Key Insights

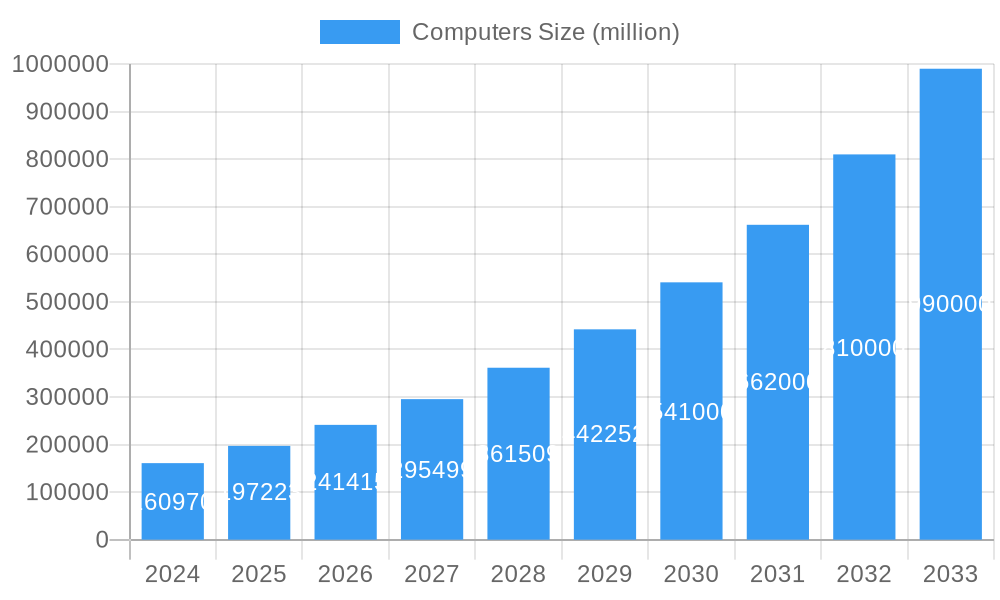

The global Computers market is poised for substantial expansion, reaching an estimated $160.97 billion in 2024. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 22.4% projected over the study period. Several dynamic factors are fueling this upward trajectory. The increasing demand for enhanced processing power and multitasking capabilities across various applications, from gaming and content creation to enterprise solutions, is a primary driver. Furthermore, the relentless innovation in hardware, including the integration of advanced processors, improved graphics, and longer battery life, is making computing devices more attractive and indispensable for both consumers and businesses. The proliferation of remote work and hybrid models further solidifies the need for reliable and efficient personal computing solutions.

Computers Market Size (In Billion)

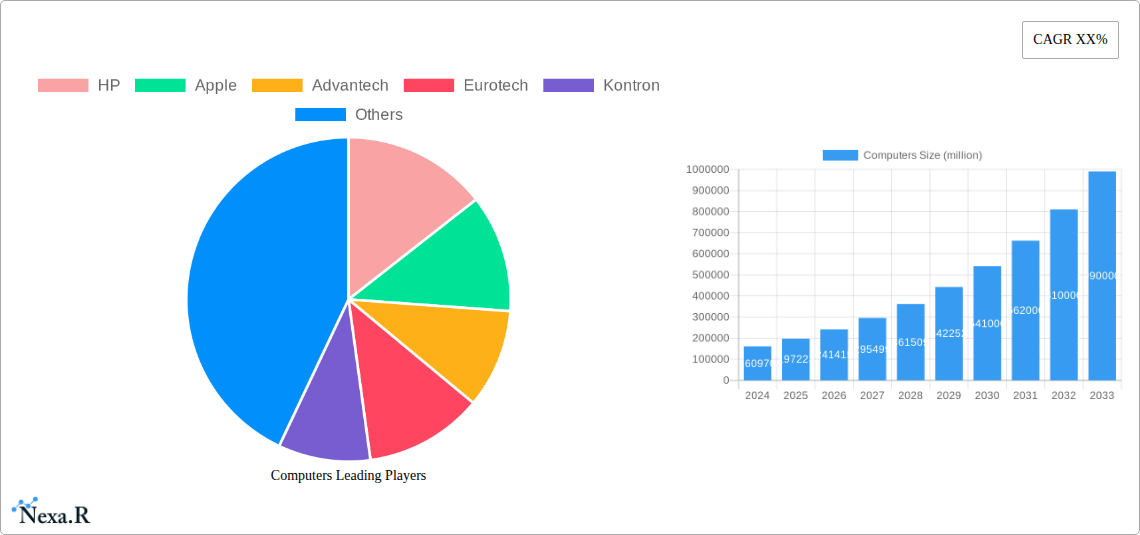

The market's segmentation reveals significant opportunities. The "Online" application segment is expected to lead, driven by the increasing adoption of cloud-based services, e-commerce, and digital entertainment. Conversely, the "Offline" segment, while perhaps growing at a slower pace, will continue to be crucial for sectors requiring dedicated, high-performance computing environments. Within the "Types" segment, Desktop and Laptop Computers are anticipated to maintain their dominance due to their versatility and widespread use. However, the rapid advancements and increasing affordability of Tablets and Smartphones, coupled with their growing capabilities, suggest they will capture a significant and expanding market share, particularly in emerging economies and for specific mobile-centric applications. Key players like HP, Apple, Advantech, Eurotech, and Kontron are actively investing in research and development to cater to these evolving demands, particularly in the technologically advanced regions of North America and Asia Pacific.

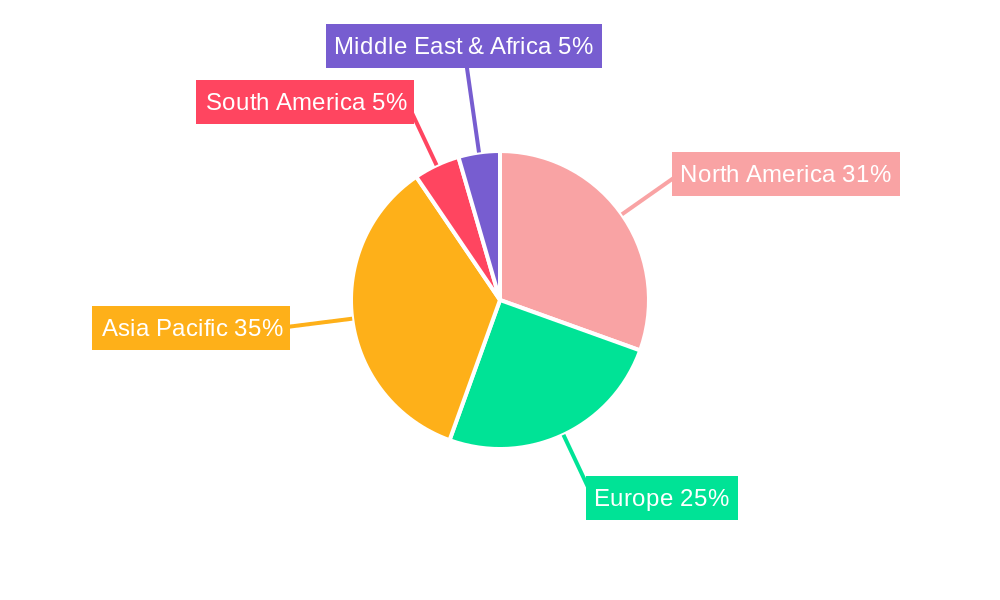

Computers Company Market Share

Computers Market Dynamics & Structure: A Comprehensive Analysis (2019-2033)

This in-depth report delves into the intricate dynamics and structure of the global computers market, providing critical insights for industry professionals navigating this ever-evolving landscape. From 2019 to 2033, we meticulously analyze market concentration, the relentless drivers of technological innovation, evolving regulatory frameworks, the competitive interplay of product substitutes, detailed end-user demographics, and the pervasive impact of mergers and acquisitions (M&A) on market consolidation. Our analysis quantifies market share percentages for key players and identifies trends in M&A deal volumes, while also qualitatively assessing innovation barriers and competitive advantages shaping the industry.

- Market Concentration: The computers market exhibits a mixed concentration, with a few dominant players like HP and Apple holding significant shares in the consumer and enterprise segments, particularly in Desktop and Laptop Computers. However, specialized segments like Mainframes and industrial computing (represented by companies such as Advantech, Eurotech, and Kontron) showcase a more fragmented structure, driven by niche applications and tailored solutions.

- Technological Innovation Drivers: Rapid advancements in Artificial Intelligence (AI), machine learning, cloud computing, and the Internet of Things (IoT) are fundamentally reshaping computer architecture and functionality. Miniaturization, enhanced processing power, and energy efficiency continue to be key innovation thrusts.

- Regulatory Frameworks: Evolving data privacy regulations (e.g., GDPR, CCPA), cybersecurity mandates, and environmental standards (e.g., EPEAT, RoHS) are influencing product design, manufacturing processes, and go-to-market strategies, particularly impacting Smartphones and Tablets.

- Competitive Product Substitutes: While traditional Desktop and Laptop Computers remain central, the rise of powerful Smartphones and Tablets, coupled with the increasing capabilities of cloud-based services and specialized embedded systems, presents significant substitution opportunities, especially for offline applications.

- End-User Demographics: A growing demand for sophisticated computing solutions across diverse age groups and professional sectors fuels market expansion. The increasing digital literacy and the proliferation of remote work models are particularly boosting the adoption of Laptops and cloud-connected devices.

- M&A Trends: Strategic acquisitions and mergers are actively reshaping the competitive landscape, with larger entities acquiring innovative startups or consolidating market presence in specific segments. For instance, acquisitions in the embedded systems and IoT hardware space by established players are observed. The volume of M&A deals in the personal computing segment remains significant, driven by market consolidation and portfolio expansion.

Computers Growth Trends & Insights: A Deep Dive into Market Evolution (2019-2033)

This section provides a comprehensive 600-word analysis of the global computers market's growth trajectory, leveraging critical data to illuminate market size evolution, adoption rates, transformative technological disruptions, and significant shifts in consumer and enterprise behavior. The study period spans from 2019 to 2033, with the base year and estimated year both set at 2025, and a forecast period extending from 2025 to 2033. We examine historical trends from 2019 to 2024 to contextualize future projections, offering actionable insights for stakeholders. The Compound Annual Growth Rate (CAGR) is projected to be robust, driven by an expanding digital economy and increasing per capita spending on computing devices.

The global computers market has demonstrated remarkable resilience and continuous evolution, exhibiting a consistent upward trend in market size from 2019 to 2024. This historical growth was fueled by the ubiquitous demand for digital connectivity, increasing digitalization across industries, and the proliferation of personal computing devices. The surge in remote work and online learning during the pandemic significantly accelerated the adoption of Laptop Computers and Tablets, marking a substantial shift in usage patterns and sales volumes. Even as the initial pandemic-driven boom moderates, these segments continue to experience steady growth due to ongoing hybrid work models and the increasing reliance on digital tools for productivity and communication.

Looking ahead to the forecast period of 2025-2033, the market is poised for sustained expansion, albeit with a dynamic interplay of growth drivers and moderating factors. The estimated market size for 2025 is xx billion units, with projections indicating a CAGR of approximately 5.5% through 2033. This growth is underpinned by several key trends. Firstly, the relentless advancement of technology, including the integration of AI and machine learning into everyday computing, is driving demand for more powerful and specialized hardware. This is particularly evident in enterprise solutions and advanced analytics platforms. Secondly, the expanding digital infrastructure in emerging economies is opening up new avenues for market penetration, increasing the adoption of Smartphones and Tablets even in previously underserved regions.

Technological disruptions continue to be a defining characteristic of the computers industry. The ongoing evolution of semiconductor technology, leading to more energy-efficient and powerful processors, is enabling the development of thinner, lighter, and more capable devices. The rise of foldable and flexible display technologies for Tablets and Smartphones, alongside advancements in augmented reality (AR) and virtual reality (VR) integrated computing, is creating new product categories and use cases. Furthermore, the increasing focus on sustainability and energy efficiency in computing hardware is influencing product development and consumer choices, driving demand for eco-friendly devices.

Consumer behavior has undergone a significant metamorphosis, with an increased expectation for seamless integration of devices and services across online and offline environments. The demand for personalized computing experiences, enhanced security features, and robust connectivity is paramount. Mobile-first strategies by many businesses are further solidifying the importance of Smartphones and Tablets in the overall computing ecosystem. The increasing sophistication of gaming and creative software also drives demand for high-performance Desktop Computers and Laptops. The market penetration of computing devices, particularly in developing nations, is projected to deepen, contributing significantly to overall market growth. The increasing reliance on cloud computing is also influencing the demand for end-user devices, favoring those with robust connectivity and processing capabilities to seamlessly access cloud-based applications and data. The continuous innovation in user interfaces and operating systems further enhances the appeal and usability of various computer types, driving sustained adoption rates.

Dominant Regions, Countries, or Segments in Computers: Unveiling Growth Engines (2019-2033)

This section identifies the leading regions, countries, and segments that are currently driving, and are projected to continue driving, market growth within the global computers industry. We provide a detailed analysis of dominance factors, including market share, growth potential, and the underlying economic and infrastructural catalysts.

Dominant Segment: Laptop Computers

Laptop Computers have emerged as the undisputed leader in the computers market, consistently outperforming other categories in terms of sales volume and revenue. This dominance is driven by a confluence of factors, including their unparalleled portability, versatility, and increasingly powerful capabilities that rival traditional desktop systems. The shift towards hybrid work models and remote learning has cemented their position as essential tools for both professional and educational purposes. In 2025, Laptop Computers are estimated to account for xx% of the total computers market value, with a projected CAGR of 6.2% through 2033.

- Key Drivers of Dominance:

- Hybrid Work & Remote Learning: The sustained adoption of flexible work arrangements and the ongoing need for accessible educational tools have created a persistent demand for portable computing solutions.

- Technological Advancements: Continuous innovation in battery life, processing power, display quality, and form factors (e.g., ultraportables, 2-in-1 convertibles) enhances their appeal and utility.

- Consumer & Enterprise Demand: Laptops cater to a broad spectrum of users, from students and casual users to demanding professionals in fields like graphic design, software development, and video editing.

- Ecosystem Integration: Seamless integration with cloud services, peripherals, and other smart devices further enhances their value proposition.

Dominant Region: Asia-Pacific

The Asia-Pacific region stands out as the most dynamic and rapidly growing market for computers, driven by its vast population, burgeoning economies, and increasing digital adoption. Government initiatives promoting digital transformation, coupled with a growing middle class with disposable income, are fueling demand across all computer segments. The region is also a major manufacturing hub, contributing to competitive pricing and product availability. In 2025, the Asia-Pacific region is projected to contribute xx% to the global computers market revenue, with an anticipated CAGR of 7.1% during the forecast period.

- Key Drivers of Regional Dominance:

- Economic Growth & Digitalization: Rapid economic expansion and strong government support for digitalization are driving widespread adoption of computing devices.

- Large & Young Population: A youthful demographic with a high propensity for technology adoption and a growing demand for digital services.

- Manufacturing Prowess: The region's role as a global manufacturing center for electronics ensures competitive pricing and access to the latest technologies.

- Infrastructure Development: Significant investments in internet infrastructure and telecommunications are facilitating greater connectivity and online computer usage.

Dominant Country: United States

The United States continues to be a leading market for computers, driven by a highly developed economy, a strong culture of innovation, and a significant demand for advanced computing solutions across both consumer and enterprise sectors. The country is a key market for high-end Laptops, Desktop Computers, and Smartphones, with a considerable uptake of cutting-edge technologies. In 2025, the United States is expected to represent xx% of the global computers market value.

- Key Drivers of Country Dominance:

- Technological Innovation Hub: Home to major technology companies, driving demand for the latest computing hardware and software.

- High Disposable Income: A strong economic base allows for higher consumer spending on premium computing devices.

- Enterprise Adoption: Widespread adoption of advanced computing solutions in businesses for productivity, data analytics, and AI integration.

- Research & Development: Significant investment in R&D fuels the demand for high-performance computing for scientific and technological advancements.

Dominant Application: Online

The shift towards online applications is a pervasive trend across the entire computers market. The convenience, accessibility, and collaborative capabilities offered by online platforms have made them indispensable for a wide range of activities, from work and education to entertainment and commerce. This trend is particularly pronounced in the usage of Smartphones, Tablets, and Laptops. In 2025, online applications are projected to account for xx% of the total computer usage time, and this proportion is expected to grow.

- Key Drivers of Online Application Dominance:

- Cloud Computing Services: The proliferation of cloud-based software and storage solutions necessitates constant online connectivity.

- Digital Services: The growth of e-commerce, streaming services, online gaming, and social media platforms is heavily reliant on online computer access.

- Remote Collaboration Tools: Platforms for video conferencing, project management, and document sharing have become essential for modern workforces.

- Accessibility & Flexibility: Online access provides users with the flexibility to work, learn, and communicate from virtually any location with an internet connection.

Computers Product Landscape: Innovation at the Forefront

The computers market is characterized by a relentless stream of product innovations and evolving applications, driven by the pursuit of enhanced performance, user experience, and specialized functionalities. From the foundational power of Mainframes powering critical infrastructure to the hyper-connectivity of Smartphones, the landscape is diverse and dynamic. Desktop Computers continue to evolve with increased processing power and graphics capabilities for demanding tasks, while Laptop Computers are pushing the boundaries of portability and battery life without compromising performance. Tablets offer a unique blend of portability and functionality, bridging the gap between smartphones and laptops, with advancements in stylus integration and productivity software. Smartphones, the most ubiquitous computing devices, are witnessing rapid innovation in camera technology, display quality, processing speed, and AI integration, making them indispensable personal computers. The underlying trend across all these types is miniaturization, improved energy efficiency, and the seamless integration of Artificial Intelligence, enabling more intelligent and personalized user experiences.

Key Drivers, Barriers & Challenges in Computers

The computers industry is propelled by powerful forces, yet faces significant headwinds that shape its trajectory.

Key Drivers:

- Technological Advancements: Continuous innovation in processors (e.g., ARM, x86 architectures), AI integration, 5G connectivity, and display technologies (e.g., OLED, micro-LED) are creating demand for new and upgraded devices.

- Digital Transformation: The ongoing digitalization of industries and government services necessitates robust computing infrastructure and end-user devices.

- Growing Demand for Data Analytics & AI: The increasing reliance on data-driven decision-making and the deployment of AI applications are driving demand for high-performance computing power.

- Emerging Economies: Rapid economic growth and increasing internet penetration in developing regions are expanding the addressable market for all types of computers.

Key Barriers & Challenges:

- Supply Chain Disruptions: Global chip shortages and geopolitical tensions continue to pose risks to production volumes and component availability, impacting lead times and costs. For instance, the semiconductor shortage in recent years led to an estimated xx% increase in production costs for certain components.

- Intensifying Competition: The market is highly competitive, with established players constantly innovating to maintain market share, leading to price pressures and reduced profit margins in certain segments.

- Cybersecurity Threats: Growing sophistication of cyberattacks necessitates continuous investment in security features, increasing product development costs and posing reputational risks for manufacturers.

- Evolving Consumer Preferences: Rapid shifts in consumer demand for form factors, features, and ecosystem integration can lead to inventory management challenges and the risk of product obsolescence.

- Regulatory Hurdles: Stringent data privacy regulations, environmental standards, and trade policies can impact manufacturing, distribution, and market access, with compliance costs potentially reaching millions of dollars annually for larger corporations.

Emerging Opportunities in Computers

The computers sector is ripe with emerging opportunities, driven by evolving technological paradigms and unmet market needs. The burgeoning field of edge computing presents a significant avenue for growth, with a demand for specialized, robust computers that can process data closer to the source, reducing latency and enhancing real-time analytics. The continued expansion of the Internet of Things (IoT) ecosystem is creating a substantial market for embedded computers and industrial PCs, tailored for specific applications in manufacturing, healthcare, and smart cities. Furthermore, the increasing demand for sustainable and energy-efficient computing solutions offers a niche for eco-friendly devices and innovative power management technologies. The integration of advanced AI capabilities directly into hardware, enabling on-device machine learning, is another promising area, driving the development of next-generation processors and specialized AI accelerators for consumer and enterprise applications. The growth of the metaverse and immersive technologies also presents opportunities for the development of high-performance computing hardware capable of rendering complex virtual environments.

Growth Accelerators in the Computers Industry

Several catalysts are poised to significantly accelerate growth within the computers industry. The ongoing advancements in Artificial Intelligence and Machine Learning are not merely software-driven but are increasingly dictating hardware requirements, pushing the demand for specialized AI chips and powerful processors that can handle complex computations at scale. Strategic partnerships between hardware manufacturers, software developers, and cloud service providers are fostering integrated ecosystems that enhance user experience and drive device adoption. For example, collaborations focused on optimizing operating systems for specific hardware architectures can lead to significant performance gains and a more seamless user journey. Furthermore, market expansion strategies targeting underserved developing regions, coupled with localized product offerings and accessible pricing models, will unlock new customer bases. The continued integration of 5G technology into computing devices will also spur growth by enabling faster, more reliable connectivity, opening up new possibilities for real-time applications and enhanced mobile computing experiences.

Key Players Shaping the Computers Market

- HP

- Apple

- Advantech

- Eurotech

- Kontron

Notable Milestones in Computers Sector

- 2019: Release of Intel's 10th Gen Core processors, enhancing performance and efficiency for laptops and desktops.

- 2020: Significant surge in demand for laptops and tablets due to the global shift to remote work and online learning.

- 2021: Continued supply chain challenges, particularly semiconductor shortages, impacting production volumes across the industry.

- 2022: Increased focus on AI integration in mobile processors, enhancing on-device machine learning capabilities for smartphones.

- 2023: Growing momentum in the foldable device market for tablets and smartphones, signaling a new form factor trend.

- 2024: Advancements in energy-efficient computing architectures, particularly ARM-based processors, gaining traction in mainstream computing.

In-Depth Computers Market Outlook

The future of the computers market is characterized by sustained growth driven by relentless technological innovation and expanding global digital adoption. The integration of Artificial Intelligence into computing hardware, from smartphones to industrial PCs, will unlock new levels of performance and user personalization. Strategic alliances between key industry players, fostering end-to-end solutions and optimized user experiences, will be pivotal in capturing market share. Furthermore, the expansion of computing capabilities into emerging economies, coupled with tailored product offerings, presents a significant avenue for unlocking untapped demand. The continued evolution of connectivity technologies like 5G and the emergence of new computing paradigms like edge and metaverse computing will act as significant growth accelerators, shaping a dynamic and opportunity-rich market landscape.

Computers Segmentation

-

1. Application

- 1.1. Online

- 1.2. Offline

-

2. Types

- 2.1. Mainframes

- 2.2. Desktop

- 2.3. Laptop Computers

- 2.4. Tablets

- 2.5. Smartphones

Computers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Computers Regional Market Share

Geographic Coverage of Computers

Computers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Online

- 5.1.2. Offline

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Mainframes

- 5.2.2. Desktop

- 5.2.3. Laptop Computers

- 5.2.4. Tablets

- 5.2.5. Smartphones

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Computers Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Online

- 6.1.2. Offline

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Mainframes

- 6.2.2. Desktop

- 6.2.3. Laptop Computers

- 6.2.4. Tablets

- 6.2.5. Smartphones

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Computers Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Online

- 7.1.2. Offline

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Mainframes

- 7.2.2. Desktop

- 7.2.3. Laptop Computers

- 7.2.4. Tablets

- 7.2.5. Smartphones

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Computers Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Online

- 8.1.2. Offline

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Mainframes

- 8.2.2. Desktop

- 8.2.3. Laptop Computers

- 8.2.4. Tablets

- 8.2.5. Smartphones

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Computers Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Online

- 9.1.2. Offline

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Mainframes

- 9.2.2. Desktop

- 9.2.3. Laptop Computers

- 9.2.4. Tablets

- 9.2.5. Smartphones

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Computers Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Online

- 10.1.2. Offline

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Mainframes

- 10.2.2. Desktop

- 10.2.3. Laptop Computers

- 10.2.4. Tablets

- 10.2.5. Smartphones

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Computers Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Online

- 11.1.2. Offline

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Mainframes

- 11.2.2. Desktop

- 11.2.3. Laptop Computers

- 11.2.4. Tablets

- 11.2.5. Smartphones

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 HP

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Apple

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Advantech

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Eurotech

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Kontron

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.1 HP

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Computers Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Computers Revenue (million), by Application 2025 & 2033

- Figure 3: North America Computers Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Computers Revenue (million), by Types 2025 & 2033

- Figure 5: North America Computers Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Computers Revenue (million), by Country 2025 & 2033

- Figure 7: North America Computers Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Computers Revenue (million), by Application 2025 & 2033

- Figure 9: South America Computers Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Computers Revenue (million), by Types 2025 & 2033

- Figure 11: South America Computers Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Computers Revenue (million), by Country 2025 & 2033

- Figure 13: South America Computers Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Computers Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Computers Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Computers Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Computers Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Computers Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Computers Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Computers Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Computers Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Computers Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Computers Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Computers Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Computers Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Computers Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Computers Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Computers Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Computers Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Computers Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Computers Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Computers Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Computers Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Computers Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Computers Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Computers Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Computers Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Computers Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Computers Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Computers Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Computers Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Computers Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Computers Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Computers Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Computers Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Computers Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Computers Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Computers Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Computers Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Computers Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Computers Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Computers?

The projected CAGR is approximately 7.8%.

2. Which companies are prominent players in the Computers?

Key companies in the market include HP, Apple, Advantech, Eurotech, Kontron.

3. What are the main segments of the Computers?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 68.6 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Computers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Computers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Computers?

To stay informed about further developments, trends, and reports in the Computers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence