Key Insights

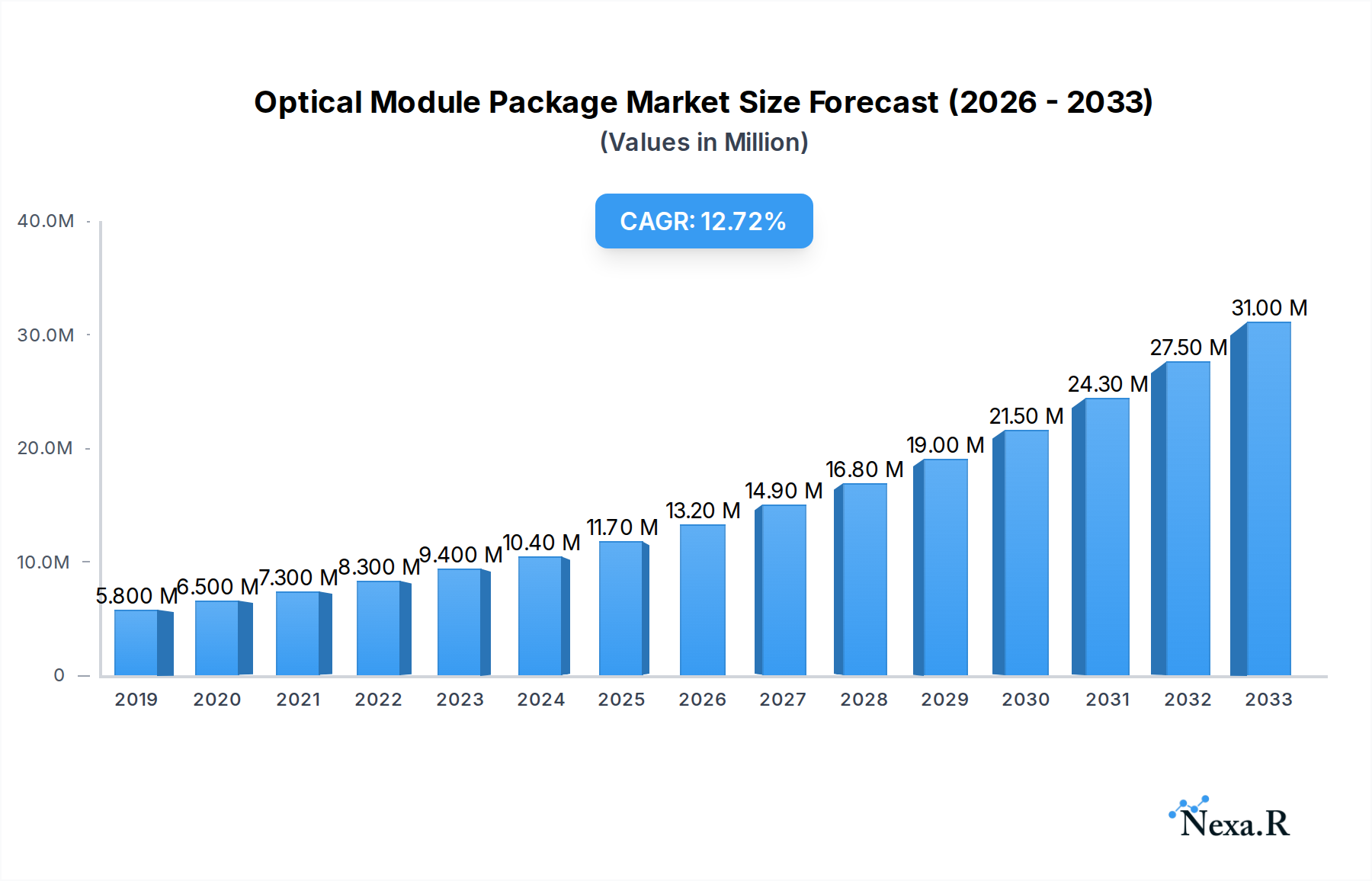

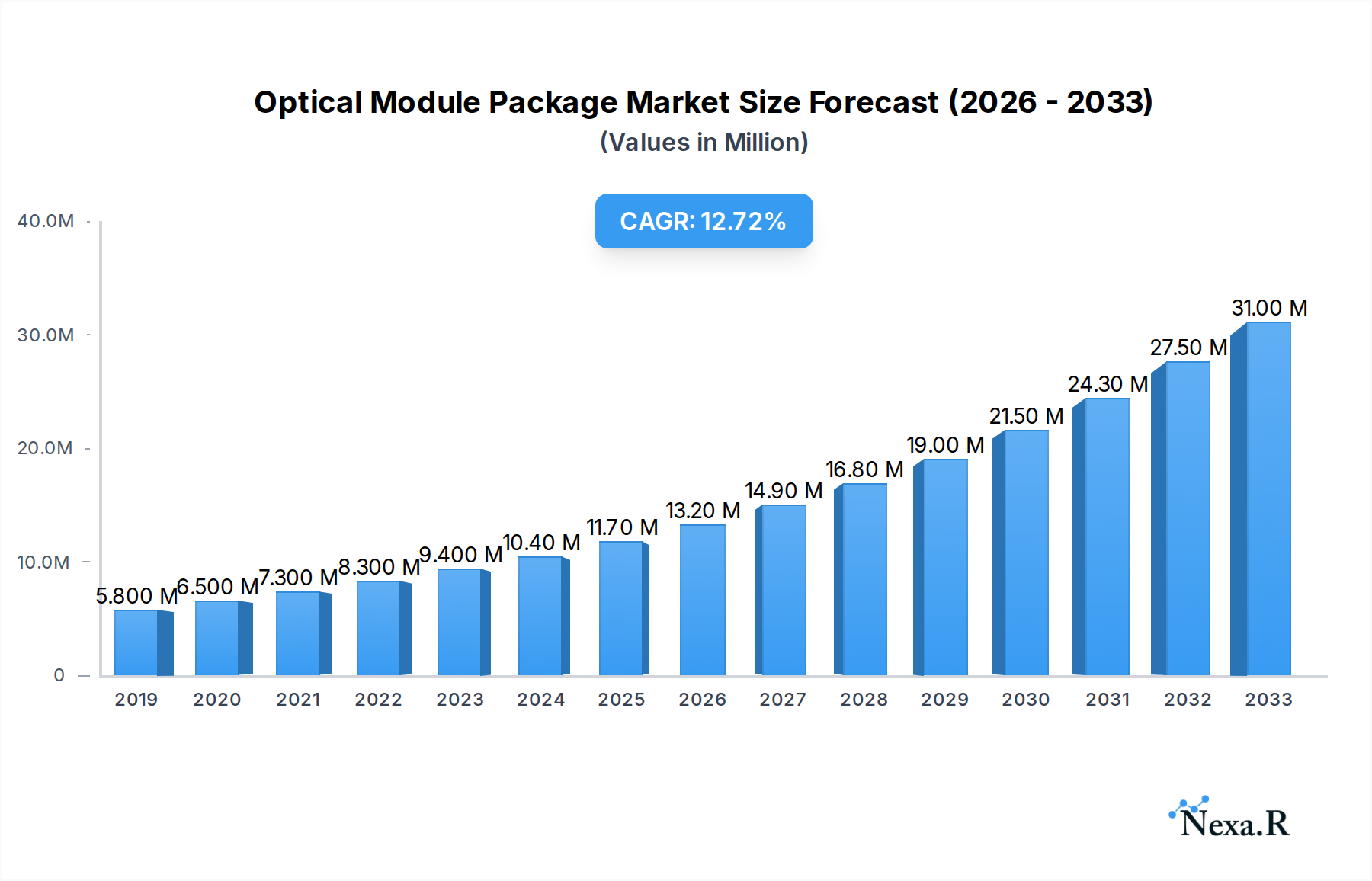

The Optical Module Package market is poised for significant expansion, projected to reach $10.4 billion in 2024, with a robust compound annual growth rate (CAGR) of 12.9% forecasted through 2033. This surge is primarily driven by the escalating demand for higher bandwidth and faster data transmission across various sectors, most notably telecommunications and data communication. The insatiable appetite for streaming services, cloud computing, AI-driven applications, and the continued rollout of 5G networks are fundamental catalysts fueling this growth. Furthermore, the increasing adoption of advanced networking technologies and the persistent need for efficient data center interconnects are compelling factors supporting the market's upward trajectory. The market is witnessing a pronounced trend towards miniaturization and higher density optical modules, enabling more capacity within smaller form factors, which is critical for the evolving landscape of network infrastructure.

Optical Module Package Market Size (In Million)

Despite the overwhelmingly positive growth outlook, certain factors could influence the market's pace. High manufacturing costs associated with advanced optical components and the complex supply chains involved in producing these specialized modules present a degree of restraint. Additionally, the rapid pace of technological innovation necessitates continuous investment in research and development, which can be a barrier for smaller players. However, the sheer volume of data generated globally, coupled with the ongoing digital transformation across industries, ensures that the demand for sophisticated optical module packages will remain strong. Emerging applications such as the Internet of Things (IoT) and the expansion of smart cities will further amplify the need for high-performance optical solutions, solidifying the market's bright future.

Optical Module Package Company Market Share

Optical Module Package Market Report: Driving 5G, AI, and Cloud Infrastructure Growth (2019-2033)

This comprehensive report delivers an in-depth analysis of the global Optical Module Package market, a critical component underpinning modern telecommunications, data communication, and the burgeoning demands of 5G, AI, and cloud computing. Spanning the historical period from 2019 to 2024, with a base year of 2025 and a robust forecast period extending to 2033, this study provides unparalleled insights into market dynamics, growth trajectories, and future opportunities.

Optical Module Package Market Dynamics & Structure

The global Optical Module Package market is characterized by a dynamic interplay of technological innovation, evolving regulatory landscapes, and intensifying competition. Market concentration is moderate, with a few key players holding significant share, but a vibrant ecosystem of emerging innovators continues to drive advancements. Technological innovation is primarily driven by the insatiable demand for higher bandwidth, lower latency, and increased power efficiency, fueled by the expansion of 5G networks, data centers, and artificial intelligence workloads. Regulatory frameworks, particularly concerning standards for interoperability and safety, play a crucial role in shaping product development and market access. Competitive product substitutes are emerging, though direct replacements for the core functionality of optical modules are limited in the short to medium term. End-user demographics are rapidly shifting towards hyperscale data centers, telecommunications service providers, and enterprises with substantial networking requirements. Mergers and acquisitions (M&A) trends are active as larger players seek to consolidate market share, acquire critical intellectual property, and expand their product portfolios. For instance, a projected xx M&A deals are anticipated within the forecast period, underscoring strategic consolidation efforts. Innovation barriers include the high cost of R&D, complex manufacturing processes, and the need for rigorous testing and certification to meet industry standards.

- Market Concentration: Moderate, with a blend of established leaders and agile innovators.

- Technological Innovation Drivers: 5G deployment, AI/ML workloads, cloud infrastructure expansion, data center upgrades, demand for higher data rates (e.g., 100GbE, 400GbE, 800GbE).

- Regulatory Frameworks: IEEE standards, OIF interoperability agreements, regional telecommunications regulations.

- Competitive Product Substitutes: While limited, advancements in co-packaged optics and silicon photonics represent potential long-term alternatives.

- End-User Demographics: Hyperscale data centers, telecom operators (Tier 1 & 2), enterprise networks, content delivery networks (CDNs).

- M&A Trends: Strategic acquisitions to gain technology, market access, and expand product offerings; consolidation for economies of scale.

- Innovation Barriers: High R&D expenditure, precision manufacturing challenges, lengthy qualification cycles.

Optical Module Package Growth Trends & Insights

The global Optical Module Package market is poised for significant expansion, driven by the pervasive digital transformation across industries. Leveraging the projected market size of $xx billion in 2025, the market is anticipated to witness a Compound Annual Growth Rate (CAGR) of xx% during the forecast period of 2025–2033, reaching an estimated $xx billion by 2033. This robust growth is fueled by the escalating demand for high-speed connectivity solutions essential for the deployment of 5G networks, the exponential growth of data traffic in data centers, and the increasing adoption of cloud computing services. Technological disruptions, such as the advancement of pluggable optical modules and the exploration of co-packaged optics, are reshaping the competitive landscape and driving innovation. Consumer behavior shifts are characterized by an increased reliance on bandwidth-intensive applications and services, from streaming high-definition content to sophisticated AI-powered tools, necessitating continuous upgrades in network infrastructure. The adoption rate of higher-speed optical modules, such as 400GbE and 800GbE, is accelerating as data centers and telecommunication providers strive to meet the ever-increasing data throughput demands. Furthermore, the development of advanced packaging technologies that enhance performance, reduce power consumption, and lower costs are key factors contributing to market penetration. The study will delve into the granular evolution of market size, analyzing historical trends from 2019 to 2024, with a particular focus on the significant growth observed in recent years due to accelerated 5G rollouts and data center investments. This deep dive into market evolution, adoption rates, and technological shifts will provide stakeholders with actionable intelligence for strategic decision-making.

Dominant Regions, Countries, or Segments in Optical Module Package

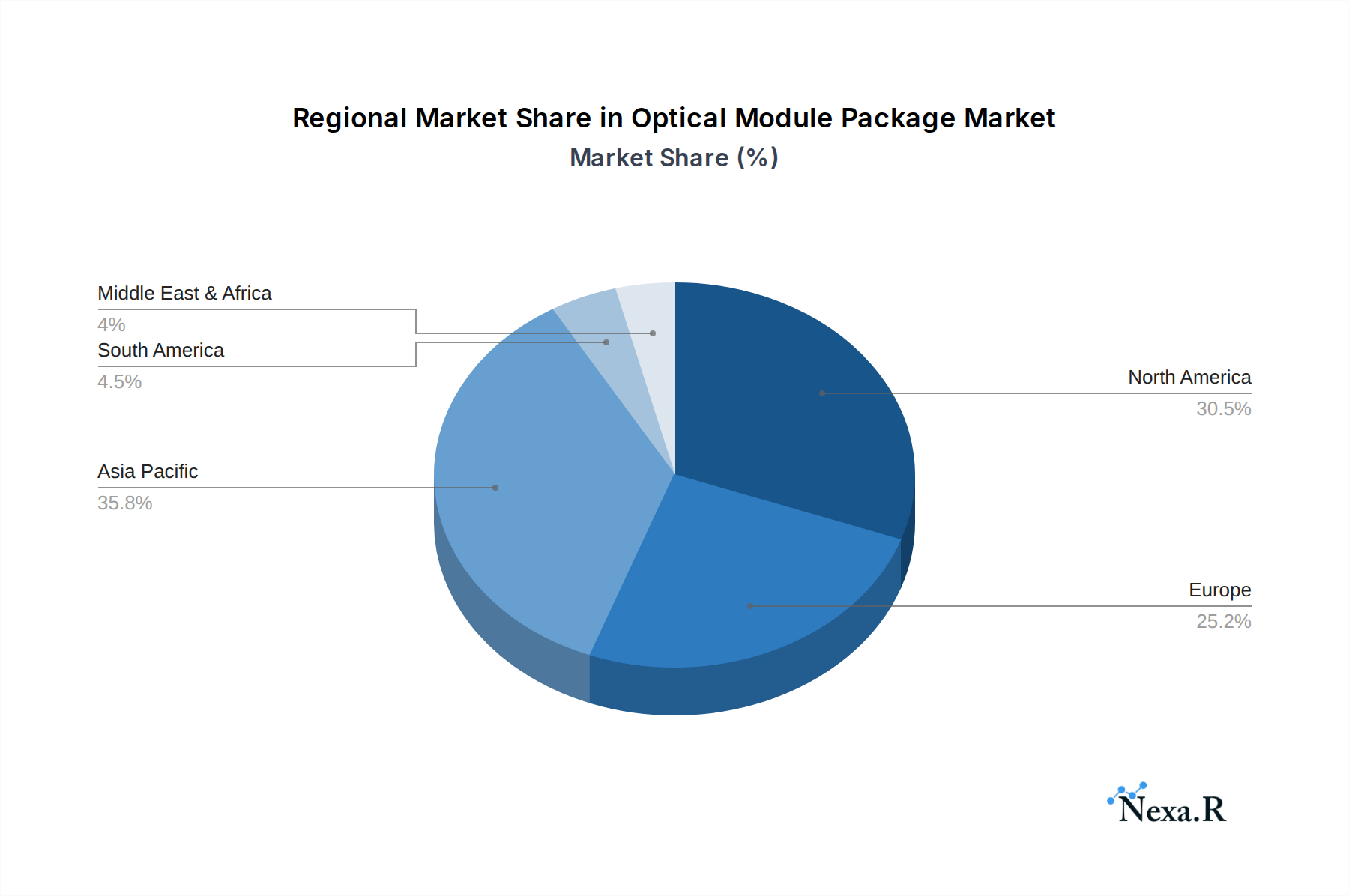

The Data Communication segment, encompassing the infrastructure powering hyperscale data centers and enterprise networks, is projected to be the dominant force driving growth in the global Optical Module Package market. This dominance is intricately linked to the ever-increasing demand for high-speed data transfer and processing capabilities, essential for cloud computing, big data analytics, and artificial intelligence applications. The QSFP-DD form factor is emerging as a leading type, driven by its capability to support 400GbE and future 800GbE speeds, making it indispensable for next-generation data center interconnects. North America, particularly the United States, is expected to lead market growth within this segment, fueled by significant investments in cloud infrastructure, hyperscale data center expansion, and the robust development of AI and machine learning technologies. Furthermore, governmental policies supporting digital transformation and innovation in the region create a conducive environment for market expansion. Asia Pacific, with its rapid economic development and massive adoption of digital services, including the extensive build-out of 5G networks, also presents a substantial growth opportunity. Within this region, countries like China are major hubs for both manufacturing and consumption of optical modules.

- Dominant Segment: Data Communication

- Key Drivers: Hyperscale data center expansion, cloud computing growth, AI/ML workloads, big data analytics.

- Market Share Projection: Expected to account for xx% of the global market by 2033.

- Leading Type: QSFP-DD

- Rationale: Support for 400GbE and future 800GbE speeds, essential for high-density networking.

- Growth Potential: Rapid adoption driven by data center upgrade cycles.

- Leading Region: North America

- Key Countries: United States

- Dominance Factors: Massive cloud infrastructure investments, hyperscale data center presence, government support for innovation, high adoption of advanced networking technologies.

- Significant Growth Region: Asia Pacific

- Key Countries: China, Japan, South Korea

- Growth Drivers: Extensive 5G network deployments, growing internet penetration, increasing digitalization across industries, strong manufacturing base for optical modules.

- Telecommunications Application: Remains a critical segment, with 5G deployment driving demand for various optical module types, especially for fronthaul and backhaul networks.

Optical Module Package Product Landscape

The optical module package market is witnessing continuous innovation focused on delivering higher bandwidth, increased energy efficiency, and smaller form factors. Key product developments include advanced packaging techniques for 400GbE, 800GbE, and beyond, catering to the escalating demands of data centers and telecommunications. The QSFP-DD, QSFP+/QSFP28, and emerging QSFP-DD variants are central to these advancements, offering enhanced performance and density. Unique selling propositions often revolve around improved thermal management, reduced power consumption per bit, and superior signal integrity, crucial for mission-critical applications. Technological advancements are pushing the boundaries of data transmission, enabling seamless connectivity for AI, 5G, and cloud infrastructure.

Key Drivers, Barriers & Challenges in Optical Module Package

Key Drivers:

- Accelerated 5G Deployment: The global rollout of 5G networks necessitates widespread deployment of high-speed optical modules for fronthaul, midhaul, and backhaul, significantly driving market demand.

- Data Center Expansion and Upgrades: The exponential growth of data traffic and the increasing adoption of cloud computing are fueling massive investments in data center infrastructure, requiring higher-bandwidth optical interconnects.

- AI and Machine Learning Workloads: The computational demands of AI and ML applications are driving the need for faster and more efficient data transfer within and between data centers, boosting demand for advanced optical modules.

- Technological Advancements in Optical Technologies: Innovations in silicon photonics, advanced modulation techniques, and efficient packaging are enabling higher data rates and improved performance, creating new market opportunities.

- Increasing demand for higher data rates: The continuous need for 100GbE, 400GbE, and upcoming 800GbE solutions to support bandwidth-intensive applications.

Barriers & Challenges:

- Supply Chain Disruptions and Component Shortages: Global supply chain vulnerabilities, exacerbated by geopolitical factors and unforeseen events, can lead to shortages of critical components, impacting production and lead times. A projected xx% impact on production capacity due to supply chain issues is anticipated.

- High Research & Development Costs: Developing cutting-edge optical module technology requires substantial investment in R&D, posing a barrier for smaller players.

- Intense Price Competition: The market is characterized by fierce price competition, particularly in high-volume segments, which can squeeze profit margins for manufacturers.

- Stringent Testing and Qualification Requirements: Meeting industry standards and ensuring interoperability requires rigorous testing and qualification processes, adding to development time and cost.

- Evolving Standards and Interoperability: The continuous evolution of industry standards and the need for seamless interoperability across different vendors can create complexity and potential compatibility issues.

Emerging Opportunities in Optical Module Package

Emerging opportunities in the Optical Module Package market lie in several key areas. The expansion of edge computing will create demand for compact and power-efficient optical modules for distributed network architectures. The growing adoption of optical networking in industrial IoT (IIoT) and automotive applications, such as advanced driver-assistance systems (ADAS), presents a new frontier for specialized optical solutions. Furthermore, the development of co-packaged optics (CPO) represents a significant long-term opportunity, promising further integration of optical components with silicon chips for enhanced performance and power efficiency. The increasing focus on sustainability and energy efficiency in data centers is also creating opportunities for greener optical module designs and manufacturing processes.

Growth Accelerators in the Optical Module Package Industry

Several factors are acting as significant growth accelerators for the Optical Module Package industry. The relentless pace of digital transformation across all sectors is a primary catalyst, creating a perpetual demand for faster and more robust networking infrastructure. Strategic partnerships between module manufacturers, semiconductor providers, and network equipment vendors are crucial for accelerating innovation and bringing new products to market more efficiently. Furthermore, the ongoing expansion of global data center capacity, driven by the insatiable demand for cloud services and AI capabilities, directly translates into increased demand for optical modules. The continued evolution and widespread adoption of higher data rates, such as 400GbE and the anticipated rise of 800GbE, are powerful market expansion strategies that propel industry growth.

Key Players Shaping the Optical Module Package Market

- Coherent

- InnoLight

- Cisco

- Huawei

- Accelink

- Hisense

- Eoptolink

- HGG

- Intel

- Source Photonics

- Kyocera

- Broadcom

- Sumitomo Electric Industries

- Gigalight

- ATOP Technology

- FIBERSTAMP

- FOIT

- Lumentum

- AOI

- Fujitsu

- CIGTECH

- Broadex Technologies

- Guangdong Unionman

Notable Milestones in Optical Module Package Sector

- 2021/Q4: Launch of industry-leading 400G ZR optical modules by multiple vendors, enabling wider reach and interoperability in metro networks.

- 2022/Q1: Significant advancements in silicon photonics integration, paving the way for more cost-effective and higher-density optical modules.

- 2022/Q3: Increased investment and development in co-packaged optics (CPO) solutions by major players, signaling a future direction for high-performance computing.

- 2023/Q2: Standardization efforts for 800G optical modules gain momentum, with initial prototypes demonstrated by leading manufacturers.

- 2023/Q4: Growing adoption of QSFP-DD form factors in hyperscale data centers for 400GbE deployments.

- 2024/Q1: Focus on power efficiency and thermal management solutions for high-speed optical modules to meet data center sustainability goals.

In-Depth Optical Module Package Market Outlook

The future outlook for the Optical Module Package market remains exceptionally strong, driven by the sustained growth of digital infrastructure. The relentless expansion of 5G, the ever-increasing computational demands of AI and big data, and the continued reliance on cloud services will serve as powerful growth accelerators. Strategic partnerships and technological breakthroughs in areas like silicon photonics and co-packaged optics are poised to redefine the market's landscape and unlock new levels of performance and efficiency. The ongoing evolution towards higher data rates, coupled with a focus on sustainable and power-efficient solutions, presents significant strategic opportunities for companies that can innovate and adapt to these evolving industry needs.

Optical Module Package Segmentation

-

1. Application

- 1.1. Telecommunications

- 1.2. Data Communication

-

2. Types

- 2.1. SFP/eSFP

- 2.2. XFP /SFP+

- 2.3. QSFP+/QSFP28

- 2.4. CXP/CXP2

- 2.5. CFP/CFP2

- 2.6. QSFP-DD

Optical Module Package Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Optical Module Package Regional Market Share

Geographic Coverage of Optical Module Package

Optical Module Package REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Telecommunications

- 5.1.2. Data Communication

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. SFP/eSFP

- 5.2.2. XFP /SFP+

- 5.2.3. QSFP+/QSFP28

- 5.2.4. CXP/CXP2

- 5.2.5. CFP/CFP2

- 5.2.6. QSFP-DD

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Optical Module Package Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Telecommunications

- 6.1.2. Data Communication

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. SFP/eSFP

- 6.2.2. XFP /SFP+

- 6.2.3. QSFP+/QSFP28

- 6.2.4. CXP/CXP2

- 6.2.5. CFP/CFP2

- 6.2.6. QSFP-DD

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Optical Module Package Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Telecommunications

- 7.1.2. Data Communication

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. SFP/eSFP

- 7.2.2. XFP /SFP+

- 7.2.3. QSFP+/QSFP28

- 7.2.4. CXP/CXP2

- 7.2.5. CFP/CFP2

- 7.2.6. QSFP-DD

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Optical Module Package Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Telecommunications

- 8.1.2. Data Communication

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. SFP/eSFP

- 8.2.2. XFP /SFP+

- 8.2.3. QSFP+/QSFP28

- 8.2.4. CXP/CXP2

- 8.2.5. CFP/CFP2

- 8.2.6. QSFP-DD

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Optical Module Package Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Telecommunications

- 9.1.2. Data Communication

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. SFP/eSFP

- 9.2.2. XFP /SFP+

- 9.2.3. QSFP+/QSFP28

- 9.2.4. CXP/CXP2

- 9.2.5. CFP/CFP2

- 9.2.6. QSFP-DD

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Optical Module Package Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Telecommunications

- 10.1.2. Data Communication

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. SFP/eSFP

- 10.2.2. XFP /SFP+

- 10.2.3. QSFP+/QSFP28

- 10.2.4. CXP/CXP2

- 10.2.5. CFP/CFP2

- 10.2.6. QSFP-DD

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Optical Module Package Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Telecommunications

- 11.1.2. Data Communication

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. SFP/eSFP

- 11.2.2. XFP /SFP+

- 11.2.3. QSFP+/QSFP28

- 11.2.4. CXP/CXP2

- 11.2.5. CFP/CFP2

- 11.2.6. QSFP-DD

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Coherent

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 InnoLight

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Cisco

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Huawei

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Accelink

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Hisense

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Eoptolink

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 HGG

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Intel

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Source Photonics

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Kyocera

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Broadcom

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Sumitomo Electric Industries

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Gigalight

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 ATOP Technology

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 FIBERSTAMP

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 FOIT

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Lumentum

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 AOI

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Fujitsu

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 CIGTECH

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 Broadex Technologies

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.23 Guangdong Unionman

- 12.1.23.1. Company Overview

- 12.1.23.2. Products

- 12.1.23.3. Company Financials

- 12.1.23.4. SWOT Analysis

- 12.1.1 Coherent

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Optical Module Package Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Optical Module Package Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Optical Module Package Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Optical Module Package Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Optical Module Package Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Optical Module Package Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Optical Module Package Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Optical Module Package Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Optical Module Package Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Optical Module Package Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Optical Module Package Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Optical Module Package Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Optical Module Package Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Optical Module Package Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Optical Module Package Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Optical Module Package Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Optical Module Package Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Optical Module Package Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Optical Module Package Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Optical Module Package Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Optical Module Package Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Optical Module Package Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Optical Module Package Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Optical Module Package Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Optical Module Package Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Optical Module Package Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Optical Module Package Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Optical Module Package Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Optical Module Package Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Optical Module Package Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Optical Module Package Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Optical Module Package Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Optical Module Package Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Optical Module Package Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Optical Module Package Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Optical Module Package Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Optical Module Package Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Optical Module Package Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Optical Module Package Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Optical Module Package Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Optical Module Package Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Optical Module Package Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Optical Module Package Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Optical Module Package Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Optical Module Package Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Optical Module Package Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Optical Module Package Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Optical Module Package Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Optical Module Package Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Optical Module Package Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Optical Module Package?

The projected CAGR is approximately 12.9%.

2. Which companies are prominent players in the Optical Module Package?

Key companies in the market include Coherent, InnoLight, Cisco, Huawei, Accelink, Hisense, Eoptolink, HGG, Intel, Source Photonics, Kyocera, Broadcom, Sumitomo Electric Industries, Gigalight, ATOP Technology, FIBERSTAMP, FOIT, Lumentum, AOI, Fujitsu, CIGTECH, Broadex Technologies, Guangdong Unionman.

3. What are the main segments of the Optical Module Package?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Optical Module Package," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Optical Module Package report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Optical Module Package?

To stay informed about further developments, trends, and reports in the Optical Module Package, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence