Key Insights

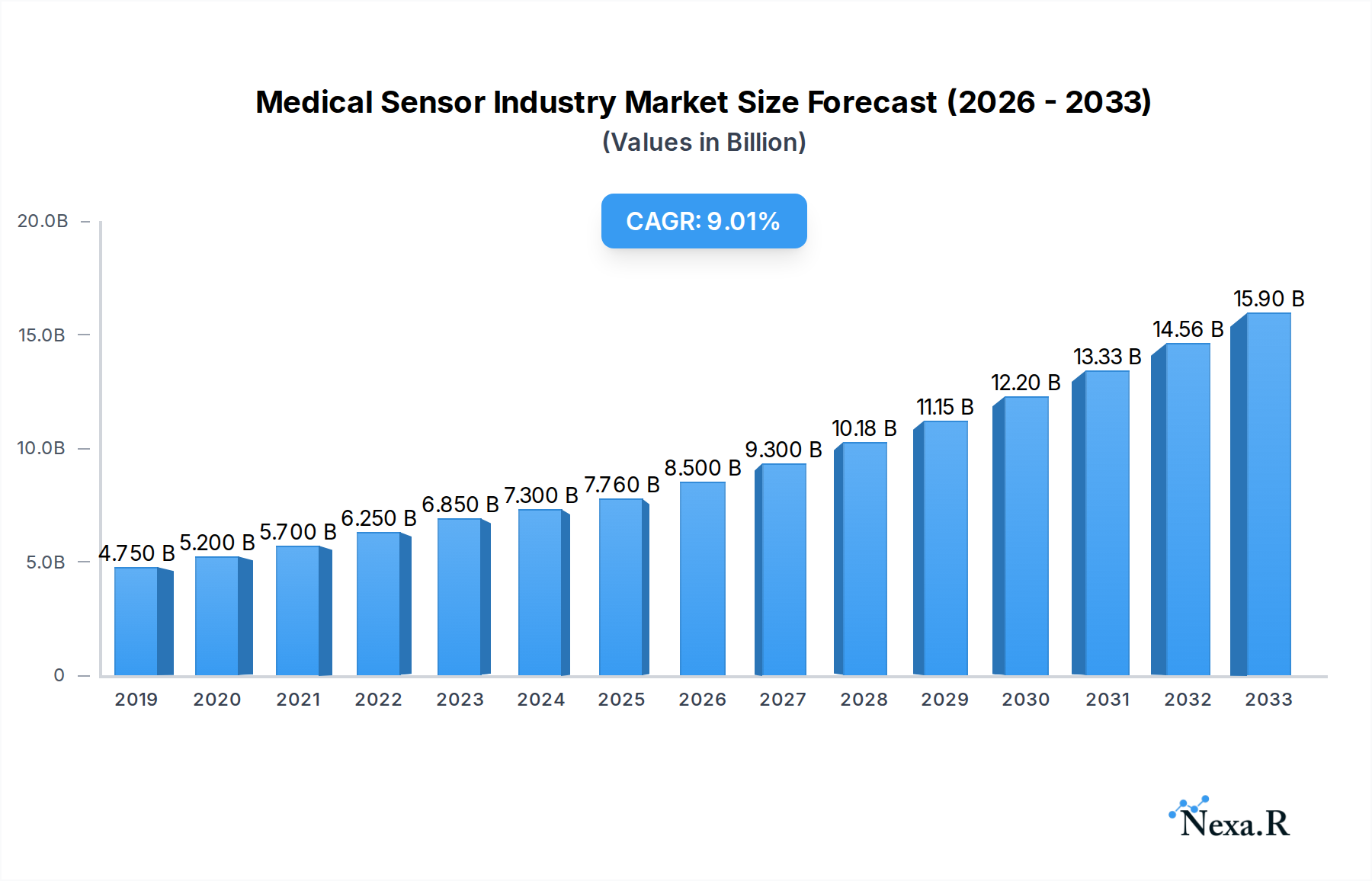

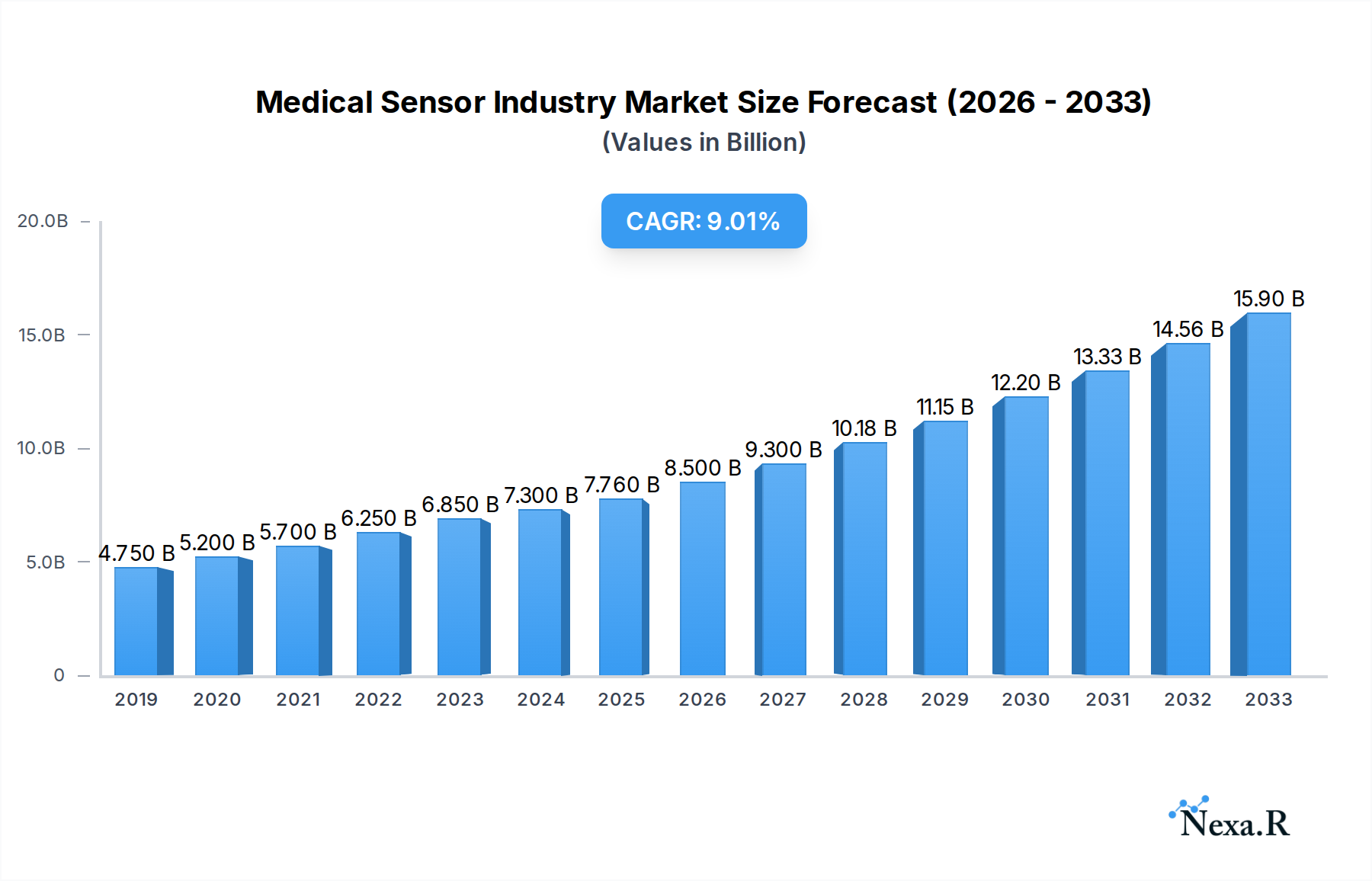

The global medical sensor market is poised for significant expansion, with a projected market size of USD 7760 million by 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 10.24%. This impressive growth trajectory is fueled by a confluence of factors, including the increasing prevalence of chronic diseases, the growing demand for remote patient monitoring solutions, and advancements in miniaturization and wireless sensor technology. The integration of biosensors for early disease detection and diagnosis is a particularly strong driver, alongside the escalating adoption of consumer wearable devices for health and wellness tracking. Furthermore, the continuous push for innovative diagnostic tools and the expanding healthcare infrastructure globally are further propelling the market forward. Key segments within this dynamic market include various sensor types such as biosensors, flow sensors, temperature sensors, and pressure sensors, catering to a wide array of applications spanning clinical settings and consumer health.

Medical Sensor Industry Market Size (In Billion)

The market's expansion is also being shaped by several emerging trends, including the rise of the Internet of Medical Things (IoMT), which facilitates seamless data exchange and enhances healthcare delivery. The development of highly sensitive and specific sensors, coupled with advancements in artificial intelligence and machine learning for data analysis, is revolutionizing patient care and diagnostics. However, the market is not without its restraints. Stringent regulatory approvals for medical devices, the high cost of advanced sensor development and integration, and concerns surrounding data security and privacy pose significant challenges. Despite these hurdles, the industry is witnessing a substantial investment in research and development, fostering innovation and paving the way for novel medical sensor solutions that promise to enhance patient outcomes and revolutionize the healthcare landscape. Companies are actively engaged in strategic collaborations and acquisitions to strengthen their market position and expand their product portfolios in this rapidly evolving sector.

Medical Sensor Industry Company Market Share

Medical Sensor Industry Report: Comprehensive Market Analysis & Growth Outlook (2019–2033)

This in-depth report delivers a critical analysis of the global medical sensor market, a vital and rapidly evolving sector within the healthcare technology landscape. Spanning 2019 to 2033, with a base and estimated year of 2025 and a forecast period from 2025–2033, this comprehensive study provides actionable insights into market dynamics, growth trajectories, and competitive landscapes. We meticulously examine both parent and child markets, offering a granular view of how advancements in components like flow sensors, biosensors, temperature sensors, and pressure sensors directly impact broader applications in clinical applications and consumer applications. Leveraging high-traffic keywords such as "medical device sensors," "wearable health sensors," "IoT healthcare," "biometric sensors," and "diagnostic sensors," this report is optimized for maximum search engine visibility and engagement among industry professionals, investors, and researchers. All values are presented in Million units, ensuring clarity and comparability.

Medical Sensor Industry Market Dynamics & Structure

The medical sensor industry exhibits a moderately consolidated market structure, driven by intense technological innovation and stringent regulatory frameworks. Key drivers include the escalating demand for remote patient monitoring, the growing prevalence of chronic diseases, and the increasing adoption of personalized medicine. The continuous development of miniaturized, highly sensitive, and cost-effective sensors is paramount, with companies investing heavily in R&D for advanced materials and integration capabilities. Servoflo Corporation, Honeywell International Inc, TE Connectivity Ltd (First Sensors AG), Sensirion Holding AG, Amphenol Advanced Sensors (Amphenol Corporation), Siemens AG, Omron Corporation, STMicroelectronics NV, NXP Semiconductors (Freescale Semiconductor), and GE Healthcare Inc are prominent players constantly vying for market share through product differentiation and strategic partnerships.

- Technological Innovation Drivers: Advancements in MEMS (Micro-Electro-Mechanical Systems), nanotechnology, and wireless communication technologies are crucial. The integration of AI and machine learning with sensor data for predictive diagnostics is a significant trend.

- Regulatory Frameworks: Compliance with FDA, CE marking, and other regional regulatory bodies is a major factor influencing product development cycles and market entry. Standards for data security and interoperability are becoming increasingly important.

- Competitive Product Substitutes: While direct substitutes are limited due to specialized functionalities, advancements in non-invasive monitoring techniques and alternative diagnostic methods pose indirect competition.

- End-User Demographics: An aging global population and a rising middle class with increased healthcare expenditure are key demographic trends fueling demand. The growing adoption of wearables by health-conscious individuals also contributes significantly.

- M&A Trends: Mergers and acquisitions are strategic tools for companies to expand their product portfolios, gain access to new technologies, and broaden their geographical reach. Deal volumes are projected to remain robust as companies seek synergistic growth.

Medical Sensor Industry Growth Trends & Insights

The medical sensor market is poised for substantial growth, driven by an increasing emphasis on proactive healthcare and the integration of digital health technologies. The global market size has witnessed a consistent upward trajectory, fueled by the widespread adoption of sophisticated diagnostic and monitoring devices. In the base year of 2025, the market is estimated to be valued at [Insert Predicted Value for 2025 in Million Units]. Projections indicate a robust Compound Annual Growth Rate (CAGR) of approximately [Insert Predicted CAGR]% from 2025 to 2033, underscoring a significant expansion in market penetration. This growth is largely attributed to the escalating demand for wearable health sensors, remote patient monitoring solutions, and point-of-care diagnostic devices.

Technological disruptions, such as the miniaturization of sensors and advancements in biocompatible materials, are enabling the development of more comfortable and effective medical devices. The proliferation of the Internet of Medical Things (IoMT) is a key catalyst, facilitating seamless data exchange between sensors, healthcare providers, and patients. Consumer behavior is also shifting towards preventative health management, with individuals increasingly investing in personal health monitoring devices. The rising incidence of chronic conditions like diabetes, cardiovascular diseases, and respiratory disorders necessitates continuous monitoring, thereby boosting the demand for advanced biosensors and pressure sensors. Furthermore, the ongoing research and development in areas like neuroprosthetics and advanced wound care are opening new avenues for medical sensor applications. The COVID-19 pandemic also accelerated the adoption of telemedicine and remote monitoring, highlighting the critical role of reliable medical sensors in public health infrastructure. The integration of AI with sensor data is revolutionizing diagnostics, enabling early disease detection and personalized treatment plans, further contributing to the market's expansive growth.

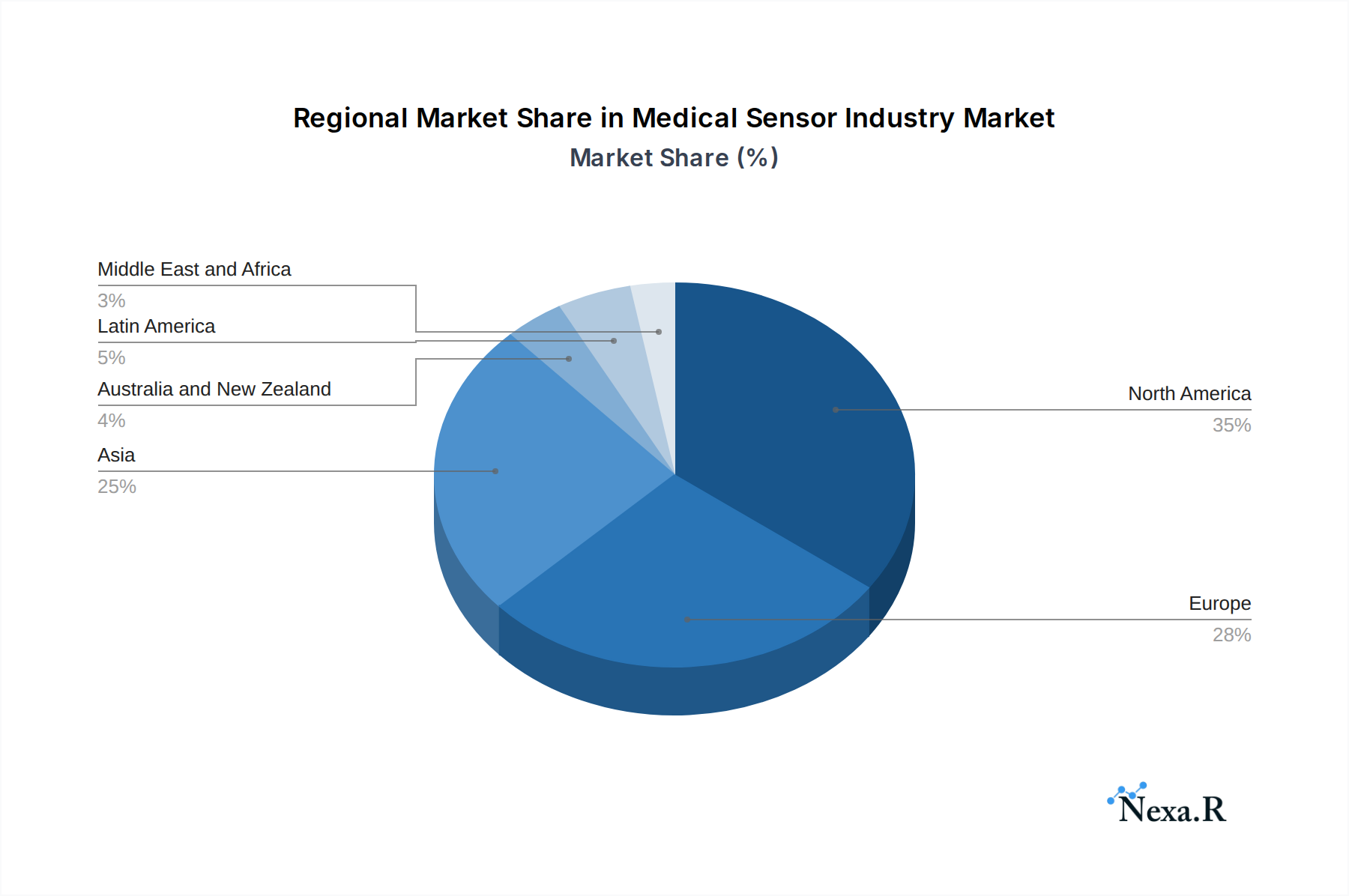

Dominant Regions, Countries, or Segments in Medical Sensor Industry

The medical sensor industry is characterized by significant regional disparities and segment dominance, with North America currently leading the market, driven by its robust healthcare infrastructure, high disposable income, and early adoption of advanced medical technologies. The United States, in particular, accounts for a substantial share of the global market due to extensive R&D investments and the presence of major medical device manufacturers. The Clinical Applications segment, encompassing patient monitoring, diagnostics, and surgical tools, is the primary driver of this dominance, accounting for an estimated [Insert Predicted Market Share %] of the total market in 2025. Within this segment, biosensors and temperature sensors are experiencing particularly high growth rates, fueled by their critical role in disease detection and management.

Key drivers of dominance in North America include favorable reimbursement policies for advanced medical treatments, a well-established regulatory framework (FDA), and a strong emphasis on innovation. The region also benefits from a significant patient pool suffering from chronic diseases, necessitating continuous monitoring solutions. In terms of specific segments, biosensors are experiencing remarkable expansion due to their application in rapid diagnostic tests, continuous glucose monitoring, and genetic analysis. The increasing focus on personalized medicine and companion diagnostics further propels the growth of this segment.

- North America: Dominates due to advanced healthcare systems, high R&D expenditure, and strong regulatory support.

- Europe: A significant market player with a growing emphasis on digital health initiatives and a mature regulatory environment. Germany, the UK, and France are key contributors.

- Asia Pacific: Exhibits the fastest growth potential, driven by expanding healthcare access, a large and aging population, and increasing investments in medical technology from countries like China and India.

- Clinical Applications: The largest and most influential segment, benefiting from the growing demand for diagnostic, monitoring, and therapeutic devices.

- Biosensors: A high-growth segment, critical for diagnostics, drug delivery, and personalized medicine.

- Temperature Sensors: Essential for fever detection, thermal imaging, and patient monitoring, particularly relevant in post-pandemic healthcare settings.

Medical Sensor Industry Product Landscape

The medical sensor industry is characterized by a dynamic product landscape, showcasing continuous innovation in accuracy, miniaturization, and functionality. Key product developments focus on enhancing patient comfort, improving diagnostic precision, and enabling remote patient management. Innovations include smart wearable sensors capable of real-time physiological data collection, implantable sensors for long-term health monitoring, and disposable biosensors for rapid point-of-care diagnostics. Companies are increasingly integrating advanced materials and wireless connectivity to create more seamless and user-friendly devices. The performance metrics are continually being pushed, with a focus on increased sensitivity, reduced power consumption, and enhanced biocompatibility for implantable devices. Unique selling propositions often revolve around non-invasiveness, superior accuracy, and cost-effectiveness.

Key Drivers, Barriers & Challenges in Medical Sensor Industry

Key Drivers:

- Rising Chronic Disease Prevalence: An aging global population and lifestyle changes lead to a surge in chronic conditions, demanding continuous monitoring and diagnosis.

- Advancements in Digital Health & IoMT: The proliferation of connected devices and telemedicine platforms creates a substantial demand for reliable medical sensors.

- Growing Demand for Remote Patient Monitoring: Wearable and home-use sensors enable continuous patient oversight, reducing hospitalizations and improving care.

- Technological Innovations: Miniaturization, increased accuracy, and the development of novel sensing materials (e.g., nanomaterials) are driving product development.

- Government Initiatives & Funding: Support for healthcare innovation and digital health adoption by governments worldwide accelerates market growth.

Barriers & Challenges:

- Stringent Regulatory Approvals: The lengthy and complex regulatory processes for medical devices can significantly delay market entry and increase development costs.

- High R&D and Manufacturing Costs: Developing and producing sophisticated medical sensors requires substantial investment in research, specialized equipment, and quality control.

- Data Security & Privacy Concerns: The collection and transmission of sensitive patient data necessitate robust cybersecurity measures, adding complexity and cost.

- Interoperability Issues: Ensuring seamless communication and data integration between different sensor systems and healthcare IT platforms remains a challenge.

- Reimbursement Policies: Inconsistent or inadequate reimbursement policies for novel sensor-based diagnostics and monitoring can hinder widespread adoption.

Emerging Opportunities in Medical Sensor Industry

Emerging opportunities in the medical sensor industry are abundant, driven by unmet clinical needs and evolving patient preferences. The burgeoning field of personalized medicine presents significant potential for tailored diagnostic and therapeutic sensors. The development of AI-powered biosensors capable of predicting disease onset or treatment response is a key growth area. The expansion of the IoMT ecosystem offers fertile ground for integrating smart sensors into everyday devices for continuous health tracking, moving beyond traditional medical settings. Untapped markets in developing economies, where healthcare access is expanding, represent substantial growth potential for cost-effective and reliable sensor solutions. Furthermore, innovations in flexible and stretchable electronics are paving the way for more comfortable and unobtrusive wearable and implantable sensors for diverse applications, including advanced wound monitoring and neurological interfaces.

Growth Accelerators in the Medical Sensor Industry Industry

Several catalysts are propelling the long-term growth of the medical sensor industry. Technological breakthroughs, particularly in materials science, nanotechnology, and microelectronics, are enabling the creation of smaller, more sensitive, and more energy-efficient sensors. Strategic partnerships between sensor manufacturers, device developers, and healthcare providers are crucial for fostering innovation and facilitating market penetration. The increasing focus on preventative healthcare and wellness is creating a sustained demand for consumer-grade health monitoring devices. Market expansion strategies, including targeting emerging economies with tailored solutions and navigating evolving reimbursement landscapes, will be critical for sustained growth. Investments in research and development for novel applications, such as non-invasive glucose monitoring and advanced cancer detection, are also key growth accelerators.

Key Players Shaping the Medical Sensor Industry Market

- Servoflo Corporation

- Honeywell International Inc

- TE Connectivity Ltd

- Sensirion Holding AG

- Amphenol Advanced Sensors

- Siemens AG

- Omron Corporation

- STMicroelectronics NV

- NXP Semiconductors

- GE Healthcare Inc

Notable Milestones in Medical Sensor Industry Sector

- August 2022 - Sibel Health announced raising USD 33 million in its Series B financing round. The funding aims to scale wearable sensors for remote monitoring in the hospital.

- August 2022 - A team at Nottingham Trent University and Nottingham University Hospitals NHS Trust has developed a new biosensor capable of accurately monitoring the condition of a chronic wound. The aim is for the technology to be embedded into dressings to avoid frequent removal and replacement for injury assessment.

- September 2021 - TE Connectivity Ltd acquired three companies known as Toolbox Medical Innovations, Wi Inc., and micro liquid. The combined entities will leverage US and European design and manufacturing capabilities to serve its global customer base.

- May 2021 - Honeywell announced that Dnata USA expanded its deployment of Honeywell ThermoRebellion temperature monitoring solution to support domestic and international passengers at Boston Logan International Airport. Honeywell's solution was designed and tested to meet the recommendations set by the US Food and Drug Administration Enforcement Policy for Telethermographic Devices in April 2020 to address the usage of thermal imaging systems during the COVID-19 pandemic.

In-Depth Medical Sensor Industry Market Outlook

The future outlook for the medical sensor industry is exceptionally promising, marked by sustained innovation and expanding applications. Growth accelerators such as the ongoing digital transformation of healthcare, the increasing demand for personalized medicine, and the global imperative for efficient chronic disease management will continue to fuel market expansion. Strategic collaborations between technology providers and healthcare institutions will be pivotal in translating cutting-edge research into impactful clinical solutions. The market is expected to witness a substantial increase in the adoption of advanced biosensors and wearable technologies for proactive health monitoring and early disease detection. Furthermore, the growing focus on improving patient outcomes and reducing healthcare costs globally underscores the indispensable role of sophisticated medical sensors in shaping the future of healthcare delivery.

Medical Sensor Industry Segmentation

-

1. Component

- 1.1. Flow Sensor

- 1.2. Biosensor

- 1.3. Temperature Sensor

- 1.4. Pressure Sensor

- 1.5. Other Types

-

2. Application

- 2.1. Clinical Applications

- 2.2. Consumer Applications

Medical Sensor Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Medical Sensor Industry Regional Market Share

Geographic Coverage of Medical Sensor Industry

Medical Sensor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.24% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Flow Sensor

- 5.1.2. Biosensor

- 5.1.3. Temperature Sensor

- 5.1.4. Pressure Sensor

- 5.1.5. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Clinical Applications

- 5.2.2. Consumer Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Australia and New Zealand

- 5.3.5. Latin America

- 5.3.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Global Medical Sensor Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Flow Sensor

- 6.1.2. Biosensor

- 6.1.3. Temperature Sensor

- 6.1.4. Pressure Sensor

- 6.1.5. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Clinical Applications

- 6.2.2. Consumer Applications

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. North America Medical Sensor Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Flow Sensor

- 7.1.2. Biosensor

- 7.1.3. Temperature Sensor

- 7.1.4. Pressure Sensor

- 7.1.5. Other Types

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Clinical Applications

- 7.2.2. Consumer Applications

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. Europe Medical Sensor Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Flow Sensor

- 8.1.2. Biosensor

- 8.1.3. Temperature Sensor

- 8.1.4. Pressure Sensor

- 8.1.5. Other Types

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Clinical Applications

- 8.2.2. Consumer Applications

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Asia Medical Sensor Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Flow Sensor

- 9.1.2. Biosensor

- 9.1.3. Temperature Sensor

- 9.1.4. Pressure Sensor

- 9.1.5. Other Types

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Clinical Applications

- 9.2.2. Consumer Applications

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Australia and New Zealand Medical Sensor Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Flow Sensor

- 10.1.2. Biosensor

- 10.1.3. Temperature Sensor

- 10.1.4. Pressure Sensor

- 10.1.5. Other Types

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Clinical Applications

- 10.2.2. Consumer Applications

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Latin America Medical Sensor Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Component

- 11.1.1. Flow Sensor

- 11.1.2. Biosensor

- 11.1.3. Temperature Sensor

- 11.1.4. Pressure Sensor

- 11.1.5. Other Types

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Clinical Applications

- 11.2.2. Consumer Applications

- 11.1. Market Analysis, Insights and Forecast - by Component

- 12. Middle East and Africa Medical Sensor Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Component

- 12.1.1. Flow Sensor

- 12.1.2. Biosensor

- 12.1.3. Temperature Sensor

- 12.1.4. Pressure Sensor

- 12.1.5. Other Types

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Clinical Applications

- 12.2.2. Consumer Applications

- 12.1. Market Analysis, Insights and Forecast - by Component

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Servoflo Corporation

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Honeywell International Inc

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 TE Connectivity Ltd (First Sensors AG)

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Sensirion Holding AG

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Amphenol Advanced Sensors (Amphenol Corporation)

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Siemens AG

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Omron Corporation

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 STMicroelectronics NV

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 NXP Semiconductors (Freescale Semiconductor)

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 GE Healthcare Inc

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 Servoflo Corporation

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Medical Sensor Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Medical Sensor Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Medical Sensor Industry Revenue (Million), by Component 2025 & 2033

- Figure 4: North America Medical Sensor Industry Volume (K Unit), by Component 2025 & 2033

- Figure 5: North America Medical Sensor Industry Revenue Share (%), by Component 2025 & 2033

- Figure 6: North America Medical Sensor Industry Volume Share (%), by Component 2025 & 2033

- Figure 7: North America Medical Sensor Industry Revenue (Million), by Application 2025 & 2033

- Figure 8: North America Medical Sensor Industry Volume (K Unit), by Application 2025 & 2033

- Figure 9: North America Medical Sensor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: North America Medical Sensor Industry Volume Share (%), by Application 2025 & 2033

- Figure 11: North America Medical Sensor Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: North America Medical Sensor Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America Medical Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Medical Sensor Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Medical Sensor Industry Revenue (Million), by Component 2025 & 2033

- Figure 16: Europe Medical Sensor Industry Volume (K Unit), by Component 2025 & 2033

- Figure 17: Europe Medical Sensor Industry Revenue Share (%), by Component 2025 & 2033

- Figure 18: Europe Medical Sensor Industry Volume Share (%), by Component 2025 & 2033

- Figure 19: Europe Medical Sensor Industry Revenue (Million), by Application 2025 & 2033

- Figure 20: Europe Medical Sensor Industry Volume (K Unit), by Application 2025 & 2033

- Figure 21: Europe Medical Sensor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Europe Medical Sensor Industry Volume Share (%), by Application 2025 & 2033

- Figure 23: Europe Medical Sensor Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: Europe Medical Sensor Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Europe Medical Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Medical Sensor Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Medical Sensor Industry Revenue (Million), by Component 2025 & 2033

- Figure 28: Asia Medical Sensor Industry Volume (K Unit), by Component 2025 & 2033

- Figure 29: Asia Medical Sensor Industry Revenue Share (%), by Component 2025 & 2033

- Figure 30: Asia Medical Sensor Industry Volume Share (%), by Component 2025 & 2033

- Figure 31: Asia Medical Sensor Industry Revenue (Million), by Application 2025 & 2033

- Figure 32: Asia Medical Sensor Industry Volume (K Unit), by Application 2025 & 2033

- Figure 33: Asia Medical Sensor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 34: Asia Medical Sensor Industry Volume Share (%), by Application 2025 & 2033

- Figure 35: Asia Medical Sensor Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Asia Medical Sensor Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Asia Medical Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Medical Sensor Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Australia and New Zealand Medical Sensor Industry Revenue (Million), by Component 2025 & 2033

- Figure 40: Australia and New Zealand Medical Sensor Industry Volume (K Unit), by Component 2025 & 2033

- Figure 41: Australia and New Zealand Medical Sensor Industry Revenue Share (%), by Component 2025 & 2033

- Figure 42: Australia and New Zealand Medical Sensor Industry Volume Share (%), by Component 2025 & 2033

- Figure 43: Australia and New Zealand Medical Sensor Industry Revenue (Million), by Application 2025 & 2033

- Figure 44: Australia and New Zealand Medical Sensor Industry Volume (K Unit), by Application 2025 & 2033

- Figure 45: Australia and New Zealand Medical Sensor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 46: Australia and New Zealand Medical Sensor Industry Volume Share (%), by Application 2025 & 2033

- Figure 47: Australia and New Zealand Medical Sensor Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Australia and New Zealand Medical Sensor Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Australia and New Zealand Medical Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Australia and New Zealand Medical Sensor Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Latin America Medical Sensor Industry Revenue (Million), by Component 2025 & 2033

- Figure 52: Latin America Medical Sensor Industry Volume (K Unit), by Component 2025 & 2033

- Figure 53: Latin America Medical Sensor Industry Revenue Share (%), by Component 2025 & 2033

- Figure 54: Latin America Medical Sensor Industry Volume Share (%), by Component 2025 & 2033

- Figure 55: Latin America Medical Sensor Industry Revenue (Million), by Application 2025 & 2033

- Figure 56: Latin America Medical Sensor Industry Volume (K Unit), by Application 2025 & 2033

- Figure 57: Latin America Medical Sensor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 58: Latin America Medical Sensor Industry Volume Share (%), by Application 2025 & 2033

- Figure 59: Latin America Medical Sensor Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: Latin America Medical Sensor Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: Latin America Medical Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Latin America Medical Sensor Industry Volume Share (%), by Country 2025 & 2033

- Figure 63: Middle East and Africa Medical Sensor Industry Revenue (Million), by Component 2025 & 2033

- Figure 64: Middle East and Africa Medical Sensor Industry Volume (K Unit), by Component 2025 & 2033

- Figure 65: Middle East and Africa Medical Sensor Industry Revenue Share (%), by Component 2025 & 2033

- Figure 66: Middle East and Africa Medical Sensor Industry Volume Share (%), by Component 2025 & 2033

- Figure 67: Middle East and Africa Medical Sensor Industry Revenue (Million), by Application 2025 & 2033

- Figure 68: Middle East and Africa Medical Sensor Industry Volume (K Unit), by Application 2025 & 2033

- Figure 69: Middle East and Africa Medical Sensor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 70: Middle East and Africa Medical Sensor Industry Volume Share (%), by Application 2025 & 2033

- Figure 71: Middle East and Africa Medical Sensor Industry Revenue (Million), by Country 2025 & 2033

- Figure 72: Middle East and Africa Medical Sensor Industry Volume (K Unit), by Country 2025 & 2033

- Figure 73: Middle East and Africa Medical Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 74: Middle East and Africa Medical Sensor Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Sensor Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 2: Global Medical Sensor Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 3: Global Medical Sensor Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Global Medical Sensor Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 5: Global Medical Sensor Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Medical Sensor Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global Medical Sensor Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 8: Global Medical Sensor Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 9: Global Medical Sensor Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 10: Global Medical Sensor Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 11: Global Medical Sensor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Medical Sensor Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: Global Medical Sensor Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 14: Global Medical Sensor Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 15: Global Medical Sensor Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 16: Global Medical Sensor Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 17: Global Medical Sensor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 18: Global Medical Sensor Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 19: Global Medical Sensor Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 20: Global Medical Sensor Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 21: Global Medical Sensor Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 22: Global Medical Sensor Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 23: Global Medical Sensor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global Medical Sensor Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Global Medical Sensor Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 26: Global Medical Sensor Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 27: Global Medical Sensor Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Global Medical Sensor Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 29: Global Medical Sensor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Global Medical Sensor Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Global Medical Sensor Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 32: Global Medical Sensor Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 33: Global Medical Sensor Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 34: Global Medical Sensor Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 35: Global Medical Sensor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Global Medical Sensor Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 37: Global Medical Sensor Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 38: Global Medical Sensor Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 39: Global Medical Sensor Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 40: Global Medical Sensor Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 41: Global Medical Sensor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 42: Global Medical Sensor Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Sensor Industry?

The projected CAGR is approximately 10.24%.

2. Which companies are prominent players in the Medical Sensor Industry?

Key companies in the market include Servoflo Corporation, Honeywell International Inc, TE Connectivity Ltd (First Sensors AG), Sensirion Holding AG, Amphenol Advanced Sensors (Amphenol Corporation), Siemens AG, Omron Corporation, STMicroelectronics NV, NXP Semiconductors (Freescale Semiconductor), GE Healthcare Inc.

3. What are the main segments of the Medical Sensor Industry?

The market segments include Component, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.76 Million as of 2022.

5. What are some drivers contributing to market growth?

Miniaturization of Sensors Leading to Ease in Integration; Increasing Advancement in Medical Devices and Accessories.

6. What are the notable trends driving market growth?

Pressure Sensors Play a Significant Role in the Medical Sensor Market.

7. Are there any restraints impacting market growth?

Lack of Proper IoT Technology Skills across Healthcare Organizations; High Deployment Cost of Necessary Infrastructure and Connected Medical Devices.

8. Can you provide examples of recent developments in the market?

August 2022 - Sibel Health announced raising USD 33 million in its Series B financing round. The funding aims to scale wearable sensors for remote monitoring in the hospital.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Sensor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Sensor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Sensor Industry?

To stay informed about further developments, trends, and reports in the Medical Sensor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence