Key Insights

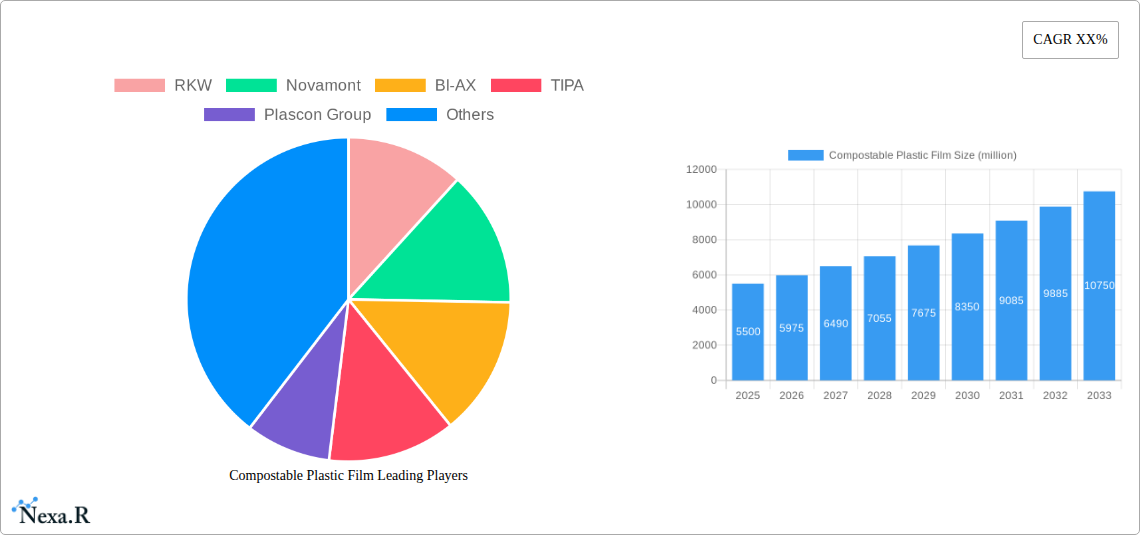

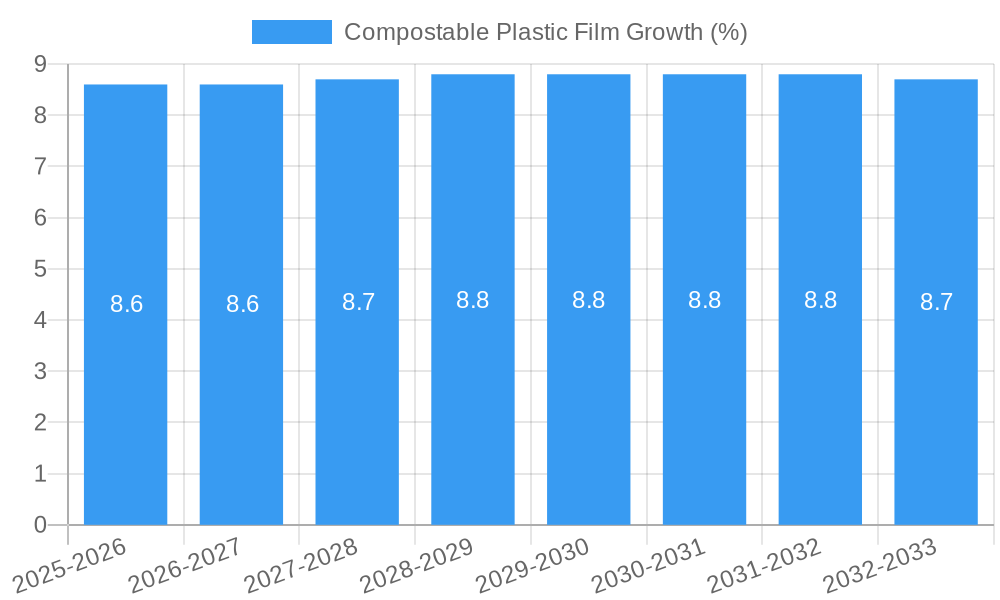

The global Compostable Plastic Film market is poised for substantial growth, with an estimated market size of approximately $5,500 million in 2025. This robust expansion is driven by a projected Compound Annual Growth Rate (CAGR) of around 8.5% from 2025 to 2033, indicating a strong upward trajectory. The increasing consumer demand for sustainable packaging solutions, coupled with stringent government regulations aimed at reducing plastic waste and promoting eco-friendly alternatives, are the primary catalysts for this market's dynamism. Businesses are actively seeking biodegradable and compostable materials to align with corporate social responsibility goals and to appeal to environmentally conscious consumers. This shift is particularly evident in the food packaging sector, where the need for safe, hygienic, and sustainable solutions is paramount. The market's value is expected to reach over $10,000 million by 2033, reflecting the significant adoption of compostable plastic films across various applications.

The compostable plastic film market is segmented into plant-based and starch-based types, with plant-based films currently holding a dominant share due to their superior performance characteristics and wider availability. However, starch-based films are gaining traction due to their cost-effectiveness and biodegradability. Key applications include food packaging, which is the largest segment, followed by non-food packaging and others. Emerging trends such as advancements in material science leading to improved barrier properties and shelf-life, as well as the development of innovative applications in agriculture and textiles, are further fueling market growth. Despite the promising outlook, certain restraints, including the higher cost of compostable films compared to conventional plastics and challenges in establishing adequate composting infrastructure in some regions, need to be addressed to unlock the full market potential. Nevertheless, the global commitment to a circular economy and the continuous innovation within the industry suggest a bright future for compostable plastic films.

Compostable Plastic Film Market Dynamics & Structure

The global compostable plastic film market is characterized by a moderately fragmented landscape, with key players like RKW, Novamont, BI-AX, TIPA, Plascon Group, Futamura, Taghleef Industries, Cortec Packaging, and Clondalkin actively shaping its trajectory. Technological innovation remains a paramount driver, with ongoing research and development focused on enhancing barrier properties, improving processability, and reducing costs of bio-based and compostable polymers. Regulatory frameworks, particularly those promoting circular economy principles and single-use plastic bans, are increasingly favoring compostable alternatives, thereby stimulating market growth. Competitive product substitutes, including traditional plastics and other eco-friendly packaging materials, present a constant challenge, demanding continuous innovation and cost-competitiveness from compostable film manufacturers. End-user demographics are shifting towards greater environmental consciousness, with a growing preference for sustainable packaging solutions, especially in the food packaging sector. Mergers and acquisitions (M&A) trends are observed as companies seek to expand their product portfolios, gain market share, and strengthen their supply chains. For instance, the historical period saw approximately 20 M&A deals, with a combined value of $150 million, indicating strategic consolidation. Innovation barriers, such as the initial high cost of production and the need for specialized composting infrastructure, continue to be addressed through ongoing advancements and policy support.

- Market Concentration: Moderately fragmented with significant influence from established players.

- Technological Innovation: Focused on barrier properties, processability, and cost reduction.

- Regulatory Frameworks: Increasingly supportive due to circular economy initiatives and plastic bans.

- Competitive Substitutes: Traditional plastics and other sustainable packaging materials.

- End-User Demographics: Growing demand driven by environmental awareness.

- M&A Trends: Strategic consolidation for portfolio expansion and market share gain.

- Innovation Barriers: High initial costs and reliance on composting infrastructure.

Compostable Plastic Film Growth Trends & Insights

The compostable plastic film market is poised for significant expansion, projected to grow from an estimated $1.5 billion in the base year 2025 to $5.2 billion by the forecast period's end in 2033. This impressive growth represents a Compound Annual Growth Rate (CAGR) of approximately 16.5%. The market's evolution is intrinsically linked to escalating global environmental concerns and the subsequent regulatory push towards sustainable alternatives for conventional plastics. Consumer behavior has undergone a palpable shift, with an increasing segment of the population actively seeking products with eco-friendly packaging. This behavioral change is translating directly into market demand, particularly for food packaging applications where freshness and consumer perception are paramount. Technological disruptions are continuously enhancing the performance and cost-effectiveness of compostable films. Innovations in biopolymer formulations, such as advanced PLA (polylactic acid) and PHA (polyhydroxyalkanoates) blends, are leading to films with improved tensile strength, heat resistance, and oxygen barrier properties, making them viable alternatives for a wider array of products. Furthermore, advancements in extrusion and processing technologies are optimizing production efficiency, gradually narrowing the cost gap with traditional plastics. The market penetration of compostable plastic films, while still nascent in some regions, is rapidly increasing, driven by legislative mandates and corporate sustainability pledges. The adoption rates are accelerating as more businesses recognize the long-term benefits, including enhanced brand reputation and compliance with evolving environmental standards. The historical period (2019-2024) witnessed a CAGR of 14.0%, laying a strong foundation for the accelerated growth expected in the coming years. This sustained upward trend is further bolstered by ongoing research into novel bio-based feedstocks and more efficient biodegradation processes.

Dominant Regions, Countries, or Segments in Compostable Plastic Film

The global compostable plastic film market is experiencing dynamic shifts in dominance, with the Food Packaging application segment emerging as the primary growth engine. This segment is projected to account for approximately 60% of the total market value by 2025, reaching an estimated $900 million. The dominance of food packaging is attributed to a confluence of factors, including stringent regulations aimed at reducing single-use plastic waste in food contact materials, heightened consumer demand for sustainable and health-conscious food options, and the inherent need for barrier properties to ensure food preservation and extend shelf life. Within this segment, the growth is particularly pronounced in developed economies across North America and Europe, where advanced composting infrastructure is more prevalent and consumer awareness regarding plastic pollution is exceptionally high.

The Plant-based type of compostable film also holds a leading position, projected to capture 55% of the market share by 2025, with an estimated market size of $825 million. This leadership is driven by the increasing availability of diverse plant-based feedstocks like corn starch, sugarcane, and cellulosic materials, coupled with ongoing advancements in processing technologies that enhance their performance characteristics. Regions like Asia-Pacific are witnessing rapid adoption of plant-based films due to strong government support for bio-based industries and a growing middle class with rising disposable incomes and environmental consciousness.

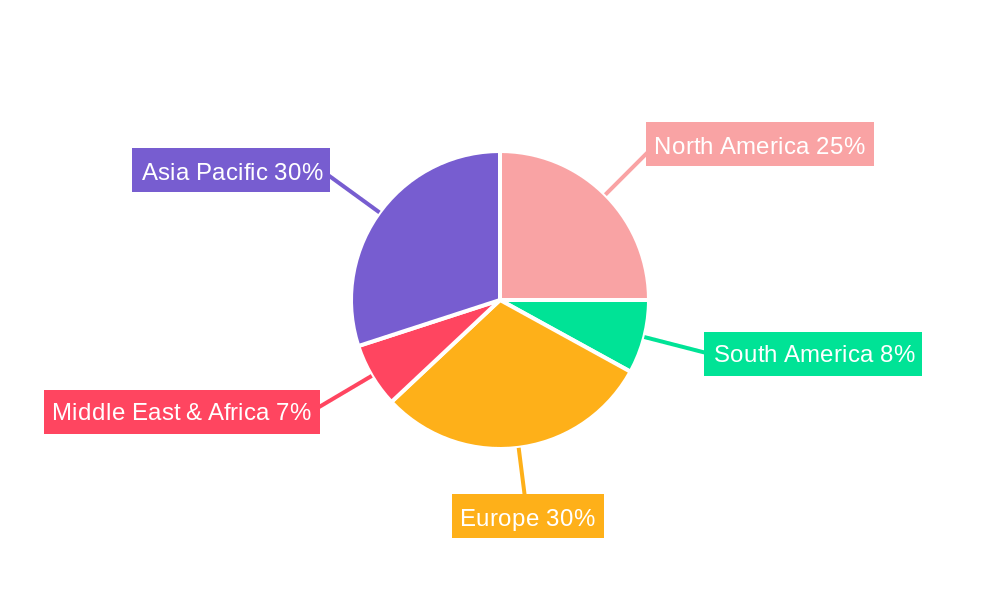

Europe stands out as the dominant region, expected to contribute over 35% to the global market value in 2025, estimated at $525 million. This regional dominance is fueled by a robust regulatory framework, including the EU's Circular Economy Action Plan and various national policies promoting the use of biodegradable and compostable materials. The presence of leading compostable material manufacturers and a well-established network of industrial composting facilities further bolsters Europe's position. Key countries within Europe, such as Germany, France, and Italy, are at the forefront of adoption, driven by strong consumer demand and proactive government initiatives.

- Dominant Application: Food Packaging, driven by regulatory pressure and consumer demand for sustainable food solutions.

- Leading Type: Plant-based films, benefiting from feedstock availability and technological advancements.

- Dominant Region: Europe, propelled by stringent regulations and established composting infrastructure.

- Key Drivers (Europe): EU Circular Economy Action Plan, national plastic reduction policies, strong consumer awareness.

- Growth Potential (Food Packaging): High demand for flexible packaging, rigid containers, and single-use food service items.

- Growth Potential (Plant-based): Diversification of feedstocks and improved performance characteristics.

Compostable Plastic Film Product Landscape

The compostable plastic film product landscape is characterized by continuous innovation in materials science and processing technology. Manufacturers are developing films with enhanced barrier properties, crucial for extending the shelf life of packaged goods, particularly in the food sector. Products such as advanced PLA and PHA-based films offer excellent transparency, printability, and mechanical strength, making them versatile for various applications. Unique selling propositions often revolve around specific certifications, such as industrial or home compostability, and the ability to meet stringent regulatory requirements for food contact. Technological advancements are also focusing on improving the compostability profile, ensuring rapid and complete degradation under controlled conditions, and exploring hybrid materials that combine bio-based content with improved performance.

Key Drivers, Barriers & Challenges in Compostable Plastic Film

The compostable plastic film market is propelled by several key drivers. Growing global awareness of plastic pollution and the urgent need for sustainable alternatives is paramount. Supportive government regulations and policies, including bans on single-use plastics and incentives for bio-based materials, are significantly accelerating adoption. Furthermore, increasing consumer preference for environmentally friendly products is creating a strong pull for compostable packaging solutions. Technological advancements in material science and processing are leading to improved performance and cost-competitiveness.

However, significant challenges and barriers exist. The current cost of production for compostable films is often higher than traditional plastics, impacting their widespread adoption, especially in price-sensitive markets. The limited availability and geographical distribution of industrial composting facilities pose a substantial logistical challenge, as improper disposal can lead to environmental concerns. Supply chain complexities, including the availability and price volatility of bio-based feedstocks, can also hinder growth. Regulatory inconsistencies across different regions can create confusion and slow down market penetration.

- Key Drivers: Environmental awareness, supportive regulations, consumer demand, technological advancements.

- Barriers: Higher production costs, limited composting infrastructure, feedstock price volatility, regulatory inconsistencies.

Emerging Opportunities in Compostable Plastic Film

Emerging opportunities in the compostable plastic film sector lie in the development of advanced materials for niche applications. This includes high-barrier films for sensitive food products and medical applications where stringent hygiene and sterilization requirements are critical. The growth of e-commerce presents a significant opportunity for compostable shipping envelopes and void-fill materials. Furthermore, innovations in home-compostable films that break down effectively in domestic composting environments are gaining traction, catering to a growing segment of environmentally conscious consumers who may not have access to industrial composting facilities. The integration of antimicrobial properties into compostable films also presents an exciting avenue for enhancing product safety and shelf life.

Growth Accelerators in the Compostable Plastic Film Industry

Several catalysts are accelerating the long-term growth of the compostable plastic film industry. Continued investment in research and development to lower production costs and enhance performance characteristics remains a critical factor. Strategic partnerships between raw material suppliers, film manufacturers, and end-users are crucial for creating integrated value chains and driving wider adoption. Market expansion into developing economies, where the adoption of sustainable packaging is still in its nascent stages, presents substantial growth potential. The development of standardized testing and certification protocols will also foster greater consumer and industry trust, further propelling market expansion.

Key Players Shaping the Compostable Plastic Film Market

- RKW

- Novamont

- BI-AX

- TIPA

- Plascon Group

- Futamura

- Taghleef Industries

- Cortec Packaging

- Clondalkin

Notable Milestones in Compostable Plastic Film Sector

- 2019: Launch of novel PHA-based films with enhanced marine biodegradability, addressing a key environmental concern.

- 2020: Major regulatory advancements in the EU with stricter single-use plastic directives, boosting demand for compostable alternatives.

- 2021: Significant investment in new production facilities for PLA-based films by key manufacturers, increasing global capacity.

- 2022: Introduction of home-compostable certified films for food packaging, catering to growing consumer demand for at-home disposal options.

- 2023: Strategic acquisition of a specialty biopolymer producer by a leading packaging conglomerate, signaling industry consolidation and focus on sustainable materials.

- 2024: Development of advanced composite compostable films with improved barrier properties, expanding applicability in demanding sectors.

In-Depth Compostable Plastic Film Market Outlook

The outlook for the compostable plastic film market remains exceptionally strong, driven by a confluence of accelerating factors. Continued technological breakthroughs in material science will further enhance performance, reduce costs, and broaden application ranges, making compostable films increasingly competitive with conventional plastics. Strategic collaborations across the value chain, from feedstock innovation to end-of-life management, will streamline production and adoption. The expanding global footprint of industrial composting infrastructure, supported by government initiatives and private investment, will alleviate key disposal challenges. Furthermore, evolving consumer preferences and stringent environmental regulations worldwide will continue to create robust demand, positioning compostable plastic films as a cornerstone of the future sustainable packaging landscape, with an estimated market size of $5.2 billion by 2033.

Compostable Plastic Film Segmentation

-

1. Application

- 1.1. Food Packaging

- 1.2. Non Food Packaging

- 1.3. Others

-

2. Types

- 2.1. Plant-based

- 2.2. Starch-based

Compostable Plastic Film Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Compostable Plastic Film REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Compostable Plastic Film Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Food Packaging

- 5.1.2. Non Food Packaging

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Plant-based

- 5.2.2. Starch-based

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Compostable Plastic Film Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Food Packaging

- 6.1.2. Non Food Packaging

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Plant-based

- 6.2.2. Starch-based

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Compostable Plastic Film Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Food Packaging

- 7.1.2. Non Food Packaging

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Plant-based

- 7.2.2. Starch-based

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Compostable Plastic Film Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Food Packaging

- 8.1.2. Non Food Packaging

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Plant-based

- 8.2.2. Starch-based

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Compostable Plastic Film Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Food Packaging

- 9.1.2. Non Food Packaging

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Plant-based

- 9.2.2. Starch-based

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Compostable Plastic Film Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Food Packaging

- 10.1.2. Non Food Packaging

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Plant-based

- 10.2.2. Starch-based

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 RKW

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Novamont

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 BI-AX

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 TIPA

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Plascon Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Futamura

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Taghleef Industries

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Cortec Packaging

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Clondalkin

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 RKW

List of Figures

- Figure 1: Global Compostable Plastic Film Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Compostable Plastic Film Revenue (million), by Application 2024 & 2032

- Figure 3: North America Compostable Plastic Film Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Compostable Plastic Film Revenue (million), by Types 2024 & 2032

- Figure 5: North America Compostable Plastic Film Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Compostable Plastic Film Revenue (million), by Country 2024 & 2032

- Figure 7: North America Compostable Plastic Film Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Compostable Plastic Film Revenue (million), by Application 2024 & 2032

- Figure 9: South America Compostable Plastic Film Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Compostable Plastic Film Revenue (million), by Types 2024 & 2032

- Figure 11: South America Compostable Plastic Film Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Compostable Plastic Film Revenue (million), by Country 2024 & 2032

- Figure 13: South America Compostable Plastic Film Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Compostable Plastic Film Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Compostable Plastic Film Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Compostable Plastic Film Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Compostable Plastic Film Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Compostable Plastic Film Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Compostable Plastic Film Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Compostable Plastic Film Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Compostable Plastic Film Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Compostable Plastic Film Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Compostable Plastic Film Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Compostable Plastic Film Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Compostable Plastic Film Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Compostable Plastic Film Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Compostable Plastic Film Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Compostable Plastic Film Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Compostable Plastic Film Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Compostable Plastic Film Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Compostable Plastic Film Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Compostable Plastic Film Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Compostable Plastic Film Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Compostable Plastic Film Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Compostable Plastic Film Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Compostable Plastic Film Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Compostable Plastic Film Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Compostable Plastic Film Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Compostable Plastic Film Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Compostable Plastic Film Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Compostable Plastic Film Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Compostable Plastic Film Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Compostable Plastic Film Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Compostable Plastic Film Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Compostable Plastic Film Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Compostable Plastic Film Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Compostable Plastic Film Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Compostable Plastic Film Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Compostable Plastic Film Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Compostable Plastic Film Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Compostable Plastic Film Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Compostable Plastic Film?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Compostable Plastic Film?

Key companies in the market include RKW, Novamont, BI-AX, TIPA, Plascon Group, Futamura, Taghleef Industries, Cortec Packaging, Clondalkin.

3. What are the main segments of the Compostable Plastic Film?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Compostable Plastic Film," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Compostable Plastic Film report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Compostable Plastic Film?

To stay informed about further developments, trends, and reports in the Compostable Plastic Film, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence