Key Insights

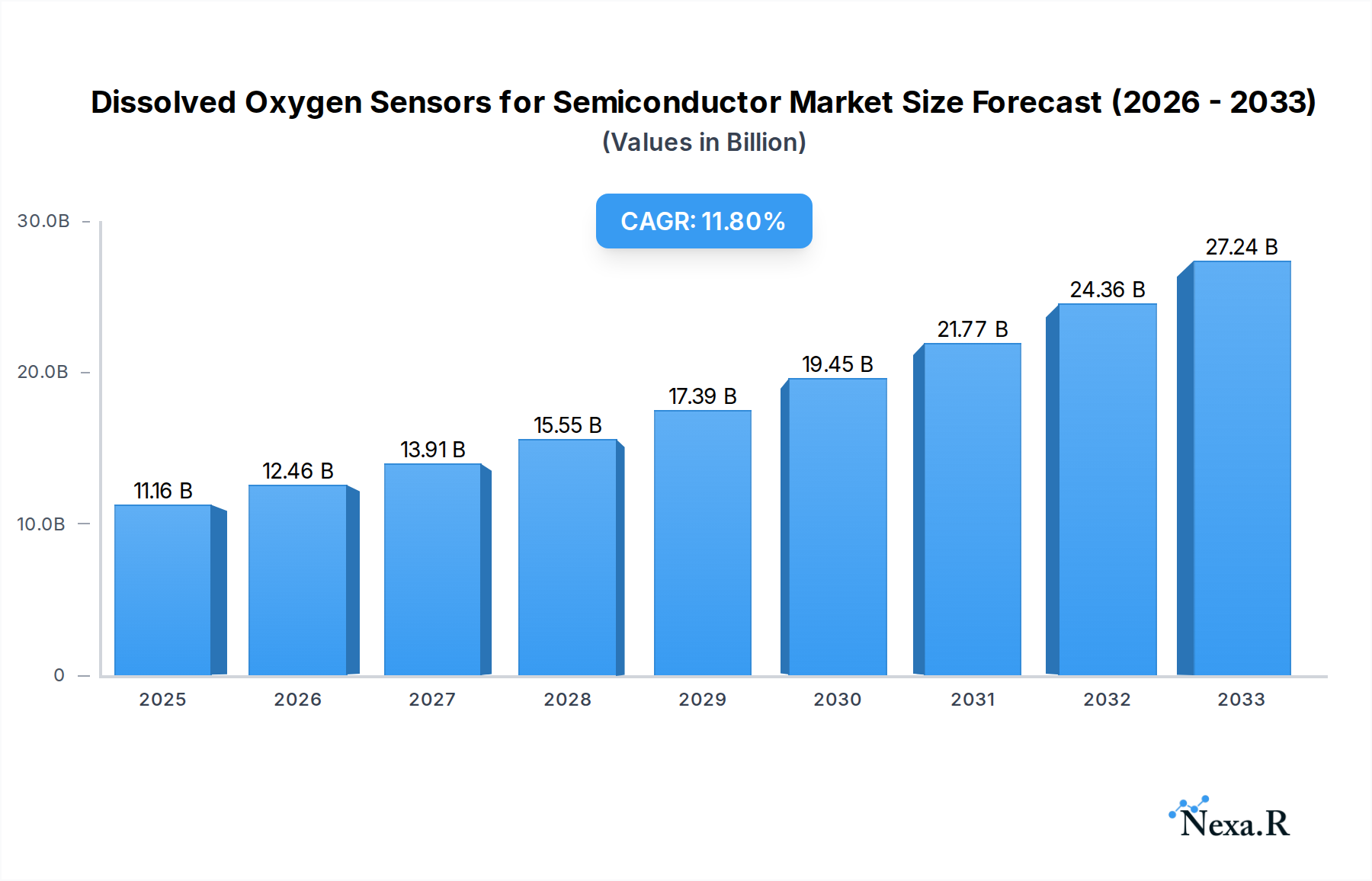

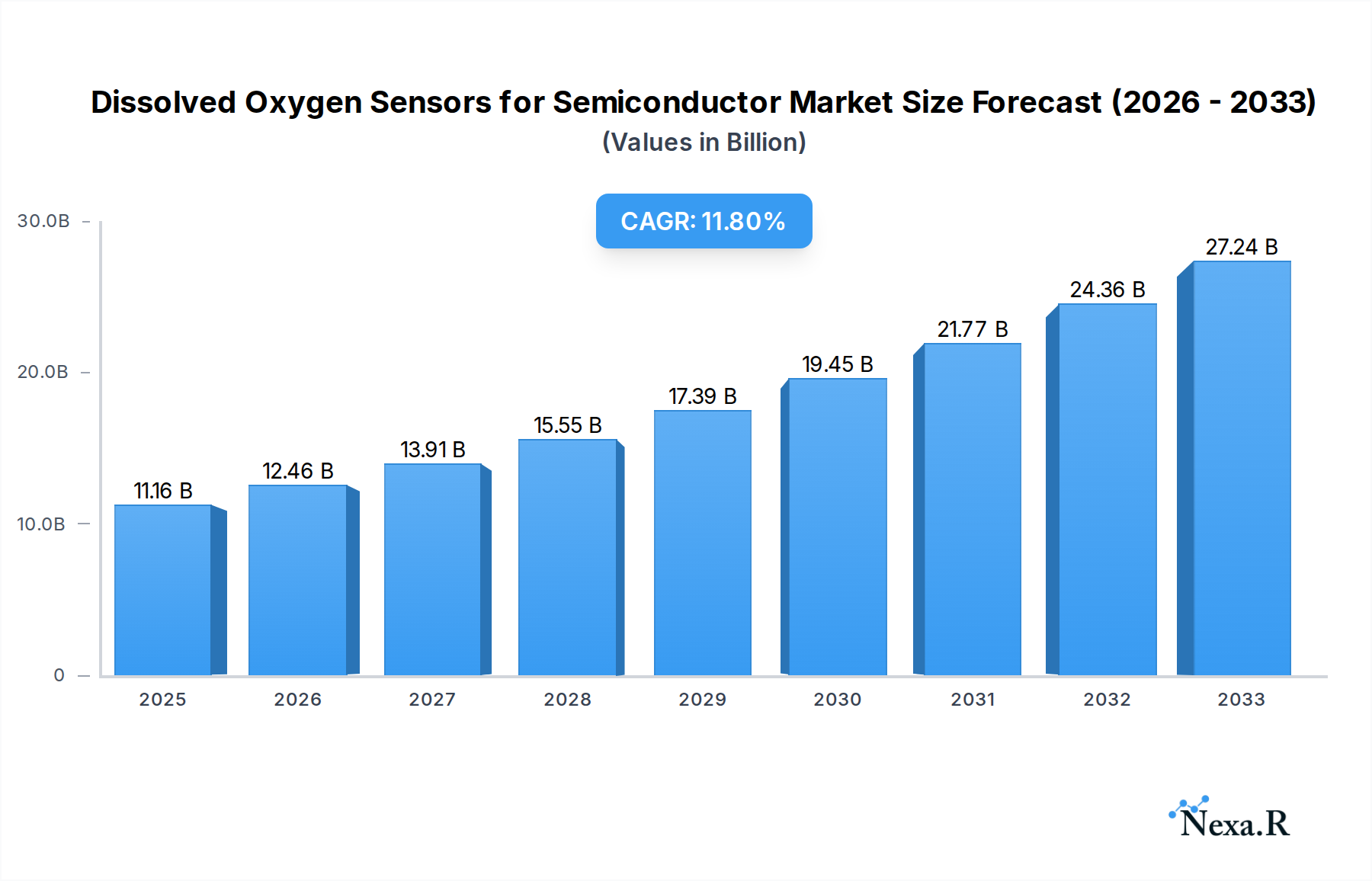

The Dissolved Oxygen (DO) Sensors for Semiconductor market is poised for significant expansion, projected to reach an estimated $11.16 billion by 2025. This robust growth is fueled by an anticipated Compound Annual Growth Rate (CAGR) of 11.45% during the forecast period. The semiconductor industry's increasing demand for ultra-pure water and stringent process control is a primary driver. Dissolved oxygen levels directly impact water quality, and precise measurement is crucial for preventing contamination and ensuring the integrity of delicate semiconductor manufacturing processes. Consequently, the adoption of advanced DO sensor technologies, particularly those employing polarography, current, and optical methods, is escalating. These technologies offer enhanced accuracy, faster response times, and greater reliability, making them indispensable for sophisticated semiconductor fabrication plants. The laboratory segment also contributes to market growth, driven by research and development activities focused on optimizing semiconductor manufacturing processes and developing new materials.

Dissolved Oxygen Sensors for Semiconductor Market Size (In Billion)

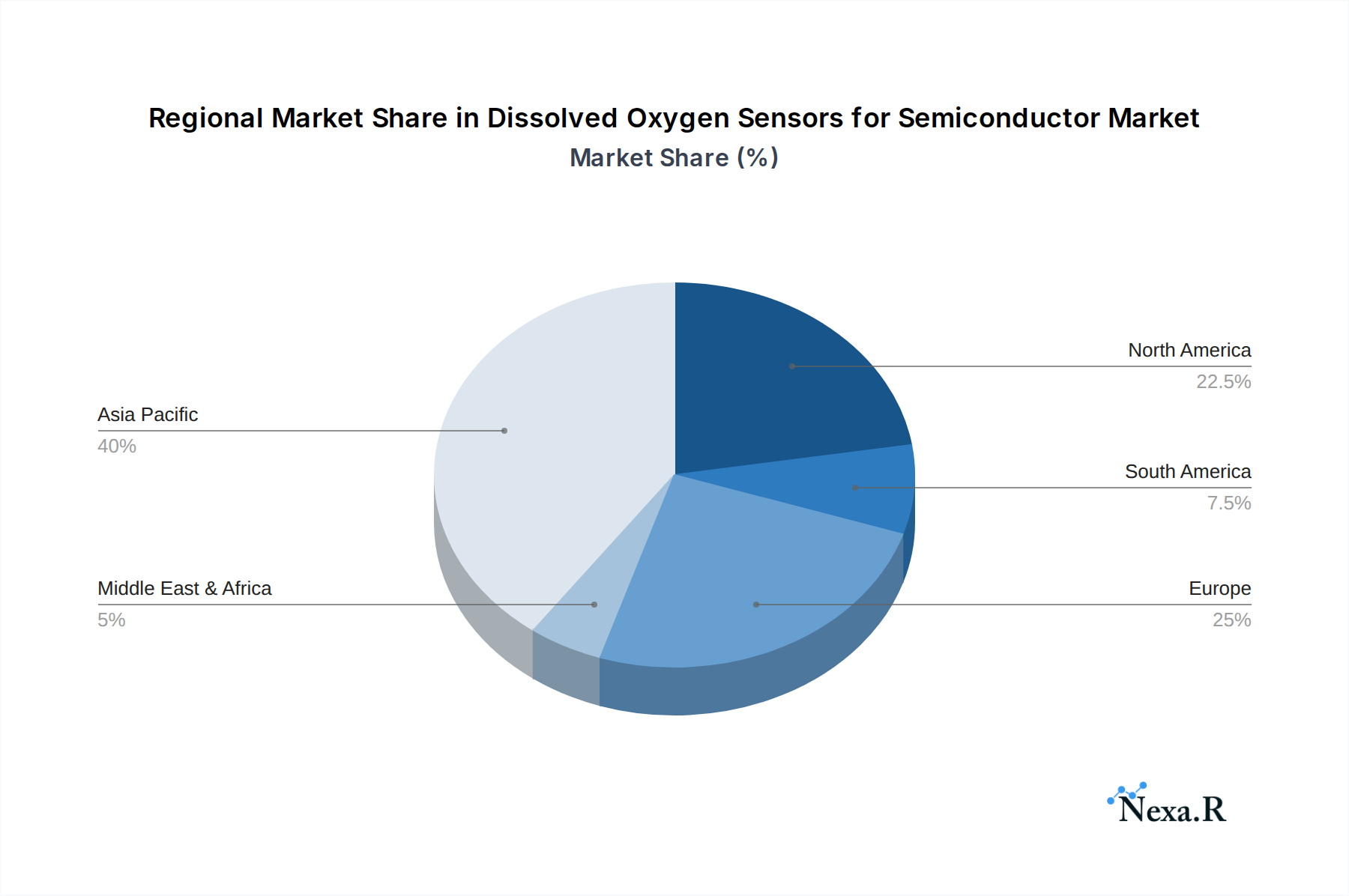

The market's upward trajectory is further supported by technological advancements in sensor design and manufacturing, leading to more compact, durable, and cost-effective solutions. Leading companies like Entegris, HORIBA, ABB, and Mettler-Toledo are actively investing in innovation, introducing next-generation DO sensors that cater to the evolving needs of the semiconductor industry. While the market benefits from strong demand drivers, potential restraints such as the high initial investment costs for advanced sensor systems and the need for specialized expertise in calibration and maintenance could pose challenges. However, the undeniable importance of dissolved oxygen monitoring for semiconductor yield, quality, and operational efficiency is expected to outweigh these limitations, driving continued market penetration and growth throughout the forecast period. Regions like Asia Pacific, particularly China and South Korea, are expected to be significant growth hubs due to their dominant presence in semiconductor manufacturing.

Dissolved Oxygen Sensors for Semiconductor Company Market Share

Dissolved Oxygen Sensors for Semiconductor Market Report: In-Depth Analysis and Future Outlook (2019-2033)

This comprehensive report offers a detailed analysis of the global Dissolved Oxygen (DO) Sensors for Semiconductor market, providing critical insights into market dynamics, growth trends, regional dominance, product landscape, and key players. With a study period spanning from 2019 to 2033, including a base year of 2025 and a forecast period of 2025-2033, this report is an indispensable resource for industry professionals, investors, and stakeholders seeking to understand the evolving landscape of this vital market. The report leverages high-traffic keywords such as "dissolved oxygen sensors semiconductor," "semiconductor industrial DO sensors," "laboratory DO sensors," "polarography DO sensor," "current method DO sensor," "optical DO sensor," "semiconductor manufacturing," and "water quality monitoring in semiconductors" to maximize search engine visibility and attract relevant industry attention. Furthermore, it analyzes the parent market encompassing industrial water quality monitoring and the child market focused specifically on semiconductor applications, offering a holistic view.

Dissolved Oxygen Sensors for Semiconductor Market Dynamics & Structure

The Dissolved Oxygen Sensors for Semiconductor market is characterized by a moderate concentration, with key players investing heavily in technological innovation to meet the stringent purity requirements of semiconductor manufacturing. Regulatory frameworks, particularly those concerning environmental protection and water quality standards in industrial processes, play a significant role in shaping market entry and product development. Competitive product substitutes, though limited in their ability to precisely replicate DO monitoring in ultra-pure water environments, do exist and necessitate continuous innovation from incumbent players. End-user demographics are primarily driven by semiconductor fabrication plants (fabs) and advanced research laboratories requiring precise process control. Mergers and acquisitions (M&A) are observed, albeit at a moderate pace, as larger entities seek to expand their sensor portfolios and gain market share. For instance, the market saw an estimated XX M&A deal volumes during the historical period (2019-2024). Barriers to innovation include the high cost of research and development for specialized semiconductor-grade sensors and the complex validation processes required.

- Market Concentration: Moderate, with a few key players holding significant market share.

- Technological Innovation Drivers: Increasing demand for ultra-pure water, stricter process control, and miniaturization of semiconductor components.

- Regulatory Frameworks: Stringent environmental regulations and industry-specific quality standards (e.g., SEMI standards).

- Competitive Product Substitutes: While direct substitutes for high-precision semiconductor applications are scarce, alternative water quality monitoring methods can pose indirect competition.

- End-User Demographics: Primarily semiconductor fabrication plants, wafer manufacturers, and research and development facilities.

- M&A Trends: Moderate activity, driven by portfolio expansion and market consolidation. Estimated XX deal volumes (2019-2024).

- Innovation Barriers: High R&D costs, complex validation procedures, and the need for specialized materials.

Dissolved Oxygen Sensors for Semiconductor Growth Trends & Insights

The Dissolved Oxygen Sensors for Semiconductor market is projected to experience robust growth, driven by the ever-expanding semiconductor industry's insatiable demand for high-purity water and increasingly sophisticated process control. The market size for DO sensors in semiconductor applications, estimated at approximately $XX billion in 2025, is anticipated to grow at a Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025-2033). This upward trajectory is fueled by several key trends, including the escalating complexity of semiconductor manufacturing processes that necessitate precise monitoring of dissolved oxygen levels to prevent defects and optimize yields. Adoption rates for advanced DO sensor technologies, particularly optical and advanced polarographic methods, are on the rise as fabs seek greater accuracy and reliability. Technological disruptions, such as the development of in-line, real-time monitoring systems and the integration of AI for predictive maintenance of sensors, are poised to further accelerate adoption. Consumer behavior shifts, from a reactive approach to quality control to a proactive, data-driven strategy, are also influencing the demand for sophisticated DO sensing solutions. The overall market penetration of specialized DO sensors within the semiconductor industry is projected to increase significantly as awareness of their critical role in yield enhancement and cost reduction grows. The parent market, encompassing broader industrial water quality monitoring solutions, provides a foundational market upon which the specialized semiconductor segment thrives, with the semiconductor segment itself representing a substantial and rapidly growing child market.

Dominant Regions, Countries, or Segments in Dissolved Oxygen Sensors for Semiconductor

The Asia-Pacific region, spearheaded by China, South Korea, Taiwan, and Japan, is the dominant force in the Dissolved Oxygen Sensors for Semiconductor market. This regional dominance is underpinned by the concentration of the world's leading semiconductor manufacturing hubs and the relentless drive for technological advancement in these nations. Within this region, China's burgeoning semiconductor industry, supported by substantial government investment and ambitious domestic production targets, is a particularly strong growth engine. The Semiconductor Industrial application segment is the primary driver of market growth, accounting for an estimated XX% of the total market revenue in 2025. This dominance is attributed to the critical need for precise dissolved oxygen monitoring in ultra-pure water used in wafer fabrication processes, etching, cleaning, and other critical manufacturing steps. The Polarography Method, while a mature technology, continues to hold a significant market share due to its established reliability and cost-effectiveness in certain applications. However, the Optical Method is experiencing accelerated growth due to its non-consumable nature, reduced maintenance, and enhanced accuracy in challenging semiconductor environments, representing a key technological shift. Economic policies in these dominant regions, including incentives for domestic semiconductor production and stringent environmental regulations mandating efficient water usage and quality, further bolster the demand for advanced DO sensing solutions. Infrastructure development, including the expansion of semiconductor fabrication facilities, directly correlates with the increased adoption of these sensors. Market share within the Asia-Pacific region for DO sensors in semiconductor applications is estimated to be approximately XX% of the global market in 2025, with a projected growth rate of XX% during the forecast period.

- Dominant Region: Asia-Pacific (China, South Korea, Taiwan, Japan).

- Key Drivers in Asia-Pacific:

- Concentration of global semiconductor manufacturing hubs.

- Government initiatives and investments in the semiconductor sector.

- Strict environmental regulations.

- Extensive infrastructure development for semiconductor fabs.

- Dominant Application Segment: Semiconductor Industrial.

- Market Share (2025): Estimated XX% of the total market.

- Growth Potential: High, driven by increasing semiconductor production and process sophistication.

- Dominant Sensor Type (by adoption trend): Optical Method (experiencing rapid growth), Polarography Method (established, significant share).

- Market Share (2025) - Polarography: Estimated XX%.

- Market Share (2025) - Optical: Estimated XX%.

Dissolved Oxygen Sensors for Semiconductor Product Landscape

The product landscape for Dissolved Oxygen Sensors in the Semiconductor market is defined by continuous innovation focused on enhanced accuracy, reduced footprint, and seamless integration into complex manufacturing systems. Manufacturers are increasingly offering compact, in-line sensors capable of real-time, non-invasive monitoring of dissolved oxygen levels in ultra-pure water circuits. Key technological advancements include the development of sensors with lower detection limits, improved resistance to process chemicals, and enhanced long-term stability. Optical DO sensors are gaining traction due to their maintenance-free operation and resistance to fouling, offering a significant advantage in semiconductor cleanroom environments. Unique selling propositions revolve around superior calibration capabilities, digital output signals for easy data integration, and compliance with stringent semiconductor industry standards.

Key Drivers, Barriers & Challenges in Dissolved Oxygen Sensors for Semiconductor

Key Drivers:

- Increasing Demand for Ultra-Pure Water: The semiconductor industry's reliance on ultra-pure water necessitates precise monitoring of dissolved oxygen to prevent contamination and ensure process integrity.

- Advancements in Semiconductor Manufacturing: The drive for smaller, more complex chips requires tighter process control, where DO levels are a critical parameter.

- Focus on Yield Optimization and Cost Reduction: Accurate DO monitoring directly contributes to reduced defect rates and improved manufacturing yields, leading to significant cost savings.

- Environmental Regulations: Growing emphasis on water conservation and responsible water management in industrial processes drives the adoption of efficient monitoring technologies.

- Technological Evolution of Sensors: Developments in optical and advanced polarographic sensor technologies offer greater accuracy, reliability, and ease of use.

Barriers & Challenges:

- High Cost of Specialized Sensors: Semiconductor-grade DO sensors, with their stringent specifications, can be expensive, posing a barrier for smaller fabs or research institutions.

- Complex Integration and Calibration: Integrating new sensor systems into existing fab infrastructure and ensuring accurate calibration can be a time-consuming and resource-intensive process.

- Stringent Purity Requirements: The extreme purity demands of semiconductor manufacturing mean that sensors themselves must not introduce any contaminants into the water.

- Competition from Traditional Water Quality Monitoring: While not direct substitutes for critical semiconductor processes, broader water quality monitoring solutions can pose indirect competition in less demanding applications.

- Supply Chain Volatility: Global supply chain disruptions can impact the availability and lead times of specialized sensor components and finished products. For instance, the historical period saw an estimated XX% increase in lead times for critical sensor components due to supply chain issues.

Emerging Opportunities in Dissolved Oxygen Sensors for Semiconductor

Emerging opportunities in the Dissolved Oxygen Sensors for Semiconductor market lie in the development of smart, connected sensing solutions. The integration of IoT capabilities, cloud-based data analytics, and AI for predictive maintenance of DO sensors presents a significant growth avenue. Furthermore, the expansion of the semiconductor industry into new geographical regions and the increasing demand for smaller, more portable DO sensor solutions for on-site process verification offer untapped market potential. The development of highly specialized DO sensors for emerging semiconductor manufacturing techniques, such as advanced lithography and 3D IC fabrication, also represents a significant opportunity for innovation and market penetration.

Growth Accelerators in the Dissolved Oxygen Sensors for Semiconductor Industry

Long-term growth in the Dissolved Oxygen Sensors for Semiconductor industry will be significantly accelerated by continuous technological breakthroughs, particularly in the realm of optical sensing technologies, which promise enhanced performance and reduced maintenance. Strategic partnerships between sensor manufacturers and leading semiconductor equipment providers are crucial for co-developing integrated solutions that meet the evolving needs of fab operators. Furthermore, aggressive market expansion strategies targeting emerging semiconductor manufacturing centers in regions like Southeast Asia and Eastern Europe will unlock new revenue streams. The increasing adoption of Industry 4.0 principles within semiconductor manufacturing will also act as a major growth accelerator, driving demand for sensor data and sophisticated monitoring systems.

Key Players Shaping the Dissolved Oxygen Sensors for Semiconductor Market

- Entegris

- HORIBA

- ABB

- M4 Knick

- Walchem

- Sensorex

- Hach

- Mettler-Toledo

- RS Hydro

- Emerson

Notable Milestones in Dissolved Oxygen Sensors for Semiconductor Sector

- 2019: Launch of next-generation optical DO sensors with enhanced accuracy and durability for semiconductor applications.

- 2020: Introduction of advanced data logging and remote monitoring capabilities for industrial DO sensor systems.

- 2021: Acquisition of a specialized water quality sensor company by a major player to bolster its semiconductor portfolio.

- 2022: Development of new sensor materials resistant to aggressive chemicals used in advanced semiconductor etching processes.

- 2023: Increased focus on IoT integration and AI-driven analytics for predictive maintenance of DO sensors.

- 2024: Introduction of ultra-compact, in-line DO sensors for micro-fabrication processes.

In-Depth Dissolved Oxygen Sensors for Semiconductor Market Outlook

The future outlook for the Dissolved Oxygen Sensors for Semiconductor market is exceptionally bright, driven by sustained growth in the global semiconductor industry and the increasing criticality of precise water quality monitoring. Key growth accelerators, including advancements in optical sensor technology and the widespread adoption of Industry 4.0 principles, will continue to propel market expansion. Strategic opportunities lie in the development of smart, integrated sensing platforms that offer real-time data analytics and predictive maintenance capabilities. As semiconductor manufacturing processes become more complex and demand for ultra-high purity water intensifies, the indispensable role of sophisticated dissolved oxygen sensors will only grow, presenting a lucrative landscape for innovation and investment. The market is poised for significant expansion, with estimated future market potential reaching $XX billion by 2033.

Dissolved Oxygen Sensors for Semiconductor Segmentation

-

1. Application

- 1.1. Semiconductor Industrial

- 1.2. Laboratory

-

2. Types

- 2.1. Polarography Method

- 2.2. Current Method

- 2.3. Optical Method

Dissolved Oxygen Sensors for Semiconductor Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Dissolved Oxygen Sensors for Semiconductor Regional Market Share

Geographic Coverage of Dissolved Oxygen Sensors for Semiconductor

Dissolved Oxygen Sensors for Semiconductor REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.45% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Semiconductor Industrial

- 5.1.2. Laboratory

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Polarography Method

- 5.2.2. Current Method

- 5.2.3. Optical Method

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Dissolved Oxygen Sensors for Semiconductor Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Semiconductor Industrial

- 6.1.2. Laboratory

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Polarography Method

- 6.2.2. Current Method

- 6.2.3. Optical Method

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Dissolved Oxygen Sensors for Semiconductor Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Semiconductor Industrial

- 7.1.2. Laboratory

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Polarography Method

- 7.2.2. Current Method

- 7.2.3. Optical Method

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Dissolved Oxygen Sensors for Semiconductor Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Semiconductor Industrial

- 8.1.2. Laboratory

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Polarography Method

- 8.2.2. Current Method

- 8.2.3. Optical Method

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Dissolved Oxygen Sensors for Semiconductor Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Semiconductor Industrial

- 9.1.2. Laboratory

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Polarography Method

- 9.2.2. Current Method

- 9.2.3. Optical Method

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Dissolved Oxygen Sensors for Semiconductor Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Semiconductor Industrial

- 10.1.2. Laboratory

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Polarography Method

- 10.2.2. Current Method

- 10.2.3. Optical Method

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Dissolved Oxygen Sensors for Semiconductor Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Semiconductor Industrial

- 11.1.2. Laboratory

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Polarography Method

- 11.2.2. Current Method

- 11.2.3. Optical Method

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Entegris

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 HORIBA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 ABB

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 M4 Knick

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Walchem

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Sensorex

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Hach

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Mettler-Toledo

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 RS Hydro

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Emerson

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Entegris

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Dissolved Oxygen Sensors for Semiconductor Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Dissolved Oxygen Sensors for Semiconductor Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Dissolved Oxygen Sensors for Semiconductor Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Dissolved Oxygen Sensors for Semiconductor Volume (K), by Application 2025 & 2033

- Figure 5: North America Dissolved Oxygen Sensors for Semiconductor Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Dissolved Oxygen Sensors for Semiconductor Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Dissolved Oxygen Sensors for Semiconductor Revenue (billion), by Types 2025 & 2033

- Figure 8: North America Dissolved Oxygen Sensors for Semiconductor Volume (K), by Types 2025 & 2033

- Figure 9: North America Dissolved Oxygen Sensors for Semiconductor Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Dissolved Oxygen Sensors for Semiconductor Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Dissolved Oxygen Sensors for Semiconductor Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Dissolved Oxygen Sensors for Semiconductor Volume (K), by Country 2025 & 2033

- Figure 13: North America Dissolved Oxygen Sensors for Semiconductor Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Dissolved Oxygen Sensors for Semiconductor Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Dissolved Oxygen Sensors for Semiconductor Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Dissolved Oxygen Sensors for Semiconductor Volume (K), by Application 2025 & 2033

- Figure 17: South America Dissolved Oxygen Sensors for Semiconductor Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Dissolved Oxygen Sensors for Semiconductor Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Dissolved Oxygen Sensors for Semiconductor Revenue (billion), by Types 2025 & 2033

- Figure 20: South America Dissolved Oxygen Sensors for Semiconductor Volume (K), by Types 2025 & 2033

- Figure 21: South America Dissolved Oxygen Sensors for Semiconductor Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Dissolved Oxygen Sensors for Semiconductor Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Dissolved Oxygen Sensors for Semiconductor Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Dissolved Oxygen Sensors for Semiconductor Volume (K), by Country 2025 & 2033

- Figure 25: South America Dissolved Oxygen Sensors for Semiconductor Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Dissolved Oxygen Sensors for Semiconductor Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Dissolved Oxygen Sensors for Semiconductor Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Dissolved Oxygen Sensors for Semiconductor Volume (K), by Application 2025 & 2033

- Figure 29: Europe Dissolved Oxygen Sensors for Semiconductor Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Dissolved Oxygen Sensors for Semiconductor Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Dissolved Oxygen Sensors for Semiconductor Revenue (billion), by Types 2025 & 2033

- Figure 32: Europe Dissolved Oxygen Sensors for Semiconductor Volume (K), by Types 2025 & 2033

- Figure 33: Europe Dissolved Oxygen Sensors for Semiconductor Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Dissolved Oxygen Sensors for Semiconductor Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Dissolved Oxygen Sensors for Semiconductor Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Dissolved Oxygen Sensors for Semiconductor Volume (K), by Country 2025 & 2033

- Figure 37: Europe Dissolved Oxygen Sensors for Semiconductor Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Dissolved Oxygen Sensors for Semiconductor Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Dissolved Oxygen Sensors for Semiconductor Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Dissolved Oxygen Sensors for Semiconductor Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Dissolved Oxygen Sensors for Semiconductor Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Dissolved Oxygen Sensors for Semiconductor Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Dissolved Oxygen Sensors for Semiconductor Revenue (billion), by Types 2025 & 2033

- Figure 44: Middle East & Africa Dissolved Oxygen Sensors for Semiconductor Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Dissolved Oxygen Sensors for Semiconductor Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Dissolved Oxygen Sensors for Semiconductor Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Dissolved Oxygen Sensors for Semiconductor Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Dissolved Oxygen Sensors for Semiconductor Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Dissolved Oxygen Sensors for Semiconductor Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Dissolved Oxygen Sensors for Semiconductor Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Dissolved Oxygen Sensors for Semiconductor Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Dissolved Oxygen Sensors for Semiconductor Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Dissolved Oxygen Sensors for Semiconductor Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Dissolved Oxygen Sensors for Semiconductor Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Dissolved Oxygen Sensors for Semiconductor Revenue (billion), by Types 2025 & 2033

- Figure 56: Asia Pacific Dissolved Oxygen Sensors for Semiconductor Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Dissolved Oxygen Sensors for Semiconductor Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Dissolved Oxygen Sensors for Semiconductor Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Dissolved Oxygen Sensors for Semiconductor Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Dissolved Oxygen Sensors for Semiconductor Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Dissolved Oxygen Sensors for Semiconductor Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Dissolved Oxygen Sensors for Semiconductor Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Types 2020 & 2033

- Table 4: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Types 2020 & 2033

- Table 10: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Types 2020 & 2033

- Table 22: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Types 2020 & 2033

- Table 34: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Types 2020 & 2033

- Table 58: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Types 2020 & 2033

- Table 76: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Dissolved Oxygen Sensors for Semiconductor Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Dissolved Oxygen Sensors for Semiconductor Volume K Forecast, by Country 2020 & 2033

- Table 79: China Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Dissolved Oxygen Sensors for Semiconductor Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Dissolved Oxygen Sensors for Semiconductor Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Dissolved Oxygen Sensors for Semiconductor?

The projected CAGR is approximately 11.45%.

2. Which companies are prominent players in the Dissolved Oxygen Sensors for Semiconductor?

Key companies in the market include Entegris, HORIBA, ABB, M4 Knick, Walchem, Sensorex, Hach, Mettler-Toledo, RS Hydro, Emerson.

3. What are the main segments of the Dissolved Oxygen Sensors for Semiconductor?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 11.16 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Dissolved Oxygen Sensors for Semiconductor," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Dissolved Oxygen Sensors for Semiconductor report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Dissolved Oxygen Sensors for Semiconductor?

To stay informed about further developments, trends, and reports in the Dissolved Oxygen Sensors for Semiconductor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence