global Cyber Security Vehicle Market Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Cyber Security Vehicle Market Revenue Million Forecast, by Type of Solution 2020 & 2033

- Table 8: Global Cyber Security Vehicle Market Revenue Million Forecast, by Type of Security 2020 & 2033

- Table 9: Global Cyber Security Vehicle Market Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Global Cyber Security Vehicle Market Revenue Million Forecast, by Type of Solution 2020 & 2033

- Table 11: Global Cyber Security Vehicle Market Revenue Million Forecast, by Type of Security 2020 & 2033

- Table 12: Global Cyber Security Vehicle Market Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Cyber Security Vehicle Market Revenue Million Forecast, by Type of Solution 2020 & 2033

- Table 14: Global Cyber Security Vehicle Market Revenue Million Forecast, by Type of Security 2020 & 2033

- Table 15: Global Cyber Security Vehicle Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Cyber Security Vehicle Market Revenue Million Forecast, by Type of Solution 2020 & 2033

- Table 17: Global Cyber Security Vehicle Market Revenue Million Forecast, by Type of Security 2020 & 2033

- Table 18: Global Cyber Security Vehicle Market Revenue Million Forecast, by Country 2020 & 2033

- Table 19: Global Cyber Security Vehicle Market Revenue Million Forecast, by Type of Solution 2020 & 2033

- Table 20: Global Cyber Security Vehicle Market Revenue Million Forecast, by Type of Security 2020 & 2033

- Table 21: Global Cyber Security Vehicle Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cyber Security Vehicle Market?

The projected CAGR is approximately 16.66%.

2. Which companies are prominent players in the Cyber Security Vehicle Market?

Key companies in the market include Karamba Security Ltd , Harman International Industries Inc (Samsung), Escrypt GmbH, Infineon Technologies AG, Honeywell International Inc, Denso Corporation, Visteon Corporation, Delphi Automotive PLC, NXP Semiconductors NV, Arilou Technologies Ltd, Cisco Systems Inc, Continental AG, Argus Cybersecurity Ltd, Secunet AG.

3. What are the main segments of the Cyber Security Vehicle Market?

The market segments include Type of Solution, Type of Security.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.06 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Remote Working and Real-time Collaboration in Organizations.

6. What are the notable trends driving market growth?

Rising Security Threats as More Technologies Get Integrated Into Cars is Expected to Drive the Market.

7. Are there any restraints impacting market growth?

Lack of Awareness and Digital Resources in Developing Countries.

8. Can you provide examples of recent developments in the market?

July 2022: NoBug Consulting SRL (Romania) and NoBug d.o.o. were acquired by Infineon Technologies (Serbia). NoBug, founded in 1998, is a privately held engineering firm that provides verification and design services for all digital functions of semiconductor products. Infineon is enhancing its Connected Secure Systems (CSS) Division's capacity to work on complex IoT product development. Thus, Infineon is laying the groundwork for the future IoT infrastructure, enabling cybersecurity, AI, machine learning, and robust connections.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cyber Security Vehicle Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cyber Security Vehicle Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cyber Security Vehicle Market?

To stay informed about further developments, trends, and reports in the Cyber Security Vehicle Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence