Key Insights

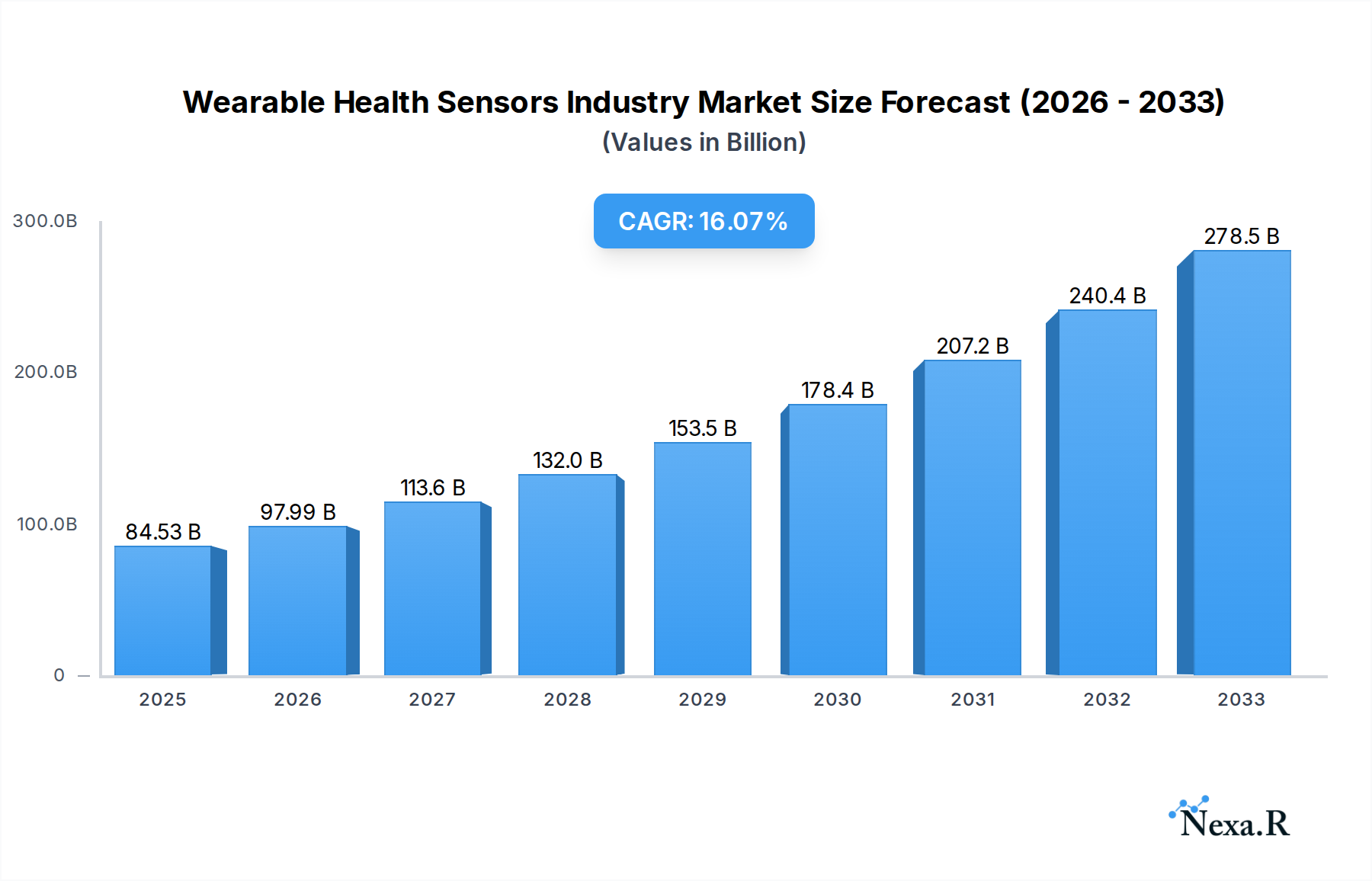

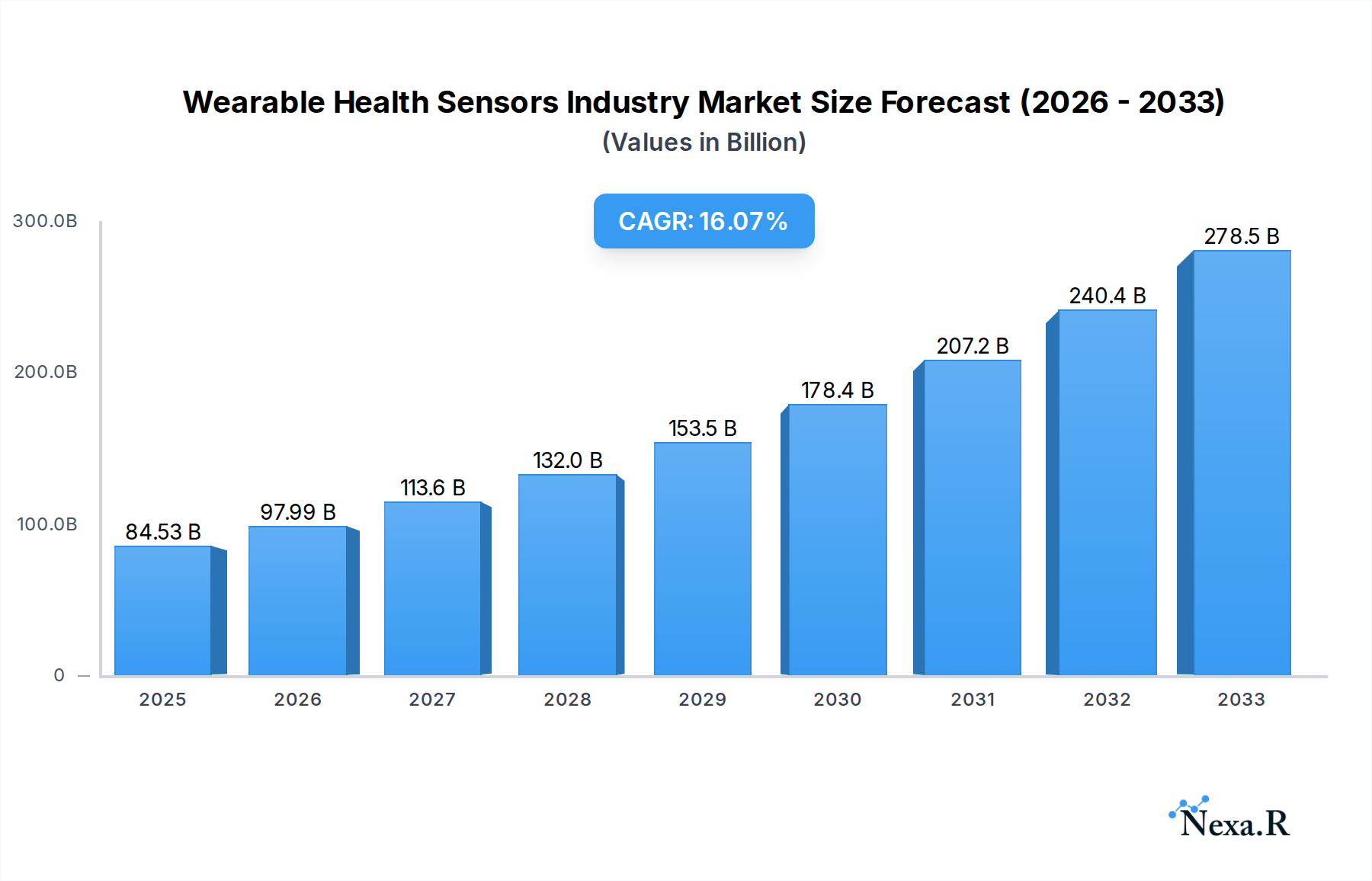

The Wearable Health Sensors Industry is poised for significant expansion, with the market size estimated at $84.53 billion in 2025. This robust growth is underpinned by an impressive compound annual growth rate (CAGR) of 15.9% projected over the forecast period. The primary drivers fueling this surge include the escalating demand for proactive and personalized healthcare solutions, a growing awareness among consumers regarding preventative wellness, and the increasing adoption of smart devices equipped with sophisticated sensing capabilities. Technological advancements, particularly in miniaturization, power efficiency, and data accuracy of sensors, are continuously enabling the development of more sophisticated and user-friendly wearable health devices. The integration of artificial intelligence and machine learning further enhances the analytical power of these devices, allowing for deeper insights into individual health metrics and the early detection of potential health issues. This makes wearable health sensors indispensable tools in the modern healthcare ecosystem.

Wearable Health Sensors Industry Market Size (In Billion)

The market's segmentation reveals a dynamic landscape. Pressure sensors, temperature sensors, and position sensors are key technological components driving innovation, with diverse applications spanning the healthcare, consumer electronics, and sports/fitness industries. The healthcare sector, in particular, is witnessing a paradigm shift towards remote patient monitoring, chronic disease management, and post-operative care, all heavily reliant on accurate and continuous data from wearable sensors. Similarly, the burgeoning consumer electronics market integrates these sensors into a wide array of devices, from smartwatches and fitness trackers to advanced personal monitoring systems. While the market is experiencing tremendous growth, challenges such as data privacy concerns, regulatory hurdles, and the need for robust interoperability standards across different devices and platforms need to be strategically addressed to ensure sustained and widespread adoption. The competitive landscape features key players like Infineon Technologies AG, STMicroelectronics Inc., and TE Connectivity Ltd., among others, who are continuously innovating to capture market share.

Wearable Health Sensors Industry Company Market Share

This in-depth report provides a definitive outlook on the wearable health sensors market, a rapidly expanding sector driven by technological advancements and increasing consumer demand for proactive health monitoring. Explore the intricate dynamics, growth trajectories, and competitive landscape of this critical industry, covering the global wearable health sensors market size, wearable sensor technology, medical wearables, and health tracking devices. With a comprehensive study period spanning from 2019 to 2033, this report offers actionable insights for stakeholders seeking to capitalize on the burgeoning opportunities in connected health devices and remote patient monitoring.

Wearable Health Sensors Industry Market Dynamics & Structure

The wearable health sensors industry exhibits a dynamic and evolving market structure, characterized by intense technological innovation and a growing emphasis on data-driven healthcare solutions. Market concentration is moderate, with key players investing heavily in R&D to develop miniaturized, power-efficient, and highly accurate sensors. Technological innovation serves as a primary driver, fueled by advancements in materials science, microelectronics, and artificial intelligence, enabling novel applications in disease prevention and management. Regulatory frameworks, particularly those set by the FDA and EMA, play a crucial role in shaping product development and market access, ensuring the safety and efficacy of wearable medical devices. Competitive product substitutes are emerging, ranging from traditional medical equipment to sophisticated consumer-grade wearables offering basic health metrics. End-user demographics are diversifying, with a significant shift towards proactive health management across all age groups, particularly the elderly and individuals with chronic conditions. Mergers and acquisitions (M&A) are a prominent trend, with larger companies acquiring innovative startups to enhance their product portfolios and gain access to specialized technologies. For instance, the acquisition of Bend Labs by Nitto Denko Corporation signifies a strategic move to integrate advanced sensor capabilities into next-generation products.

- Market Concentration: Moderate, with a mix of large established players and agile startups.

- Technological Innovation Drivers: Miniaturization, power efficiency, AI integration, advanced material science.

- Regulatory Frameworks: Crucial for product approval and market entry (e.g., FDA, EMA).

- Competitive Product Substitutes: Traditional medical devices, advanced consumer electronics.

- End-User Demographics: Expanding to include elderly populations, chronic disease patients, and health-conscious individuals.

- M&A Trends: Active, driven by the pursuit of innovative technologies and market expansion.

Wearable Health Sensors Industry Growth Trends & Insights

The wearable health sensors market is poised for substantial growth, projected to reach xx billion units by 2033, with a compound annual growth rate (CAGR) of xx% from the base year 2025. This robust expansion is fueled by an accelerating adoption rate of health monitoring wearables across both the healthcare and consumer electronics sectors. Technological disruptions, such as the development of highly sensitive biosensors and advanced connectivity protocols, are enabling more sophisticated health tracking capabilities. Consumer behavior is shifting towards a more proactive and preventative approach to health, with individuals increasingly seeking tools to monitor their well-being and manage chronic conditions. The integration of AI and machine learning algorithms into wearable devices is further enhancing their analytical power, providing personalized health insights and early disease detection. The market penetration of smart health wearables is expected to rise significantly as accessibility improves and awareness of their benefits grows. Key trends include the increasing demand for continuous glucose monitoring (CGM) devices, advanced cardiovascular monitoring systems, and non-invasive diagnostic tools. The evolving digital health ecosystem, encompassing telemedicine and remote patient monitoring platforms, acts as a significant growth accelerator.

Dominant Regions, Countries, or Segments in Wearable Health Sensors Industry

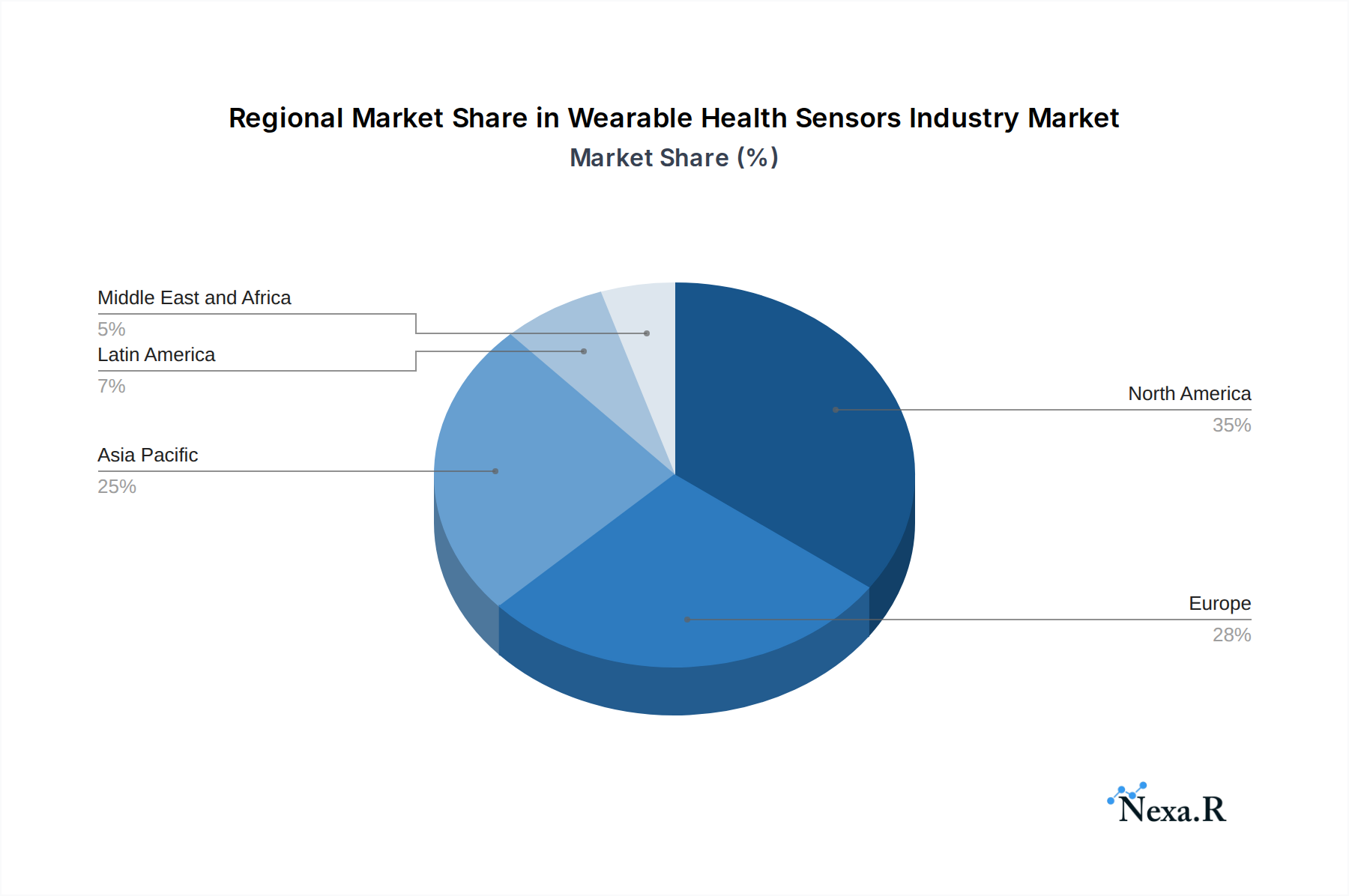

The wearable health sensors industry is experiencing dominant growth driven by specific regions, countries, and segments. North America, particularly the United States, leads the market due to its advanced healthcare infrastructure, high disposable income, and early adoption of innovative technologies. The healthcare end-user industry is a significant growth driver, with an increasing focus on remote patient monitoring, chronic disease management, and post-operative care. Within this segment, the demand for continuous monitoring solutions for conditions like heart failure, diabetes, and respiratory illnesses is surging. The consumer electronics and sports/fitness segments also contribute substantially, with a rising awareness of preventive healthcare and the desire for personalized fitness tracking.

- Leading Region: North America, driven by strong R&D investment and widespread adoption.

- Dominant Country: United States, with robust healthcare policies and a tech-savvy population.

- Key End User Industry: Healthcare, due to the growing adoption of remote patient monitoring and chronic disease management solutions.

- Type Segment Driving Growth: While all sensor types are important, pressure sensors are seeing increased demand for applications like blood pressure monitoring and fall detection, while temperature sensors are crucial for fever detection and overall health status.

- Market Share: The healthcare segment holds the largest market share, estimated at xx% in 2025, followed by consumer electronics at xx%.

- Growth Potential: Emerging economies in Asia-Pacific are exhibiting high growth potential due to increasing healthcare expenditure and a growing middle class.

Wearable Health Sensors Industry Product Landscape

The product landscape of the wearable health sensors industry is characterized by a relentless pursuit of innovation, miniaturization, and enhanced functionality. Companies are developing advanced wearable sensor technology capable of measuring a wider range of physiological parameters with greater accuracy. Innovations include flexible and stretchable sensors that integrate seamlessly into clothing and accessories, enhancing user comfort and compliance. Applications are expanding beyond basic activity tracking to encompass sophisticated diagnostic and therapeutic functions, such as continuous glucose monitoring, real-time ECG analysis, and non-invasive blood pressure measurement. Performance metrics are constantly being pushed, with improvements in battery life, data transmission speed, and signal-to-noise ratio. Unique selling propositions often lie in the development of multi-functional sensors capable of simultaneous data acquisition from various physiological indicators, offering a holistic view of an individual's health.

Key Drivers, Barriers & Challenges in Wearable Health Sensors Industry

Key Drivers:

- Rising prevalence of chronic diseases: Increasing need for continuous monitoring and early detection.

- Growing consumer demand for proactive health management: Shift towards preventative healthcare and wellness.

- Technological advancements in sensor technology: Miniaturization, accuracy, and power efficiency.

- Government initiatives and healthcare reforms: Promoting digital health and remote patient monitoring.

- Increasing adoption of smartphones and IoT devices: Enabling seamless data integration and connectivity.

Barriers & Challenges:

- Data privacy and security concerns: Protecting sensitive health information is paramount.

- Regulatory hurdles and compliance: Obtaining approvals for medical-grade devices can be time-consuming and costly.

- High cost of advanced wearable devices: Limiting accessibility for certain demographic segments.

- Accuracy and reliability issues: Ensuring consistent and precise measurements in real-world conditions.

- User adoption and adherence: Overcoming challenges related to comfort, usability, and perceived value.

- Interoperability and standardization: Ensuring seamless data exchange between different devices and platforms.

- Supply chain disruptions: Global events can impact the availability of raw materials and components.

Emerging Opportunities in Wearable Health Sensors Industry

Emerging opportunities in the wearable health sensors industry lie in untapped markets and innovative applications. The development of wearable biosensors for non-invasive detection of biomarkers for diseases like cancer and neurological disorders presents a significant frontier. The integration of AI-powered predictive analytics into wearable devices offers the potential for personalized interventions and early disease forecasting. The expansion of wearable health technology into mental health monitoring, sleep analysis, and stress management represents another burgeoning area. Furthermore, the application of these sensors in remote areas and developing countries, through affordable and robust solutions, can address significant healthcare gaps. The increasing focus on personalized medicine and preventative care will drive demand for highly customized wearable solutions tailored to individual needs.

Growth Accelerators in the Wearable Health Sensors Industry Industry

Several catalysts are accelerating the growth of the wearable health sensors industry. Technological breakthroughs in materials science, such as the development of flexible and biocompatible substrates, are enabling more comfortable and integrated wearable designs. Strategic partnerships between technology companies, healthcare providers, and pharmaceutical firms are fostering innovation and accelerating market penetration. For instance, collaborations aimed at developing integrated diagnostic and therapeutic solutions are gaining traction. Market expansion strategies, including the penetration of emerging economies and the development of specialized wearable devices for specific patient populations, are further propelling growth. The increasing availability of cloud-based platforms for data storage, analysis, and sharing is also a key accelerator, facilitating the development of comprehensive digital health ecosystems.

Key Players Shaping the Wearable Health Sensors Industry Market

- Infineon Technologies AG

- mCube Inc

- STMicroelectronics Inc

- TE Connectivity Ltd

- Texas Instruments Incorporated

- Arm Limited

- TDK Corporation

- Fraunhofer IIS

- Analog Devices Inc

- Maxim Integrated Products Inc

Notable Milestones in Wearable Health Sensors Industry Sector

- June 2022: Nitto Denko Corporation agreed to acquire Bend Labs, Inc. Bend merged into the Nitto Group to form Nitto Bend Technologies, combining Bend's sensor device technologies with Nitto's strengths for developing next-generation technologies, products, and new businesses utilizing sensor-acquired data.

- February 2022: Abbott announced that the US FDA approved an expanded indication for its Cardio MEMS HF System to support the care of people with heart failure. This expansion made an additional 1.2 million US patients eligible for advanced monitoring with Abbott's sensor, offering an early warning system to protect against worsening heart failure.

In-Depth Wearable Health Sensors Industry Market Outlook

The future outlook for the wearable health sensors industry is exceptionally bright, driven by continued technological innovation and expanding market applications. Growth accelerators such as the relentless pursuit of miniaturization and enhanced sensor accuracy will unlock new diagnostic capabilities. Strategic partnerships between technology developers and healthcare providers will further integrate wearable data into clinical workflows, promoting seamless remote patient monitoring and personalized treatment plans. The increasing focus on preventative healthcare and the growing demand for data-driven health insights will fuel the expansion of the wearable health technology market. Opportunities in emerging applications like mental health tracking and non-invasive disease detection present significant avenues for future growth, ensuring the connected health devices market remains a dynamic and evolving sector.

Wearable Health Sensors Industry Segmentation

-

1. Type

- 1.1. Pressure Sensor

- 1.2. Temperature Sensor

- 1.3. Position Sensor

- 1.4. Other Types

-

2. End User Industry

- 2.1. Healthcare

- 2.2. Consumer Electronic

- 2.3. Sports/Fitness

- 2.4. Other End User Industries

Wearable Health Sensors Industry Segmentation By Geography

- 1. Asia Pacific

- 2. Europe

- 3. Latin America

- 4. Middle East and Africa

- 5. North America

Wearable Health Sensors Industry Regional Market Share

Geographic Coverage of Wearable Health Sensors Industry

Wearable Health Sensors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Pressure Sensor

- 5.1.2. Temperature Sensor

- 5.1.3. Position Sensor

- 5.1.4. Other Types

- 5.2. Market Analysis, Insights and Forecast - by End User Industry

- 5.2.1. Healthcare

- 5.2.2. Consumer Electronic

- 5.2.3. Sports/Fitness

- 5.2.4. Other End User Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. Europe

- 5.3.3. Latin America

- 5.3.4. Middle East and Africa

- 5.3.5. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Wearable Health Sensors Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Pressure Sensor

- 6.1.2. Temperature Sensor

- 6.1.3. Position Sensor

- 6.1.4. Other Types

- 6.2. Market Analysis, Insights and Forecast - by End User Industry

- 6.2.1. Healthcare

- 6.2.2. Consumer Electronic

- 6.2.3. Sports/Fitness

- 6.2.4. Other End User Industries

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Asia Pacific Wearable Health Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Pressure Sensor

- 7.1.2. Temperature Sensor

- 7.1.3. Position Sensor

- 7.1.4. Other Types

- 7.2. Market Analysis, Insights and Forecast - by End User Industry

- 7.2.1. Healthcare

- 7.2.2. Consumer Electronic

- 7.2.3. Sports/Fitness

- 7.2.4. Other End User Industries

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Wearable Health Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Pressure Sensor

- 8.1.2. Temperature Sensor

- 8.1.3. Position Sensor

- 8.1.4. Other Types

- 8.2. Market Analysis, Insights and Forecast - by End User Industry

- 8.2.1. Healthcare

- 8.2.2. Consumer Electronic

- 8.2.3. Sports/Fitness

- 8.2.4. Other End User Industries

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Latin America Wearable Health Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Pressure Sensor

- 9.1.2. Temperature Sensor

- 9.1.3. Position Sensor

- 9.1.4. Other Types

- 9.2. Market Analysis, Insights and Forecast - by End User Industry

- 9.2.1. Healthcare

- 9.2.2. Consumer Electronic

- 9.2.3. Sports/Fitness

- 9.2.4. Other End User Industries

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East and Africa Wearable Health Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Pressure Sensor

- 10.1.2. Temperature Sensor

- 10.1.3. Position Sensor

- 10.1.4. Other Types

- 10.2. Market Analysis, Insights and Forecast - by End User Industry

- 10.2.1. Healthcare

- 10.2.2. Consumer Electronic

- 10.2.3. Sports/Fitness

- 10.2.4. Other End User Industries

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. North America Wearable Health Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Pressure Sensor

- 11.1.2. Temperature Sensor

- 11.1.3. Position Sensor

- 11.1.4. Other Types

- 11.2. Market Analysis, Insights and Forecast - by End User Industry

- 11.2.1. Healthcare

- 11.2.2. Consumer Electronic

- 11.2.3. Sports/Fitness

- 11.2.4. Other End User Industries

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Infineon Technologies AG

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 mCube Inc *List Not Exhaustive

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 STMicroelectronics Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 TE Connectivity Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Texas Instruments Incorporated

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Arm Limited

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 TDK Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Fraunhofer IIS

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Analog Devices Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Maxim Integrated Products Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Infineon Technologies AG

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Wearable Health Sensors Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Wearable Health Sensors Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: Asia Pacific Wearable Health Sensors Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: Asia Pacific Wearable Health Sensors Industry Revenue (billion), by End User Industry 2025 & 2033

- Figure 5: Asia Pacific Wearable Health Sensors Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 6: Asia Pacific Wearable Health Sensors Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: Asia Pacific Wearable Health Sensors Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Wearable Health Sensors Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: Europe Wearable Health Sensors Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Europe Wearable Health Sensors Industry Revenue (billion), by End User Industry 2025 & 2033

- Figure 11: Europe Wearable Health Sensors Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 12: Europe Wearable Health Sensors Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Wearable Health Sensors Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Latin America Wearable Health Sensors Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Latin America Wearable Health Sensors Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Latin America Wearable Health Sensors Industry Revenue (billion), by End User Industry 2025 & 2033

- Figure 17: Latin America Wearable Health Sensors Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 18: Latin America Wearable Health Sensors Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Latin America Wearable Health Sensors Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Wearable Health Sensors Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Middle East and Africa Wearable Health Sensors Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Middle East and Africa Wearable Health Sensors Industry Revenue (billion), by End User Industry 2025 & 2033

- Figure 23: Middle East and Africa Wearable Health Sensors Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 24: Middle East and Africa Wearable Health Sensors Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East and Africa Wearable Health Sensors Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: North America Wearable Health Sensors Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: North America Wearable Health Sensors Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: North America Wearable Health Sensors Industry Revenue (billion), by End User Industry 2025 & 2033

- Figure 29: North America Wearable Health Sensors Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 30: North America Wearable Health Sensors Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: North America Wearable Health Sensors Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Wearable Health Sensors Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Wearable Health Sensors Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 3: Global Wearable Health Sensors Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Wearable Health Sensors Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Wearable Health Sensors Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 6: Global Wearable Health Sensors Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Wearable Health Sensors Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Global Wearable Health Sensors Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 9: Global Wearable Health Sensors Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Wearable Health Sensors Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global Wearable Health Sensors Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 12: Global Wearable Health Sensors Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Wearable Health Sensors Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Global Wearable Health Sensors Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 15: Global Wearable Health Sensors Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Wearable Health Sensors Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global Wearable Health Sensors Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 18: Global Wearable Health Sensors Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Wearable Health Sensors Industry?

The projected CAGR is approximately 15.9%.

2. Which companies are prominent players in the Wearable Health Sensors Industry?

Key companies in the market include Infineon Technologies AG, mCube Inc *List Not Exhaustive, STMicroelectronics Inc, TE Connectivity Ltd, Texas Instruments Incorporated, Arm Limited, TDK Corporation, Fraunhofer IIS, Analog Devices Inc, Maxim Integrated Products Inc.

3. What are the main segments of the Wearable Health Sensors Industry?

The market segments include Type, End User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 84.53 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Need for Continuous Monitoring In Healthcare Services; Rising Growth toward Advanced Functions Sensors in Smart Gadgets; Miniaturization of Physiological Sensors.

6. What are the notable trends driving market growth?

Healthcare Industry Holds a Dominant Share in Wearable Health Sensors Market.

7. Are there any restraints impacting market growth?

Dearth of Common Standards and Interoperability Issues.

8. Can you provide examples of recent developments in the market?

June 2022 : Nitto Denko Corporation agreed to acquire Bend Labs, Inc. In line with this acquisition, Bend merged into the Nitto Group from June 1, 2022 to continue its business operations as Nitto Bend Technologies. As a result of this merger agreement, Bend's sensor device technologies were combined with Nitto's strengths for developing a next-generation technologies and products portfolio and new businesses utilizing sensor-acquired data.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Wearable Health Sensors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Wearable Health Sensors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Wearable Health Sensors Industry?

To stay informed about further developments, trends, and reports in the Wearable Health Sensors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence