Key Insights

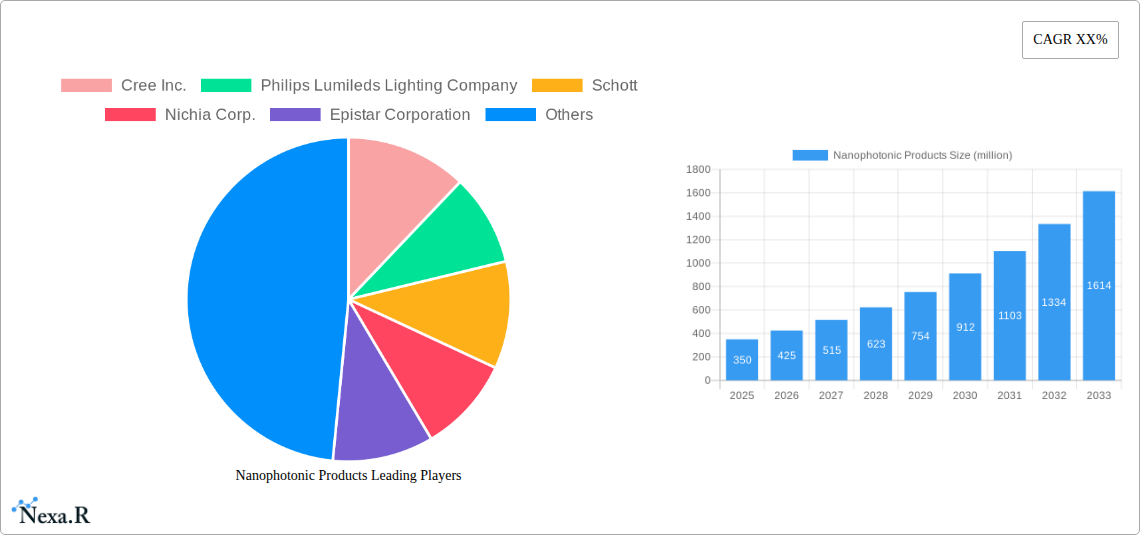

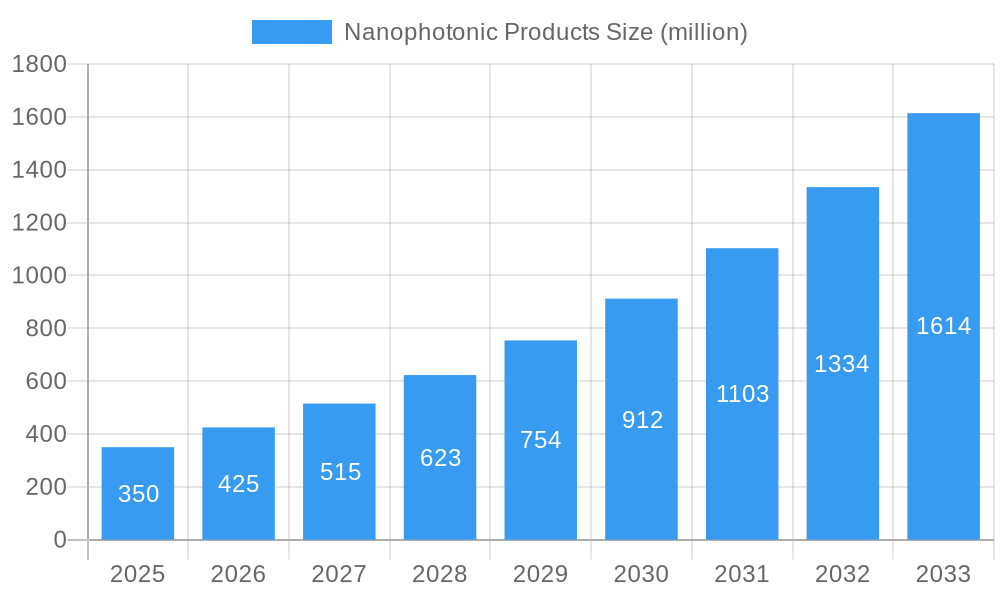

The nanophotonic products market is poised for remarkable expansion, projected to reach USD 0.35 billion in 2025 with a significant compound annual growth rate (CAGR) of 21.23%. This robust growth trajectory is fueled by a confluence of factors, primarily the burgeoning demand across diverse applications such as entertainment, consumer electronics, and advanced lighting solutions. The increasing integration of nanophotonic components in high-speed telecommunication networks, driving faster data transfer rates and improved signal integrity, is another substantial contributor. Furthermore, the non-visual applications, including advanced sensing, medical diagnostics, and data storage, are witnessing rapid innovation and adoption, propelling market expansion. The continuous advancements in material science and fabrication techniques are enabling the creation of more efficient, compact, and cost-effective nanophotonic devices, further accelerating market penetration.

Nanophotonic Products Market Size (In Million)

The market landscape is characterized by a dynamic interplay of evolving technologies and a widening array of applications. Key segments driving this growth include Light Emitting Diodes (LEDs) and Organic LEDs (OLEDs), which are becoming ubiquitous in displays and lighting due to their energy efficiency and superior visual quality. Near Field Optics, Photovoltaic Cells, Optical Switches, and Holographic Memory represent emerging and high-potential areas, promising breakthroughs in energy generation, data processing, and information storage. Key industry players such as Cree Inc., Philips Lumileds Lighting Company, and Nichia Corp. are investing heavily in research and development to introduce next-generation nanophotonic products. While the market benefits from strong demand and technological innovation, potential restraints such as high initial manufacturing costs for certain advanced technologies and the need for specialized expertise in fabrication and integration could present challenges. However, the overall outlook remains exceptionally positive, driven by the transformative potential of nanophotonics across numerous industries.

Nanophotonic Products Company Market Share

Here is a comprehensive, SEO-optimized report description for Nanophotonic Products, designed for immediate use without modification.

Nanophotonic Products Market Dynamics & Structure

The global nanophotonic products market is characterized by a moderately fragmented structure, with key players like Cree Inc., Philips Lumileds Lighting Company, Schott, Nichia Corp., Epistar Corporation, and Sharp vying for market dominance. Technological innovation is the primary driver, fueled by advancements in materials science and fabrication techniques that enable the creation of smaller, more efficient, and versatile photonic devices. Regulatory frameworks, particularly those pertaining to energy efficiency standards and semiconductor manufacturing, play a crucial role in shaping market entry and product development. Competitive product substitutes, while emerging, are largely outpaced by the unique performance advantages offered by nanophotonic solutions in areas like speed, miniaturization, and energy consumption. End-user demographics are expanding rapidly, driven by the increasing demand for sophisticated electronic devices, high-speed communication infrastructure, and advanced display technologies. Merger and acquisition (M&A) trends indicate a strategic consolidation phase, with larger entities acquiring innovative startups to bolster their product portfolios and expand their technological capabilities.

- Market Concentration: Moderately fragmented with significant contributions from established giants and agile innovators.

- Technological Innovation Drivers: Miniaturization, quantum dot integration, metamaterials, and advanced lithography techniques.

- Regulatory Frameworks: Focus on energy efficiency (e.g., LED lighting standards), data security, and semiconductor manufacturing incentives.

- Competitive Product Substitutes: While traditional optics exist, nanophotonics offer superior performance in specific high-demand applications.

- End-User Demographics: Growing adoption across consumer electronics, telecommunications, healthcare, and industrial sectors.

- M&A Trends: Strategic acquisitions of specialized nanophotonics firms by larger technology conglomerates seeking to integrate advanced optical capabilities.

Nanophotonic Products Growth Trends & Insights

The nanophotonic products market is poised for substantial growth, driven by a convergence of technological advancements and escalating demand across diverse industries. The global market size is projected to expand significantly, reaching an estimated $125.6 billion by 2025 and further accelerating to $280.3 billion by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of approximately 10.8% during the forecast period (2025-2033). This trajectory is underpinned by the relentless pursuit of enhanced performance, miniaturization, and energy efficiency in electronic and optical devices. Adoption rates for nanophotonic components, particularly within the Light Emitting Diodes (LEDs) and Organic Light Emitting Diodes (OLEDs) segments, are accelerating due to their widespread application in displays, solid-state lighting, and consumer electronics. Technological disruptions, such as the development of high-efficiency perovskite solar cells and advanced photonic integrated circuits (PICs), are creating new market frontiers. Consumer behavior shifts, influenced by the demand for immersive entertainment experiences, faster mobile communication (5G and beyond), and smarter home devices, are directly translating into increased market penetration for nanophotonic solutions. The integration of nanophotonics in telecommunication infrastructure is crucial for meeting the ever-increasing data bandwidth demands, further fueling market expansion. Furthermore, non-visual applications, including advanced sensing and biomedical imaging, are emerging as significant growth avenues. The historical period from 2019-2024 saw foundational growth, with the base year of 2025 marking a pivotal point for accelerated expansion.

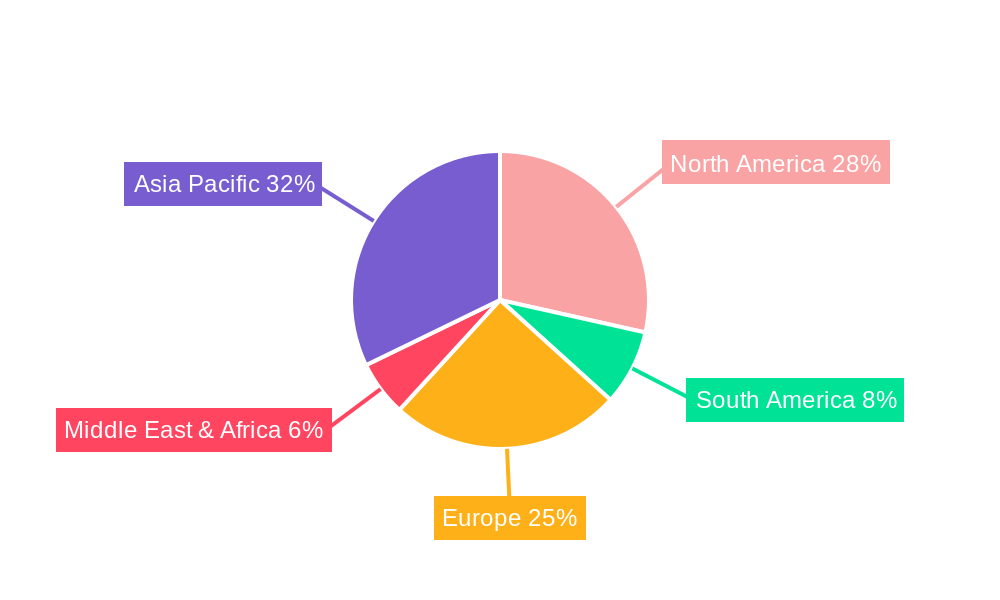

Dominant Regions, Countries, or Segments in Nanophotonic Products

The global nanophotonic products market's dominance is intricately linked to the Lighting application segment, which consistently outpaces other applications due to the widespread adoption of energy-efficient LED and OLED technologies across residential, commercial, and industrial sectors. This segment is projected to contribute significantly to the overall market valuation, driven by stringent government regulations promoting energy conservation and the declining cost of advanced lighting solutions. Geographically, Asia Pacific has emerged as the leading region, propelled by its robust manufacturing capabilities, substantial investments in research and development, and a burgeoning demand for consumer electronics and telecommunications infrastructure. Countries like China, South Korea, and Taiwan are at the forefront of nanophotonic product manufacturing and innovation, benefiting from supportive government policies and a large domestic market. The Types segment analysis reveals that Light Emitting Diodes (LEDs) remain the most dominant, owing to their established market presence and versatility. However, Organic Light Emitting Diodes (OLEDs) are exhibiting rapid growth, particularly in high-end display applications for smartphones, televisions, and wearable devices. Near Field Optics, Photovoltaic Cells, Optical Switches, and Optical Amplifiers, while smaller in market share currently, represent areas of significant future potential, driven by advancements in communication technology, renewable energy, and computing. The telecommunication sector’s insatiable demand for higher bandwidth and faster data transmission, facilitated by optical switches and amplifiers, also contributes to the Asia Pacific’s regional dominance. Economic policies promoting technological self-sufficiency and infrastructure development in key Asian nations further solidify this region's leading position in the nanophotonic products market.

Nanophotonic Products Product Landscape

The nanophotonic products landscape is characterized by continuous innovation, pushing the boundaries of optical performance and miniaturization. Key product categories include highly efficient Light Emitting Diodes (LEDs) and vibrant Organic Light Emitting Diodes (OLEDs), integral to modern displays and lighting solutions. Advancements in Near Field Optics are enabling novel applications in microscopy and data storage. Photovoltaic Cells are witnessing transformative improvements in efficiency and cost-effectiveness through nanoscale engineering. The development of high-speed Optical Switches and Optical Amplifiers is revolutionizing telecommunication networks, enabling faster data transfer and increased network capacity. Emerging technologies like Holographic Memory promise unprecedented data storage density. These products offer unique selling propositions such as enhanced energy efficiency, superior color rendition, faster response times, and reduced form factors.

Key Drivers, Barriers & Challenges in Nanophotonic Products

Key Drivers: The nanophotonic products market is propelled by several pivotal factors. Technological innovation remains paramount, with continuous advancements in materials science, quantum dot technology, and nanofabrication enabling the development of increasingly sophisticated and efficient devices. The escalating global demand for energy-efficient lighting solutions and high-resolution displays, driven by consumer electronics and environmental consciousness, significantly fuels market growth. Furthermore, the rapid expansion of the telecommunications sector, with the rollout of 5G and future wireless technologies, necessitates advanced optical components for high-speed data transmission. Government initiatives and funding for R&D in advanced materials and photonics also act as significant catalysts.

Barriers & Challenges: Despite robust growth, the nanophotonic products market faces considerable hurdles. High manufacturing costs associated with nanoscale fabrication processes can be a significant barrier, particularly for smaller companies. Technological complexity and the need for specialized expertise also pose challenges for widespread adoption. Supply chain vulnerabilities and the reliance on specific raw materials can lead to price volatility and production disruptions, impacting the overall market stability. Stringent regulatory approvals for new materials and devices, especially in medical and sensitive applications, can slow down market entry. Lastly, intense competition and the threat of disruptive emerging technologies necessitate continuous innovation and strategic market positioning.

Emerging Opportunities in Nanophotonic Products

Emerging opportunities in the nanophotonic products sector are abundant and diverse. The burgeoning field of biomedical photonics presents significant potential, with nanophotonic devices enabling more accurate and less invasive diagnostic tools, targeted drug delivery systems, and advanced imaging techniques for disease detection and monitoring. The growing demand for immersive virtual and augmented reality (VR/AR) experiences is driving innovation in high-resolution, lightweight, and power-efficient display technologies powered by nanophotonics. The expansion of quantum computing and advanced sensing applications, requiring highly sensitive and precise optical components, opens new avenues for nanophotonic solutions. Furthermore, the development of next-generation telecommunication networks beyond 5G, requiring unprecedented data speeds and low latency, will be a significant growth catalyst. Untapped markets in areas like advanced industrial automation and smart agriculture also hold substantial promise for nanophotonic integration.

Growth Accelerators in the Nanophotonic Products Industry

Several catalysts are accelerating the growth of the nanophotonic products industry. Breakthroughs in metamaterials and plasmonics are enabling unprecedented light manipulation capabilities, leading to novel device functionalities. Strategic partnerships and collaborations between research institutions and industry leaders are fostering faster innovation cycles and facilitating the commercialization of cutting-edge technologies. The increasing adoption of photonic integrated circuits (PICs), which combine multiple optical functions on a single chip, is driving miniaturization and cost reduction across various applications, especially in telecommunications and data centers. Furthermore, the continuous drive towards energy efficiency and sustainability across all sectors is creating a sustained demand for nanophotonic solutions that offer superior power performance. Market expansion strategies focusing on emerging economies and niche applications are also contributing to sustained growth.

Key Players Shaping the Nanophotonic Products Market

- Cree Inc.

- Philips Lumileds Lighting Company

- Schott

- Nichia Corp.

- Epistar Corporation

- Sharp

- Smd Led

Notable Milestones in Nanophotonic Products Sector

- 2019: Introduction of next-generation quantum dot-enhanced LEDs offering superior color gamut and energy efficiency.

- 2020: Significant advancements in perovskite solar cell technology, achieving record efficiencies for photovoltaic applications.

- 2021: Development of ultra-compact, high-speed optical switches for advanced data center infrastructure.

- 2022: Launch of novel nanophotonic sensors for enhanced medical diagnostics and environmental monitoring.

- 2023: Major breakthroughs in holographic data storage, promising terabytes of storage in a small form factor.

- 2024: Increased integration of OLED technology in foldable and rollable displays, expanding consumer electronics possibilities.

In-Depth Nanophotonic Products Market Outlook

The nanophotonic products market is set for an era of sustained and robust growth, propelled by a confluence of technological innovation and escalating global demand. Growth accelerators, including advancements in metamaterials, the increasing adoption of photonic integrated circuits, and a global push for energy efficiency, will continue to fuel expansion. Strategic collaborations and market expansion into emerging economies will further broaden the reach of these advanced optical solutions. The future market potential lies in leveraging nanophotonics for transformative applications in quantum computing, advanced healthcare, and next-generation communication networks, offering substantial strategic opportunities for market players to innovate and capture value in this dynamic and evolving sector.

Nanophotonic Products Segmentation

-

1. Application

- 1.1. Entertainment

- 1.2. Consumer Electronics

- 1.3. Indicators And Signs

- 1.4. Lighting

- 1.5. Telecommunication

- 1.6. Non-Visual Applications

-

2. Types

- 2.1. Light Emitting Diodes (Leds)

- 2.2. Organic Leds (Oleds)

- 2.3. Near Field Optics

- 2.4. Photovoltaic Cells

- 2.5. Optical Switches

- 2.6. Optical Amplifiers

- 2.7. Holographic Memory

Nanophotonic Products Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Nanophotonic Products Regional Market Share

Geographic Coverage of Nanophotonic Products

Nanophotonic Products REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Entertainment

- 5.1.2. Consumer Electronics

- 5.1.3. Indicators And Signs

- 5.1.4. Lighting

- 5.1.5. Telecommunication

- 5.1.6. Non-Visual Applications

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Light Emitting Diodes (Leds)

- 5.2.2. Organic Leds (Oleds)

- 5.2.3. Near Field Optics

- 5.2.4. Photovoltaic Cells

- 5.2.5. Optical Switches

- 5.2.6. Optical Amplifiers

- 5.2.7. Holographic Memory

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Nanophotonic Products Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Entertainment

- 6.1.2. Consumer Electronics

- 6.1.3. Indicators And Signs

- 6.1.4. Lighting

- 6.1.5. Telecommunication

- 6.1.6. Non-Visual Applications

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Light Emitting Diodes (Leds)

- 6.2.2. Organic Leds (Oleds)

- 6.2.3. Near Field Optics

- 6.2.4. Photovoltaic Cells

- 6.2.5. Optical Switches

- 6.2.6. Optical Amplifiers

- 6.2.7. Holographic Memory

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Nanophotonic Products Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Entertainment

- 7.1.2. Consumer Electronics

- 7.1.3. Indicators And Signs

- 7.1.4. Lighting

- 7.1.5. Telecommunication

- 7.1.6. Non-Visual Applications

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Light Emitting Diodes (Leds)

- 7.2.2. Organic Leds (Oleds)

- 7.2.3. Near Field Optics

- 7.2.4. Photovoltaic Cells

- 7.2.5. Optical Switches

- 7.2.6. Optical Amplifiers

- 7.2.7. Holographic Memory

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Nanophotonic Products Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Entertainment

- 8.1.2. Consumer Electronics

- 8.1.3. Indicators And Signs

- 8.1.4. Lighting

- 8.1.5. Telecommunication

- 8.1.6. Non-Visual Applications

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Light Emitting Diodes (Leds)

- 8.2.2. Organic Leds (Oleds)

- 8.2.3. Near Field Optics

- 8.2.4. Photovoltaic Cells

- 8.2.5. Optical Switches

- 8.2.6. Optical Amplifiers

- 8.2.7. Holographic Memory

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Nanophotonic Products Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Entertainment

- 9.1.2. Consumer Electronics

- 9.1.3. Indicators And Signs

- 9.1.4. Lighting

- 9.1.5. Telecommunication

- 9.1.6. Non-Visual Applications

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Light Emitting Diodes (Leds)

- 9.2.2. Organic Leds (Oleds)

- 9.2.3. Near Field Optics

- 9.2.4. Photovoltaic Cells

- 9.2.5. Optical Switches

- 9.2.6. Optical Amplifiers

- 9.2.7. Holographic Memory

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Nanophotonic Products Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Entertainment

- 10.1.2. Consumer Electronics

- 10.1.3. Indicators And Signs

- 10.1.4. Lighting

- 10.1.5. Telecommunication

- 10.1.6. Non-Visual Applications

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Light Emitting Diodes (Leds)

- 10.2.2. Organic Leds (Oleds)

- 10.2.3. Near Field Optics

- 10.2.4. Photovoltaic Cells

- 10.2.5. Optical Switches

- 10.2.6. Optical Amplifiers

- 10.2.7. Holographic Memory

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Nanophotonic Products Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Entertainment

- 11.1.2. Consumer Electronics

- 11.1.3. Indicators And Signs

- 11.1.4. Lighting

- 11.1.5. Telecommunication

- 11.1.6. Non-Visual Applications

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Light Emitting Diodes (Leds)

- 11.2.2. Organic Leds (Oleds)

- 11.2.3. Near Field Optics

- 11.2.4. Photovoltaic Cells

- 11.2.5. Optical Switches

- 11.2.6. Optical Amplifiers

- 11.2.7. Holographic Memory

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Cree Inc.

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Philips Lumileds Lighting Company

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Schott

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Nichia Corp.

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Epistar Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Sharp

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Smd Led

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.1 Cree Inc.

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Nanophotonic Products Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Nanophotonic Products Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Nanophotonic Products Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Nanophotonic Products Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Nanophotonic Products Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Nanophotonic Products Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Nanophotonic Products Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Nanophotonic Products Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Nanophotonic Products Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Nanophotonic Products Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Nanophotonic Products Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Nanophotonic Products Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Nanophotonic Products Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Nanophotonic Products Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Nanophotonic Products Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Nanophotonic Products Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Nanophotonic Products Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Nanophotonic Products Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Nanophotonic Products Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Nanophotonic Products Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Nanophotonic Products Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Nanophotonic Products Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Nanophotonic Products Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Nanophotonic Products Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Nanophotonic Products Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Nanophotonic Products Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Nanophotonic Products Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Nanophotonic Products Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Nanophotonic Products Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Nanophotonic Products Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Nanophotonic Products Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Nanophotonic Products Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Nanophotonic Products Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Nanophotonic Products Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Nanophotonic Products Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Nanophotonic Products Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Nanophotonic Products Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Nanophotonic Products Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Nanophotonic Products Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Nanophotonic Products Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Nanophotonic Products Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Nanophotonic Products Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Nanophotonic Products Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Nanophotonic Products Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Nanophotonic Products Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Nanophotonic Products Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Nanophotonic Products Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Nanophotonic Products Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Nanophotonic Products Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Nanophotonic Products Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Nanophotonic Products?

The projected CAGR is approximately 16%.

2. Which companies are prominent players in the Nanophotonic Products?

Key companies in the market include Cree Inc., Philips Lumileds Lighting Company, Schott, Nichia Corp., Epistar Corporation, Sharp, Smd Led.

3. What are the main segments of the Nanophotonic Products?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 20.5 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Nanophotonic Products," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Nanophotonic Products report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Nanophotonic Products?

To stay informed about further developments, trends, and reports in the Nanophotonic Products, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence