Key Insights into Wetland Management Service Market Trends

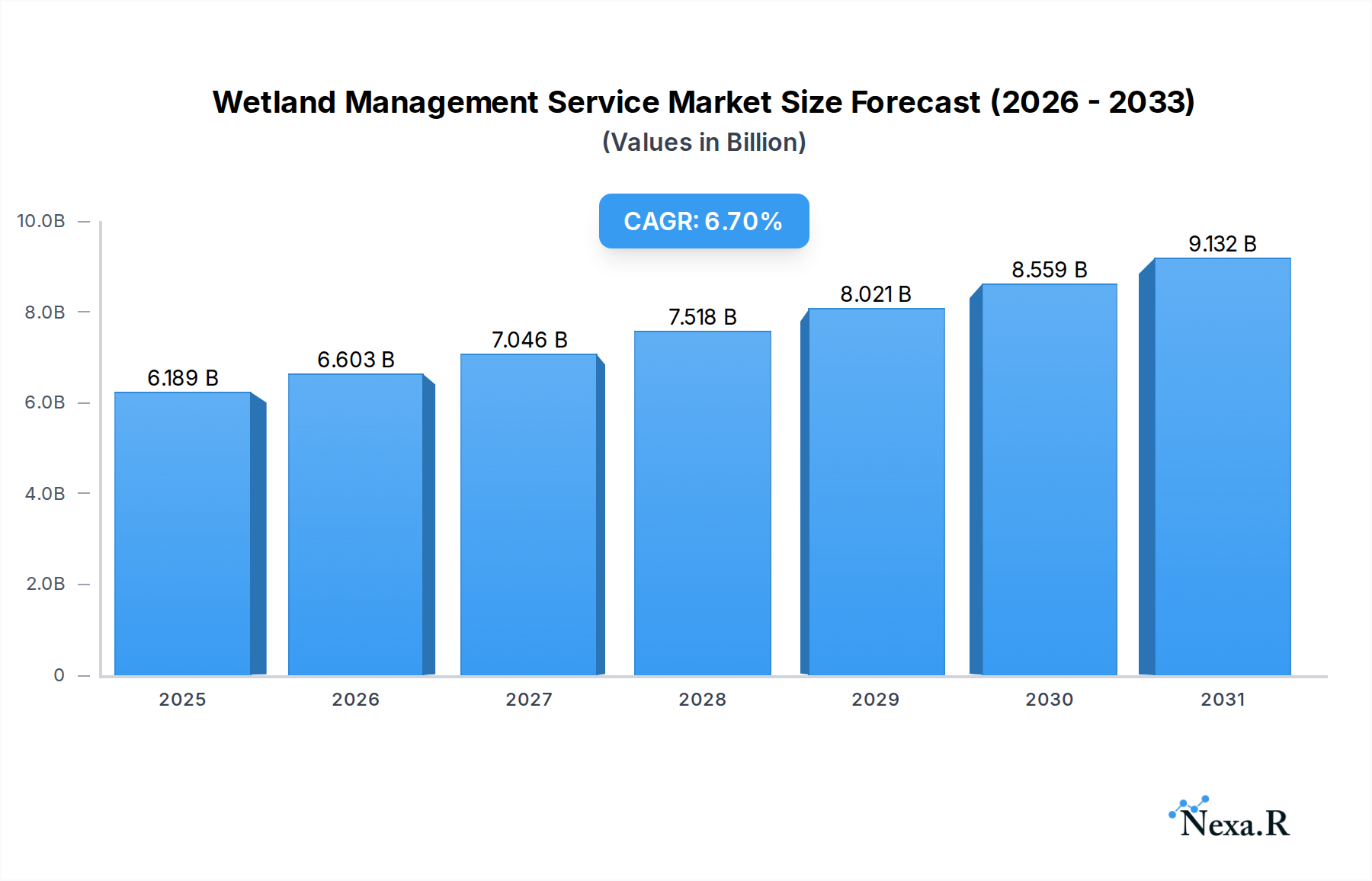

The Wetland Management Service Market, valued at an estimated $5.8 billion in 2024, is poised for substantial expansion, projected to reach approximately $11.11 billion by 2034, exhibiting a robust Compound Annual Growth Rate (CAGR) of 6.7% over the forecast period. This growth trajectory is primarily propelled by a confluence of escalating environmental regulations, increased public and private sector awareness regarding ecological conservation, and the imperative to mitigate the impacts of climate change. Demand for wetland management services is inherently tied to the health of broader ecosystems and human infrastructure, with global emphasis on biodiversity protection and sustainable land use practices serving as foundational macro tailwinds. The increasing frequency and intensity of extreme weather events necessitate resilient natural infrastructure, positioning wetland management as a critical component of climate adaptation strategies. Furthermore, the expansion of the Infrastructure Development Market globally indirectly fuels demand for compensatory wetland mitigation services, as development often impacts existing wetland areas. Regulatory frameworks such as the Ramsar Convention, the Clean Water Act (in the U.S.), and similar national legislations across Europe and Asia Pacific, mandate the protection, restoration, and creation of wetlands, driving consistent service demand. Technological advancements in areas such as the Remote Sensing Technology Market and the Geospatial Technology Market are enhancing the precision and efficiency of wetland assessment, mapping, and monitoring activities, thereby expanding the scope and efficacy of available services. Moreover, the growing focus on corporate social responsibility (CSR) and Environmental, Social, and Governance (ESG) principles within the private sector contributes significantly to the uptake of wetland conservation and restoration projects. The ongoing global dialogue around carbon sequestration and natural climate solutions also underscores the value of intact and functional wetlands, further cementing their importance in environmental policy and investment portfolios. This dynamic interplay of regulatory push, environmental necessity, and technological enabler suggests a sustained bullish outlook for the Wetland Management Service Market.

Wetland Management Service Market Size (In Billion)

Dominant Restoration & Rehabilitation Services in Wetland Management Service Market

Within the multifaceted Wetland Management Service Market, the Restoration & Rehabilitation service type segment stands out as the predominant revenue generator, capturing a significant share of the overall market. This dominance is attributed to several critical factors, primarily the widespread degradation of natural wetlands globally due to anthropogenic activities such as urbanization, agricultural expansion, pollution, and climate change. As these vital ecosystems diminish, the urgent need for their ecological recovery becomes paramount, translating into substantial demand for comprehensive restoration and rehabilitation projects. These services encompass a broad spectrum of activities, including hydrological restoration (re-establishing natural water flow regimes), vegetation re-establishment (planting native species), soil amendment, invasive species control, and the creation of new wetland features to mitigate past damages or compensate for unavoidable impacts. The complex nature and large-scale scope of these projects often necessitate significant capital investment and specialized expertise, thus commanding higher service fees compared to routine monitoring or consulting activities. Key players in this segment, such as SOLitude Lake Management, Applied Aquatic Management, and Environmental Quality Management, leverage integrated approaches that combine scientific research, engineering solutions, and long-term adaptive management strategies. The inherent complexity of ecological restoration, requiring a deep understanding of hydrogeology, soil science, botany, and zoology, limits entry barriers for less specialized firms, allowing established companies to consolidate their market share through proven methodologies and project portfolios. Furthermore, regulatory mandates frequently prioritize 'no net loss' policies for wetlands, compelling developers and governmental entities to invest heavily in compensatory mitigation, where destroyed wetlands are replaced or enhanced elsewhere. This regulatory impetus provides a stable and expanding demand base for restoration projects. The increasing recognition of wetlands as natural infrastructure capable of providing crucial ecosystem services—such as flood control, water purification, and carbon sequestration—further solidifies the importance and funding for restoration efforts. For instance, the demand from the Water Treatment Service Market and the Wastewater Management Market often involves the creation or restoration of constructed wetlands for natural filtration, directly feeding into this segment. The ongoing drive towards creating more resilient landscapes in the face of climate change ensures that the Ecological Restoration Service Market, particularly within the wetland domain, will continue to be a cornerstone of the broader Wetland Management Service Market, with its share likely to expand as environmental degradation pressures intensify globally.

Wetland Management Service Company Market Share

Key Market Drivers in Wetland Management Service Market

The Wetland Management Service Market is significantly driven by a combination of stringent environmental regulations, increasing recognition of ecosystem services, and growing investments in sustainable infrastructure. Each driver is underpinned by quantifiable trends and policy shifts. Firstly, Evolving Regulatory Frameworks are a primary impetus. Governments worldwide are enacting and enforcing stricter laws for wetland protection and mitigation. For instance, the U.S. Clean Water Act's Section 404 permits and similar directives in the European Union (e.g., Water Framework Directive, Habitats Directive) mandate compensatory mitigation for wetland impacts. This means any development affecting wetlands requires a corresponding investment in restoration, creation, or enhancement of other wetland areas. This regulatory environment creates a non-discretionary demand for expert wetland management services. Secondly, the Economic Valuation of Ecosystem Services provided by wetlands is gaining traction. Studies by institutions like the United Nations Environment Programme (UNEP) quantify wetlands' role in flood control, water purification, biodiversity support, and carbon sequestration. This increased valuation compels policymakers and corporations to invest in wetland health as a cost-effective natural solution, rather than relying solely on engineered infrastructure. For example, coastal wetlands are increasingly recognized for their role in storm surge protection, driving investments in their restoration as a cheaper and more sustainable alternative to sea walls. Thirdly, Global Climate Change Mitigation and Adaptation Efforts are profoundly influencing the market. Wetlands are significant carbon sinks, and their restoration is a key strategy for reducing greenhouse gas emissions. The Intergovernmental Panel on Climate Change (IPCC) highlights the role of nature-based solutions, including wetland restoration, in achieving climate targets. Simultaneously, the need for climate adaptation, such as enhancing resilience to floods and droughts, positions healthy wetlands as critical natural infrastructure. This drives projects aimed at restoring hydrological functions and biodiversity, often supported by international climate finance mechanisms. Furthermore, the expansion of the Environmental Monitoring System Market, fueled by technological advancements, directly supports regulatory compliance and impact assessment, thereby expanding the need for specialized wetland services. The integration of the Sustainability Service Market objectives into corporate strategies also encourages voluntary wetland conservation efforts beyond regulatory minimums, contributing to a diversified demand base.

Competitive Ecosystem of Wetland Management Service Market

The Wetland Management Service Market is characterized by a mix of specialized regional firms and larger environmental consultancies, all vying for projects related to conservation, restoration, and compliance. Innovation in ecological science and project management, alongside adherence to complex regulatory frameworks, are key competitive differentiators.

- SOLitude Lake Management: A leading provider of lake, pond, wetland, and fisheries management services, focusing on ecological balance, water quality, and invasive species control across North America. Their comprehensive approach integrates scientific expertise with practical implementation for diverse client needs.

- Specialist Lake Services: Offers a range of aquatic management solutions, including wetland creation, erosion control, and water body maintenance, often serving residential, commercial, and golf course clients with tailored ecological solutions.

- PREMIER LAKES: Specializes in sustainable aquatic ecosystem management, providing services from design and construction of wetlands to ongoing maintenance and water quality improvements for various land management contexts.

- Applied Aquatic Management: Delivers integrated solutions for water resource management, including wetland construction, invasive plant management, and habitat enhancement, often working with governmental and private sector clients on large-scale projects.

- Lake Management: Focuses on enhancing and maintaining the health of aquatic environments, offering services such as aeration, vegetation management, and water quality testing, which are often integral to surrounding wetland ecosystems.

- Aquagenix: Provides comprehensive aquatic management services, including wetland restoration, stormwater pond maintenance, and regulatory compliance, with an emphasis on sustainable and environmentally sound practices.

- EnvMart: Operates as an environmental solutions provider, potentially offering wetland management services as part of a broader portfolio that may include environmental consulting and remediation efforts.

- Maryland Environmental Service: A state agency providing environmental solutions to state and local governments, including wetland creation, stream restoration, and solid waste management, playing a critical role in public sector environmental projects.

- Ecolibrium: An environmental consulting firm likely providing advisory services for wetland delineation, permitting, mitigation planning, and ecological assessments, crucial for regulatory navigation within the Wetland Management Service Market.

- Meryman Environmental: Offers specialized environmental consulting services, including wetland permitting, impact assessments, and mitigation design, supporting clients through complex environmental compliance processes.

- Moore Engineering: Provides civil and environmental engineering services, often including wetland delineations, mitigation plans, and design of stormwater treatment wetlands, integrating ecological considerations into infrastructure projects.

- Kramer J. Services: Aims to provide diverse environmental services, potentially including aspects of wetland maintenance or restoration, often catering to local and regional clients with specific land management requirements.

- Balance Enviro: Specializes in ecological consulting and restoration, focusing on wetland and stream restoration, ecological surveys, and environmental permitting, emphasizing sustainable and science-based solutions.

- Environmental Quality Management: A prominent environmental consulting and engineering firm offering a wide array of services, including wetland delineation, permitting, remediation, and ecological risk assessments, serving industrial, governmental, and commercial clients.

Recent Developments & Milestones in Wetland Management Service Market

Recent years have seen a dynamic acceleration in both regulatory action and technological adoption within the Wetland Management Service Market, reflecting a global pivot towards stronger environmental stewardship and climate resilience.

- May 2024: Several European nations, including France and Germany, finalized new national implementation strategies for the EU Biodiversity Strategy for 2030, with a strong focus on restoring degraded ecosystems, including wetlands, aiming for significant progress by 2025. This legislative push is anticipated to drive substantial project funding in the coming years.

- February 2024: A major conservation initiative launched in North America, backed by federal and philanthropic funding, targeting the restoration of over 500,000 acres of critical wetland habitat across the Mississippi Flyway. This multi-year program represents a significant boon for large-scale Ecological Restoration Service Market providers.

- November 2023: Advancements in Remote Sensing Technology Market applications, specifically in drone-based LiDAR and hyperspectral imaging, enabled more precise and cost-effective wetland mapping and monitoring. This technological integration allows service providers to offer enhanced assessment, mapping, and monitoring services, improving project efficiency and accuracy.

- September 2023: Several leading Environmental Consulting Service Market firms announced strategic partnerships with data analytics companies to integrate predictive modeling and artificial intelligence into wetland management planning. This move aims to optimize restoration outcomes and predict future hydrological changes more effectively.

- July 2023: The United Nations Environment Programme (UNEP) highlighted the role of wetlands in achieving Sustainable Development Goals (SDGs), particularly those related to water, climate action, and biodiversity. This global advocacy effort is expected to galvanize further governmental and NGO investments in the Wetland Management Service Market.

- April 2023: New guidelines for carbon credit generation from wetland restoration projects were introduced by various international standards bodies, providing financial incentives for private sector engagement in large-scale wetland conservation and rehabilitation efforts, thereby attracting new investment avenues into the Sustainability Service Market.

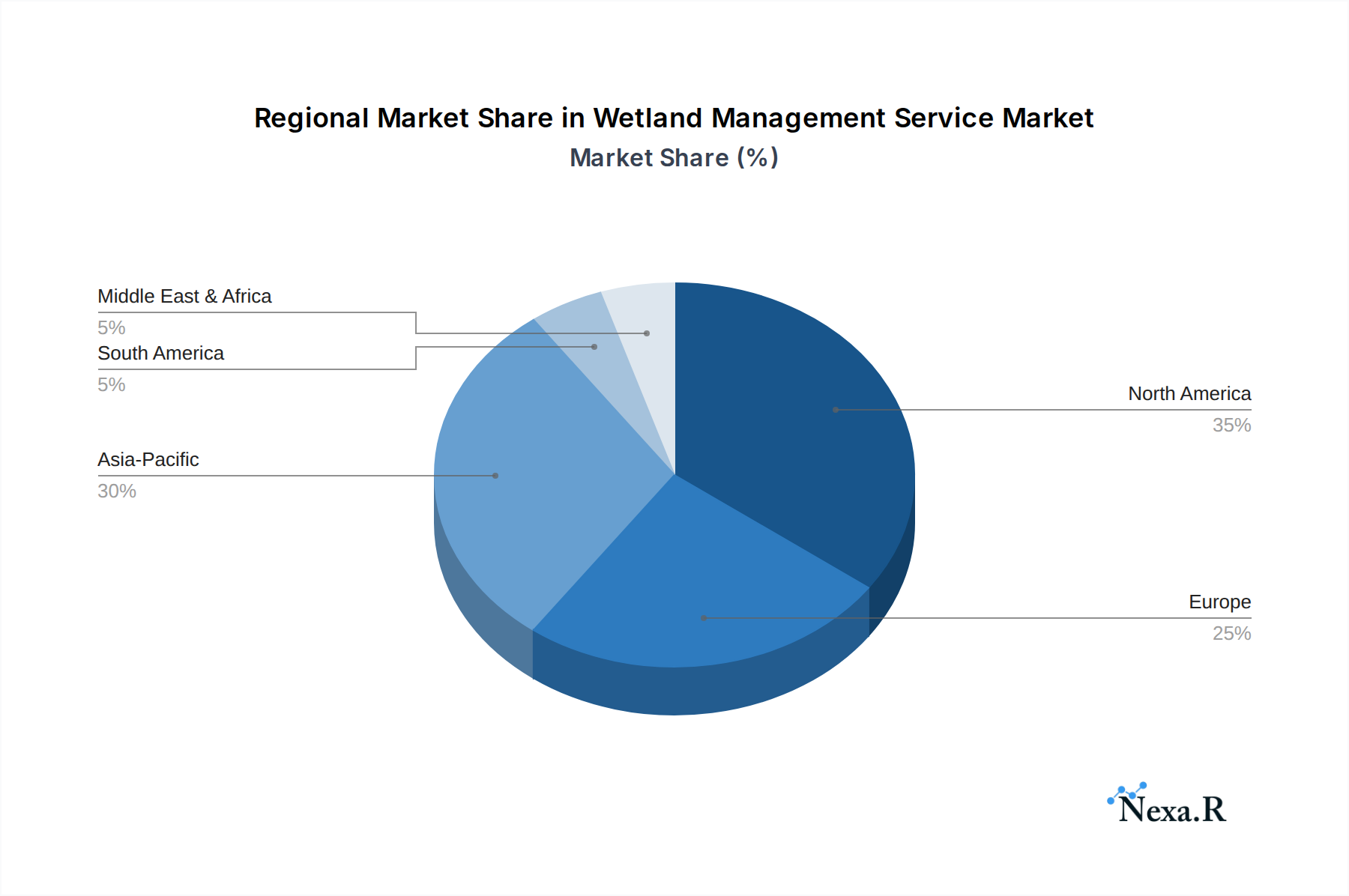

Regional Market Breakdown for Wetland Management Service Market

The Wetland Management Service Market demonstrates varied dynamics across key global regions, driven by distinct regulatory landscapes, environmental priorities, and economic development stages. Overall, the market is characterized by mature demand in developed economies and rapidly emerging opportunities in developing regions.

North America holds the largest revenue share in the Wetland Management Service Market, primarily due to well-established and stringent environmental regulations, such as the Clean Water Act in the United States and similar federal and provincial legislation in Canada. These regulatory frameworks necessitate extensive wetland delineation, permitting, mitigation, and monitoring activities, creating a stable and high-value demand for services. The region also sees significant investment from the Infrastructure Development Market, which frequently requires compensatory wetland mitigation. Demand is further buoyed by a strong focus on biodiversity conservation and climate resilience initiatives. The United States, in particular, leads in adopting advanced solutions from the Geospatial Technology Market and the Environmental Monitoring System Market for wetland assessment.

Europe represents another significant market, driven by the European Union's comprehensive environmental policies, including the Water Framework Directive and the Habitats Directive, which prioritize the protection and restoration of aquatic ecosystems. Countries like Germany, France, and the UK are actively investing in wetland restoration projects to improve water quality, enhance biodiversity, and mitigate flood risks. The region's mature environmental consciousness and robust scientific research base support the continuous demand for high-quality Environmental Consulting Service Market offerings in wetland management. While growth rates are steady, the emphasis is often on maintaining existing wetland health and rehabilitating degraded sites within densely populated areas.

Asia Pacific is projected to be the fastest-growing region in the Wetland Management Service Market. This rapid expansion is fueled by accelerated industrialization, urbanization, and a growing awareness of environmental degradation. Countries like China, India, and Australia are increasingly recognizing the ecological and economic value of wetlands. While regulatory enforcement historically lagged, there is a clear trend towards strengthening environmental protection laws and investing in large-scale ecological restoration projects. The significant expansion of the Water Treatment Service Market and the Wastewater Management Market in this region often involves the construction and management of artificial wetlands for treatment purposes. Major infrastructure projects and increasing climate change impacts also drive substantial demand for mitigation and adaptation services, with a nascent but growing Remote Sensing Technology Market being applied for monitoring.

Middle East & Africa is an emerging market, driven by increasing concerns over water scarcity, desertification, and the need for sustainable resource management. Investments are primarily concentrated in GCC countries due to large-scale development projects and increasing adoption of environmental standards. South Africa also shows significant activity in wetland conservation. Demand is often linked to major industrial and resource extraction projects requiring environmental impact assessments and mitigation, including wetland services.

South America presents a developing market, with Brazil and Argentina leading in wetland management activities. The Amazon basin's ecological significance drives a global and local focus on conservation, although enforcement can be challenging. Demand is often associated with agricultural expansion, mining, and hydropower projects, necessitating impact assessments and mitigation efforts. There is a growing emphasis on adopting sustainable practices, potentially increasing the uptake of services from the Ecological Restoration Service Market.

Wetland Management Service Regional Market Share

Export, Trade Flow & Tariff Impact on Wetland Management Service Market

The Wetland Management Service Market, being inherently location-specific due to the physical nature of wetlands, does not experience traditional cross-border goods trade. However, there is a significant trade in specialized expertise, technology, and strategic consulting across national borders. Major trade corridors for these services involve highly skilled professionals, often from North American and European firms, exporting their knowledge and methodologies to emerging markets in Asia Pacific, the Middle East, and South America. This 'export of services' is driven by the demand for advanced ecological engineering, geospatial analysis, and regulatory compliance expertise that may not be readily available locally. For instance, consultants from the Geospatial Technology Market and the Remote Sensing Technology Market are often contracted internationally for complex mapping and monitoring projects. There are typically no direct tariffs on these services, but non-tariff barriers, such as visa requirements for skilled labor, professional licensing, and local content requirements in government contracts, can impact the ease of cross-border service provision. Harmonization of environmental standards and international agreements (like the Ramsar Convention) facilitate this trade by creating a common framework for wetland protection, fostering the adoption of best practices. Recent trade policies focused on environmental goods and services, such as those discussed under the World Trade Organization (WTO), could potentially streamline the export of related technologies (e.g., specialized monitoring equipment from the Environmental Monitoring System Market), indirectly benefiting the service market by making tools more accessible. However, geopolitical tensions or protectionist policies could lead to increased scrutiny on foreign firms participating in national environmental projects, potentially increasing operational costs or favoring domestic providers.

Customer Segmentation & Buying Behavior in Wetland Management Service Market

Customer segmentation in the Wetland Management Service Market reveals distinct purchasing criteria and procurement channels across various end-user groups. The primary end-users include Government & Public Agencies, Mining, Energy, & Infrastructure companies, Agriculture & Forestry entities, Water & Wastewater Treatment Utilities, and NGOs & Trusts.

Government & Public Agencies (e.g., federal environmental protection agencies, state departments of natural resources, municipal stormwater authorities) represent the largest customer segment. Their buying behavior is primarily driven by regulatory compliance, public mandate for environmental protection, and infrastructure development needs. Procurement often occurs through public tenders, long-term contracts, and competitive bidding processes, emphasizing proven expertise, cost-effectiveness over multi-year projects, and adherence to strict environmental standards. Price sensitivity exists but is often balanced against demonstrable ecological outcomes and long-term value. These agencies are significant purchasers within the Environmental Consulting Service Market as well as for direct management services.

Mining, Energy, & Infrastructure companies form another substantial segment. Their demand is largely driven by permit requirements for new projects or expansions, compensatory mitigation obligations, and corporate sustainability goals. These clients seek providers with a strong track record in navigating complex regulatory environments, efficient project execution to minimize delays, and robust environmental impact assessment capabilities. Procurement is typically through RFPs issued directly by project developers, often prioritizing firms that can offer integrated solutions from planning through restoration. The Infrastructure Development Market directly feeds into this segment's demand for wetland services.

Agriculture & Forestry entities, while smaller individually, collectively contribute to demand, particularly for services related to stormwater management, soil erosion control, and habitat enhancement for sustainable farming practices. Their buying behavior is highly price-sensitive, often seeking cost-effective, practical solutions that integrate with existing land-use practices. Procurement is typically direct or through agricultural cooperatives, sometimes influenced by government incentive programs for conservation.

Water & Wastewater Treatment Utilities are key clients, especially for constructed wetlands used in natural water filtration and treatment processes. Their purchasing criteria focus on the efficacy of treatment, compliance with discharge limits, and the long-term operational costs of wetland systems. These utilities heavily leverage the Water Treatment Service Market and the Wastewater Management Market and look for service providers that can design, construct, and maintain these specialized wetlands to achieve specific water quality objectives. Procurement involves specialized engineering and environmental firms through competitive bidding.

NGOs & Trusts prioritize ecological outcomes, biodiversity enhancement, and community engagement. Their funding often comes from grants and donations, leading to a focus on maximizing ecological benefits within budget constraints. They tend to partner with firms that demonstrate strong scientific integrity, a commitment to conservation, and transparent reporting. The Sustainability Service Market is often where these groups find alignment.

Notable shifts in buyer preference include an increasing demand for integrated solutions that combine monitoring, data analytics (leveraging the Geospatial Technology Market), and adaptive management strategies. There's also a growing emphasis on services that can quantify environmental benefits (e.g., carbon credits, biodiversity uplift) to support ESG reporting and attract green financing. Clients are increasingly seeking long-term partners capable of delivering both initial restoration and ongoing management and monitoring.

Wetland Management Service Segmentation

-

1. Service Type

- 1.1. Restoration & Rehabilitation

- 1.2. Conservation

- 1.3. Assessment, Mapping, & Monitoring

- 1.4. Consulting and Planning

- 1.5. Others

-

2. Wetland Type

- 2.1. Natural Wetlands

- 2.2. Constructed/Artificial Wetlands

-

3. Application

- 3.1. Commercial

- 3.2. Municipal

-

4. End User

- 4.1. Government & Public Agencies

- 4.2. Mining, Energy, & Infrastructure

- 4.3. Agriculture & Forestry

- 4.4. Water & Wastewater Treatment Utilities

- 4.5. NGOs & Trusts

- 4.6. Others

Wetland Management Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Wetland Management Service Regional Market Share

Geographic Coverage of Wetland Management Service

Wetland Management Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 5.1.1. Restoration & Rehabilitation

- 5.1.2. Conservation

- 5.1.3. Assessment, Mapping, & Monitoring

- 5.1.4. Consulting and Planning

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Wetland Type

- 5.2.1. Natural Wetlands

- 5.2.2. Constructed/Artificial Wetlands

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Commercial

- 5.3.2. Municipal

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Government & Public Agencies

- 5.4.2. Mining, Energy, & Infrastructure

- 5.4.3. Agriculture & Forestry

- 5.4.4. Water & Wastewater Treatment Utilities

- 5.4.5. NGOs & Trusts

- 5.4.6. Others

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. South America

- 5.5.3. Europe

- 5.5.4. Middle East & Africa

- 5.5.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 6. Global Wetland Management Service Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 6.1.1. Restoration & Rehabilitation

- 6.1.2. Conservation

- 6.1.3. Assessment, Mapping, & Monitoring

- 6.1.4. Consulting and Planning

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Wetland Type

- 6.2.1. Natural Wetlands

- 6.2.2. Constructed/Artificial Wetlands

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Commercial

- 6.3.2. Municipal

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Government & Public Agencies

- 6.4.2. Mining, Energy, & Infrastructure

- 6.4.3. Agriculture & Forestry

- 6.4.4. Water & Wastewater Treatment Utilities

- 6.4.5. NGOs & Trusts

- 6.4.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 7. North America Wetland Management Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 7.1.1. Restoration & Rehabilitation

- 7.1.2. Conservation

- 7.1.3. Assessment, Mapping, & Monitoring

- 7.1.4. Consulting and Planning

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Wetland Type

- 7.2.1. Natural Wetlands

- 7.2.2. Constructed/Artificial Wetlands

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Commercial

- 7.3.2. Municipal

- 7.4. Market Analysis, Insights and Forecast - by End User

- 7.4.1. Government & Public Agencies

- 7.4.2. Mining, Energy, & Infrastructure

- 7.4.3. Agriculture & Forestry

- 7.4.4. Water & Wastewater Treatment Utilities

- 7.4.5. NGOs & Trusts

- 7.4.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 8. South America Wetland Management Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 8.1.1. Restoration & Rehabilitation

- 8.1.2. Conservation

- 8.1.3. Assessment, Mapping, & Monitoring

- 8.1.4. Consulting and Planning

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Wetland Type

- 8.2.1. Natural Wetlands

- 8.2.2. Constructed/Artificial Wetlands

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Commercial

- 8.3.2. Municipal

- 8.4. Market Analysis, Insights and Forecast - by End User

- 8.4.1. Government & Public Agencies

- 8.4.2. Mining, Energy, & Infrastructure

- 8.4.3. Agriculture & Forestry

- 8.4.4. Water & Wastewater Treatment Utilities

- 8.4.5. NGOs & Trusts

- 8.4.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 9. Europe Wetland Management Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Service Type

- 9.1.1. Restoration & Rehabilitation

- 9.1.2. Conservation

- 9.1.3. Assessment, Mapping, & Monitoring

- 9.1.4. Consulting and Planning

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Wetland Type

- 9.2.1. Natural Wetlands

- 9.2.2. Constructed/Artificial Wetlands

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Commercial

- 9.3.2. Municipal

- 9.4. Market Analysis, Insights and Forecast - by End User

- 9.4.1. Government & Public Agencies

- 9.4.2. Mining, Energy, & Infrastructure

- 9.4.3. Agriculture & Forestry

- 9.4.4. Water & Wastewater Treatment Utilities

- 9.4.5. NGOs & Trusts

- 9.4.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Service Type

- 10. Middle East & Africa Wetland Management Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Service Type

- 10.1.1. Restoration & Rehabilitation

- 10.1.2. Conservation

- 10.1.3. Assessment, Mapping, & Monitoring

- 10.1.4. Consulting and Planning

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Wetland Type

- 10.2.1. Natural Wetlands

- 10.2.2. Constructed/Artificial Wetlands

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Commercial

- 10.3.2. Municipal

- 10.4. Market Analysis, Insights and Forecast - by End User

- 10.4.1. Government & Public Agencies

- 10.4.2. Mining, Energy, & Infrastructure

- 10.4.3. Agriculture & Forestry

- 10.4.4. Water & Wastewater Treatment Utilities

- 10.4.5. NGOs & Trusts

- 10.4.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Service Type

- 11. Asia Pacific Wetland Management Service Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Service Type

- 11.1.1. Restoration & Rehabilitation

- 11.1.2. Conservation

- 11.1.3. Assessment, Mapping, & Monitoring

- 11.1.4. Consulting and Planning

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Wetland Type

- 11.2.1. Natural Wetlands

- 11.2.2. Constructed/Artificial Wetlands

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Commercial

- 11.3.2. Municipal

- 11.4. Market Analysis, Insights and Forecast - by End User

- 11.4.1. Government & Public Agencies

- 11.4.2. Mining, Energy, & Infrastructure

- 11.4.3. Agriculture & Forestry

- 11.4.4. Water & Wastewater Treatment Utilities

- 11.4.5. NGOs & Trusts

- 11.4.6. Others

- 11.1. Market Analysis, Insights and Forecast - by Service Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 SOLitude Lake Management

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Specialist Lake Services

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 PREMIER LAKES

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Applied Aquatic Management

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Lake Management

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Aquagenix

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 EnvMart

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Maryland Environmental Service

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Ecolibrium

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Meryman Environmental

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Moore Engineering

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Kramer J. Services

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Balance Enviro

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Environmental Quality Management

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 SOLitude Lake Management

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Wetland Management Service Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Wetland Management Service Revenue (billion), by Service Type 2025 & 2033

- Figure 3: North America Wetland Management Service Revenue Share (%), by Service Type 2025 & 2033

- Figure 4: North America Wetland Management Service Revenue (billion), by Wetland Type 2025 & 2033

- Figure 5: North America Wetland Management Service Revenue Share (%), by Wetland Type 2025 & 2033

- Figure 6: North America Wetland Management Service Revenue (billion), by Application 2025 & 2033

- Figure 7: North America Wetland Management Service Revenue Share (%), by Application 2025 & 2033

- Figure 8: North America Wetland Management Service Revenue (billion), by End User 2025 & 2033

- Figure 9: North America Wetland Management Service Revenue Share (%), by End User 2025 & 2033

- Figure 10: North America Wetland Management Service Revenue (billion), by Country 2025 & 2033

- Figure 11: North America Wetland Management Service Revenue Share (%), by Country 2025 & 2033

- Figure 12: South America Wetland Management Service Revenue (billion), by Service Type 2025 & 2033

- Figure 13: South America Wetland Management Service Revenue Share (%), by Service Type 2025 & 2033

- Figure 14: South America Wetland Management Service Revenue (billion), by Wetland Type 2025 & 2033

- Figure 15: South America Wetland Management Service Revenue Share (%), by Wetland Type 2025 & 2033

- Figure 16: South America Wetland Management Service Revenue (billion), by Application 2025 & 2033

- Figure 17: South America Wetland Management Service Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Wetland Management Service Revenue (billion), by End User 2025 & 2033

- Figure 19: South America Wetland Management Service Revenue Share (%), by End User 2025 & 2033

- Figure 20: South America Wetland Management Service Revenue (billion), by Country 2025 & 2033

- Figure 21: South America Wetland Management Service Revenue Share (%), by Country 2025 & 2033

- Figure 22: Europe Wetland Management Service Revenue (billion), by Service Type 2025 & 2033

- Figure 23: Europe Wetland Management Service Revenue Share (%), by Service Type 2025 & 2033

- Figure 24: Europe Wetland Management Service Revenue (billion), by Wetland Type 2025 & 2033

- Figure 25: Europe Wetland Management Service Revenue Share (%), by Wetland Type 2025 & 2033

- Figure 26: Europe Wetland Management Service Revenue (billion), by Application 2025 & 2033

- Figure 27: Europe Wetland Management Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Europe Wetland Management Service Revenue (billion), by End User 2025 & 2033

- Figure 29: Europe Wetland Management Service Revenue Share (%), by End User 2025 & 2033

- Figure 30: Europe Wetland Management Service Revenue (billion), by Country 2025 & 2033

- Figure 31: Europe Wetland Management Service Revenue Share (%), by Country 2025 & 2033

- Figure 32: Middle East & Africa Wetland Management Service Revenue (billion), by Service Type 2025 & 2033

- Figure 33: Middle East & Africa Wetland Management Service Revenue Share (%), by Service Type 2025 & 2033

- Figure 34: Middle East & Africa Wetland Management Service Revenue (billion), by Wetland Type 2025 & 2033

- Figure 35: Middle East & Africa Wetland Management Service Revenue Share (%), by Wetland Type 2025 & 2033

- Figure 36: Middle East & Africa Wetland Management Service Revenue (billion), by Application 2025 & 2033

- Figure 37: Middle East & Africa Wetland Management Service Revenue Share (%), by Application 2025 & 2033

- Figure 38: Middle East & Africa Wetland Management Service Revenue (billion), by End User 2025 & 2033

- Figure 39: Middle East & Africa Wetland Management Service Revenue Share (%), by End User 2025 & 2033

- Figure 40: Middle East & Africa Wetland Management Service Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East & Africa Wetland Management Service Revenue Share (%), by Country 2025 & 2033

- Figure 42: Asia Pacific Wetland Management Service Revenue (billion), by Service Type 2025 & 2033

- Figure 43: Asia Pacific Wetland Management Service Revenue Share (%), by Service Type 2025 & 2033

- Figure 44: Asia Pacific Wetland Management Service Revenue (billion), by Wetland Type 2025 & 2033

- Figure 45: Asia Pacific Wetland Management Service Revenue Share (%), by Wetland Type 2025 & 2033

- Figure 46: Asia Pacific Wetland Management Service Revenue (billion), by Application 2025 & 2033

- Figure 47: Asia Pacific Wetland Management Service Revenue Share (%), by Application 2025 & 2033

- Figure 48: Asia Pacific Wetland Management Service Revenue (billion), by End User 2025 & 2033

- Figure 49: Asia Pacific Wetland Management Service Revenue Share (%), by End User 2025 & 2033

- Figure 50: Asia Pacific Wetland Management Service Revenue (billion), by Country 2025 & 2033

- Figure 51: Asia Pacific Wetland Management Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Wetland Management Service Revenue billion Forecast, by Service Type 2020 & 2033

- Table 2: Global Wetland Management Service Revenue billion Forecast, by Wetland Type 2020 & 2033

- Table 3: Global Wetland Management Service Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Global Wetland Management Service Revenue billion Forecast, by End User 2020 & 2033

- Table 5: Global Wetland Management Service Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Wetland Management Service Revenue billion Forecast, by Service Type 2020 & 2033

- Table 7: Global Wetland Management Service Revenue billion Forecast, by Wetland Type 2020 & 2033

- Table 8: Global Wetland Management Service Revenue billion Forecast, by Application 2020 & 2033

- Table 9: Global Wetland Management Service Revenue billion Forecast, by End User 2020 & 2033

- Table 10: Global Wetland Management Service Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Global Wetland Management Service Revenue billion Forecast, by Service Type 2020 & 2033

- Table 15: Global Wetland Management Service Revenue billion Forecast, by Wetland Type 2020 & 2033

- Table 16: Global Wetland Management Service Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Wetland Management Service Revenue billion Forecast, by End User 2020 & 2033

- Table 18: Global Wetland Management Service Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Brazil Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Argentina Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Rest of South America Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global Wetland Management Service Revenue billion Forecast, by Service Type 2020 & 2033

- Table 23: Global Wetland Management Service Revenue billion Forecast, by Wetland Type 2020 & 2033

- Table 24: Global Wetland Management Service Revenue billion Forecast, by Application 2020 & 2033

- Table 25: Global Wetland Management Service Revenue billion Forecast, by End User 2020 & 2033

- Table 26: Global Wetland Management Service Revenue billion Forecast, by Country 2020 & 2033

- Table 27: United Kingdom Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Germany Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: France Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Italy Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Spain Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Russia Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Benelux Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Nordics Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Global Wetland Management Service Revenue billion Forecast, by Service Type 2020 & 2033

- Table 37: Global Wetland Management Service Revenue billion Forecast, by Wetland Type 2020 & 2033

- Table 38: Global Wetland Management Service Revenue billion Forecast, by Application 2020 & 2033

- Table 39: Global Wetland Management Service Revenue billion Forecast, by End User 2020 & 2033

- Table 40: Global Wetland Management Service Revenue billion Forecast, by Country 2020 & 2033

- Table 41: Turkey Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Israel Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: GCC Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: North Africa Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: South Africa Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Middle East & Africa Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: Global Wetland Management Service Revenue billion Forecast, by Service Type 2020 & 2033

- Table 48: Global Wetland Management Service Revenue billion Forecast, by Wetland Type 2020 & 2033

- Table 49: Global Wetland Management Service Revenue billion Forecast, by Application 2020 & 2033

- Table 50: Global Wetland Management Service Revenue billion Forecast, by End User 2020 & 2033

- Table 51: Global Wetland Management Service Revenue billion Forecast, by Country 2020 & 2033

- Table 52: China Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 53: India Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Japan Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 55: South Korea Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: ASEAN Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 57: Oceania Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Rest of Asia Pacific Wetland Management Service Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Wetland Management Service?

The projected CAGR is approximately 6.7%.

2. Which companies are prominent players in the Wetland Management Service?

Key companies in the market include SOLitude Lake Management, Specialist Lake Services, PREMIER LAKES, Applied Aquatic Management, Lake Management, Aquagenix, EnvMart, Maryland Environmental Service, Ecolibrium, Meryman Environmental, Moore Engineering, Kramer J. Services, Balance Enviro, Environmental Quality Management.

3. What are the main segments of the Wetland Management Service?

The market segments include Service Type, Wetland Type, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.8 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Wetland Management Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Wetland Management Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Wetland Management Service?

To stay informed about further developments, trends, and reports in the Wetland Management Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence