Key Insights

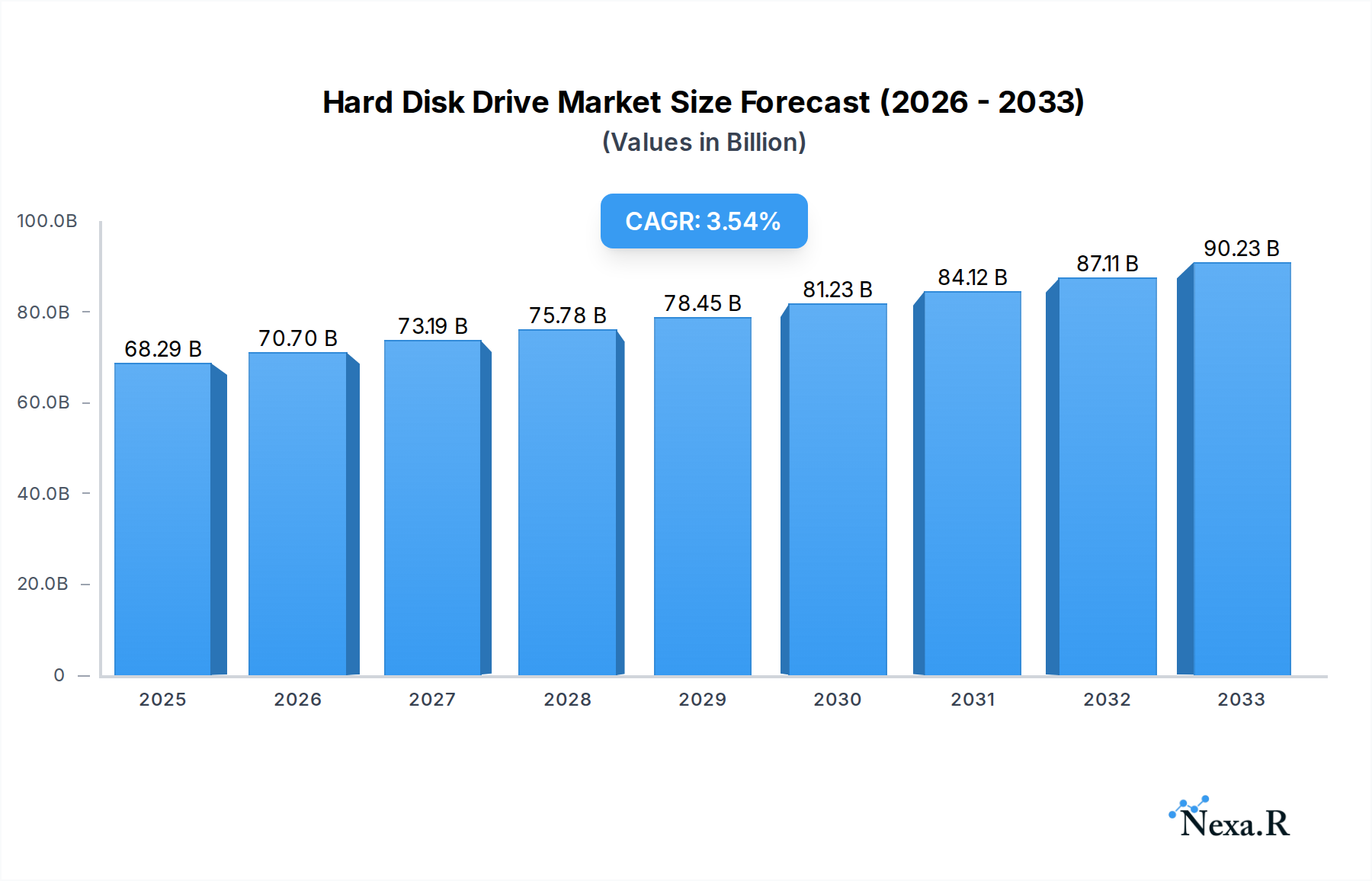

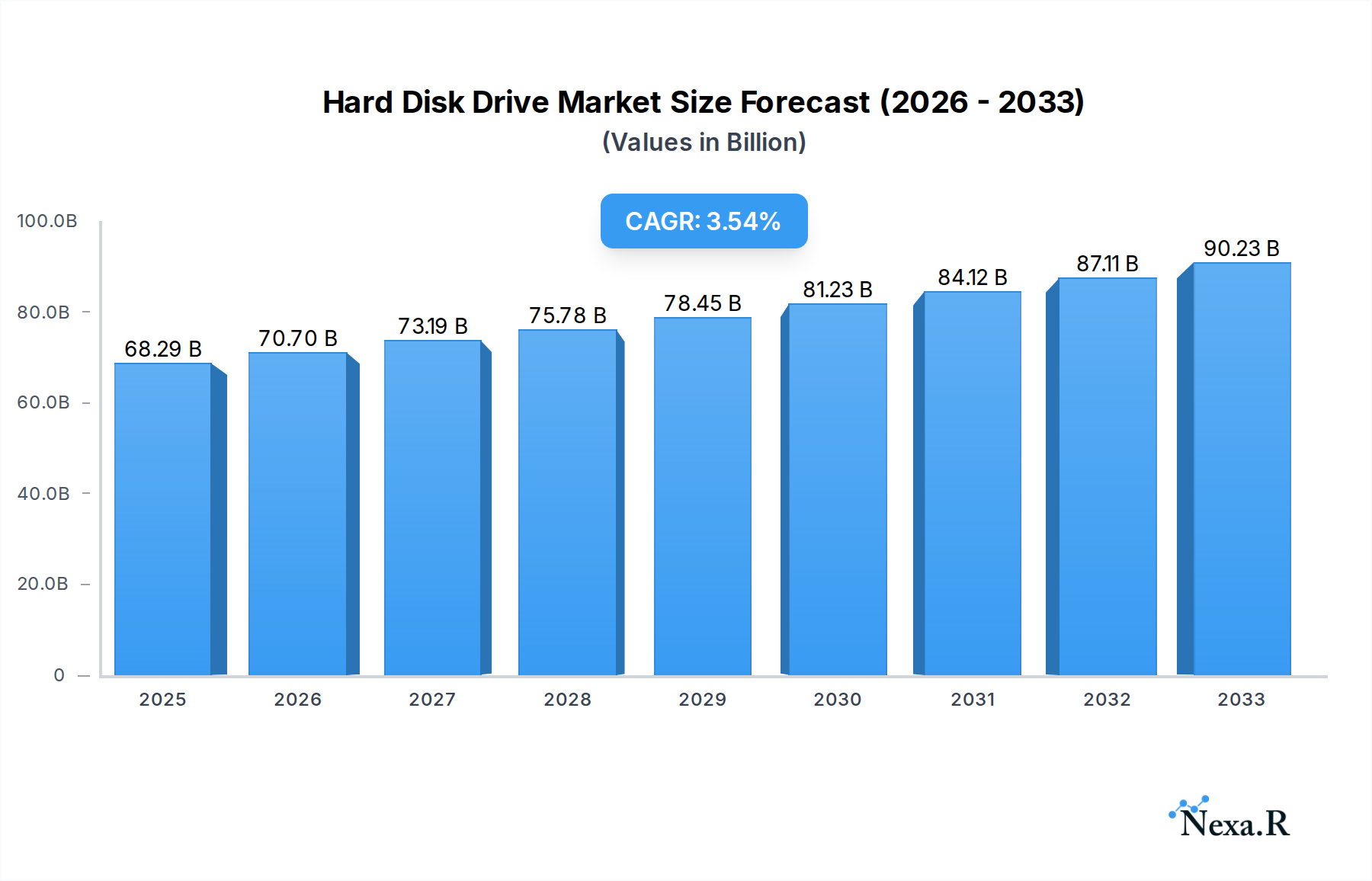

The global Hard Disk Drive (HDD) market is poised for steady growth, projecting a market size of $68,292.5 million by 2025. This expansion is driven by the sustained demand for high-capacity storage solutions across various applications, including laptops and desktop PCs. The market is expected to witness a Compound Annual Growth Rate (CAGR) of 3.49% from 2019 to 2033, indicating a consistent upward trajectory. While Solid State Drives (SSDs) have gained traction for their speed, HDDs continue to be the go-to choice for cost-effective bulk storage, especially in enterprise environments, data centers, and for consumers requiring vast amounts of data storage for media, backups, and archives. The ongoing proliferation of digital content, including high-definition video, gaming, and the expanding Internet of Things (IoT) ecosystem, further fuels the need for affordable, large-capacity storage. Key industry players are focusing on improving HDD density and reliability to meet these evolving demands, ensuring the continued relevance of this storage technology.

Hard Disk Drive Market Size (In Billion)

The HDD market is characterized by a robust segmentation, with a significant focus on storage capacities ranging from below 300GB to above 1TB, catering to diverse user needs. The "Above 1T" segment is likely to see the most substantial growth, reflecting the increasing data generation and storage requirements. Key drivers include the burgeoning cloud computing sector, the proliferation of AI and machine learning applications necessitating vast datasets, and the growing adoption of consumer electronics that require extensive storage. However, the market faces certain restraints, primarily the increasing performance and decreasing cost per gigabyte of SSDs, which are gradually eating into HDD market share, particularly in performance-sensitive applications. Despite this competition, the cost-effectiveness of HDDs for large-scale storage ensures their continued dominance in specific market segments. Innovations in areas like HAMR (Heat-Assisted Magnetic Recording) and MAMR (Microwave-Assisted Magnetic Recording) are expected to push the boundaries of HDD capacity and performance, helping to mitigate the competitive pressure from SSDs and sustain market growth.

Hard Disk Drive Company Market Share

This in-depth report offers a definitive analysis of the global Hard Disk Drive (HDD) market, covering its intricate dynamics, growth trajectories, and future outlook. Delving into both parent and child markets, this study provides unparalleled insights for industry professionals, investors, and stakeholders. The report meticulously examines market concentration, technological innovation, regulatory landscapes, competitive forces, and evolving consumer demands across the Study Period (2019–2033), with a Base Year of 2025 and a robust Forecast Period (2025–2033). All market size values are presented in million units.

Hard Disk Drive Market Dynamics & Structure

The global Hard Disk Drive (HDD) market exhibits a moderately concentrated structure, with a few key players like WD, Seagate, and Hitachi dominating market share, collectively holding an estimated 65% of the total market in 2025. Technological innovation remains a primary driver, fueled by advancements in magnetic recording density, head technology, and firmware optimization, enabling higher capacities and faster transfer speeds. Regulatory frameworks, particularly concerning data storage security and environmental compliance for manufacturing, play a crucial role in shaping market entry and operational strategies. Competitive product substitutes, primarily Solid State Drives (SSDs), present a significant challenge, especially in performance-critical applications, though HDDs continue to offer superior cost-per-gigabyte for bulk storage. End-user demographics indicate a sustained demand from enterprises for data archiving and backup, alongside a resilient segment within the desktop PC market. Merger and acquisition (M&A) trends, while less frequent in recent years due to market maturity, have historically consolidated key technologies and customer bases. For instance, a notable M&A event in the past involved the consolidation of storage businesses to enhance R&D capabilities. Innovation barriers are primarily related to the physical limitations of magnetic storage technology and the increasing R&D costs required to achieve incremental performance gains.

- Market Concentration: Dominated by a few major manufacturers, influencing pricing and innovation pace.

- Technological Innovation Drivers: Advancements in areal density, actuator technology, and servo control systems are key.

- Regulatory Frameworks: Compliance with data privacy laws (e.g., GDPR) and environmental standards impacts manufacturing and product lifecycle.

- Competitive Product Substitutes: SSDs are a significant threat, particularly for high-performance computing and consumer electronics.

- End-User Demographics: Enterprise data centers, personal computing, and archiving solutions represent major demand segments.

- M&A Trends: Historical consolidation has shaped the current competitive landscape; ongoing strategic partnerships are key.

Hard Disk Drive Growth Trends & Insights

The Hard Disk Drive (HDD) market, while facing pressure from Solid State Drives (SSDs), is projected to demonstrate a stable yet nuanced growth trajectory characterized by a compound annual growth rate (CAGR) of approximately 2.5% during the forecast period (2025–2033). The market size, estimated at around 550 million units in 2025, is expected to expand gradually, driven by the unyielding demand for high-capacity storage solutions in enterprise data centers, cloud computing infrastructure, and archival applications. Adoption rates in emerging economies are projected to remain robust, fueled by the increasing digitalization of businesses and governments. Despite the speed advantage of SSDs, the superior cost-effectiveness of HDDs for storing vast amounts of data ensures their continued relevance, particularly in sectors where cost per terabyte is a paramount consideration. Technological disruptions in HDD technology, such as the adoption of helium-filled drives for increased density and efficiency, and advancements in heat-assisted magnetic recording (HAMR) and microwave-assisted magnetic recording (MAMR), are crucial in sustaining competitive parity and expanding storage capacities. Consumer behavior shifts are also notable; while performance-oriented consumers and gamers are increasingly opting for SSDs for operating systems and frequently accessed files, a significant portion of the population still relies on HDDs for secondary storage, media archiving, and less demanding computing tasks. The market penetration of HDDs within the overall storage solutions landscape will depend on the continued innovation in cost reduction and capacity enhancement, ensuring they remain an attractive option for specific use cases. Furthermore, the integration of advanced error correction codes and improved vibration tolerance technologies will enhance the reliability and longevity of HDDs, further solidifying their position in specific market segments. The growth will be further propelled by the increasing volume of unstructured data generated by IoT devices, surveillance systems, and scientific research, necessitating cost-effective mass storage solutions.

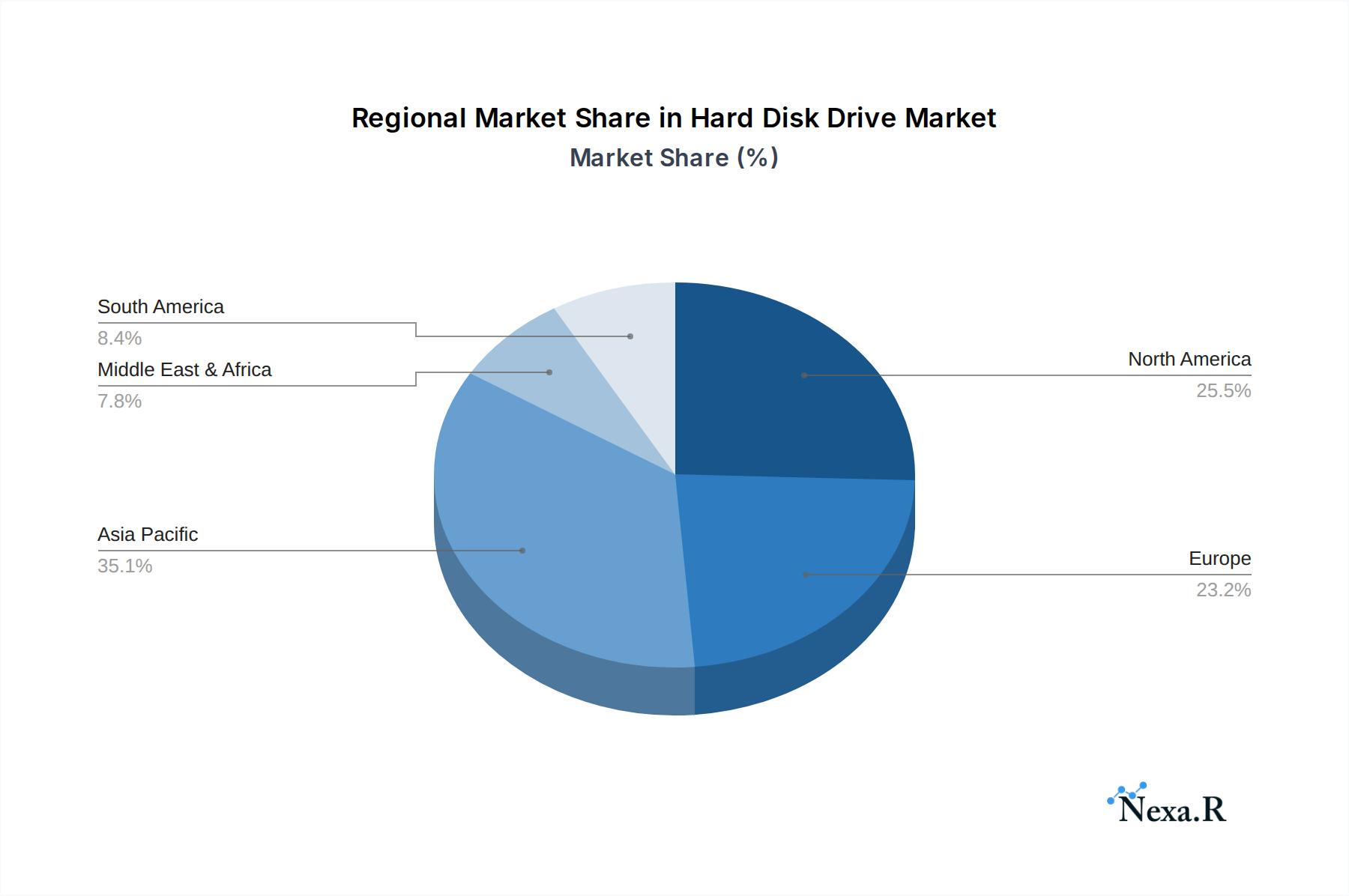

Dominant Regions, Countries, or Segments in Hard Disk Drive

The Asia Pacific region is poised to continue its dominance in the global Hard Disk Drive (HDD) market, driven by a confluence of economic powerhouses, burgeoning manufacturing capabilities, and a rapidly expanding digital infrastructure. Countries like China, South Korea, and Taiwan are not only major consumers of storage solutions for their vast IT industries and growing enterprise sectors but also critical hubs for the manufacturing and assembly of HDDs. The region's dominance is further amplified by the presence of key original design manufacturers (ODMs) and system integrators that drive demand for a wide array of storage devices. Within the application segments, Desktop PCs are expected to remain a significant driver of HDD demand, particularly in emerging markets where affordability and capacity are prioritized over extreme performance. While laptops increasingly integrate SSDs, the cost-effectiveness and large capacities of HDDs make them indispensable for many desktop users, including small businesses and home users seeking bulk storage for media and files. In terms of storage types, the Above 1T segment is experiencing the most substantial growth, reflecting the escalating need for massive data storage across all sectors. This surge is fueled by the proliferation of high-definition content, the growth of cloud storage services, and the increasing data requirements of Big Data analytics and artificial intelligence applications. The economic policies in the Asia Pacific, which often favor manufacturing and technological development, coupled with substantial investments in digital infrastructure, create a fertile ground for HDD market expansion. The increasing disposable income in many Asian countries also translates into higher demand for consumer electronics that utilize HDDs. Furthermore, the region's role as a global technology supply chain hub ensures a constant flow of components and finished products, reinforcing its leadership position. The continued innovation in HDD technology, particularly in increasing storage density and reducing power consumption, will further enhance their appeal in this dynamic region. Market share within the Asia Pacific is substantial, estimated to account for over 40% of the global HDD market in 2025, with projections indicating continued growth driven by these factors.

- Dominant Region: Asia Pacific, driven by manufacturing prowess and digital expansion.

- Key Countries: China, South Korea, Taiwan – crucial for both production and consumption.

- Leading Application Segment: Desktop PCs, especially in developing economies prioritizing affordability and capacity.

- Fastest Growing Type Segment: Above 1T, catering to the escalating demand for mass data storage.

- Key Growth Drivers: Favorable economic policies, robust digital infrastructure investment, and rising disposable incomes.

Hard Disk Drive Product Landscape

The Hard Disk Drive (HDD) product landscape is characterized by a continuous pursuit of higher storage densities and improved performance metrics, all while maintaining cost-effectiveness. Manufacturers are pushing the boundaries of areal density, a key metric representing the number of bits that can be stored per square inch of platter surface. Innovations like Shingled Magnetic Recording (SMR) and advancements in drive firmware are enabling capacities exceeding 20TB in standard 3.5-inch form factors. Applications range from enterprise-grade drives designed for 24/7 operation in data centers, offering enhanced reliability and rotational vibration safeguards, to consumer-oriented drives focused on a balance of capacity, speed, and power efficiency for desktop PCs and external storage solutions. Performance metrics like sustained read/write speeds, average seek times, and cache sizes are critical differentiators. Unique selling propositions often revolve around specific reliability ratings, energy efficiency certifications, and proprietary data management technologies. Technological advancements in materials science for platters and head technology, alongside sophisticated error correction codes, are crucial for ensuring data integrity and longevity.

Key Drivers, Barriers & Challenges in Hard Disk Drive

Key Drivers:

- Ever-increasing Data Generation: The exponential growth of data from Big Data, IoT, AI, and multimedia necessitates cost-effective mass storage solutions, which HDDs excel at providing.

- Cost-Effectiveness: HDDs offer a significantly lower cost per gigabyte compared to SSDs, making them the preferred choice for archiving, backup, and bulk data storage.

- Enterprise Demand: Cloud service providers and enterprise data centers continue to rely on HDDs for their massive storage infrastructure, driven by capacity and cost considerations.

- Technological Advancements: Innovations like HAMR and MAMR are enabling higher capacities, extending the relevance of HDDs.

Barriers & Challenges:

- SSD Competition: The performance advantage and decreasing cost of SSDs pose a significant threat, particularly in the consumer and high-performance enterprise segments.

- Limited Speed: HDDs are inherently slower than SSDs, which can be a bottleneck in applications requiring rapid data access.

- Mechanical Limitations: The reliance on moving parts makes HDDs more susceptible to physical shock and wear over time compared to solid-state alternatives.

- Supply Chain Volatility: Geopolitical factors, natural disasters, and raw material availability can impact production and pricing.

- Obsolescence Risk: A rapid shift towards all-flash storage in certain sectors could lead to a decline in demand for HDDs if innovation falters.

Emerging Opportunities in Hard Disk Drive

Emerging opportunities for Hard Disk Drives (HDDs) lie in the burgeoning sectors of the Internet of Things (IoT), edge computing, and the continued expansion of surveillance systems. As the volume of data generated at the edge increases, cost-effective and high-capacity storage solutions like HDDs will be crucial for local data buffering and pre-processing before transmission to the cloud. The growth in smart cities and autonomous vehicle technologies also presents a significant demand for rugged and high-capacity HDDs capable of operating in demanding environments. Furthermore, the demand for long-term archival storage for regulatory compliance and historical data preservation remains a robust niche for HDDs. The development of specialized HDD solutions tailored for these emerging applications, focusing on durability, power efficiency, and enhanced data integrity, will unlock new market potential.

Growth Accelerators in the Hard Disk Drive Industry

Growth in the Hard Disk Drive (HDD) industry will be significantly accelerated by continued technological breakthroughs in storage density, such as the maturation of HAMR and MAMR technologies, which promise to push capacities well beyond current limits. Strategic partnerships between HDD manufacturers and cloud service providers are crucial for driving adoption and ensuring product roadmaps align with evolving data center needs. Furthermore, the expansion of HDD solutions into emerging markets, where cost-per-gigabyte remains a primary purchasing factor, will serve as a significant growth catalyst. The increasing need for robust and cost-effective data backup and disaster recovery solutions for small and medium-sized businesses (SMBs) also presents a substantial opportunity for growth.

Key Players Shaping the Hard Disk Drive Market

- Western Digital (WD)

- Seagate Technology

- Hitachi Global Storage Technologies (HGST) (now part of Western Digital)

- Intel (primarily in SSD controllers and NAND flash, indirectly influencing HDD market dynamics)

- Samsung (primarily in SSDs and NAND flash, indirectly influencing HDD market dynamics)

- SanDisk (now part of Western Digital)

- Micron Technology (primarily in NAND flash, indirectly influencing HDD market dynamics)

- Lite-On Technology Corporation

- Kingston Digital

- Corsair

- Plextor

- Galaxy Technology

- Shinedisk

- Biwin Technology

- ADATA Technology

Notable Milestones in Hard Disk Drive Sector

- 2019: Introduction of higher capacity enterprise HDDs leveraging SMR technology, pushing capacities beyond 18TB.

- 2020: Continued advancements in HAMR technology, with vendors announcing prototypes and early production of 20TB+ drives.

- 2021: Increased adoption of helium-filled HDDs in enterprise environments for improved power efficiency and density.

- 2022: Early demonstrations and announcements regarding the commercial viability of MAMR technology for future high-capacity drives.

- 2023: Growing focus on cloud storage optimization and the integration of HDDs into hybrid storage solutions.

- 2024: Continued push for higher areal densities, with manufacturers aiming for 22TB and beyond in standard form factors.

In-Depth Hard Disk Drive Market Outlook

The future outlook for the Hard Disk Drive (HDD) market remains cautiously optimistic, with growth accelerators centered around technological innovation and the sustained demand for mass storage. The continued development and commercialization of HAMR and MAMR technologies are poised to unlock unprecedented storage capacities, ensuring HDDs remain a competitive option for data-intensive applications. Strategic collaborations with major cloud providers and data center operators will be crucial in shaping product development and market penetration. The expansion of HDD solutions into emerging markets, particularly in regions undergoing rapid digitalization, will provide a significant avenue for growth. Furthermore, the increasing requirement for cost-effective archival and backup solutions, especially for regulatory compliance and historical data preservation, will continue to underpin the HDD market's stability and potential for steady, albeit measured, expansion.

Hard Disk Drive Segmentation

-

1. Application

- 1.1. Laptops

- 1.2. Desktop PCs

- 1.3. Others

-

2. Types

- 2.1. Below 300G

- 2.2. 300G-1T

- 2.3. Above 1T

Hard Disk Drive Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Hard Disk Drive Regional Market Share

Geographic Coverage of Hard Disk Drive

Hard Disk Drive REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Laptops

- 5.1.2. Desktop PCs

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Below 300G

- 5.2.2. 300G-1T

- 5.2.3. Above 1T

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Hard Disk Drive Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Laptops

- 6.1.2. Desktop PCs

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Below 300G

- 6.2.2. 300G-1T

- 6.2.3. Above 1T

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Hard Disk Drive Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Laptops

- 7.1.2. Desktop PCs

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Below 300G

- 7.2.2. 300G-1T

- 7.2.3. Above 1T

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Hard Disk Drive Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Laptops

- 8.1.2. Desktop PCs

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Below 300G

- 8.2.2. 300G-1T

- 8.2.3. Above 1T

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Hard Disk Drive Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Laptops

- 9.1.2. Desktop PCs

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Below 300G

- 9.2.2. 300G-1T

- 9.2.3. Above 1T

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Hard Disk Drive Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Laptops

- 10.1.2. Desktop PCs

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Below 300G

- 10.2.2. 300G-1T

- 10.2.3. Above 1T

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Hard Disk Drive Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Laptops

- 11.1.2. Desktop PCs

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Below 300G

- 11.2.2. 300G-1T

- 11.2.3. Above 1T

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 WD

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Seagate

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Hitachi

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Intel

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Samsung

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Sandisk

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Micron

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Liteon

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Kingston Digital

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Corsair

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Plextor

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Galaxy Technology

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Shinedisk

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Biwin

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Adata

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 WD

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Hard Disk Drive Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Hard Disk Drive Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Hard Disk Drive Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Hard Disk Drive Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Hard Disk Drive Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Hard Disk Drive Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Hard Disk Drive Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Hard Disk Drive Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Hard Disk Drive Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Hard Disk Drive Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Hard Disk Drive Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Hard Disk Drive Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Hard Disk Drive Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Hard Disk Drive Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Hard Disk Drive Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Hard Disk Drive Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Hard Disk Drive Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Hard Disk Drive Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Hard Disk Drive Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Hard Disk Drive Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Hard Disk Drive Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Hard Disk Drive Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Hard Disk Drive Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Hard Disk Drive Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Hard Disk Drive Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Hard Disk Drive Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Hard Disk Drive Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Hard Disk Drive Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Hard Disk Drive Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Hard Disk Drive Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Hard Disk Drive Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Hard Disk Drive Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Hard Disk Drive Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Hard Disk Drive Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Hard Disk Drive Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Hard Disk Drive Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Hard Disk Drive Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Hard Disk Drive Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Hard Disk Drive Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Hard Disk Drive Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Hard Disk Drive Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Hard Disk Drive Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Hard Disk Drive Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Hard Disk Drive Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Hard Disk Drive Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Hard Disk Drive Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Hard Disk Drive Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Hard Disk Drive Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Hard Disk Drive Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Hard Disk Drive Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hard Disk Drive?

The projected CAGR is approximately 5.2%.

2. Which companies are prominent players in the Hard Disk Drive?

Key companies in the market include WD, Seagate, Hitachi, Intel, Samsung, Sandisk, Micron, Liteon, Kingston Digital, Corsair, Plextor, Galaxy Technology, Shinedisk, Biwin, Adata.

3. What are the main segments of the Hard Disk Drive?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 64.67 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Hard Disk Drive," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Hard Disk Drive report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Hard Disk Drive?

To stay informed about further developments, trends, and reports in the Hard Disk Drive, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence