Key Insights

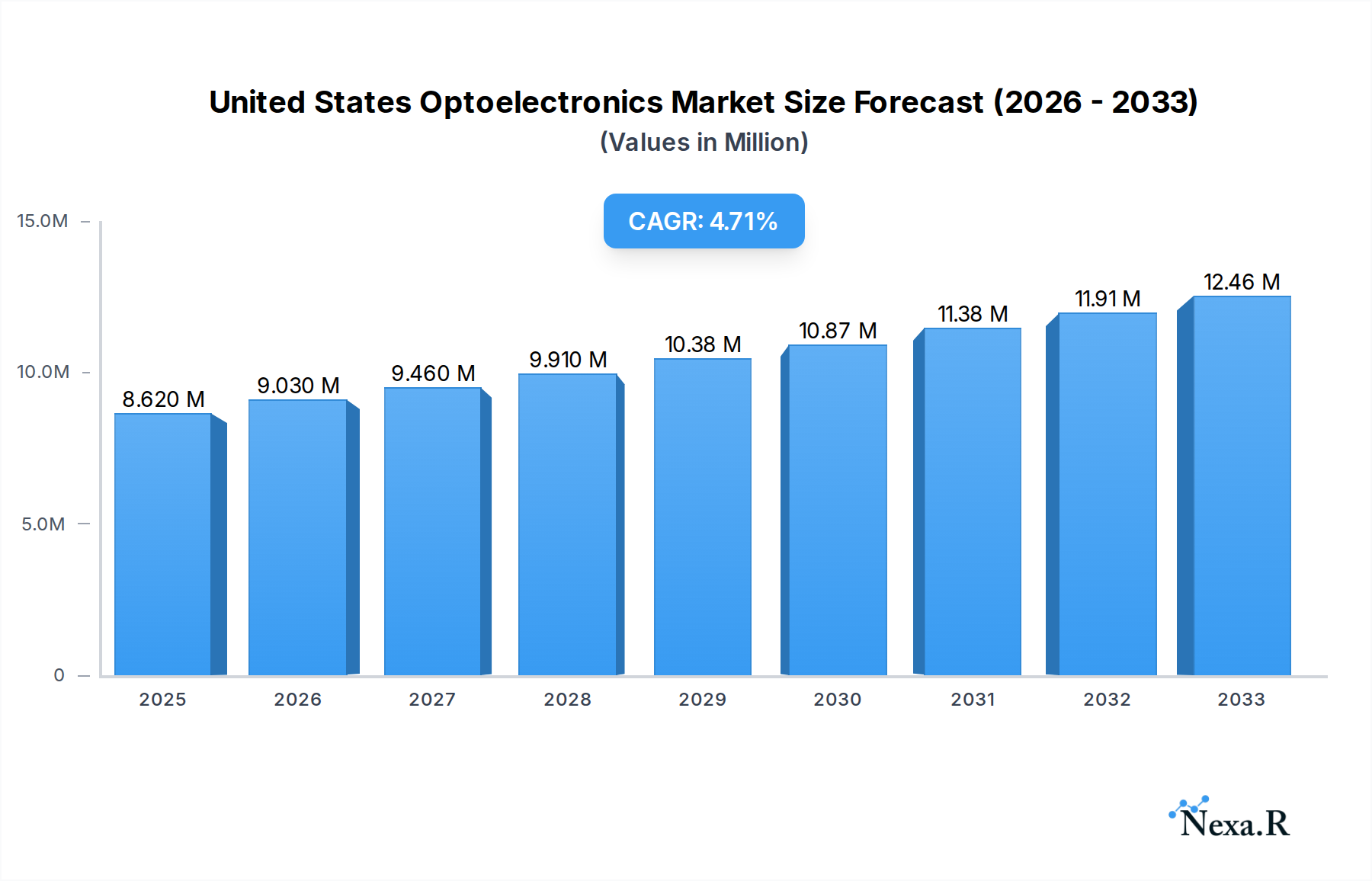

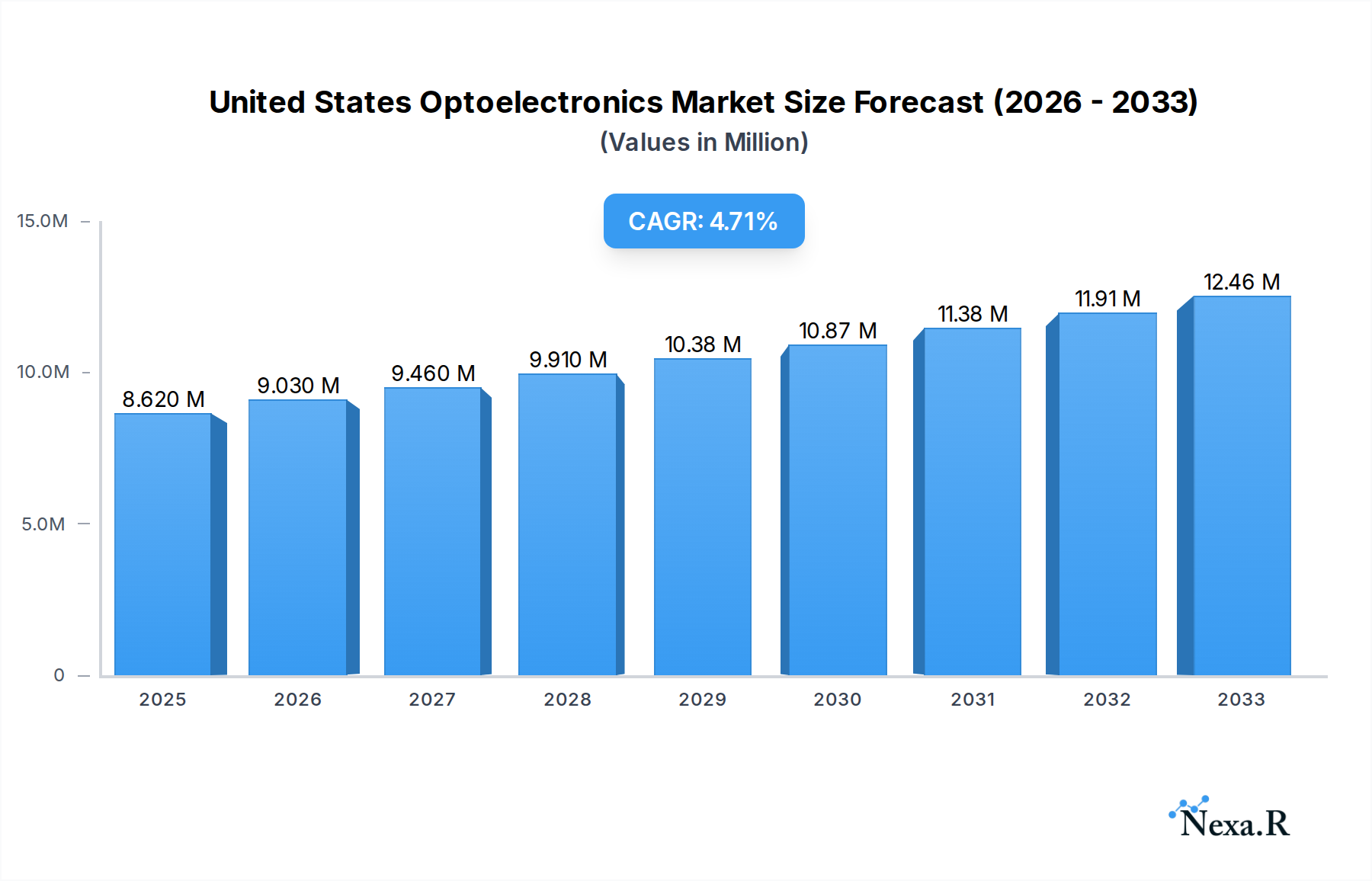

The United States optoelectronics market is poised for substantial growth, projecting a market size of USD 8.62 million with a Compound Annual Growth Rate (CAGR) of 4.70% during the forecast period of 2025-2033. This expansion is primarily driven by the burgeoning demand for advanced electronic components across various sectors. Key growth catalysts include the rapid adoption of light-emitting diodes (LEDs) in lighting and display technologies, the increasing prevalence of laser diodes in industrial applications, telecommunications, and medical devices, and the critical role of image sensors in automotive safety systems, consumer electronics, and surveillance. Furthermore, the robust expansion of the healthcare industry's reliance on optoelectronic devices for diagnostics and treatment, alongside the significant integration of optocouplers and photovoltaic cells in renewable energy solutions and industrial automation, are further fueling this market's upward trajectory. The ongoing technological advancements, miniaturization of components, and enhanced performance characteristics are making optoelectronic devices indispensable across a wide spectrum of applications.

United States Optoelectronics Market Market Size (In Million)

The market landscape is characterized by dynamic trends such as the shift towards more energy-efficient lighting solutions, the growing demand for high-resolution image sensors in autonomous driving and augmented reality, and the continuous innovation in laser technology for precision manufacturing and advanced communication networks. However, certain restraints, including the high initial investment costs for some optoelectronic manufacturing processes and the potential for supply chain disruptions, could pose challenges. Despite these, the increasing integration of optoelectronics in the aerospace and defense sector for advanced sensing and communication systems, coupled with the persistent demand from the consumer electronics and information technology industries, ensures a positive outlook. The United States, with its strong R&D capabilities and early adoption of cutting-edge technologies, is well-positioned to lead this market expansion. Key players like Samsung Electronics, Sony Corporation, and Broadcom Inc. are actively investing in innovation and strategic partnerships to capture market share.

United States Optoelectronics Market Company Market Share

This comprehensive report offers an in-depth analysis of the United States optoelectronics market, providing granular insights into its dynamics, growth trends, and competitive landscape. Covering the period from 2019 to 2033, with a base year of 2025, this study delves into the intricate interplay of segments, device types, and end-user industries shaping the future of optoelectronic technologies in the US. With a particular focus on LEDs, laser diodes, image sensors, and optocouplers, this report details market size evolution, adoption rates, and technological disruptions. We explore key drivers such as advancements in consumer electronics, the burgeoning automotive sector, and critical applications in healthcare and industrial automation. This report is essential for industry professionals, investors, and strategists seeking to understand and capitalize on the opportunities within this rapidly evolving market.

United States Optoelectronics Market Market Dynamics & Structure

The United States optoelectronics market is characterized by a dynamic and evolving structure, driven by intense technological innovation and a diverse range of end-user applications. Market concentration varies across sub-segments, with mature areas like LED lighting exhibiting a more consolidated competitive landscape, while emerging fields such as advanced laser diodes and specialized image sensors show greater fragmentation. Technological innovation acts as a primary driver, fueled by significant R&D investments by leading companies seeking to enhance performance, reduce costs, and develop novel functionalities. Regulatory frameworks, particularly those related to safety standards for laser diodes and energy efficiency for LEDs, play a crucial role in shaping product development and market access.

- Market Concentration: While some segments, like general lighting LEDs, are dominated by a few large players, others, such as specialized sensing applications, feature a more fragmented supplier base.

- Technological Innovation Drivers: Miniaturization, increased power efficiency, higher resolution for image sensors, and advancements in wavelength control for laser diodes are key innovation areas.

- Regulatory Frameworks: Standards from organizations like the FDA for laser safety and DOE for lighting efficiency influence product design and adoption.

- Competitive Product Substitutes: While direct substitutes are limited for many optoelectronic components, advancements in alternative sensing technologies (e.g., non-optical sensors) and display technologies can pose indirect competition.

- End-User Demographics: The demand is heavily influenced by the growth of sectors like automotive (ADAS, lighting), consumer electronics (smartphones, wearables), and industrial automation.

- M&A Trends: Mergers and acquisitions are prevalent as larger companies seek to acquire specialized technologies, expand their product portfolios, or gain market share. For instance, the acquisition of sensor companies by larger technology conglomerates highlights this trend. The volume of M&A deals in the semiconductor and related component industries has seen a steady flow, with approximately 15-25 significant transactions annually in the broader semiconductor space impacting optoelectronics.

United States Optoelectronics Market Growth Trends & Insights

The United States optoelectronics market is poised for substantial growth, driven by a confluence of technological advancements and escalating demand across diverse sectors. The market size is projected to expand significantly, with an estimated CAGR of approximately 8.5% from 2025 to 2033. This robust growth is underpinned by increasing adoption rates of advanced optoelectronic components in critical applications. For example, the penetration of high-resolution image sensors in smartphones and automotive cameras is nearing saturation in premium segments, while their adoption in mid-range devices and specialized automotive applications continues to climb.

Technological disruptions are a constant feature of this market. The continuous evolution of LED technology, leading to greater energy efficiency and brighter outputs, is transforming lighting solutions in residential, commercial, and industrial settings. Similarly, advancements in laser diode technology are opening new avenues in telecommunications, medical devices, and industrial processing. Consumer behavior shifts also play a pivotal role; the growing preference for smart home devices, wearable technology, and advanced driver-assistance systems (ADAS) in vehicles directly translates into increased demand for sophisticated optoelectronic components like image sensors, proximity sensors, and LiDAR. The expansion of 5G infrastructure also necessitates high-performance optical components for data transmission.

The adoption of miniaturized and power-efficient optoelectronic devices is accelerating as manufacturers strive to meet the demands of portable electronics and the Internet of Things (IoT). Furthermore, the increasing focus on health monitoring and diagnostics is spurring innovation and adoption of optical sensors in healthcare devices. The market penetration of specialized optoelectronic devices, such as those used in augmented reality (AR) and virtual reality (VR) headsets, is still in its early stages but shows immense potential for future expansion. The overall market is transitioning from commodity-driven sales to value-added solutions, with an emphasis on customized components and integrated systems. The market penetration of advanced LED lighting in the commercial sector is estimated to be around 70%, with significant growth still expected in retrofitting older installations and in specialized architectural lighting. The automotive segment’s adoption of advanced driver-assistance systems, heavily reliant on image sensors and LiDAR, is projected to reach over 90% of new vehicle sales by 2030.

Dominant Regions, Countries, or Segments in United States Optoelectronics Market

The Consumer Electronics segment, alongside the Automotive industry, stands as a dominant force driving growth within the United States optoelectronics market. These sectors collectively represent a significant portion of the market share, estimated to be around 45-50% when combined. The relentless pace of innovation and high consumer demand for sophisticated features in devices like smartphones, smart televisions, wearables, and gaming consoles directly fuels the demand for advanced optoelectronic components such as high-resolution image sensors, efficient LEDs for displays and lighting, and proximity sensors.

In the Automotive sector, the integration of optoelectronics is undergoing a profound transformation. The increasing adoption of Advanced Driver-Assistance Systems (ADAS), autonomous driving technologies, and sophisticated in-car infotainment systems necessitates a wide array of optoelectronic solutions. This includes LiDAR for environmental sensing, image sensors for cameras, LED lighting for both exterior (adaptive headlights, dynamic tail lights) and interior applications, and optical sensors for various monitoring functions. The push for enhanced safety, driver comfort, and personalized in-car experiences ensures a continuous demand for cutting-edge optoelectronic components. The government’s focus on road safety and the automotive industry’s commitment to innovation further bolster this segment.

Beyond these two giants, the Information Technology sector, encompassing data centers, networking equipment, and computing devices, is another crucial growth engine. The demand for high-speed data transmission, driven by cloud computing and the expansion of 5G networks, necessitates advanced optical transceivers and fiber optic components. The increasing need for efficient cooling and illuminated interfaces also contributes to the demand for LEDs and other optical solutions. The Healthcare sector, while perhaps smaller in absolute terms, presents a high-growth opportunity due to the increasing application of optoelectronics in medical imaging, diagnostics, surgical tools, and patient monitoring devices.

- Dominant Segments:

- Consumer Electronics: Driven by smartphones, tablets, wearables, and smart home devices. Expected to hold a market share of approximately 30-35% by 2028.

- Automotive: Fueled by ADAS, autonomous driving, and advanced lighting systems. Forecasted to represent 15-20% of the market by 2028.

- Key Drivers for Dominance:

- Technological Advancements: Continuous innovation in image sensor resolution, LED efficiency, and laser diode capabilities.

- Consumer Demand: High consumer appetite for advanced features and smart functionalities in electronics and vehicles.

- Government Initiatives: Support for technological development and safety standards in automotive and IT sectors.

- Infrastructure Development: Expansion of 5G networks and data centers driving demand for optical communication components.

- Healthcare Innovation: Growing application of optoelectronics in medical devices and diagnostics.

United States Optoelectronics Market Product Landscape

The United States optoelectronics market is characterized by a diverse and rapidly evolving product landscape, with continuous innovation driving enhanced performance and novel applications. Key product categories include Light Emitting Diodes (LEDs), which have seen advancements in efficiency, color rendering, and form factors for a wide array of lighting and display applications. Laser Diodes are crucial for telecommunications, industrial processing, and medical devices, with ongoing developments in power output, wavelength precision, and miniaturization. Image Sensors, integral to digital imaging and sensing technologies, are seeing improvements in resolution, sensitivity, and low-light performance, enabling sophisticated applications in mobile devices, automotive, and security systems. Optocouplers, vital for electrical isolation in various industrial and consumer applications, are becoming smaller and more robust. Photovoltaic cells, while a distinct category, are also seeing advancements in efficiency and integration for energy harvesting.

Key Drivers, Barriers & Challenges in United States Optoelectronics Market

Key Drivers:

The United States optoelectronics market is propelled by several key drivers. The rapid advancement in artificial intelligence and machine learning algorithms, which rely heavily on high-quality data from image sensors, is a significant growth catalyst. The expanding adoption of advanced driver-assistance systems (ADAS) and the pursuit of autonomous vehicles are creating substantial demand for LiDAR, radar, and sophisticated image sensors. Furthermore, the continuous growth of the consumer electronics sector, with a constant stream of new products featuring enhanced visual displays and integrated sensing capabilities, acts as a perpetual demand generator. Investments in next-generation communication infrastructure, such as 5G and beyond, are also driving demand for high-speed optical components.

Barriers & Challenges:

Despite strong growth potential, the market faces several barriers and challenges. Intense global competition, particularly from Asian manufacturers offering cost-effective solutions, puts pressure on domestic pricing and margins. Supply chain disruptions, exacerbated by geopolitical factors and global events, can lead to component shortages and increased lead times, impacting production schedules. Stringent regulatory requirements, especially for applications in healthcare and aerospace, add to the complexity and cost of product development and certification. The high cost of research and development for next-generation optoelectronic technologies can be a significant barrier for smaller companies. Furthermore, the need for skilled labor to design, manufacture, and integrate these complex components poses a challenge for workforce development.

Emerging Opportunities in United States Optoelectronics Market

Emerging opportunities within the United States optoelectronics market are abundant, stemming from new technological frontiers and evolving consumer needs. The burgeoning field of augmented reality (AR) and virtual reality (VR) presents a significant avenue for growth, requiring advanced display technologies, high-resolution image sensors, and sophisticated optical components for immersive experiences. The increasing focus on sustainable energy solutions is driving demand for highly efficient photovoltaic cells and optoelectronic components for energy management systems. The expansion of smart cities initiatives, with their emphasis on intelligent infrastructure, sensor networks, and advanced lighting solutions, offers substantial opportunities for various optoelectronic devices. Furthermore, the growing application of optical technologies in advanced manufacturing, robotics, and inspection systems points towards a robust future for industrial optoelectronics. The integration of optoelectronics in the burgeoning quantum computing sector also represents a significant, albeit long-term, opportunity.

Growth Accelerators in the United States Optoelectronics Market Industry

Several factors are acting as significant growth accelerators for the United States optoelectronics industry. Technological breakthroughs in materials science are enabling the development of more efficient and cost-effective optoelectronic components, such as perovskite solar cells and new generations of quantum dots for displays and lighting. Strategic partnerships between established technology giants and innovative startups are fostering rapid product development and market penetration of novel solutions. The increasing government funding and support for research and development in areas like advanced manufacturing, AI, and next-generation communications are also providing a strong impetus for growth. Furthermore, the expansion of e-commerce and the growing demand for customized and personalized electronic products are encouraging manufacturers to develop agile production lines and offer a wider range of specialized optoelectronic components.

Key Players Shaping the United States Optoelectronics Market Market

- SK Hynix Inc

- Panasonic Corporation

- Samsung Electronics

- Omnivision Technologies Inc

- Sony Corporation

- Osram Licht AG

- Koninklijke Philips N V

- Vishay Intertechnology Inc

- Texas Instruments Inc

- LITE-ON Technology Corporation

- Rohm Co Ltd (ROHM SEMICONDUCTOR)

- Mitsubishi Electric Corporation

- Broadcom Inc

- Sharp Corporation

Notable Milestones in United States Optoelectronics Market Sector

- January 2024: AMS Osram AG introduced SYNIOS P1515 side looker low-power LEDs. This innovation streamlines design for automotive light bars and rear lighting, offering uniform illumination and enabling slimmer optical assemblies, enhancing vehicle aesthetics and functionality.

- December 2023: Marktech Optoelectronics, Inc. launched enhanced sharpness 25 and 50 micron green dot point source LEDs (MTSP-1358 and MTSP-1360). These are designed for precision aiming applications, including reflex sights and camera viewfinders, significantly improving accuracy and performance in sports optics and other sighting devices. The company also expanded its red dot LED offerings with additional micron sizes and package options, demonstrating a commitment to serving niche optical markets.

In-Depth United States Optoelectronics Market Market Outlook

The United States optoelectronics market is set for an optimistic future, driven by relentless innovation and the increasing integration of optoelectronic components across a spectrum of industries. Future market potential is significantly amplified by the accelerating advancements in artificial intelligence and the expanding capabilities of autonomous systems, which rely heavily on sophisticated image sensors and LiDAR. The ongoing digital transformation and the expansion of high-speed communication networks will continue to fuel demand for advanced optical components. Strategic opportunities lie in leveraging the growing interest in personalized healthcare, smart home technologies, and sustainable energy solutions, where optoelectronics play a pivotal role. The market is expected to witness a paradigm shift towards integrated optoelectronic systems and highly specialized solutions, creating a fertile ground for companies that can deliver cutting-edge technology and value-added services.

United States Optoelectronics Market Segmentation

-

1. Device Type

- 1.1. LED

- 1.2. Laser Diode

- 1.3. Image Sensors

- 1.4. Optocouplers

- 1.5. Photovoltaic cells

- 1.6. Others

-

2. End-User Industry

- 2.1. Automotive

- 2.2. Aerospace & Defense

- 2.3. Consumer Electronics

- 2.4. Information Technology

- 2.5. Healthcare

- 2.6. Residential and Commercial

- 2.7. Industrial

- 2.8. Others

United States Optoelectronics Market Segmentation By Geography

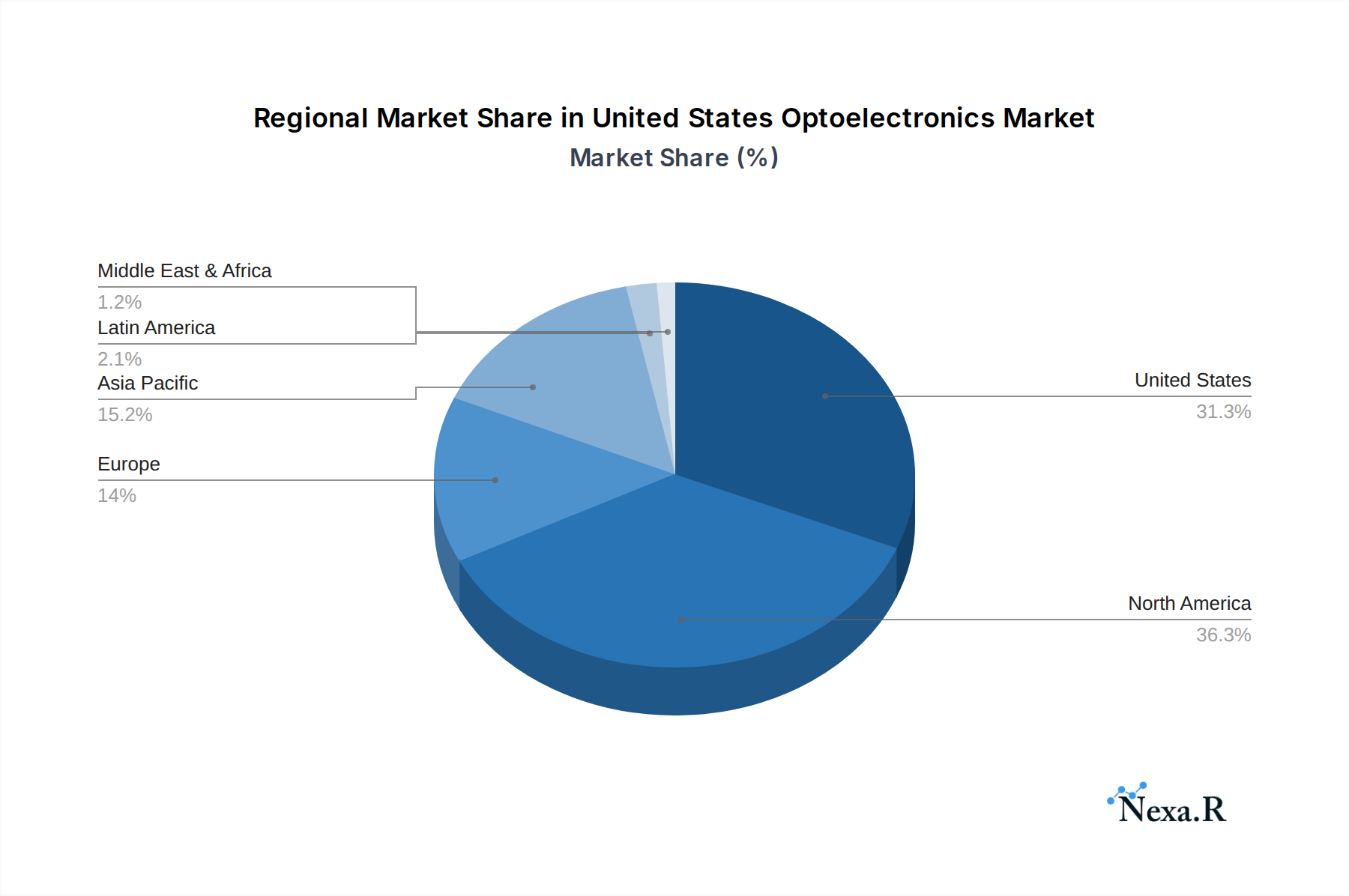

- 1. United States

United States Optoelectronics Market Regional Market Share

Geographic Coverage of United States Optoelectronics Market

United States Optoelectronics Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.70% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 5.1.1. LED

- 5.1.2. Laser Diode

- 5.1.3. Image Sensors

- 5.1.4. Optocouplers

- 5.1.5. Photovoltaic cells

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by End-User Industry

- 5.2.1. Automotive

- 5.2.2. Aerospace & Defense

- 5.2.3. Consumer Electronics

- 5.2.4. Information Technology

- 5.2.5. Healthcare

- 5.2.6. Residential and Commercial

- 5.2.7. Industrial

- 5.2.8. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 6. United States Optoelectronics Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 6.1.1. LED

- 6.1.2. Laser Diode

- 6.1.3. Image Sensors

- 6.1.4. Optocouplers

- 6.1.5. Photovoltaic cells

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by End-User Industry

- 6.2.1. Automotive

- 6.2.2. Aerospace & Defense

- 6.2.3. Consumer Electronics

- 6.2.4. Information Technology

- 6.2.5. Healthcare

- 6.2.6. Residential and Commercial

- 6.2.7. Industrial

- 6.2.8. Others

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 SK Hynix Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Panasonic Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Samsung Electronics

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Omnivision Technologies Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Sony Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Osram Licht AG

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Koninklijke Philips N V

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Vishay Intertechnology Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Texas Instruments Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 LITE-ON Technology Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Rohm Co Ltd (ROHM SEMICONDUCTOR)

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Mitsubishi Electric Corporation

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Broadcom Inc

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Sharp Corporatio

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.1 SK Hynix Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United States Optoelectronics Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: United States Optoelectronics Market Share (%) by Company 2025

List of Tables

- Table 1: United States Optoelectronics Market Revenue Million Forecast, by Device Type 2020 & 2033

- Table 2: United States Optoelectronics Market Volume Billion Forecast, by Device Type 2020 & 2033

- Table 3: United States Optoelectronics Market Revenue Million Forecast, by End-User Industry 2020 & 2033

- Table 4: United States Optoelectronics Market Volume Billion Forecast, by End-User Industry 2020 & 2033

- Table 5: United States Optoelectronics Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: United States Optoelectronics Market Volume Billion Forecast, by Region 2020 & 2033

- Table 7: United States Optoelectronics Market Revenue Million Forecast, by Device Type 2020 & 2033

- Table 8: United States Optoelectronics Market Volume Billion Forecast, by Device Type 2020 & 2033

- Table 9: United States Optoelectronics Market Revenue Million Forecast, by End-User Industry 2020 & 2033

- Table 10: United States Optoelectronics Market Volume Billion Forecast, by End-User Industry 2020 & 2033

- Table 11: United States Optoelectronics Market Revenue Million Forecast, by Country 2020 & 2033

- Table 12: United States Optoelectronics Market Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Optoelectronics Market?

The projected CAGR is approximately 4.70%.

2. Which companies are prominent players in the United States Optoelectronics Market?

Key companies in the market include SK Hynix Inc, Panasonic Corporation, Samsung Electronics, Omnivision Technologies Inc, Sony Corporation, Osram Licht AG, Koninklijke Philips N V, Vishay Intertechnology Inc, Texas Instruments Inc, LITE-ON Technology Corporation, Rohm Co Ltd (ROHM SEMICONDUCTOR), Mitsubishi Electric Corporation, Broadcom Inc, Sharp Corporatio.

3. What are the main segments of the United States Optoelectronics Market?

The market segments include Device Type, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.62 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Smart Consumer Electronics and Next-Generation Technologies; Increasing Industrial Applications of the Technology; Expansion of the Li-Fi Market.

6. What are the notable trends driving market growth?

The Image Sensors Segment Anticipated to Drive Demand.

7. Are there any restraints impacting market growth?

Growing Demand for Smart Consumer Electronics and Next-Generation Technologies; Increasing Industrial Applications of the Technology; Expansion of the Li-Fi Market.

8. Can you provide examples of recent developments in the market?

January 2024 - AMS Osram AG introduced a line of low-power LEDs, named SYNIOS P1515 side lookers, designed to streamline design processes, enhance implementation, and facilitate the creation of uniform lighting in extended automotive light bars and rear lighting applications. As per the company, by opting for these side-looker LEDs over traditional top-looker ones, automakers can achieve a consistent appearance spanning the vehicle's width. Furthermore, utilizing the same LED count as a top looker setup, these side lookers allow for significantly slimmer and more straightforward optical assemblies in rear combination lamps and turn indicators.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Optoelectronics Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Optoelectronics Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Optoelectronics Market?

To stay informed about further developments, trends, and reports in the United States Optoelectronics Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence