Key Insights

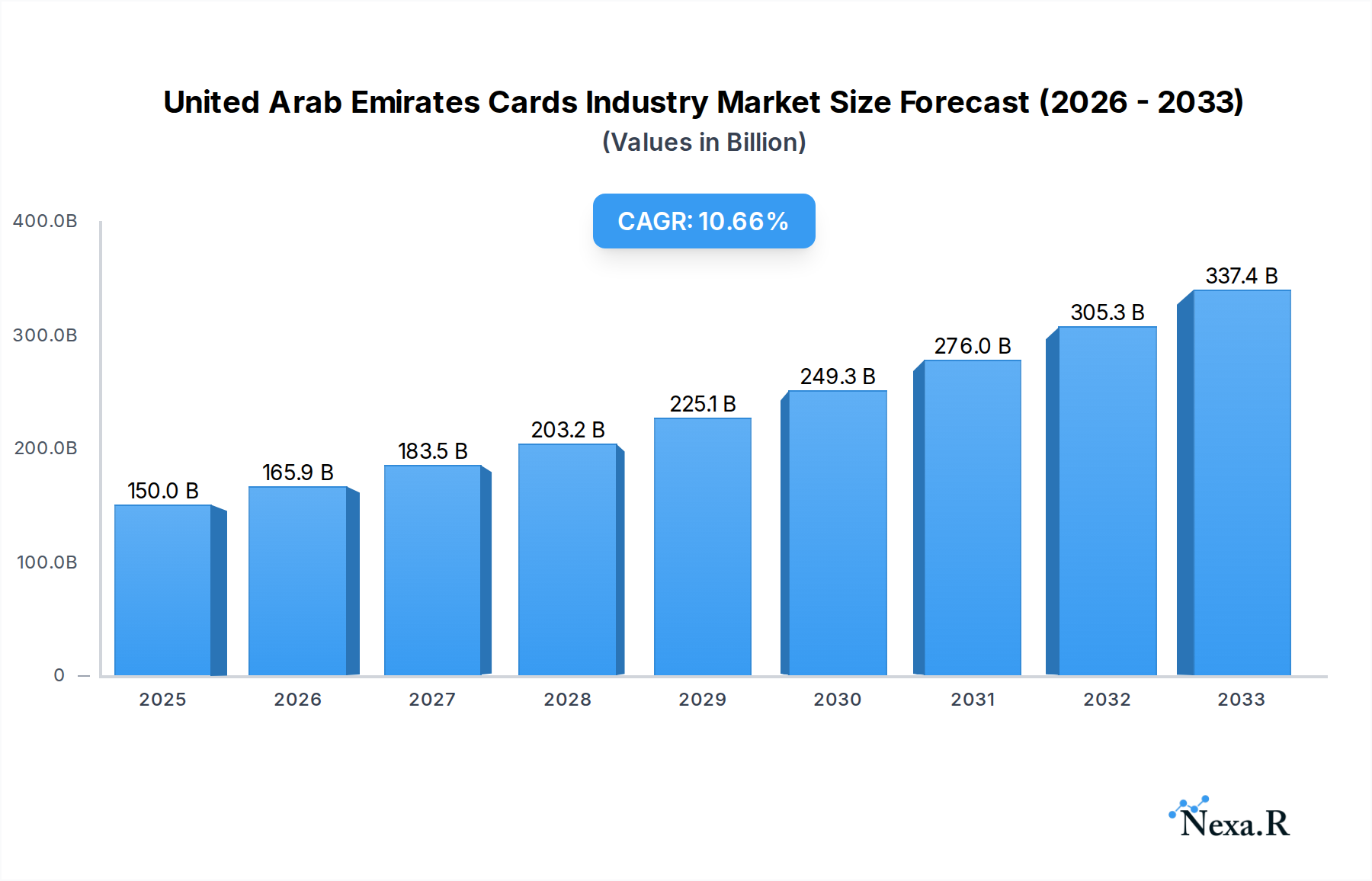

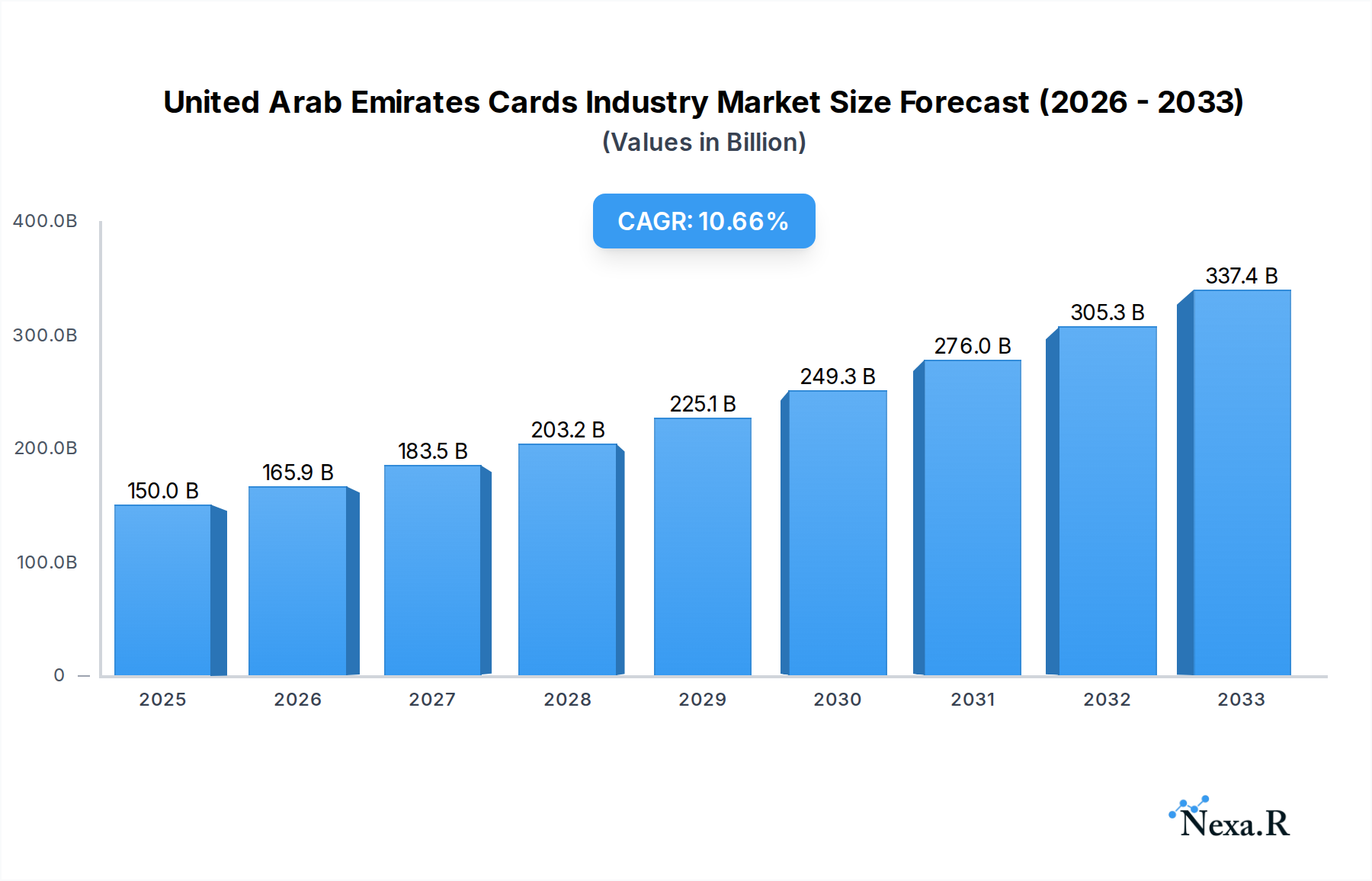

The United Arab Emirates (UAE) Cards Industry is poised for significant expansion, projected to reach a market size of $150 billion in 2025. This robust growth is fueled by a compelling CAGR of 10.6%, indicating sustained upward momentum over the forecast period of 2025-2033. A primary driver for this surge is the increasing adoption of digital payment methods, propelled by the government's vision for a cashless economy and initiatives like the UAE's National Digital Transformation Strategy. The burgeoning e-commerce sector and the continuous influx of tourists and expatriates further bolster demand for card-based transactions across various touchpoints. Technological advancements, including the widespread integration of contactless payment options and the growing popularity of digital wallets, are transforming the consumer payment experience, making it more seamless and secure.

United Arab Emirates Cards Industry Market Size (In Billion)

The market is segmented into distinct payment modes, with Point of Sale (POS) transactions, encompassing card payments, digital wallets, and cash, dominating current activity. However, online sales are exhibiting a steeper growth trajectory, driven by the convenience and expanding reach of e-commerce platforms. Key end-user industries such as retail and entertainment are experiencing a heightened reliance on card transactions, while healthcare and hospitality are rapidly adopting these methods for improved customer experience and operational efficiency. Despite the overwhelming shift towards digital, the "Others" category for both POS and online sales suggests emerging payment avenues that warrant close monitoring. Industry titans like Telr Pte Ltd, 2Checkout com Inc, and Stripe Inc are at the forefront, innovating and expanding their services to cater to this dynamic market, actively shaping the future of payments in the UAE.

United Arab Emirates Cards Industry Company Market Share

United Arab Emirates Cards Industry Market Dynamics & Structure

The United Arab Emirates (UAE) cards industry is characterized by a dynamic landscape shaped by rapid technological advancements, robust government initiatives promoting digital transformation, and evolving consumer preferences for convenient and secure payment solutions. Market concentration is moderately fragmented, with key players vying for market share through innovative product offerings and strategic partnerships. The proliferation of fintech startups, alongside established financial institutions, fuels intense competition and drives continuous innovation.

- Technological Innovation Drivers: The surge in contactless payments, the adoption of digital wallets, and the integration of AI and machine learning for fraud detection are primary technological drivers. The development of advanced payment gateways and the increasing use of QR code payments are also significant.

- Regulatory Frameworks: A supportive regulatory environment, with the Central Bank of the UAE spearheading initiatives for digital payments and cybersecurity, fosters trust and adoption. Stringent data protection laws and regulations governing card security further enhance the industry's integrity.

- Competitive Product Substitutes: While credit and debit cards remain dominant, the UAE market sees a growing presence of alternative payment methods. These include digital wallets like Apple Pay and Google Pay, prepaid cards, and emerging buy-now-pay-later (BNPL) solutions, all competing for consumer spend.

- End-User Demographics: The UAE's diverse and digitally savvy population, comprising a significant expatriate community, readily embraces new payment technologies. A young demographic with high smartphone penetration and a strong inclination towards online shopping further bolsters the cards industry.

- M&A Trends: Mergers and acquisitions are driven by the desire to consolidate market presence, acquire new technologies, and expand service offerings. Strategic alliances and partnerships, such as the one between Nayax Ltd and Network International, are also prevalent, aimed at enhancing reach and capabilities across the Middle East and Africa (MEA) region. The market is projected to reach USD 12.5 billion by 2033, with a CAGR of 8.2% during the forecast period.

United Arab Emirates Cards Industry Growth Trends & Insights

The United Arab Emirates cards industry is poised for substantial expansion, driven by a confluence of factors including a digitally empowered consumer base, supportive government digitalization agendas, and an increasing volume of both online and in-store transactions. The study period from 2019 to 2033, with a base year of 2025, encapsulates a transformative era for payment methods in the UAE. By 2025, the market is estimated to reach USD 7.1 billion, demonstrating a robust growth trajectory. The forecast period, 2025–2033, is expected to witness a Compound Annual Growth Rate (CAGR) of 8.2%, propelling the market to an estimated USD 12.5 billion by the end of the forecast horizon. This impressive growth is underpinned by several key trends.

The accelerating adoption of contactless payment technologies has significantly reshaped consumer behavior. As consumers increasingly prioritize convenience and speed, card-present transactions are shifting towards tap-to-pay functionalities facilitated by both physical cards and mobile wallets. The historical period (2019–2024) saw a nascent but rapid embrace of these technologies, laying the groundwork for the accelerated adoption witnessed in the base and forecast years. Digital wallets, in particular, have experienced phenomenal growth, integrating seamlessly with loyalty programs and offering personalized discounts, thereby encouraging higher transaction volumes.

Technological disruptions are continuously redefining the payment ecosystem. Innovations in blockchain technology, while still in early stages for widespread card application, hold promise for enhanced security and reduced transaction costs. Furthermore, the integration of Artificial Intelligence (AI) for personalized customer experiences and sophisticated fraud detection mechanisms is becoming standard practice among leading payment providers. The increasing penetration of smartphones and the growth of e-commerce platforms are directly correlated with the rise in online card transactions. As more businesses, both large and small, establish their online presence, the demand for secure and efficient online payment gateways, such as those offered by Telr Pte Ltd, 2Checkout com Inc, and Stripe Inc, continues to soar.

Consumer behavior is also undergoing a significant shift. There is a growing preference for seamless, omnichannel payment experiences that allow for fluid transitions between online and offline purchasing. Loyalty programs, often integrated with card services, play a crucial role in driving repeat business and customer retention. The younger demographic, in particular, is highly receptive to new payment methods and digital innovations, acting as early adopters and trendsetters. The increasing disposable income and a strong propensity for spending on retail, entertainment, and hospitality sectors further contribute to the sustained demand for card-based payment solutions. The UAE's strategic vision for becoming a global hub for innovation and digital commerce provides a fertile ground for the continued evolution and expansion of its cards industry.

Dominant Regions, Countries, or Segments in United Arab Emirates Cards Industry

The United Arab Emirates cards industry exhibits a pronounced dominance within specific segments and end-user industries, driven by economic policies, robust infrastructure, and evolving consumer behavior. The Point of Sale (POS) segment, particularly Card Pay, is the primary engine of growth, accounting for a substantial market share. This dominance is fueled by the widespread adoption of credit and debit cards across all strata of the economy, from large retail chains to smaller merchants. The UAE's strategic focus on developing a cashless society, coupled with extensive merchant acceptance networks established by companies like Network International, has propelled card payments to the forefront.

- Card Pay (Point of Sale): This sub-segment is the largest driver, benefiting from continuous technological upgrades in POS terminals that support contactless payments, EMV chip technology, and mobile payment integrations. The high penetration of physical card usage in traditional retail environments and the increasing acceptance of contactless transactions have cemented its leading position. Market share for Card Pay at POS is estimated to be 55% of the total POS transactions.

- Digital Wallet (includes Mobile Wallets): While still evolving, Digital Wallets are rapidly gaining traction, especially within younger demographics and for online transactions. Their convenience and integration with loyalty programs are key drivers. This segment is projected to experience the highest CAGR, estimated at 15% over the forecast period, and is expected to capture 30% of POS transactions by 2033.

- Retail End-User Industry: The retail sector is overwhelmingly the largest consumer of card payment services. This encompasses fashion, electronics, groceries, and luxury goods. The UAE's status as a major global retail destination, attracting millions of tourists annually, significantly boosts card transaction volumes within this sector. The retail segment is estimated to account for 45% of all card transactions.

- Hospitality End-User Industry: Hotels, restaurants, and tourism-related services also represent a significant portion of card usage. The affluent population and high tourist inflow contribute to substantial spending in this sector, with card payments being the preferred mode of settlement for convenience and security. This segment holds an estimated 20% market share.

The Online Sale segment, while still growing, is currently secondary to POS transactions but exhibits immense potential. The proliferation of e-commerce platforms, facilitated by companies like Amazon Payments Inc and Infibeam Avenues Limited (CC Avenues), has led to a surge in online card payments. The increasing ease of online shopping, coupled with secure payment gateways, is driving this segment's growth. The UAE government's continued investment in digital infrastructure and its ambition to become a global e-commerce hub further underscore the burgeoning importance of online card transactions.

Geographically, the emirates of Dubai and Abu Dhabi are the dominant regions, reflecting their status as economic powerhouses and major tourist destinations. These emirates have the highest concentration of retail outlets, hotels, and a technologically adept population, leading to the highest card transaction volumes. The proactive adoption of new payment technologies in these leading emirates often sets the trend for the rest of the country.

United Arab Emirates Cards Industry Product Landscape

The UAE cards industry is witnessing a vibrant evolution in its product landscape, driven by a relentless pursuit of enhanced security, convenience, and personalized user experiences. Innovations are primarily centered around the development of advanced contactless payment solutions, the integration of biometric authentication for heightened security, and the creation of smart cards with embedded functionalities. Digital wallets are no longer mere payment tools but have transformed into comprehensive lifestyle apps, offering rewards, loyalty programs, and seamless integration with e-commerce platforms. The introduction of virtual cards and tokenization technology by companies like PayTabs LLC and HyperPay Inc is further bolstering transaction security and privacy. Performance metrics are increasingly evaluated on transaction speed, fraud detection rates, and customer satisfaction, with an upward trend in contactless transaction adoption and a decline in traditional chip-and-PIN usage where contactless is available.

Key Drivers, Barriers & Challenges in United Arab Emirates Cards Industry

The United Arab Emirates cards industry is propelled by several key drivers, primarily centered around the nation's robust digital transformation agenda and a tech-savvy population.

- Drivers:

- Government Initiatives: Strong government support for a cashless economy through initiatives like the UAE Vision 2030 and the Smart Dubai initiative.

- High Smartphone Penetration: Widespread availability and affordability of smartphones facilitate mobile payments and digital wallet adoption.

- Growing E-commerce Sector: The burgeoning online retail market necessitates secure and efficient digital payment solutions.

- Tourism Hub: The UAE's status as a global tourist destination drives a high volume of card transactions, especially in retail and hospitality.

- Technological Advancements: Continuous innovation in payment technologies, including contactless, NFC, and tokenization, enhances user experience and security.

However, the industry faces significant barriers and challenges that could temper its growth.

- Barriers & Challenges:

- Cybersecurity Threats: The increasing sophistication of cyberattacks poses a constant threat to data security and consumer trust.

- Regulatory Compliance: Navigating evolving data privacy and financial regulations requires continuous investment and adaptation.

- Digital Divide: While penetration is high, ensuring access and digital literacy for all segments of the population remains a challenge.

- Cash Reliance in Certain Sectors: Despite digital push, some micro-businesses and informal sectors still prefer cash, posing a barrier to complete cashless adoption.

- Competition from Fintechs: The rapidly growing fintech sector, while innovative, also intensifies competition and can lead to market fragmentation.

Emerging Opportunities in United Arab Emirates Cards Industry

Emerging opportunities in the UAE cards industry lie in the untapped potential of niche markets and the innovative application of existing technologies. The burgeoning SME sector presents a significant opportunity for tailored payment solutions and financial inclusion. Furthermore, the increasing adoption of Buy Now, Pay Later (BNPL) services, especially among younger consumers, indicates a strong demand for flexible payment options, which can be integrated with existing card infrastructures. The expansion of cross-border e-commerce also offers a vast untapped market for payment providers.

Growth Accelerators in the United Arab Emirates Cards Industry Industry

Several catalysts are accelerating the growth of the UAE cards industry, notably the continued strategic partnerships between financial institutions and technology providers, fostering innovation and expanding service reach. The ongoing investment in robust digital payment infrastructure, including the expansion of secure and fast transaction networks, is crucial. Furthermore, the UAE's consistent efforts to attract foreign direct investment in the fintech sector, coupled with a proactive approach to regulatory sandboxes for emerging payment technologies, are significant growth accelerators.

Key Players Shaping the United Arab Emirates Cards Industry Market

- Telr Pte Ltd

- 2Checkout com Inc

- PayTabs LLC

- Amazon Payments Inc

- HyperPay Inc

- PayCaps in

- Stripe Inc

- Infibeam Avenues Limited (CC Avenues)

- Checkout Ltd

- Cashu FZ LLC

- Network International

Notable Milestones in United Arab Emirates Cards Industry Sector

- May 2022: Nayax Ltd partnered with Network International, expanding its reach and customer base in the MEA region, enhancing digital commerce enablement.

- February 2022: Apple Inc announced plans to open its fourth store in the UAE on Al Maryah Island, Abu Dhabi, reinforcing its presence and potentially driving the payment market.

In-Depth United Arab Emirates Cards Industry Market Outlook

The UAE cards industry is set for sustained high growth, driven by a convergence of digital-first consumer habits, supportive government policies promoting innovation, and a rapidly expanding e-commerce ecosystem. The market's outlook is exceptionally positive, fueled by continued investment in cutting-edge payment technologies like AI-powered fraud detection and blockchain-based security solutions. Strategic collaborations, such as those observed between payment enablers and regional infrastructure providers, will further consolidate market positions and expand service offerings, ensuring the UAE remains a leading hub for digital payments in the MENA region.

United Arab Emirates Cards Industry Segmentation

-

1. Mode of Payment

-

1.1. Point of Sale

- 1.1.1. Card Pay

- 1.1.2. Digital Wallet (includes Mobile Wallets)

- 1.1.3. Cash

- 1.1.4. Others

-

1.2. Online Sale

- 1.2.1. Others (

-

1.1. Point of Sale

-

2. End-user Industry

- 2.1. Retail

- 2.2. Entertainment

- 2.3. Healthcare

- 2.4. Hospitality

- 2.5. Other End-user Industries

United Arab Emirates Cards Industry Segmentation By Geography

- 1. United Arab Emirates

United Arab Emirates Cards Industry Regional Market Share

Geographic Coverage of United Arab Emirates Cards Industry

United Arab Emirates Cards Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 5.1.1. Point of Sale

- 5.1.1.1. Card Pay

- 5.1.1.2. Digital Wallet (includes Mobile Wallets)

- 5.1.1.3. Cash

- 5.1.1.4. Others

- 5.1.2. Online Sale

- 5.1.2.1. Others (

- 5.1.1. Point of Sale

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Retail

- 5.2.2. Entertainment

- 5.2.3. Healthcare

- 5.2.4. Hospitality

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Arab Emirates

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6. United Arab Emirates Cards Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6.1.1. Point of Sale

- 6.1.1.1. Card Pay

- 6.1.1.2. Digital Wallet (includes Mobile Wallets)

- 6.1.1.3. Cash

- 6.1.1.4. Others

- 6.1.2. Online Sale

- 6.1.2.1. Others (

- 6.1.1. Point of Sale

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Retail

- 6.2.2. Entertainment

- 6.2.3. Healthcare

- 6.2.4. Hospitality

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Telr Pte Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 2Checkout com Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 PayTabs LLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Amazon Payments Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 HyperPay Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 PayCaps in

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Stripe Inc *List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Infibeam Avenues Limited (CC Avenues)

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Checkout Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Cashu FZ LLC

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Telr Pte Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United Arab Emirates Cards Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: United Arab Emirates Cards Industry Share (%) by Company 2025

List of Tables

- Table 1: United Arab Emirates Cards Industry Revenue billion Forecast, by Mode of Payment 2020 & 2033

- Table 2: United Arab Emirates Cards Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: United Arab Emirates Cards Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: United Arab Emirates Cards Industry Revenue billion Forecast, by Mode of Payment 2020 & 2033

- Table 5: United Arab Emirates Cards Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: United Arab Emirates Cards Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United Arab Emirates Cards Industry?

The projected CAGR is approximately 10.6%.

2. Which companies are prominent players in the United Arab Emirates Cards Industry?

Key companies in the market include Telr Pte Ltd, 2Checkout com Inc, PayTabs LLC, Amazon Payments Inc, HyperPay Inc, PayCaps in, Stripe Inc *List Not Exhaustive, Infibeam Avenues Limited (CC Avenues), Checkout Ltd, Cashu FZ LLC.

3. What are the main segments of the United Arab Emirates Cards Industry?

The market segments include Mode of Payment, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 150 billion as of 2022.

5. What are some drivers contributing to market growth?

High Proliferation of E-commerce. including the rise of m-commerce and cross-border e-commerce supported by the increase in purchasing power; Enablement Programs by Key Retailers and Government encouraging digitization of the market; Growth of Real-time Payments. especially Buy Now Pay Later in the country.

6. What are the notable trends driving market growth?

Significant Growth in Payment is Expected due to Digital Transformation.

7. Are there any restraints impacting market growth?

Talent Shortages in Specific Technologies.

8. Can you provide examples of recent developments in the market?

In May 2022 - Nayax Ltd, a commerce enablement and payments platform, announced a partnership with Network International, the provider of digital commerce across the Middle-East and Africa (MEA). This partnership will help the company to expand its business and customer base in the MEA region.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United Arab Emirates Cards Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United Arab Emirates Cards Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United Arab Emirates Cards Industry?

To stay informed about further developments, trends, and reports in the United Arab Emirates Cards Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence