Key Insights

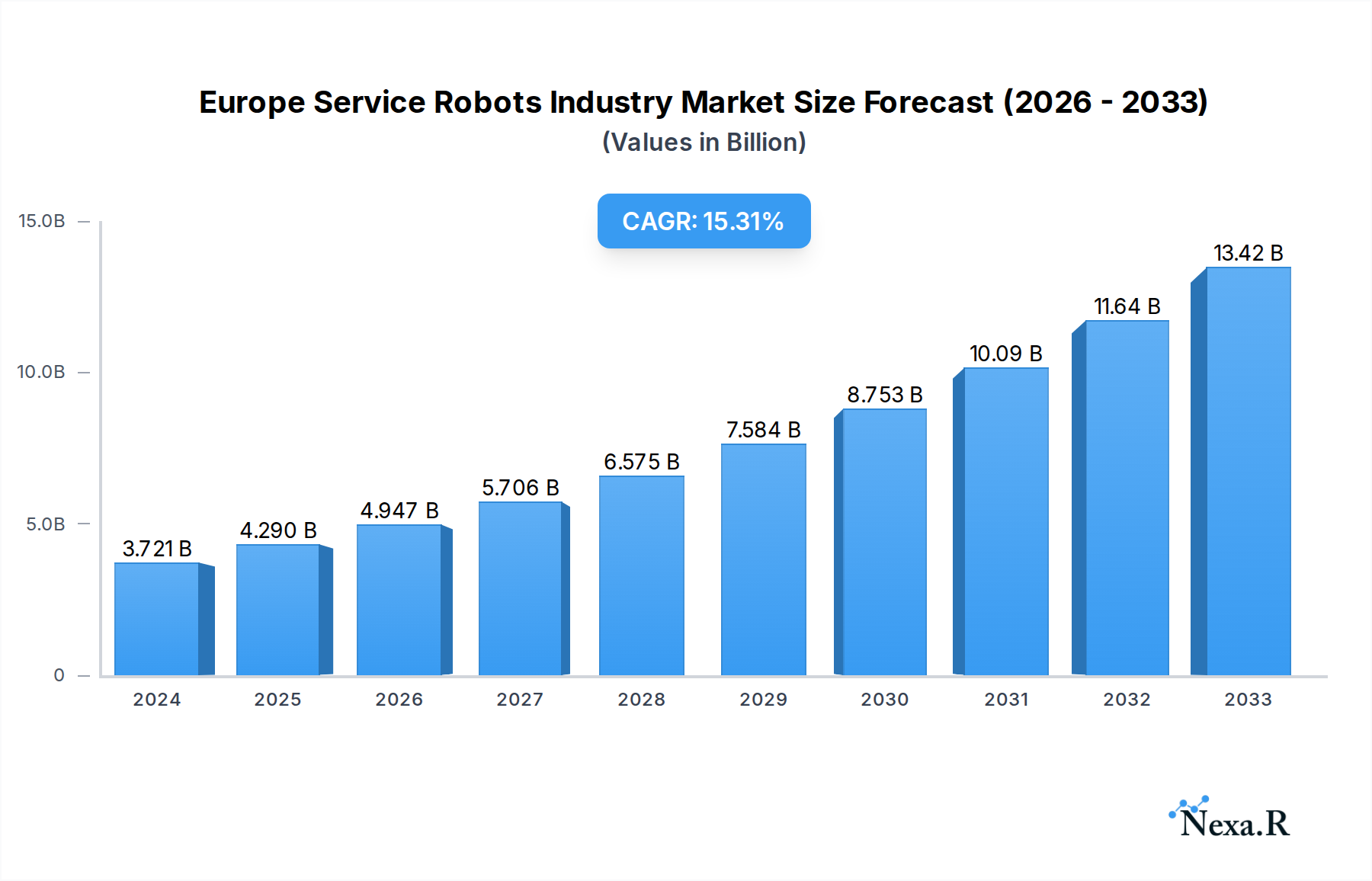

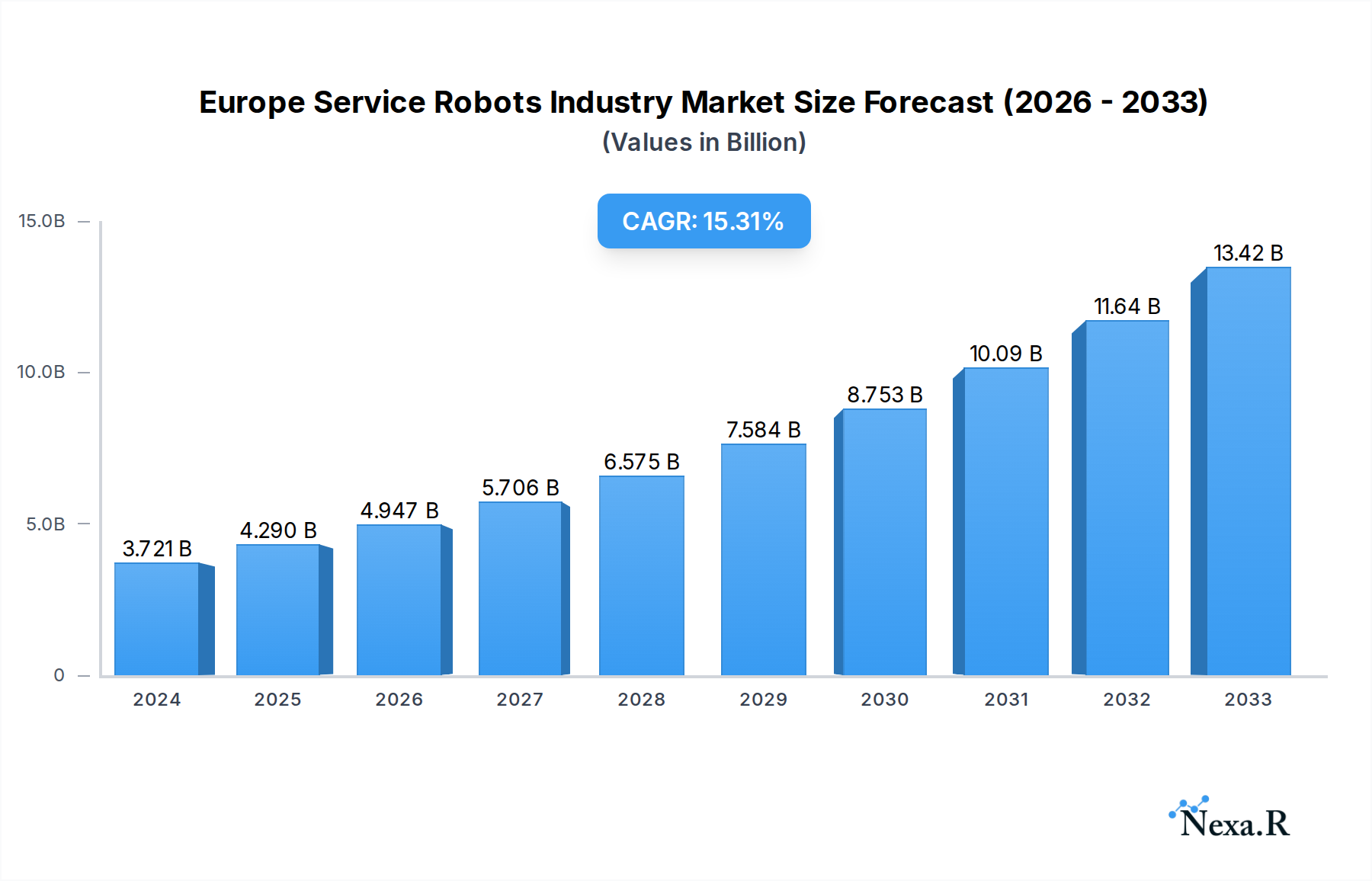

The European Service Robots market is poised for substantial growth, projected to reach an estimated $3,721.3 million in 2024 with a remarkable CAGR of 15.4% over the forecast period. This robust expansion is fueled by a confluence of factors, including increasing adoption across diverse end-user industries and advancements in robotic technology. Key drivers for this market surge are the escalating demand for automation in sectors like healthcare, where robots assist in surgery and patient care, and in logistics and transportation, optimizing supply chains and last-mile delivery. The agricultural sector is also witnessing a significant uptake of service robots for precision farming, crop monitoring, and harvesting, leading to increased efficiency and reduced labor costs. Furthermore, government initiatives promoting technological innovation and industry 4.0 adoption are providing a conducive environment for market expansion. The burgeoning need for enhanced productivity, improved safety in hazardous environments (such as construction and mining), and the growing sophistication of robotic components like advanced sensors, actuators, and AI-driven software are collectively propelling the service robots industry forward.

Europe Service Robots Industry Market Size (In Billion)

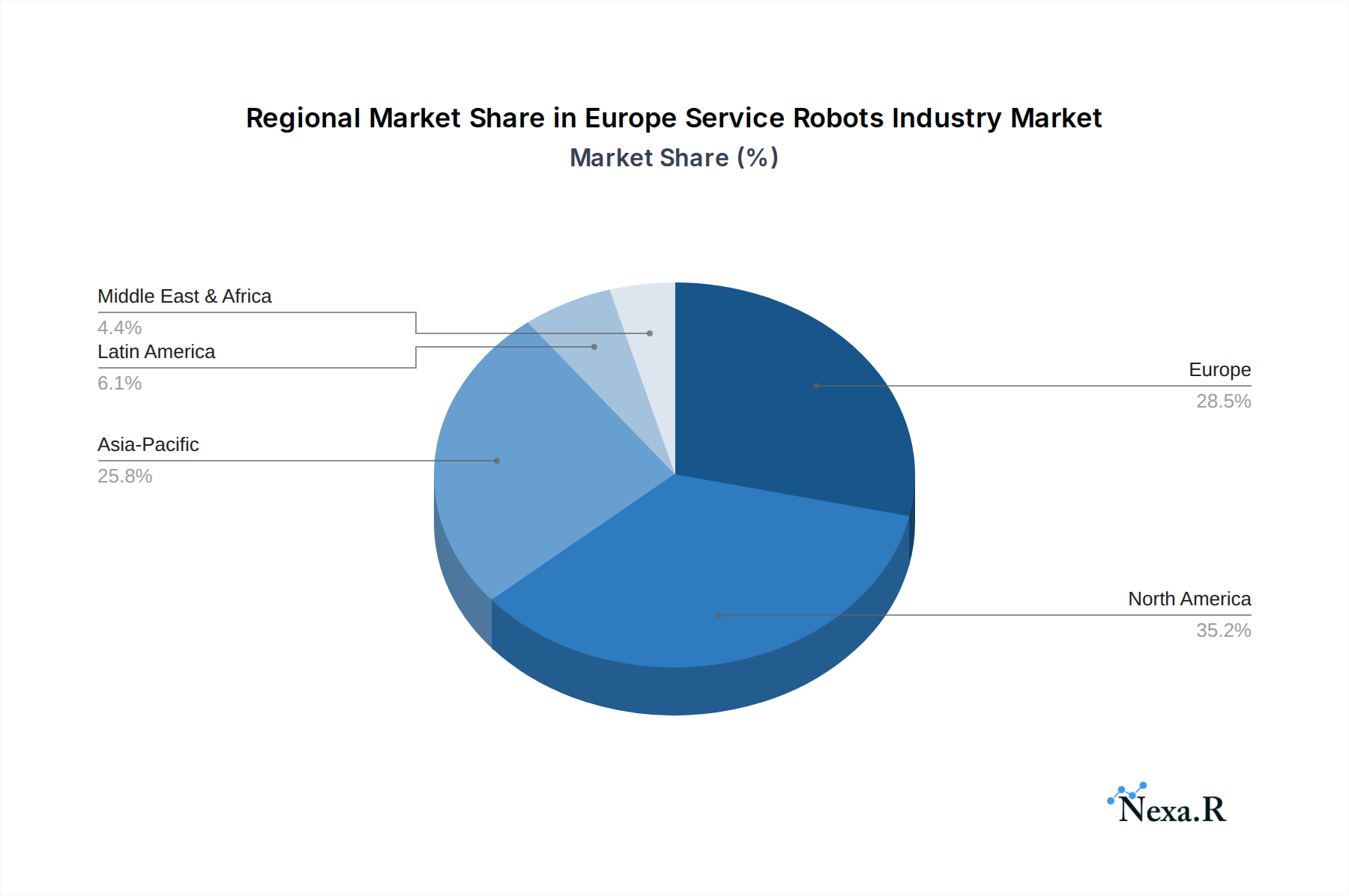

The European market is characterized by a diverse segmentation, with Personal Robots and Professional Robots forming the primary type categories. Within areas, Aerial, Land, and Underwater robots are carving out significant niches, addressing specific operational needs. The core components driving this innovation include sophisticated sensors for environmental perception, precise actuators for movement, intelligent control systems, and advanced software enabling complex tasks and decision-making. The prominent end-user industries—Military and Defense, Agriculture, Construction and Mining, Transportation & Logistics, Healthcare, and Government—are all actively integrating service robots to gain competitive advantages and address critical challenges. Leading companies like KUKA AG, iRobot Corporation, and Amazon Inc. are at the forefront, developing and deploying cutting-edge solutions. Geographically, Europe, with strong markets in the United Kingdom, Germany, and France, is a key region for service robot adoption and innovation, benefiting from a well-established industrial base and a commitment to digital transformation.

Europe Service Robots Industry Company Market Share

Europe Service Robots Industry: Comprehensive Market Analysis and Future Outlook (2019-2033)

This in-depth report offers a detailed examination of the European Service Robots Industry, forecasting market growth and identifying key trends from 2019 to 2033. With a base year of 2025 and a forecast period extending to 2033, this analysis provides actionable insights for stakeholders looking to capitalize on the burgeoning demand for service robots across various sectors. The report delves into parent and child market dynamics, exploring the intricate relationships between broader industry trends and specific niche segments.

Europe Service Robots Industry Market Dynamics & Structure

The European Service Robots Industry is characterized by a dynamic market structure shaped by intense technological innovation and evolving regulatory landscapes. While market concentration varies across segments, key players like KUKA AG, Amazon Inc., and iRobot Corporation are actively driving advancements. Technological innovation is primarily fueled by breakthroughs in AI, machine learning, and advanced sensor technology, enabling robots to perform more complex tasks. Regulatory frameworks, such as the European Commission's Robotics4EU initiative, are increasingly focusing on promoting responsible and ethical robot deployment, influencing adoption rates and product development. Competitive product substitutes, ranging from human labor in certain service roles to specialized automation solutions, necessitate continuous innovation and cost-effectiveness. End-user demographics are shifting towards sectors with labor shortages or requiring high precision and efficiency, such as healthcare and logistics. Mergers and acquisitions (M&A) trends are on the rise as larger companies seek to acquire innovative startups and expand their market reach.

- Market Concentration: Moderate to high in segments like industrial automation, but emerging in areas like personal assistance and healthcare.

- Technological Innovation Drivers: AI, machine learning, advanced sensors (LiDAR, computer vision), miniaturization, and collaborative robotics (cobots).

- Regulatory Frameworks: Emphasis on safety, data privacy, ethical considerations, and standardization (e.g., EU Robotics Strategy, Robotics4EU).

- Competitive Product Substitutes: Human labor, specialized tools, other forms of automation, and software-based solutions.

- End-User Demographics: Aging populations, increasing demand for efficiency, labor shortages in key industries, and growing acceptance of automation.

- M&A Trends: Acquisition of innovative startups, strategic alliances for technology integration, and expansion into new geographical markets.

Europe Service Robots Industry Growth Trends & Insights

The European Service Robots Industry is poised for significant expansion, driven by a confluence of factors that are reshaping market dynamics. The market size is projected to witness a robust Compound Annual Growth Rate (CAGR) of approximately 18-22% during the forecast period. This substantial growth trajectory is underpinned by an increasing adoption rate of service robots across diverse end-user industries, spurred by the need for enhanced productivity, cost reduction, and the ability to perform tasks in hazardous or inaccessible environments. Technological disruptions are at the forefront, with advancements in artificial intelligence, machine learning, and sensor technology enabling robots to perform increasingly sophisticated tasks, from autonomous navigation and manipulation to human-robot interaction. Consumer behavior shifts are also playing a crucial role; as individuals and businesses become more accustomed to and accepting of robotic solutions, demand for personalized services, automation in daily life, and efficient logistics is escalating. The integration of these robots into daily life and work processes is no longer a futuristic concept but a present reality, leading to market penetration that is expected to deepen considerably.

The evolution of the market size is a testament to the growing recognition of the benefits service robots offer. For instance, in the healthcare sector, surgical robots and assistive robots for the elderly are seeing increased deployment, contributing to improved patient outcomes and reduced healthcare costs. In logistics and transportation, autonomous mobile robots (AMRs) are revolutionizing warehouse operations and last-mile delivery. The government and defense sectors are also substantial contributors, utilizing robots for surveillance, bomb disposal, and other critical missions. The technological disruptions are not limited to hardware; sophisticated software platforms for robot control, data analysis, and fleet management are also crucial growth enablers. This comprehensive ecosystem, from advanced hardware components like sensors and actuators to intelligent software, is fostering a virtuous cycle of innovation and adoption. The estimated market size for service robots in Europe is projected to reach approximately $35,000 million units by 2033.

Dominant Regions, Countries, or Segments in Europe Service Robots Industry

The European Service Robots Industry is experiencing dynamic growth across various segments, with certain regions, countries, and specific robot types emerging as dominant forces. Among the robot types, Professional Robots are currently the dominant segment, driven by their widespread adoption in industrial, logistics, and healthcare applications where efficiency, precision, and safety are paramount. This segment is projected to account for over 65-70% of the total market share by 2025, with a projected market volume of approximately 300 million units. The growth of Professional Robots is intrinsically linked to the advancement of Land-based robots, which constitute the largest area of operation. These robots are crucial for applications in manufacturing, agriculture, construction, and logistics. The estimated market size for Land robots is expected to reach around 350 million units by 2033.

Within the End-User Industries, the Military and Defense sector, alongside Healthcare, are significant growth drivers. The Military and Defense sector’s demand for advanced robotics for surveillance, reconnaissance, and hazardous operations remains robust, projected to contribute approximately 15-20% to the market. The Healthcare sector, fueled by an aging population and the need for advanced medical procedures and elder care, is witnessing exponential growth, with an estimated market share of 20-25% and a projected volume of 100 million units by 2033. Geographically, Germany stands out as the dominant country within the European Service Robots Industry. Its strong industrial base, significant R&D investment, and government support for automation and digitalization initiatives are key factors behind its leadership. Germany is expected to hold over 25-30% of the European market share, with an estimated market volume of 120 million units by 2025. This dominance is further amplified by robust manufacturing capabilities and a well-established ecosystem of robot developers and integrators. The Components segment is seeing substantial growth in Sensors and Software, with a combined market share of over 50%, as these are critical for enabling the intelligence and functionality of advanced service robots.

Europe Service Robots Industry Product Landscape

The European Service Robots Industry is witnessing a surge in innovative product offerings designed to address a wide array of needs. Key product innovations include advanced collaborative robots (cobots) capable of working alongside humans safely and efficiently in manufacturing and logistics. Autonomous mobile robots (AMRs) are transforming warehouse operations with their ability to navigate complex environments and transport goods. In healthcare, surgical robots are becoming more precise and minimally invasive, while assistive robots are enhancing the quality of life for the elderly and individuals with disabilities. Furthermore, specialized drones equipped with sophisticated sensors are revolutionizing aerial inspection and delivery services. Performance metrics are continuously improving, with robots exhibiting enhanced dexterity, speed, and accuracy. Unique selling propositions often revolve around increased automation, reduced operational costs, improved safety, and the ability to perform tasks with unparalleled precision. Technological advancements in AI, computer vision, and machine learning are enabling these robots to learn, adapt, and perform more complex tasks autonomously.

Key Drivers, Barriers & Challenges in Europe Service Robots Industry

Key Drivers:

- Technological Advancements: Continuous innovation in AI, machine learning, sensors, and actuators is enabling more capable and versatile service robots.

- Labor Shortages & Aging Population: Increasing demand for automation in sectors facing workforce deficits and the need for elder care solutions.

- Productivity Enhancement: The drive for increased efficiency and cost reduction across industries fuels the adoption of robotics.

- Government Initiatives & Funding: European Union and national government programs supporting robotics research, development, and deployment (e.g., Robotics4EU).

- Growing Acceptance of Automation: Increased familiarity and trust in robotic solutions among businesses and consumers.

Barriers & Challenges:

- High Initial Investment Costs: The upfront cost of acquiring and implementing advanced service robots can be a significant barrier for SMEs.

- Regulatory Hurdles & Standardization: Developing consistent and adaptable regulations for robot safety, data privacy, and ethical operation across different EU member states.

- Integration Complexity: Challenges in integrating robots with existing IT infrastructure and legacy systems.

- Skill Gap & Workforce Training: The need for a skilled workforce to operate, maintain, and program complex robotic systems.

- Public Perception & Ethical Concerns: Addressing public concerns regarding job displacement, safety, and the ethical implications of autonomous systems.

- Supply Chain Disruptions: Vulnerability to global supply chain disruptions affecting component availability and manufacturing.

Emerging Opportunities in Europe Service Robots Industry

Emerging opportunities in the Europe Service Robots Industry are vast, driven by evolving societal needs and technological frontiers. The burgeoning demand for personalized healthcare and assisted living solutions presents a significant untapped market for advanced personal robots. The green transition is creating opportunities for robots in sustainable agriculture, waste management, and environmental monitoring. Furthermore, the expansion of e-commerce and the need for efficient last-mile delivery solutions are driving innovation in autonomous delivery robots, both on land and in the air. The integration of robotics with the Internet of Things (IoT) and 5G technology promises to unlock new levels of interconnectedness and intelligent automation. There is also a growing interest in robots for creative industries and entertainment, showcasing the expanding scope of service robotics beyond traditional industrial applications.

Growth Accelerators in the Europe Service Robots Industry Industry

Several catalysts are accelerating the growth of the Europe Service Robots Industry. Technological breakthroughs in areas like soft robotics and human-robot interaction are creating more adaptable and intuitive robotic solutions. Strategic partnerships between technology providers, end-users, and research institutions are fostering innovation and speeding up market penetration. Market expansion strategies, including entering new geographical regions within Europe and developing robots tailored for specific niche applications, are further propelling growth. The increasing availability of cloud-based robotics platforms is also democratizing access to advanced robotic capabilities, lowering barriers to entry for businesses. The focus on interoperability and standardization within the industry is also a significant growth accelerator, enabling seamless integration and wider adoption.

Key Players Shaping the Europe Service Robots Industry Market

- SeaRobotics Corporation

- Robobuilder Co Ltd

- Iberobtoics S L

- Hanool Robotics Corporation

- Amazon Inc.

- RedZone Robotics

- KUKA AG

- Gecko Systems Corporation

- iRobot Corporation

- Honda Motors Co Ltd

- Northrop Grumman Corporation

Notable Milestones in Europe Service Robots Industry Sector

- July 2021: Amazon announced the launch of a new center in Helsinki, Finland, to support research and development for its autonomous delivery service that currently operates in four US locations.

- October 2021: The European Commission announced the launch of its Robotics4EU, an initiative aiming to boost the use and adoption of responsible robotics within the European economy, thereby supporting the European Service Robot Market.

In-Depth Europe Service Robots Industry Market Outlook

The future outlook for the Europe Service Robots Industry is exceptionally promising, characterized by sustained high growth driven by a strong confluence of technological innovation, favorable market dynamics, and supportive policy frameworks. Growth accelerators such as advancements in AI and machine learning will continue to empower robots with greater autonomy and intelligence, expanding their applicability across new sectors and use cases. Strategic partnerships and collaborations will foster a more integrated ecosystem, leading to the development of more sophisticated and user-friendly robotic solutions. Market expansion strategies, particularly the focus on niche applications and underserved industries, will unlock further revenue streams. The ongoing commitment from the European Commission and national governments to foster the robotics sector through funding and regulatory support will provide a stable environment for continued investment and innovation, solidifying Europe's position as a global leader in service robotics.

Europe Service Robots Industry Segmentation

-

1. Type

- 1.1. Personal Robots

- 1.2. Professional Robots

-

2. Areas

- 2.1. Aerial

- 2.2. Land

- 2.3. Underwater

-

3. Components

- 3.1. Sensors

- 3.2. Actuators

- 3.3. Control Systems

- 3.4. Software

- 3.5. Others

-

4. End-User industries

- 4.1. Military and Defense

- 4.2. Agriculture, Construction and Mining

- 4.3. Transportation & Logistics

- 4.4. Healthcare

- 4.5. Government

- 4.6. Others

Europe Service Robots Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Service Robots Industry Regional Market Share

Geographic Coverage of Europe Service Robots Industry

Europe Service Robots Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Personal Robots

- 5.1.2. Professional Robots

- 5.2. Market Analysis, Insights and Forecast - by Areas

- 5.2.1. Aerial

- 5.2.2. Land

- 5.2.3. Underwater

- 5.3. Market Analysis, Insights and Forecast - by Components

- 5.3.1. Sensors

- 5.3.2. Actuators

- 5.3.3. Control Systems

- 5.3.4. Software

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by End-User industries

- 5.4.1. Military and Defense

- 5.4.2. Agriculture, Construction and Mining

- 5.4.3. Transportation & Logistics

- 5.4.4. Healthcare

- 5.4.5. Government

- 5.4.6. Others

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Europe Service Robots Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Personal Robots

- 6.1.2. Professional Robots

- 6.2. Market Analysis, Insights and Forecast - by Areas

- 6.2.1. Aerial

- 6.2.2. Land

- 6.2.3. Underwater

- 6.3. Market Analysis, Insights and Forecast - by Components

- 6.3.1. Sensors

- 6.3.2. Actuators

- 6.3.3. Control Systems

- 6.3.4. Software

- 6.3.5. Others

- 6.4. Market Analysis, Insights and Forecast - by End-User industries

- 6.4.1. Military and Defense

- 6.4.2. Agriculture, Construction and Mining

- 6.4.3. Transportation & Logistics

- 6.4.4. Healthcare

- 6.4.5. Government

- 6.4.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 SeaRobotics Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Robobuilder Co Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Iberobtoics S L

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Hanool Robotics Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Amazon Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 RedZone Robotics

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 KUKA AG

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Gecko Systems Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 iRobot Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Honda Motors Co Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Northrop Grumman Corporation

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 SeaRobotics Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Service Robots Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Europe Service Robots Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Service Robots Industry Revenue million Forecast, by Type 2020 & 2033

- Table 2: Europe Service Robots Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 3: Europe Service Robots Industry Revenue million Forecast, by Areas 2020 & 2033

- Table 4: Europe Service Robots Industry Volume K Unit Forecast, by Areas 2020 & 2033

- Table 5: Europe Service Robots Industry Revenue million Forecast, by Components 2020 & 2033

- Table 6: Europe Service Robots Industry Volume K Unit Forecast, by Components 2020 & 2033

- Table 7: Europe Service Robots Industry Revenue million Forecast, by End-User industries 2020 & 2033

- Table 8: Europe Service Robots Industry Volume K Unit Forecast, by End-User industries 2020 & 2033

- Table 9: Europe Service Robots Industry Revenue million Forecast, by Region 2020 & 2033

- Table 10: Europe Service Robots Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 11: Europe Service Robots Industry Revenue million Forecast, by Type 2020 & 2033

- Table 12: Europe Service Robots Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 13: Europe Service Robots Industry Revenue million Forecast, by Areas 2020 & 2033

- Table 14: Europe Service Robots Industry Volume K Unit Forecast, by Areas 2020 & 2033

- Table 15: Europe Service Robots Industry Revenue million Forecast, by Components 2020 & 2033

- Table 16: Europe Service Robots Industry Volume K Unit Forecast, by Components 2020 & 2033

- Table 17: Europe Service Robots Industry Revenue million Forecast, by End-User industries 2020 & 2033

- Table 18: Europe Service Robots Industry Volume K Unit Forecast, by End-User industries 2020 & 2033

- Table 19: Europe Service Robots Industry Revenue million Forecast, by Country 2020 & 2033

- Table 20: Europe Service Robots Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 21: United Kingdom Europe Service Robots Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Europe Service Robots Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Germany Europe Service Robots Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Germany Europe Service Robots Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: France Europe Service Robots Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: France Europe Service Robots Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: Italy Europe Service Robots Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Italy Europe Service Robots Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Spain Europe Service Robots Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Spain Europe Service Robots Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Netherlands Europe Service Robots Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Netherlands Europe Service Robots Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Belgium Europe Service Robots Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: Belgium Europe Service Robots Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Sweden Europe Service Robots Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Sweden Europe Service Robots Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Norway Europe Service Robots Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: Norway Europe Service Robots Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Poland Europe Service Robots Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Poland Europe Service Robots Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Denmark Europe Service Robots Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Denmark Europe Service Robots Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Service Robots Industry?

The projected CAGR is approximately 15.4%.

2. Which companies are prominent players in the Europe Service Robots Industry?

Key companies in the market include SeaRobotics Corporation, Robobuilder Co Ltd, Iberobtoics S L, Hanool Robotics Corporation, Amazon Inc, RedZone Robotics, KUKA AG, Gecko Systems Corporation, iRobot Corporation, Honda Motors Co Ltd, Northrop Grumman Corporation.

3. What are the main segments of the Europe Service Robots Industry?

The market segments include Type, Areas, Components, End-User industries.

4. Can you provide details about the market size?

The market size is estimated to be USD 3721.3 million as of 2022.

5. What are some drivers contributing to market growth?

Increasing demand for these robots in defense sector; Focus towards research and development is leading to robots with more user-friendly features.

6. What are the notable trends driving market growth?

Increasing demand of service robots due to labor shortage in Europe.

7. Are there any restraints impacting market growth?

Interaction with robot is hindrance for some users; Initial high costs associated with development.

8. Can you provide examples of recent developments in the market?

July 2021: Amazon announced the launch of a new center in Helsinki, Finland, to support research and development for its autonomous delivery service that currently operates in four US locations.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Service Robots Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Service Robots Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Service Robots Industry?

To stay informed about further developments, trends, and reports in the Europe Service Robots Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence