Key Insights

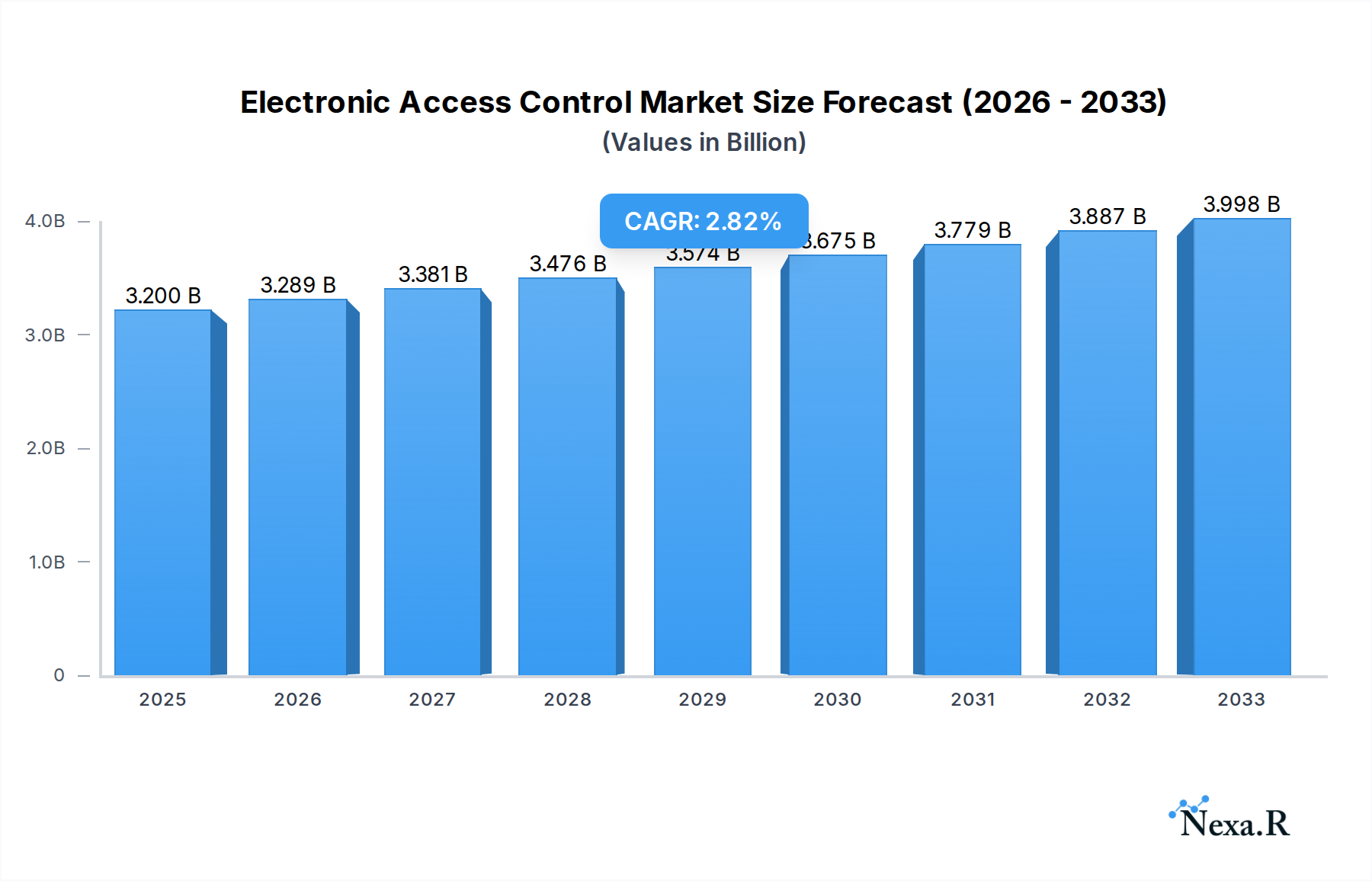

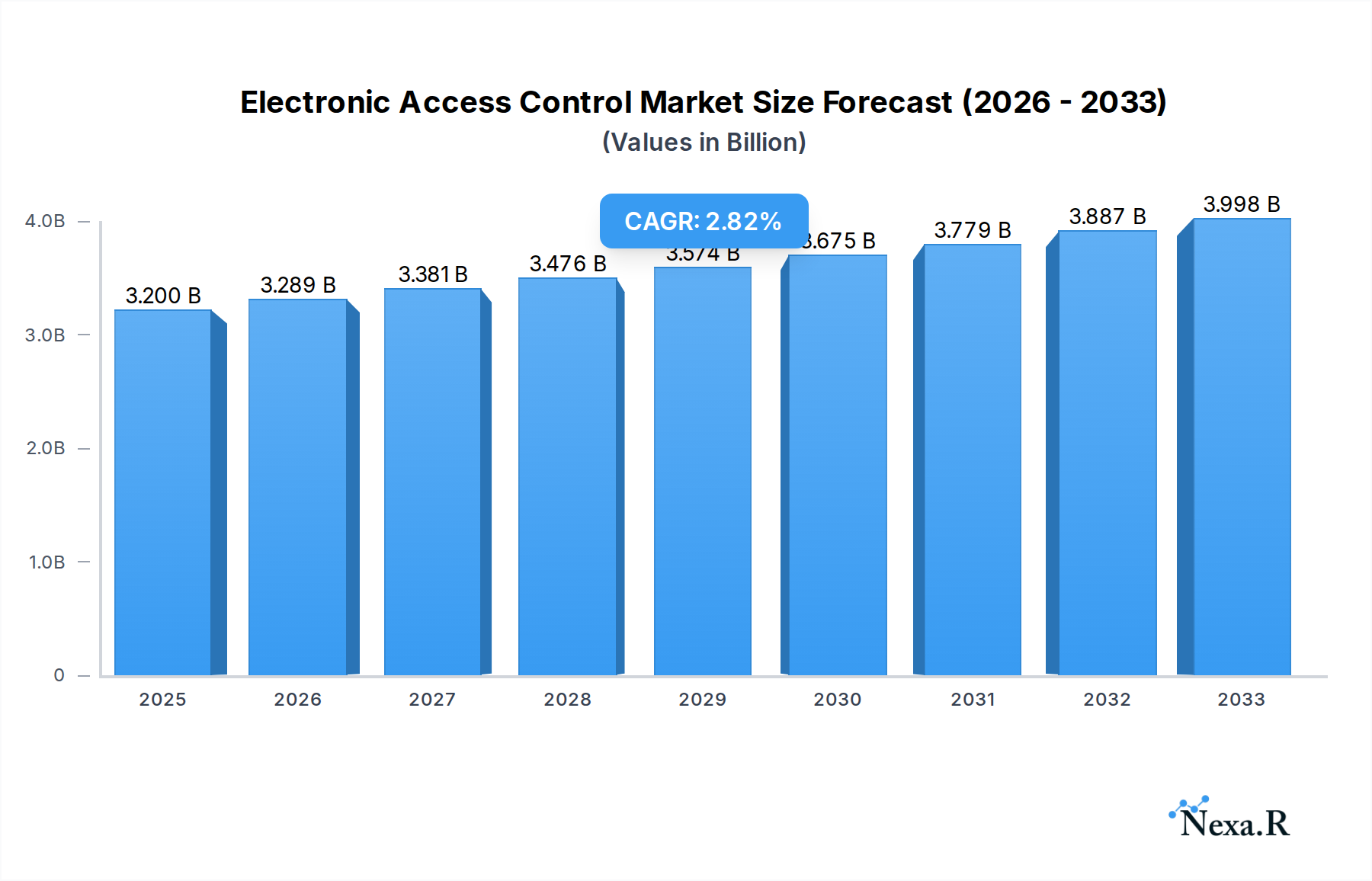

The global Electronic Access Control (EAC) market is projected to reach USD 15.5 billion by 2025, demonstrating a robust Compound Annual Growth Rate (CAGR) of 2.8% from 2025. This expansion is primarily driven by the increasing imperative for advanced security solutions across various industries. Organizations are prioritizing the safeguarding of critical assets, sensitive information, and personnel, making sophisticated access control systems essential. The rise in sophisticated security threats, coupled with the widespread adoption of smart building technologies and the Internet of Things (IoT), is further accelerating the demand for integrated and intelligent EAC solutions. Innovation is a key market characteristic, with continuous development of advanced features such as mobile credentialing, cloud-based management, and AI-powered analytics to enhance user experience and security.

Electronic Access Control Market Size (In Billion)

Market segmentation highlights key growth areas. The Commercial sector leads EAC adoption, driven by the stringent security demands of office buildings, retail environments, and hospitality establishments. The Industrial sector also shows significant demand, particularly in manufacturing, critical infrastructure, and logistics, where robust access control is vital for operational integrity and safety. While Residential applications are expanding due to smart home trends and enhanced personal security awareness, the commercial and industrial segments are currently the primary market drivers. In terms of technology, Card-based Electronic Access Control retains a substantial market share due to its proven reliability and cost-effectiveness. However, Biometric Electronic Access Control is experiencing accelerated growth, owing to its superior security features and user convenience, with fingerprint, facial recognition, and iris scanning technologies gaining prominence. Key industry players are actively investing in research and development to deliver innovative solutions aligned with evolving security needs and technological advancements.

Electronic Access Control Company Market Share

Comprehensive Electronic Access Control Market Report: 2019-2033

This in-depth report provides a definitive analysis of the global Electronic Access Control (EAC) market, offering critical insights for stakeholders, investors, and industry professionals. Spanning the historical period from 2019 to 2024 and projecting growth through 2033, with a base year of 2025, this report delves into market dynamics, growth trends, regional dominance, product landscapes, and key influencing factors. Our analysis incorporates a parent and child market perspective, ensuring a holistic understanding of the EAC ecosystem. With millions of units as the standard for quantitative data, this report delivers actionable intelligence to navigate this rapidly evolving sector.

Electronic Access Control Market Dynamics & Structure

The Electronic Access Control (EAC) market is characterized by a moderately consolidated structure, with dominant players like Honeywell, ASSA Abloy, SIEMENS, Johnson Controls, and BOSCH Security holding significant market share. Technological innovation serves as a primary driver, fueled by advancements in biometrics (fingerprint, facial recognition), IoT integration, and cloud-based solutions, enhancing security and user convenience. Regulatory frameworks, such as data privacy laws (e.g., GDPR) and building security standards, are increasingly influencing product development and deployment strategies. Competitive product substitutes, including traditional key-based systems and emerging AI-powered security platforms, present ongoing challenges. End-user demographics are shifting towards a greater demand for smart, integrated security solutions across commercial, industrial, and residential applications. Merger and acquisition (M&A) trends are active, with larger entities acquiring specialized technology firms to expand their portfolios and market reach.

- Market Concentration: The top five companies are estimated to hold approximately 55% of the global EAC market share.

- Technological Innovation Drivers: Increased adoption of AI in facial recognition systems and the integration of EAC with smart home ecosystems are key innovation areas.

- Regulatory Frameworks: Compliance with data protection regulations is a critical factor for market players.

- Competitive Product Substitutes: Traditional mechanical locks and rudimentary alarm systems represent a smaller, though persistent, segment of the security market.

- End-User Demographics: Growing demand for remote access management and mobile credentialing across all sectors.

- M&A Trends: The historical period saw over 20 significant M&A deals, with an average deal value of $XX million.

Electronic Access Control Growth Trends & Insights

The Electronic Access Control (EAC) market is poised for substantial growth, driven by an escalating demand for enhanced security, convenience, and sophisticated access management solutions across diverse applications. The market size evolution is marked by a steady upward trajectory, projected to reach approximately $35,000 million by 2033. Adoption rates for advanced EAC systems, particularly biometrics and mobile credentialing, are accelerating, moving beyond traditional card-based solutions. Technological disruptions, such as the integration of artificial intelligence (AI) for intelligent threat detection and the proliferation of the Internet of Things (IoT) enabling seamless connectivity and remote management, are reshaping the market landscape. Consumer behavior shifts are evident in the increasing preference for integrated security systems that offer unified control and monitoring capabilities, merging access control with video surveillance and alarm systems. The convenience offered by smartphone-based access and the growing awareness of sophisticated security threats are compelling businesses and individuals to invest in next-generation EAC solutions. The historical period (2019-2024) witnessed a Compound Annual Growth Rate (CAGR) of approximately 8.5%, with an estimated market size of $18,000 million in 2024. This growth is further bolstered by smart city initiatives and the increasing need for secure access in critical infrastructure. The penetration of EAC solutions in the residential sector is steadily increasing, driven by smart home technology adoption and the desire for enhanced personal security. Furthermore, the industrial sector's focus on mitigating insider threats and managing complex access hierarchies is a significant growth catalyst. The "Others" segment, encompassing sectors like healthcare, education, and transportation, is also exhibiting robust growth due to specialized security requirements. The continuous refinement of biometric technologies, offering higher accuracy and faster processing times, along with the development of more secure and user-friendly mobile access solutions, are key factors driving market expansion. The increasing affordability of these advanced systems is also contributing to their wider adoption across small and medium-sized enterprises.

Dominant Regions, Countries, or Segments in Electronic Access Control

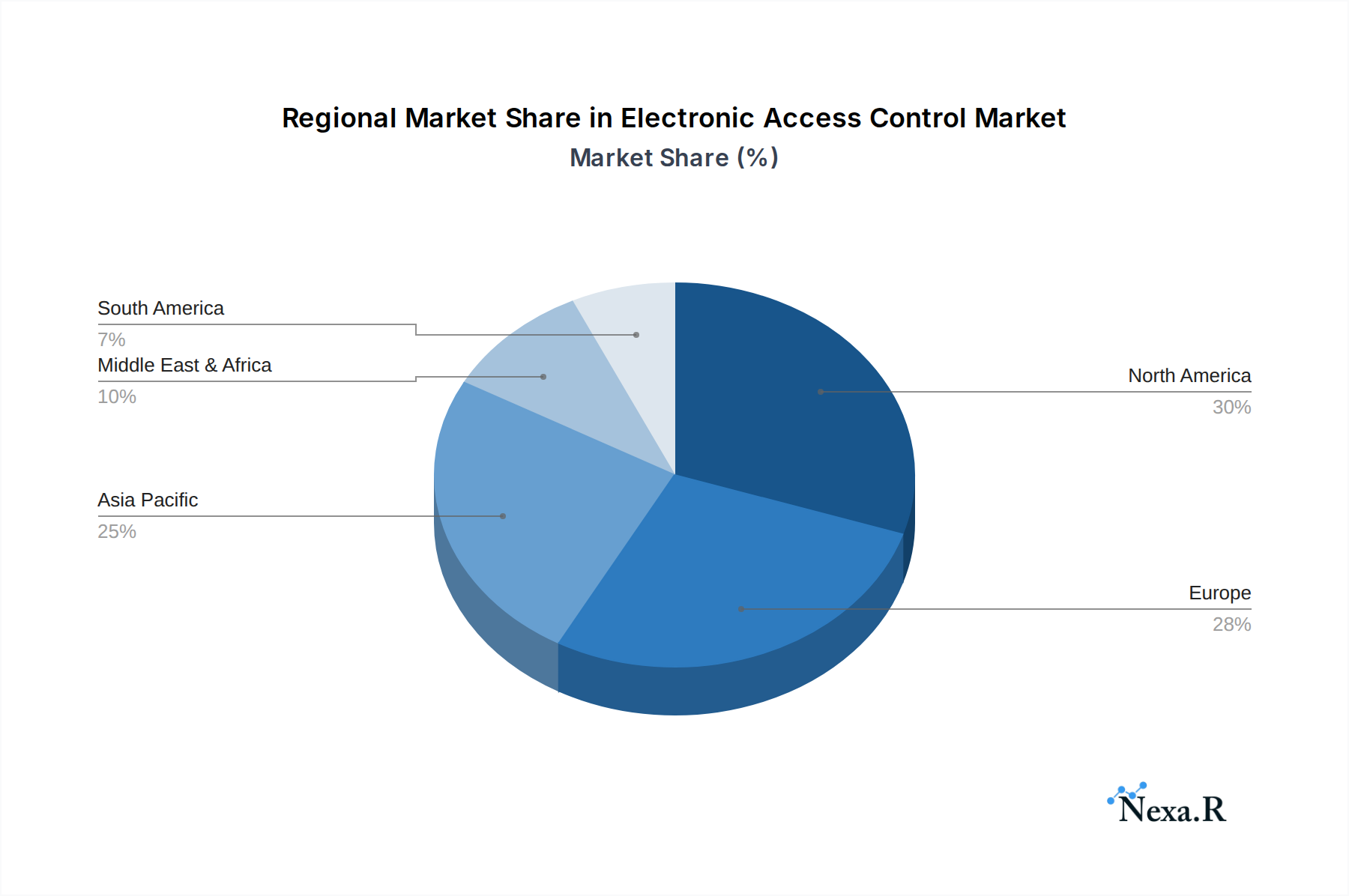

The Commercial application segment is currently the dominant force driving growth within the global Electronic Access Control (EAC) market, accounting for an estimated 45% of the total market share in the base year of 2025. This dominance is propelled by a confluence of factors, including the expanding corporate real estate sector, the increasing need for sophisticated security in office buildings, retail spaces, and hospitality venues, and the growing trend of smart building integration. The high demand for robust access management solutions to protect sensitive data, assets, and personnel within these environments makes commercial applications a prime target for EAC providers. North America, particularly the United States, stands out as the leading country due to its early adoption of advanced security technologies, strong economic policies supporting technological investment, and a mature market for both commercial and residential security solutions. The region benefits from extensive infrastructure development, a high concentration of businesses, and a well-established cybersecurity industry.

In terms of EAC types, Card-based Electronic Access Control continues to hold a significant market share, estimated at 50% in 2025, due to its established infrastructure, proven reliability, and cost-effectiveness for many applications. However, the fastest growth is anticipated in the Biometrics Electronic Access Control segment, which is projected to witness a CAGR of 12% over the forecast period (2025-2033). This surge is attributed to advancements in fingerprint, facial recognition, and iris scanning technologies, offering enhanced security and convenience, and a reduced risk of credential loss or theft. The increasing adoption of mobile credentials, leveraging smartphones as access devices, is also contributing to the growth of the "Others" type segment, which includes wireless and cloud-based solutions, and is projected to grow at a CAGR of 10%.

- Commercial Application Dominance:

- High demand for secure access in enterprise environments and data centers.

- Integration with building management systems (BMS) for comprehensive control.

- Increasing adoption of smart office technologies and visitor management systems.

- Market share estimated at $15,750 million in 2025.

- North America's Leading Role:

- Strong economic policies favoring security investments.

- High penetration of smart home and smart building technologies.

- Presence of major EAC technology developers and integrators.

- Projected to account for 35% of the global market revenue in 2025.

- Card-based EAC's Enduring Strength:

- Widespread existing infrastructure and user familiarity.

- Cost-effectiveness for mass deployment in various commercial settings.

- Market share estimated at $17,500 million in 2025.

- Biometrics' Rapid Ascendancy:

- Enhanced security through unique personal identification.

- Growing adoption in high-security environments like government facilities and financial institutions.

- Significant technological advancements improving accuracy and speed.

- Projected to reach $10,500 million by 2033.

- Emergence of Mobile & Cloud-Based Solutions:

- Increased user preference for smartphone-based access and remote management.

- Scalability and flexibility offered by cloud-based platforms.

- Significant growth potential in the residential and SMB sectors.

Electronic Access Control Product Landscape

The electronic access control product landscape is characterized by continuous innovation focused on enhancing security, user experience, and integration capabilities. Key product categories include advanced card readers supporting multiple credential technologies (e.g., MIFARE, DESFire), sophisticated biometric readers employing fingerprint, facial, and iris recognition with high accuracy rates, and mobile access solutions enabling smartphone-based entry. Performance metrics emphasize faster read speeds, enhanced encryption standards, and reduced false acceptance/rejection rates for biometrics. Unique selling propositions often lie in seamless integration with existing IT infrastructures, cloud-based management platforms for remote access and analytics, and robust cybersecurity features to protect against breaches.

Key Drivers, Barriers & Challenges in Electronic Access Control

The Electronic Access Control (EAC) market is propelled by several key drivers, primarily the escalating global security concerns, driving the demand for more advanced and reliable access management solutions. The proliferation of smart technologies and the Internet of Things (IoT) facilitates the integration of EAC systems with other building management and security platforms, creating a more comprehensive and convenient security ecosystem. Technological advancements in biometrics, such as facial recognition and fingerprint scanning, offer higher levels of security and user-friendliness. Furthermore, increasing government regulations and industry standards mandating stricter security protocols in critical infrastructure and commercial establishments are significant growth accelerators.

However, the market also faces significant barriers and challenges. High initial investment costs for advanced EAC systems can deter adoption, especially for small and medium-sized businesses. Concerns over data privacy and the security of biometric data, coupled with potential implementation complexities and the need for specialized technical expertise, can also hinder market penetration. Supply chain disruptions, particularly for electronic components, can lead to increased lead times and costs. Moreover, competition from less sophisticated, but more affordable, traditional security solutions remains a factor. Cybersecurity threats targeting EAC systems themselves pose an ongoing challenge, requiring continuous updates and robust protection measures.

- Key Drivers:

- Rising global security threats and terrorism concerns.

- IoT integration and smart building advancements.

- Technological evolution in biometrics and mobile credentials.

- Stringent regulatory compliance requirements.

- Barriers & Challenges:

- High upfront investment costs for advanced systems.

- Data privacy concerns and cybersecurity vulnerabilities.

- Complexity of integration and need for skilled personnel.

- Supply chain volatility impacting component availability and pricing.

- Persistent competition from traditional security methods.

Emerging Opportunities in Electronic Access Control

Emerging opportunities in the Electronic Access Control (EAC) market are largely driven by the increasing demand for integrated and intelligent security solutions. The expansion of EAC into the residential sector, fueled by the smart home revolution and the desire for enhanced home security, presents a significant untapped market. The healthcare industry's need for stringent access control to protect patient data and sensitive medical equipment offers another substantial growth avenue. Furthermore, the development of AI-powered EAC systems capable of proactive threat detection, behavioral analysis, and predictive security is a key emerging trend. The growing adoption of cloud-based EAC platforms, offering scalability, remote management, and advanced analytics, is creating new business models and service opportunities. The "Others" market segment, including transportation hubs, educational institutions, and government facilities, is also ripe for innovative EAC deployments tailored to specific security needs.

Growth Accelerators in the Electronic Access Control Industry

Several key factors are acting as growth accelerators for the Electronic Access Control (EAC) industry. The continuous evolution and decreasing cost of biometric technologies, making them more accessible for mainstream applications, are a significant catalyst. The widespread adoption of smartphones and the development of robust mobile credentialing technologies are revolutionizing access control, offering unparalleled convenience and flexibility. Strategic partnerships between EAC manufacturers and smart home ecosystem providers are fostering greater integration and market penetration in the residential sector. Furthermore, the increasing focus on cybersecurity and the demand for end-to-end security solutions are driving innovation and adoption of advanced EAC systems with built-in threat mitigation capabilities. Investments in research and development by leading companies, aimed at creating more intelligent, user-friendly, and secure EAC solutions, are also playing a crucial role in accelerating market growth.

Key Players Shaping the Electronic Access Control Market

- Honeywell

- ASSA Abloy

- SIEMENS

- Johnson Controls

- BOSCH Security

- DDS

- ADT LLC

- Dorma

- KABA Group

- Schneider

- Suprema

- Southco

- SALTO

- Nortek Control

- Panasonic

- Millennium

- Digital Monitoring Products

- Gallagher

- Allegion

- Integrated

Notable Milestones in Electronic Access Control Sector

- 2019: Introduction of advanced AI-powered facial recognition EAC systems by leading manufacturers, offering enhanced accuracy and real-time threat detection.

- 2020: Increased adoption of cloud-based EAC solutions, enabling remote management and scalability, particularly for SMBs.

- 2021: Significant advancements in mobile credentialing technology, with broader smartphone compatibility and enhanced security protocols.

- 2022: Major security breaches and heightened awareness leading to increased investment in multi-factor authentication and robust EAC solutions.

- 2023: Mergers and acquisitions activity intensified as larger players sought to consolidate market share and acquire innovative technologies.

- 2024: Growing emphasis on interoperability and open standards, allowing EAC systems to integrate seamlessly with a wider range of building and security platforms.

In-Depth Electronic Access Control Market Outlook

The future outlook for the Electronic Access Control (EAC) market remains exceptionally strong, driven by sustained demand for advanced security and the relentless pace of technological innovation. The convergence of IoT, AI, and advanced biometrics will continue to define the market, creating intelligent and adaptive security ecosystems. Growth accelerators such as the burgeoning smart home market, the critical need for robust access management in the healthcare and industrial sectors, and the development of cost-effective biometric solutions will fuel significant expansion. Strategic partnerships and a continued focus on cybersecurity will be paramount for market leaders. The global EAC market is projected for robust growth, with strategic opportunities in emerging economies and specialized application areas, positioning it as a critical component of future security infrastructure.

Electronic Access Control Segmentation

-

1. Application

- 1.1. Commercial

- 1.2. Industrial

- 1.3. Residential

- 1.4. Others

-

2. Types

- 2.1. Card-based Electronic Access Control

- 2.2. Biometrics Electronic Access Control

- 2.3. Others

Electronic Access Control Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Electronic Access Control Regional Market Share

Geographic Coverage of Electronic Access Control

Electronic Access Control REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial

- 5.1.2. Industrial

- 5.1.3. Residential

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Card-based Electronic Access Control

- 5.2.2. Biometrics Electronic Access Control

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Electronic Access Control Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial

- 6.1.2. Industrial

- 6.1.3. Residential

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Card-based Electronic Access Control

- 6.2.2. Biometrics Electronic Access Control

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Electronic Access Control Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial

- 7.1.2. Industrial

- 7.1.3. Residential

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Card-based Electronic Access Control

- 7.2.2. Biometrics Electronic Access Control

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Electronic Access Control Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial

- 8.1.2. Industrial

- 8.1.3. Residential

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Card-based Electronic Access Control

- 8.2.2. Biometrics Electronic Access Control

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Electronic Access Control Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial

- 9.1.2. Industrial

- 9.1.3. Residential

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Card-based Electronic Access Control

- 9.2.2. Biometrics Electronic Access Control

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Electronic Access Control Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial

- 10.1.2. Industrial

- 10.1.3. Residential

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Card-based Electronic Access Control

- 10.2.2. Biometrics Electronic Access Control

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Electronic Access Control Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Commercial

- 11.1.2. Industrial

- 11.1.3. Residential

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Card-based Electronic Access Control

- 11.2.2. Biometrics Electronic Access Control

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Honeywell

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ASSA Abloy

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 SIEMENS

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Johnson Controls

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 BOSCH Security

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 DDS

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 ADT LLC

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Dorma

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 KABA Group

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Schneider

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Suprema

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Southco

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 SALTO

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Nortek Control

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Panasonic

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Millennium

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Digital Monitoring Products

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Gallagher

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Allegion

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Integrated

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.1 Honeywell

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Electronic Access Control Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Electronic Access Control Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Electronic Access Control Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Electronic Access Control Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Electronic Access Control Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Electronic Access Control Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Electronic Access Control Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Electronic Access Control Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Electronic Access Control Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Electronic Access Control Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Electronic Access Control Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Electronic Access Control Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Electronic Access Control Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Electronic Access Control Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Electronic Access Control Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Electronic Access Control Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Electronic Access Control Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Electronic Access Control Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Electronic Access Control Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Electronic Access Control Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Electronic Access Control Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Electronic Access Control Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Electronic Access Control Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Electronic Access Control Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Electronic Access Control Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Electronic Access Control Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Electronic Access Control Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Electronic Access Control Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Electronic Access Control Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Electronic Access Control Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Electronic Access Control Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Electronic Access Control Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Electronic Access Control Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Electronic Access Control Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Electronic Access Control Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Electronic Access Control Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Electronic Access Control Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Electronic Access Control Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Electronic Access Control Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Electronic Access Control Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Electronic Access Control Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Electronic Access Control Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Electronic Access Control Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Electronic Access Control Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Electronic Access Control Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Electronic Access Control Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Electronic Access Control Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Electronic Access Control Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Electronic Access Control Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Electronic Access Control Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Electronic Access Control?

The projected CAGR is approximately 2.8%.

2. Which companies are prominent players in the Electronic Access Control?

Key companies in the market include Honeywell, ASSA Abloy, SIEMENS, Johnson Controls, BOSCH Security, DDS, ADT LLC, Dorma, KABA Group, Schneider, Suprema, Southco, SALTO, Nortek Control, Panasonic, Millennium, Digital Monitoring Products, Gallagher, Allegion, Integrated.

3. What are the main segments of the Electronic Access Control?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.2 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Electronic Access Control," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Electronic Access Control report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Electronic Access Control?

To stay informed about further developments, trends, and reports in the Electronic Access Control, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence