Key Insights

The global Ovality Sensors market is projected to experience significant expansion, reaching an estimated market size of 12.59 billion by 2025, with a projected CAGR of 8.88 through 2033. This growth is underpinned by the escalating demand for precise measurement and stringent quality control across various industrial sectors. The energy industry is a key contributor, where accurate monitoring of pipe and conduit dimensions is paramount for operational efficiency and safety, particularly in oil and gas operations. The chemical sector also heavily leverages ovality sensors for process optimization, ensuring product integrity, reducing waste, and improving production yields. Additionally, the mechanical sector benefits from these advanced sensors for enhanced manufacturing tolerance controls, fostering the development of more robust machinery and components.

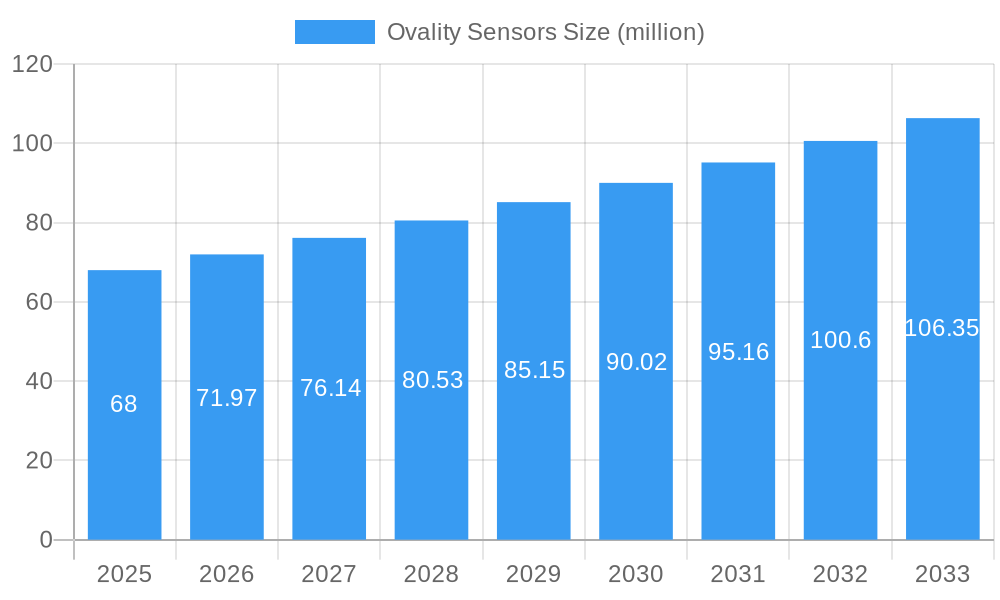

Ovality Sensors Market Size (In Billion)

Market growth is further accelerated by technological innovations and evolving industry benchmarks. Advancements in high-precision ovality sensors, featuring sophisticated data logging and real-time analytics, are meeting the rigorous demands of contemporary industrial operations. Emerging trends, including the integration of IoT and AI for predictive maintenance and remote monitoring, are opening new market opportunities. Despite this promising outlook, initial capital investment for advanced sensor systems and the requirement for specialized technical expertise may present challenges. Nevertheless, the substantial benefits of improved product quality, reduced operational expenses, and enhanced safety are anticipated to drive sustained and dynamic growth in the Ovality Sensors market.

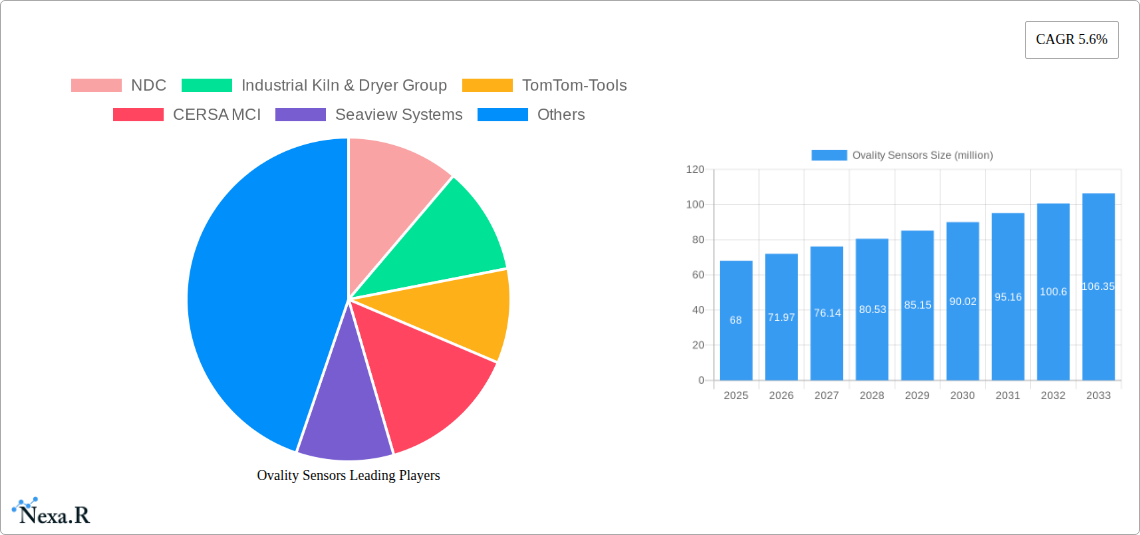

Ovality Sensors Company Market Share

Ovality Sensors Market Dynamics & Structure

The global Ovality Sensors market is characterized by a moderate to high concentration, with a few key players dominating the landscape. Technological innovation serves as a primary driver, fueled by advancements in sensor miniaturization, data analytics, and IoT integration, enabling real-time monitoring and predictive maintenance in critical industrial processes. Regulatory frameworks, particularly those concerning industrial safety and environmental compliance, also influence market adoption, pushing for more accurate and reliable measurement solutions. Competitive product substitutes, such as manual measurement tools or less sophisticated monitoring systems, are gradually being displaced by the superior precision and efficiency of modern ovality sensors. End-user demographics are diverse, spanning manufacturing, energy production, chemical processing, and heavy machinery operations, all seeking to optimize their processes and reduce downtime. Mergers and acquisitions (M&A) trends indicate a strategic consolidation, with larger entities acquiring innovative startups to expand their product portfolios and market reach.

- Market Concentration: Dominated by established players and innovative niche providers.

- Technological Innovation: Driven by IoT, AI integration, and advanced sensor materials.

- Regulatory Influence: Increasing demand for precision and compliance in industrial applications.

- End-User Diversity: Spans Energy, Chemical, Mechanical, and other industrial sectors.

- M&A Activity: Strategic acquisitions to enhance competitive positioning and technological capabilities.

Ovality Sensors Growth Trends & Insights

The Ovality Sensors market is poised for significant growth, projected to expand from an estimated $150 million in the base year of 2025 to $350 million by the end of the forecast period in 2033, exhibiting a compound annual growth rate (CAGR) of approximately 11.2%. This robust expansion is underpinned by an increasing awareness of the critical role these sensors play in enhancing operational efficiency, ensuring product quality, and preventing costly equipment failures across various industries. The adoption rates are steadily climbing as industries move towards Industry 4.0 principles, embracing automation and data-driven decision-making. Technological disruptions are a constant feature, with ongoing developments in non-contact measurement, wireless connectivity, and real-time data transmission capabilities revolutionizing how ovality is monitored. These advancements allow for continuous, precise measurements even in harsh industrial environments, a significant leap from historical manual inspection methods.

Consumer behavior shifts are also contributing to market growth. Manufacturers are increasingly prioritizing predictive maintenance strategies to minimize unplanned downtime and associated financial losses. This proactive approach directly benefits the ovality sensor market, as these devices provide essential data for identifying potential issues before they escalate. The ability of ovality sensors to detect subtle changes in component geometry, such as the wear of rotating shafts or the deformation of pipes, makes them indispensable for ensuring the longevity and optimal performance of critical machinery. Furthermore, the rising demand for higher quality standards in manufactured goods, particularly in sectors like automotive, aerospace, and pharmaceuticals, necessitates stringent quality control measures, further driving the adoption of advanced ovality sensing technologies. The integration of ovality sensor data into broader asset management systems allows for a holistic view of equipment health, enabling more informed maintenance scheduling and resource allocation. The increasing complexity of industrial machinery also necessitates sophisticated monitoring solutions, and ovality sensors are at the forefront of providing this crucial diagnostic information. The growth trajectory indicates a sustained demand, driven by both technological advancements and the imperative for operational excellence in a competitive global market.

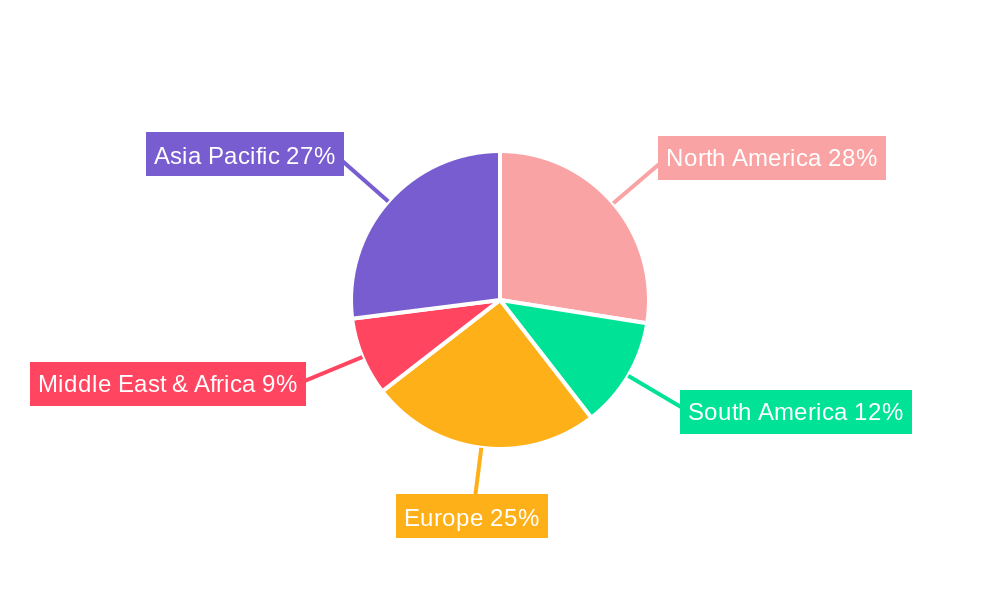

Dominant Regions, Countries, or Segments in Ovality Sensors

The global Ovality Sensors market is projected to witness significant growth across various regions, with North America emerging as a dominant force, driven by its advanced industrial infrastructure, substantial investments in research and development, and a strong emphasis on manufacturing automation. The United States, in particular, is a key contributor, boasting a robust chemical industry, a significant energy sector reliant on precise monitoring of pipelines and rotating machinery, and a burgeoning mechanical engineering segment that actively adopts cutting-edge sensor technologies. Economic policies in North America often incentivize technological adoption and industrial modernization, further bolstering the demand for advanced ovality sensing solutions. Infrastructure development and upgrades in the energy sector, including oil and gas exploration and renewable energy projects, create a continuous need for reliable measurement of component integrity.

Within the Application segment, the Energy sector stands out as a major growth driver. This is primarily due to the critical need for continuous monitoring of pipelines, turbines, and other rotating components in power generation, oil and gas extraction, and distribution networks. Ensuring the structural integrity and efficient operation of these assets is paramount for safety, environmental protection, and economic viability. The Chemical industry also represents a significant market, where precise monitoring of vessels, reactors, and rotating equipment is essential for maintaining product quality, process efficiency, and preventing hazardous leaks. In the Mechanical segment, the demand is driven by the automotive, aerospace, and heavy machinery manufacturing industries, where ovality sensors are crucial for quality control of manufactured parts and for predictive maintenance of production equipment.

In terms of Types, the Measuring Shaft Rotation type is expected to hold a dominant market share. This is attributed to the widespread application of rotating shafts in a vast array of industrial machinery, from electric motors and pumps to turbines and manufacturing equipment. The ability of these sensors to accurately measure shaft ovality provides crucial insights into wear, imbalance, and potential failure points, directly impacting operational reliability and maintenance schedules. The Table Rotation type, while important for specific applications like material handling and rotary indexing tables, is anticipated to grow at a slightly slower pace compared to shaft rotation sensors due to its more specialized application scope. The overall market dominance in North America is further solidified by the presence of leading manufacturing companies that are early adopters of advanced sensor technologies, coupled with a strong regulatory environment that mandates stringent safety and performance standards across industrial operations. The region's investment in smart manufacturing initiatives and the integration of IoT technologies in industrial processes further amplify the demand for sophisticated ovality sensing solutions, ensuring its continued leadership in the global market.

Ovality Sensors Product Landscape

The ovality sensors market is witnessing continuous product innovation, with manufacturers focusing on enhancing accuracy, miniaturization, and data integration capabilities. Key advancements include the development of non-contact optical sensors capable of measuring highly precise dimensions in challenging environments, as well as the integration of wireless communication protocols for seamless data transmission to cloud-based analytics platforms. These sensors offer superior performance metrics, such as high resolution (e.g., < 10 µm), fast response times (e.g., < 10 ms), and robust operability across wide temperature ranges (-40°C to +150°C). Unique selling propositions often lie in their ability to perform real-time monitoring, enabling predictive maintenance and reducing downtime. Technological advancements are also focused on developing sensors that are resistant to dust, moisture, and vibration, making them suitable for the demanding conditions found in the Energy, Chemical, and Mechanical industries.

Key Drivers, Barriers & Challenges in Ovality Sensors

The Ovality Sensors market is propelled by several key drivers: increasing demand for operational efficiency and predictive maintenance, stringent quality control requirements in manufacturing, and technological advancements in sensor technology leading to higher precision and data integration capabilities. The shift towards Industry 4.0 and smart manufacturing further fuels adoption.

- Drivers: Predictive maintenance adoption, strict quality standards, IoT integration, technological advancements.

However, the market faces several barriers and challenges: high initial investment costs for advanced systems, the need for skilled personnel for installation and maintenance, and potential resistance to adopting new technologies in some traditional industrial sectors. Supply chain disruptions and the availability of raw materials can also pose challenges, impacting production timelines and costs. Competitive pressures from established players and potential market saturation in certain niches can also restrain growth.

- Barriers & Challenges: High initial investment, need for skilled labor, industry inertia, supply chain volatility, competitive pressures.

Emerging Opportunities in Ovality Sensors

Emerging opportunities in the Ovality Sensors market lie in the expansion into underdeveloped industrial sectors and the development of specialized sensors for niche applications. The growing emphasis on sustainability and energy efficiency across all industries presents a significant opportunity for sensors that can optimize machinery performance and reduce energy consumption. Furthermore, advancements in artificial intelligence (AI) and machine learning (ML) are enabling the creation of "smart" ovality sensors that can not only measure but also analyze data to provide deeper insights into equipment health and potential failure modes. The increasing adoption of digital twins in manufacturing also creates a demand for highly accurate and real-time sensor data, including ovality measurements, to build and maintain reliable digital models.

Growth Accelerators in the Ovality Sensors Industry

Long-term growth in the Ovality Sensors industry will be accelerated by continuous technological breakthroughs, particularly in areas like non-contact measurement, advanced materials, and the seamless integration of sensors with AI-driven analytics platforms. Strategic partnerships between sensor manufacturers and original equipment manufacturers (OEMs) will be crucial for embedding these technologies into new machinery designs from the outset. Furthermore, market expansion into emerging economies, driven by industrialization and the adoption of modern manufacturing practices, will unlock new avenues for growth. The development of standardized data protocols and interoperability between different sensor systems will also foster wider adoption and create a more robust ecosystem.

Key Players Shaping the Ovality Sensors Market

- NDC

- Industrial Kiln & Dryer Group

- TomTom-Tools

- CERSA MCI

- Seaview Systems

- Havec

- OMS

- LIMAB

Notable Milestones in Ovality Sensors Sector

- 2019: Introduction of next-generation wireless ovality sensors with enhanced battery life and data transmission capabilities.

- 2020: Development of miniaturized, non-contact ovality sensors for use in highly confined industrial spaces.

- 2021: Integration of AI algorithms into ovality sensor systems for advanced predictive maintenance analytics.

- 2022: Strategic acquisition of a specialized sensor technology firm by a major industrial automation company to expand product offerings.

- 2023: Launch of robust, high-temperature ovality sensors designed for extreme operating conditions in the Energy sector.

- 2024: Increased adoption of IoT-enabled ovality sensors for real-time, cloud-based monitoring in chemical processing plants.

In-Depth Ovality Sensors Market Outlook

The future outlook for the Ovality Sensors market is exceptionally bright, driven by a confluence of technological innovation, increasing industrial automation, and a global push for enhanced operational efficiency and product quality. Growth accelerators such as advancements in AI for predictive analytics, the development of ultra-precise non-contact measurement technologies, and the expanding adoption of Industry 4.0 principles will continue to shape the market landscape. Strategic partnerships and the growing demand from emerging economies represent significant untapped potential. The market is poised for sustained growth, offering considerable strategic opportunities for companies that can innovate and adapt to the evolving needs of the industrial sector.

Ovality Sensors Segmentation

-

1. Application

- 1.1. Energy

- 1.2. Chemical

- 1.3. Mechanical

- 1.4. Others

-

2. Types

- 2.1. Measuring Shaft Rotation type

- 2.2. Table Rotation

Ovality Sensors Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ovality Sensors Regional Market Share

Geographic Coverage of Ovality Sensors

Ovality Sensors REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.88% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Energy

- 5.1.2. Chemical

- 5.1.3. Mechanical

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Measuring Shaft Rotation type

- 5.2.2. Table Rotation

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Ovality Sensors Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Energy

- 6.1.2. Chemical

- 6.1.3. Mechanical

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Measuring Shaft Rotation type

- 6.2.2. Table Rotation

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Ovality Sensors Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Energy

- 7.1.2. Chemical

- 7.1.3. Mechanical

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Measuring Shaft Rotation type

- 7.2.2. Table Rotation

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Ovality Sensors Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Energy

- 8.1.2. Chemical

- 8.1.3. Mechanical

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Measuring Shaft Rotation type

- 8.2.2. Table Rotation

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Ovality Sensors Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Energy

- 9.1.2. Chemical

- 9.1.3. Mechanical

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Measuring Shaft Rotation type

- 9.2.2. Table Rotation

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Ovality Sensors Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Energy

- 10.1.2. Chemical

- 10.1.3. Mechanical

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Measuring Shaft Rotation type

- 10.2.2. Table Rotation

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Ovality Sensors Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Energy

- 11.1.2. Chemical

- 11.1.3. Mechanical

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Measuring Shaft Rotation type

- 11.2.2. Table Rotation

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 NDC

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Industrial Kiln & Dryer Group

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 TomTom-Tools

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 CERSA MCI

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Seaview Systems

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Havec

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 OMS

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 LIMAB

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.1 NDC

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Ovality Sensors Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Ovality Sensors Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Ovality Sensors Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Ovality Sensors Volume (K), by Application 2025 & 2033

- Figure 5: North America Ovality Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Ovality Sensors Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Ovality Sensors Revenue (billion), by Types 2025 & 2033

- Figure 8: North America Ovality Sensors Volume (K), by Types 2025 & 2033

- Figure 9: North America Ovality Sensors Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Ovality Sensors Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Ovality Sensors Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Ovality Sensors Volume (K), by Country 2025 & 2033

- Figure 13: North America Ovality Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Ovality Sensors Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Ovality Sensors Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Ovality Sensors Volume (K), by Application 2025 & 2033

- Figure 17: South America Ovality Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Ovality Sensors Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Ovality Sensors Revenue (billion), by Types 2025 & 2033

- Figure 20: South America Ovality Sensors Volume (K), by Types 2025 & 2033

- Figure 21: South America Ovality Sensors Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Ovality Sensors Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Ovality Sensors Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Ovality Sensors Volume (K), by Country 2025 & 2033

- Figure 25: South America Ovality Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Ovality Sensors Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Ovality Sensors Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Ovality Sensors Volume (K), by Application 2025 & 2033

- Figure 29: Europe Ovality Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Ovality Sensors Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Ovality Sensors Revenue (billion), by Types 2025 & 2033

- Figure 32: Europe Ovality Sensors Volume (K), by Types 2025 & 2033

- Figure 33: Europe Ovality Sensors Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Ovality Sensors Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Ovality Sensors Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Ovality Sensors Volume (K), by Country 2025 & 2033

- Figure 37: Europe Ovality Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Ovality Sensors Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Ovality Sensors Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Ovality Sensors Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Ovality Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Ovality Sensors Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Ovality Sensors Revenue (billion), by Types 2025 & 2033

- Figure 44: Middle East & Africa Ovality Sensors Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Ovality Sensors Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Ovality Sensors Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Ovality Sensors Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Ovality Sensors Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Ovality Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Ovality Sensors Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Ovality Sensors Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Ovality Sensors Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Ovality Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Ovality Sensors Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Ovality Sensors Revenue (billion), by Types 2025 & 2033

- Figure 56: Asia Pacific Ovality Sensors Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Ovality Sensors Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Ovality Sensors Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Ovality Sensors Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Ovality Sensors Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Ovality Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Ovality Sensors Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ovality Sensors Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Ovality Sensors Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Ovality Sensors Revenue billion Forecast, by Types 2020 & 2033

- Table 4: Global Ovality Sensors Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Ovality Sensors Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Ovality Sensors Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Ovality Sensors Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Ovality Sensors Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Ovality Sensors Revenue billion Forecast, by Types 2020 & 2033

- Table 10: Global Ovality Sensors Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Ovality Sensors Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Ovality Sensors Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Ovality Sensors Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Ovality Sensors Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Ovality Sensors Revenue billion Forecast, by Types 2020 & 2033

- Table 22: Global Ovality Sensors Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Ovality Sensors Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Ovality Sensors Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Ovality Sensors Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Ovality Sensors Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Ovality Sensors Revenue billion Forecast, by Types 2020 & 2033

- Table 34: Global Ovality Sensors Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Ovality Sensors Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Ovality Sensors Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Ovality Sensors Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Ovality Sensors Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Ovality Sensors Revenue billion Forecast, by Types 2020 & 2033

- Table 58: Global Ovality Sensors Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Ovality Sensors Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Ovality Sensors Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Ovality Sensors Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Ovality Sensors Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Ovality Sensors Revenue billion Forecast, by Types 2020 & 2033

- Table 76: Global Ovality Sensors Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Ovality Sensors Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Ovality Sensors Volume K Forecast, by Country 2020 & 2033

- Table 79: China Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Ovality Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Ovality Sensors Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ovality Sensors?

The projected CAGR is approximately 8.88%.

2. Which companies are prominent players in the Ovality Sensors?

Key companies in the market include NDC, Industrial Kiln & Dryer Group, TomTom-Tools, CERSA MCI, Seaview Systems, Havec, OMS, LIMAB.

3. What are the main segments of the Ovality Sensors?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.59 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ovality Sensors," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ovality Sensors report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ovality Sensors?

To stay informed about further developments, trends, and reports in the Ovality Sensors, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence