Key Insights

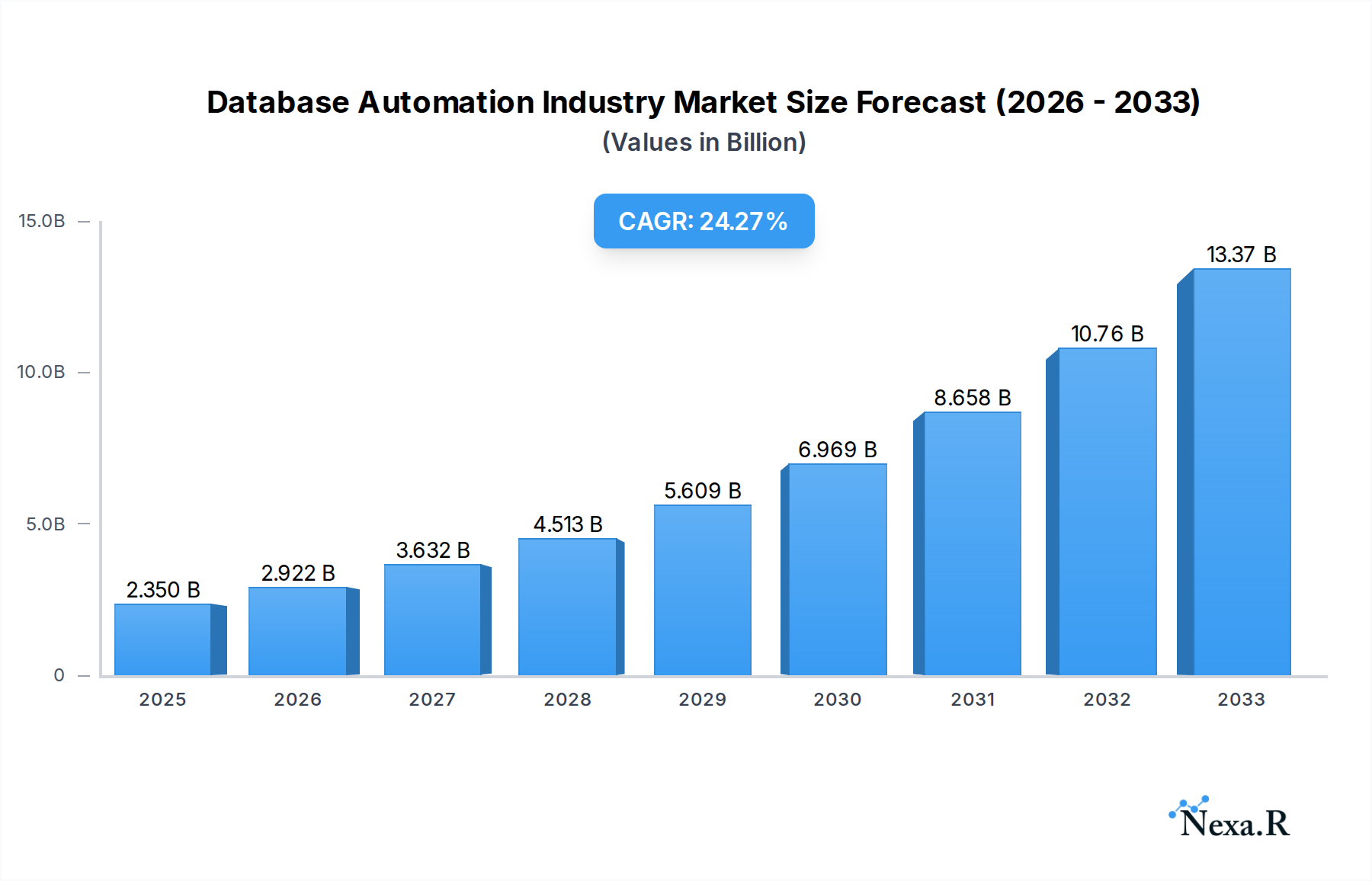

The global Database Automation Industry is experiencing remarkable expansion, projected to reach a market size of 2.35 Billion in 2025, with an anticipated CAGR of 24.38% through 2033. This robust growth is fueled by a confluence of critical drivers, including the escalating complexity of modern data landscapes, the imperative for enhanced operational efficiency, and the increasing adoption of DevOps practices across enterprises. The digital transformation initiatives sweeping across industries necessitate sophisticated solutions for managing, patching, releasing, and testing databases, making automation a non-negotiable aspect of IT infrastructure. Furthermore, the rising demand for cloud-native database solutions and the growing prevalence of data-intensive applications are significantly contributing to this upward trajectory. Organizations are increasingly recognizing that manual database management is prone to errors, time-consuming, and costly, pushing them towards automated solutions that ensure agility, consistency, and scalability.

Database Automation Industry Market Size (In Billion)

The market is segmented across various crucial areas, reflecting the diverse needs of businesses. In terms of components, the industry encompasses Solution offerings such as Database Patch and Release Automation, Application Release Automation, and Database Test Automation, alongside essential Services. Deployment modes are split between Cloud and On-Premises, with cloud solutions gaining significant traction due to their flexibility and scalability. Large Enterprises and Small and Medium-Sized Enterprises (SMEs) both represent key customer segments, indicating broad market penetration. The end-user industry landscape is dominated by sectors such as Banking, Financial Services and Insurance (BFSI), IT and Telecom, E-commerce and Retail, and Manufacturing, all of which are heavily reliant on efficient and secure database operations. Key players like IDERA Inc, IBM Corporation, Quest Software Inc, Datavail, BMC Software Inc, Bryter US Inc, Amazon Web Services Inc, CA Technologies (Broadcom Inc), Oracle Corporation, and SAP SE are actively shaping this dynamic market through continuous innovation and strategic offerings.

Database Automation Industry Company Market Share

This comprehensive report delves into the dynamic Database Automation Industry, analyzing its current market landscape, future growth trajectories, and the strategic forces shaping its evolution. With a forecast period extending to 2033, this study provides invaluable insights for industry stakeholders, IT professionals, and business leaders seeking to understand and leverage the power of automated database management. The report integrates high-traffic keywords such as "database automation," "cloud database automation," "on-premises database automation," "IT automation," "dataops," "DevOps for databases," and "database management software" to maximize search engine visibility.

Database Automation Industry Market Dynamics & Structure

The Database Automation Industry is characterized by a moderate to high market concentration, with key players continuously investing in technological innovation to drive adoption. Factors such as the increasing volume and complexity of data, coupled with the escalating demand for faster and more reliable database operations, are significant technological innovation drivers. Regulatory frameworks, particularly those concerning data privacy and security, also influence the development and deployment of automation solutions. Competitive product substitutes include manual database management processes, although the efficiency gains offered by automation are rapidly diminishing their viability. End-user demographics are expanding beyond traditional IT departments to include business analysts and data scientists, highlighting a broader democratization of data management. Mergers and acquisitions (M&A) are an ongoing trend, with companies acquiring specialized technologies and talent to enhance their offerings. For instance, recent years have seen a rise in M&A activity aimed at consolidating DataOps capabilities.

- Market Concentration: Dominated by a few large players, but with growing influence from specialized vendors.

- Technological Innovation Drivers: Big data, AI/ML integration, cloud adoption, and the need for faster release cycles.

- Regulatory Frameworks: GDPR, CCPA, and industry-specific compliance requirements are pushing for robust automation.

- Competitive Product Substitutes: Evolving from manual processes to integrated automation platforms.

- End-User Demographics: Expansion from IT to business units and data professionals.

- M&A Trends: Strategic acquisitions to gain market share and technological expertise.

Database Automation Industry Growth Trends & Insights

The Database Automation Industry is poised for substantial growth, driven by the relentless pursuit of operational efficiency and cost reduction across enterprises. Market size is projected to expand significantly, with adoption rates escalating as organizations recognize the indispensable role of automation in modern data management. Technological disruptions, including the proliferation of cloud-native databases and the integration of artificial intelligence and machine learning into automation workflows, are fundamentally reshaping the landscape. Consumer behavior shifts are marked by an increasing demand for self-service data management capabilities and real-time data quality assurance. The adoption of DevOps and DataOps methodologies further fuels this growth, as organizations seek to streamline the entire data lifecycle from development to deployment and ongoing management. The historical period (2019–2024) has witnessed steady growth, with the base year (2025) marking a pivotal point for accelerated expansion during the forecast period (2025–2033).

- Market Size Evolution: Significant upward trajectory driven by digital transformation initiatives.

- Adoption Rates: Rapidly increasing across all enterprise sizes and end-user industries.

- Technological Disruptions: AI/ML integration, serverless databases, and advanced analytics are key disruptors.

- Consumer Behavior Shifts: Demand for self-service, real-time insights, and improved data governance.

- CAGR (Compound Annual Growth Rate): XX% projected for the forecast period.

- Market Penetration: Expected to reach XX% of target organizations by 2033.

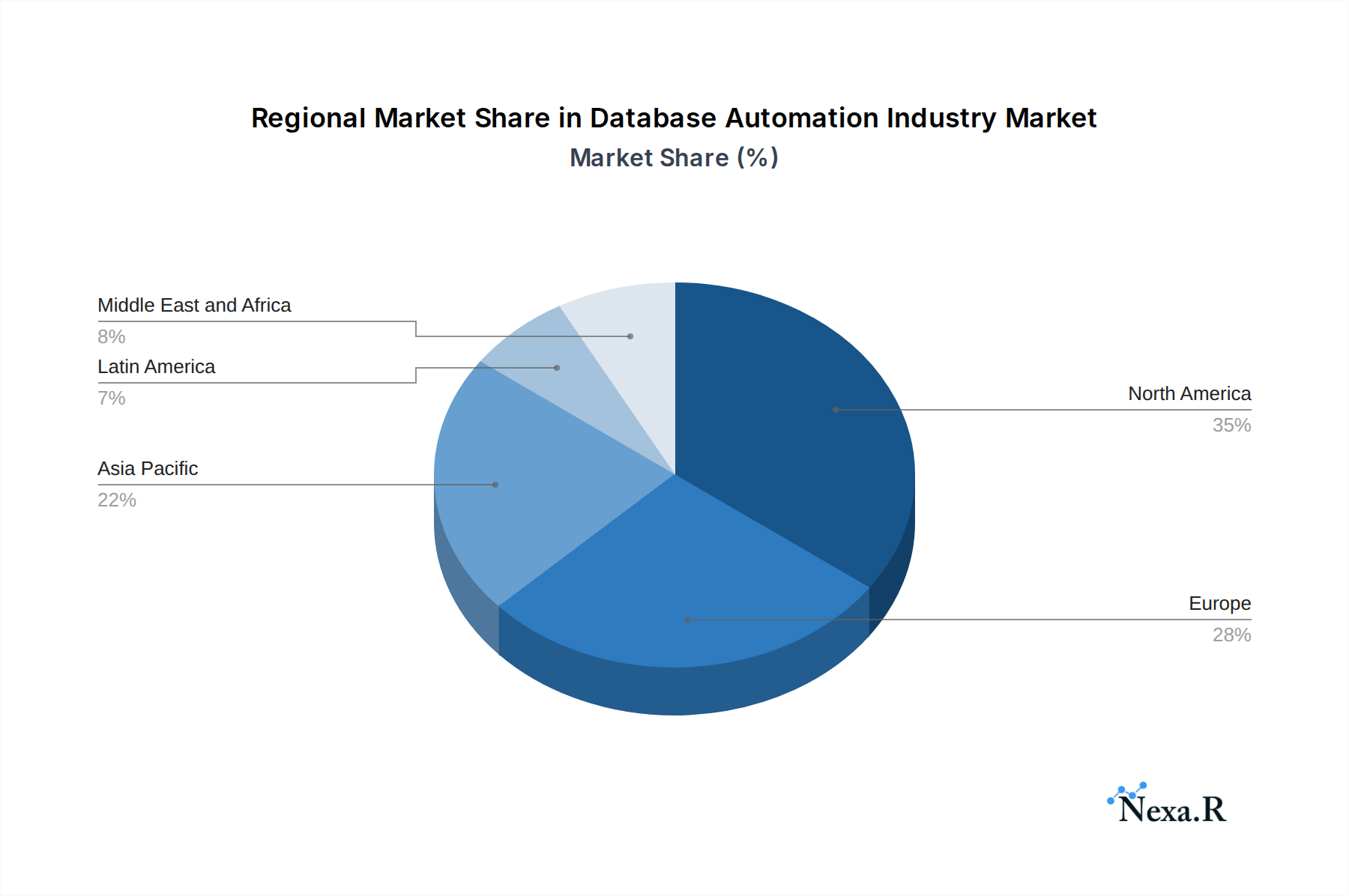

Dominant Regions, Countries, or Segments in Database Automation Industry

The Cloud Deployment Mode is emerging as a dominant segment within the Database Automation Industry, largely driven by the scalability, flexibility, and cost-effectiveness it offers. North America, particularly the United States, leads in market share due to its advanced technological infrastructure, strong presence of major IT companies, and early adoption of cloud computing and automation technologies. The IT and Telecom end-user industry is a primary growth engine, owing to the immense data volumes and complex database requirements inherent in these sectors. Within the Component segment, Database Patch and Release Automation holds a significant share, addressing critical needs for secure and efficient software updates. Large Enterprises are the largest consumers, but Small and Medium-Sized Enterprises (SMEs) are increasingly adopting automation solutions as cloud-based offerings become more accessible and affordable.

- Dominant Deployment Mode: Cloud, offering agility and scalability.

- Market share for Cloud Deployment: XX% (2025).

- Growth drivers: Reduced infrastructure costs, faster deployment, enhanced disaster recovery.

- Leading Region: North America, driven by technological innovation and enterprise adoption.

- Market share for North America: XX% (2025).

- Key countries: USA, Canada.

- Key End-User Industry: IT and Telecom, due to high data velocity and complexity.

- Contribution to market size from IT & Telecom: XX% (2025).

- Sub-segments: Telecommunications, Software Development, IT Services.

- Dominant Component: Database Patch and Release Automation, ensuring system stability and security.

- Market share for Database Patch and Release Automation: XX% (2025).

- Demand drivers: Regulatory compliance, risk mitigation, agile development.

- Enterprise Size Dominance: Large Enterprises, owing to larger budgets and complex needs.

- Market share for Large Enterprises: XX% (2025).

- Growth potential in SMEs: Driven by cost-effective SaaS solutions.

Database Automation Industry Product Landscape

The product landscape in the Database Automation Industry is characterized by sophisticated solutions that integrate artificial intelligence and machine learning to enhance efficiency and intelligence. Key innovations include intelligent patching systems that predict potential conflicts, automated release pipelines that reduce deployment times from weeks to minutes, and self-healing databases that proactively address performance issues. Performance metrics highlight significant improvements in deployment success rates, reduction in human error, and accelerated time-to-market for new database features. Unique selling propositions often revolve around seamless integration with existing DevOps toolchains and robust security features that ensure compliance with industry regulations. Technological advancements are continuously pushing the boundaries of what is possible, with a focus on cognitive automation and predictive analytics for database management.

Key Drivers, Barriers & Challenges in Database Automation Industry

The Database Automation Industry is propelled by several key drivers, including the increasing complexity of data environments, the growing demand for agility in software development and deployment, and the critical need for enhanced data security and compliance. The adoption of cloud computing and the rise of DevOps culture further catalyze market expansion.

- Key Drivers:

- Data volume and complexity explosion.

- Agile development and DevOps adoption.

- Need for stringent data security and regulatory compliance.

- Cost optimization and operational efficiency.

- Shortage of skilled database administrators.

Conversely, the industry faces several barriers and challenges, such as the high initial investment cost for some advanced solutions, resistance to change within traditional IT departments, and concerns about vendor lock-in. Integrating automation into legacy systems can also be a complex undertaking.

- Key Barriers & Challenges:

- High implementation costs for complex solutions.

- Resistance to change and organizational inertia.

- Integration complexities with legacy systems.

- Concerns over data security and privacy in automated processes.

- Skills gap in advanced automation technologies.

- Vendor lock-in concerns.

Emerging Opportunities in Database Automation Industry

Emerging opportunities in the Database Automation Industry lie in the development of more intelligent, self-learning automation platforms, particularly those leveraging AI and ML for predictive maintenance and anomaly detection. The expansion of DataOps across more diverse industries, including healthcare and manufacturing, presents a significant untapped market. Furthermore, the increasing demand for automated data governance and compliance solutions offers substantial growth potential.

- AI/ML-driven Predictive Analytics: For proactive database issue resolution.

- Expansion into New Verticals: Healthcare, manufacturing, and energy sectors.

- Automated Data Governance & Compliance: Meeting evolving regulatory demands.

- Low-Code/No-Code Automation Tools: Democratizing database management.

Growth Accelerators in the Database Automation Industry Industry

Long-term growth in the Database Automation Industry will be significantly accelerated by breakthroughs in artificial intelligence and machine learning that enable more autonomous database operations. Strategic partnerships between automation vendors and cloud service providers will further expand market reach and integration capabilities. Moreover, the ongoing digital transformation initiatives across global enterprises, coupled with the increasing adoption of data-driven decision-making, will continue to fuel demand for efficient and reliable database automation solutions.

Key Players Shaping the Database Automation Industry Market

- IDERA Inc

- IBM Corporation

- Quest Software Inc

- Datavail

- BMC Software Inc

- Bryter US Inc

- Amazon Web Services Inc

- CA Technologies (Broadcom Inc)

- Oracle Corporation

- SAP SE

Notable Milestones in Database Automation Industry Sector

- June 2023: Aquatic Informatics launched HydroCorrect, an automated data validation tool for enhanced water data management using machine learning.

- May 2023: data.world acquired Mighty Canary technology to enhance its DataOps application with automation for real-time data quality insights.

In-Depth Database Automation Industry Market Outlook

The future outlook for the Database Automation Industry is exceptionally promising, driven by the pervasive need for efficiency, agility, and security in managing increasingly vast and complex data ecosystems. The integration of advanced AI and ML capabilities will usher in an era of more autonomous database management, reducing human intervention and minimizing errors. Continued investment in cloud-native automation solutions and the expansion of DataOps principles across diverse sectors are poised to be significant growth accelerators. As organizations across the globe accelerate their digital transformation journeys, the demand for robust and intelligent database automation will only intensify, creating substantial strategic opportunities for innovation and market leadership.

Database Automation Industry Segmentation

-

1. Component

-

1.1. Solution

- 1.1.1. Database Patch and Release Automation

- 1.1.2. Application Release Automation

- 1.1.3. Database Test Automation

- 1.2. Services

-

1.1. Solution

-

2. Deployment Mode

- 2.1. Cloud

- 2.2. On-Premises

-

3. Enterprise Size

- 3.1. Large Enterprises

- 3.2. Small and Medium-Sized Enterprises

-

4. End-user Industry

- 4.1. Banking, Financial Services and Insurance (BFSI)

- 4.2. IT and Telecom

- 4.3. E-commerce and Retail

- 4.4. Manufacturing

- 4.5. Government and Defense

- 4.6. Others (Manufacturing, Media and Entertainment)

Database Automation Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Database Automation Industry Regional Market Share

Geographic Coverage of Database Automation Industry

Database Automation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 24.38% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Solution

- 5.1.1.1. Database Patch and Release Automation

- 5.1.1.2. Application Release Automation

- 5.1.1.3. Database Test Automation

- 5.1.2. Services

- 5.1.1. Solution

- 5.2. Market Analysis, Insights and Forecast - by Deployment Mode

- 5.2.1. Cloud

- 5.2.2. On-Premises

- 5.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 5.3.1. Large Enterprises

- 5.3.2. Small and Medium-Sized Enterprises

- 5.4. Market Analysis, Insights and Forecast - by End-user Industry

- 5.4.1. Banking, Financial Services and Insurance (BFSI)

- 5.4.2. IT and Telecom

- 5.4.3. E-commerce and Retail

- 5.4.4. Manufacturing

- 5.4.5. Government and Defense

- 5.4.6. Others (Manufacturing, Media and Entertainment)

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. Latin America

- 5.5.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Global Database Automation Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Solution

- 6.1.1.1. Database Patch and Release Automation

- 6.1.1.2. Application Release Automation

- 6.1.1.3. Database Test Automation

- 6.1.2. Services

- 6.1.1. Solution

- 6.2. Market Analysis, Insights and Forecast - by Deployment Mode

- 6.2.1. Cloud

- 6.2.2. On-Premises

- 6.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 6.3.1. Large Enterprises

- 6.3.2. Small and Medium-Sized Enterprises

- 6.4. Market Analysis, Insights and Forecast - by End-user Industry

- 6.4.1. Banking, Financial Services and Insurance (BFSI)

- 6.4.2. IT and Telecom

- 6.4.3. E-commerce and Retail

- 6.4.4. Manufacturing

- 6.4.5. Government and Defense

- 6.4.6. Others (Manufacturing, Media and Entertainment)

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. North America Database Automation Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Solution

- 7.1.1.1. Database Patch and Release Automation

- 7.1.1.2. Application Release Automation

- 7.1.1.3. Database Test Automation

- 7.1.2. Services

- 7.1.1. Solution

- 7.2. Market Analysis, Insights and Forecast - by Deployment Mode

- 7.2.1. Cloud

- 7.2.2. On-Premises

- 7.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 7.3.1. Large Enterprises

- 7.3.2. Small and Medium-Sized Enterprises

- 7.4. Market Analysis, Insights and Forecast - by End-user Industry

- 7.4.1. Banking, Financial Services and Insurance (BFSI)

- 7.4.2. IT and Telecom

- 7.4.3. E-commerce and Retail

- 7.4.4. Manufacturing

- 7.4.5. Government and Defense

- 7.4.6. Others (Manufacturing, Media and Entertainment)

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. Europe Database Automation Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Solution

- 8.1.1.1. Database Patch and Release Automation

- 8.1.1.2. Application Release Automation

- 8.1.1.3. Database Test Automation

- 8.1.2. Services

- 8.1.1. Solution

- 8.2. Market Analysis, Insights and Forecast - by Deployment Mode

- 8.2.1. Cloud

- 8.2.2. On-Premises

- 8.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 8.3.1. Large Enterprises

- 8.3.2. Small and Medium-Sized Enterprises

- 8.4. Market Analysis, Insights and Forecast - by End-user Industry

- 8.4.1. Banking, Financial Services and Insurance (BFSI)

- 8.4.2. IT and Telecom

- 8.4.3. E-commerce and Retail

- 8.4.4. Manufacturing

- 8.4.5. Government and Defense

- 8.4.6. Others (Manufacturing, Media and Entertainment)

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Asia Pacific Database Automation Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Solution

- 9.1.1.1. Database Patch and Release Automation

- 9.1.1.2. Application Release Automation

- 9.1.1.3. Database Test Automation

- 9.1.2. Services

- 9.1.1. Solution

- 9.2. Market Analysis, Insights and Forecast - by Deployment Mode

- 9.2.1. Cloud

- 9.2.2. On-Premises

- 9.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 9.3.1. Large Enterprises

- 9.3.2. Small and Medium-Sized Enterprises

- 9.4. Market Analysis, Insights and Forecast - by End-user Industry

- 9.4.1. Banking, Financial Services and Insurance (BFSI)

- 9.4.2. IT and Telecom

- 9.4.3. E-commerce and Retail

- 9.4.4. Manufacturing

- 9.4.5. Government and Defense

- 9.4.6. Others (Manufacturing, Media and Entertainment)

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Latin America Database Automation Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Solution

- 10.1.1.1. Database Patch and Release Automation

- 10.1.1.2. Application Release Automation

- 10.1.1.3. Database Test Automation

- 10.1.2. Services

- 10.1.1. Solution

- 10.2. Market Analysis, Insights and Forecast - by Deployment Mode

- 10.2.1. Cloud

- 10.2.2. On-Premises

- 10.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 10.3.1. Large Enterprises

- 10.3.2. Small and Medium-Sized Enterprises

- 10.4. Market Analysis, Insights and Forecast - by End-user Industry

- 10.4.1. Banking, Financial Services and Insurance (BFSI)

- 10.4.2. IT and Telecom

- 10.4.3. E-commerce and Retail

- 10.4.4. Manufacturing

- 10.4.5. Government and Defense

- 10.4.6. Others (Manufacturing, Media and Entertainment)

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Middle East and Africa Database Automation Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Component

- 11.1.1. Solution

- 11.1.1.1. Database Patch and Release Automation

- 11.1.1.2. Application Release Automation

- 11.1.1.3. Database Test Automation

- 11.1.2. Services

- 11.1.1. Solution

- 11.2. Market Analysis, Insights and Forecast - by Deployment Mode

- 11.2.1. Cloud

- 11.2.2. On-Premises

- 11.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 11.3.1. Large Enterprises

- 11.3.2. Small and Medium-Sized Enterprises

- 11.4. Market Analysis, Insights and Forecast - by End-user Industry

- 11.4.1. Banking, Financial Services and Insurance (BFSI)

- 11.4.2. IT and Telecom

- 11.4.3. E-commerce and Retail

- 11.4.4. Manufacturing

- 11.4.5. Government and Defense

- 11.4.6. Others (Manufacturing, Media and Entertainment)

- 11.1. Market Analysis, Insights and Forecast - by Component

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 IDERA Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 IBM Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Quest Software Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Datavail

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 BMC Software Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Bryter US Inc *List Not Exhaustive

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Amazon Web Services Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 CA Technologies (Broadcom Inc)

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Oracle Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 SAP SE

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 IDERA Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Database Automation Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Database Automation Industry Revenue (Million), by Component 2025 & 2033

- Figure 3: North America Database Automation Industry Revenue Share (%), by Component 2025 & 2033

- Figure 4: North America Database Automation Industry Revenue (Million), by Deployment Mode 2025 & 2033

- Figure 5: North America Database Automation Industry Revenue Share (%), by Deployment Mode 2025 & 2033

- Figure 6: North America Database Automation Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 7: North America Database Automation Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 8: North America Database Automation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 9: North America Database Automation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 10: North America Database Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 11: North America Database Automation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Database Automation Industry Revenue (Million), by Component 2025 & 2033

- Figure 13: Europe Database Automation Industry Revenue Share (%), by Component 2025 & 2033

- Figure 14: Europe Database Automation Industry Revenue (Million), by Deployment Mode 2025 & 2033

- Figure 15: Europe Database Automation Industry Revenue Share (%), by Deployment Mode 2025 & 2033

- Figure 16: Europe Database Automation Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 17: Europe Database Automation Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 18: Europe Database Automation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 19: Europe Database Automation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 20: Europe Database Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Europe Database Automation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Database Automation Industry Revenue (Million), by Component 2025 & 2033

- Figure 23: Asia Pacific Database Automation Industry Revenue Share (%), by Component 2025 & 2033

- Figure 24: Asia Pacific Database Automation Industry Revenue (Million), by Deployment Mode 2025 & 2033

- Figure 25: Asia Pacific Database Automation Industry Revenue Share (%), by Deployment Mode 2025 & 2033

- Figure 26: Asia Pacific Database Automation Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 27: Asia Pacific Database Automation Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 28: Asia Pacific Database Automation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 29: Asia Pacific Database Automation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Asia Pacific Database Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Database Automation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Latin America Database Automation Industry Revenue (Million), by Component 2025 & 2033

- Figure 33: Latin America Database Automation Industry Revenue Share (%), by Component 2025 & 2033

- Figure 34: Latin America Database Automation Industry Revenue (Million), by Deployment Mode 2025 & 2033

- Figure 35: Latin America Database Automation Industry Revenue Share (%), by Deployment Mode 2025 & 2033

- Figure 36: Latin America Database Automation Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 37: Latin America Database Automation Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 38: Latin America Database Automation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 39: Latin America Database Automation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 40: Latin America Database Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Latin America Database Automation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Database Automation Industry Revenue (Million), by Component 2025 & 2033

- Figure 43: Middle East and Africa Database Automation Industry Revenue Share (%), by Component 2025 & 2033

- Figure 44: Middle East and Africa Database Automation Industry Revenue (Million), by Deployment Mode 2025 & 2033

- Figure 45: Middle East and Africa Database Automation Industry Revenue Share (%), by Deployment Mode 2025 & 2033

- Figure 46: Middle East and Africa Database Automation Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 47: Middle East and Africa Database Automation Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 48: Middle East and Africa Database Automation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 49: Middle East and Africa Database Automation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 50: Middle East and Africa Database Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 51: Middle East and Africa Database Automation Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Database Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 2: Global Database Automation Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 3: Global Database Automation Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 4: Global Database Automation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 5: Global Database Automation Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Database Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 7: Global Database Automation Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 8: Global Database Automation Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 9: Global Database Automation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 10: Global Database Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Global Database Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 12: Global Database Automation Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 13: Global Database Automation Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 14: Global Database Automation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 15: Global Database Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Database Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 17: Global Database Automation Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 18: Global Database Automation Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 19: Global Database Automation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 20: Global Database Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global Database Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 22: Global Database Automation Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 23: Global Database Automation Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 24: Global Database Automation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 25: Global Database Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Global Database Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 27: Global Database Automation Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 28: Global Database Automation Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 29: Global Database Automation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 30: Global Database Automation Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Database Automation Industry?

The projected CAGR is approximately 24.38%.

2. Which companies are prominent players in the Database Automation Industry?

Key companies in the market include IDERA Inc, IBM Corporation, Quest Software Inc, Datavail, BMC Software Inc, Bryter US Inc *List Not Exhaustive, Amazon Web Services Inc, CA Technologies (Broadcom Inc), Oracle Corporation, SAP SE.

3. What are the main segments of the Database Automation Industry?

The market segments include Component, Deployment Mode, Enterprise Size, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.35 Million as of 2022.

5. What are some drivers contributing to market growth?

Continuously Growing Volumes of Data Across Verticals; Increasing Demand for Automating Repetitive Database Management Processes.

6. What are the notable trends driving market growth?

IT and Telecommunication industry is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

; Managing Identities Across Multiple Operation Environments.

8. Can you provide examples of recent developments in the market?

June 2023: Aquatic Informatics launched a new automated data validation tool, HydroCorrect, that can accelerate proactive monitoring and management of flooding, groundwater, and water quality in the Aquarius platform. With machine-learning technology, HydroCorrect will transform the QA/QC process with automation and standardized workflows that save time and improve data quality.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Database Automation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Database Automation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Database Automation Industry?

To stay informed about further developments, trends, and reports in the Database Automation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence