Key Insights

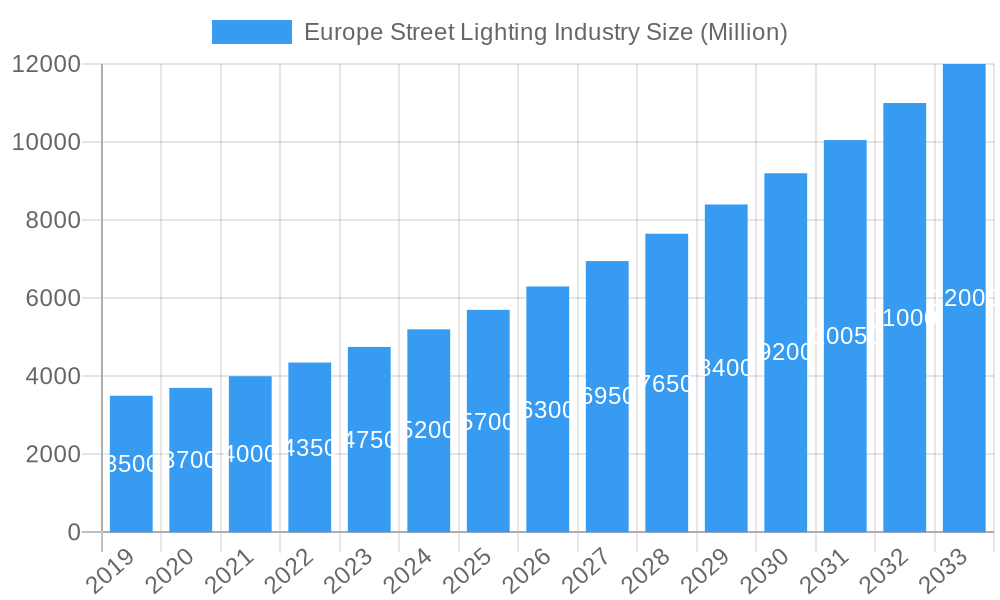

The European street lighting market is projected to reach 2445.6 million by 2024, expanding at a Compound Annual Growth Rate (CAGR) of 2.8% through 2033. This growth is propelled by the widespread adoption of smart lighting technologies and the increasing integration of LEDs. European governments are investing in upgrading conventional street lighting to energy-efficient, technologically advanced solutions, driven by the need to reduce energy consumption, operational costs, and enhance public safety and environmental sustainability. The rising demand for intelligent urban infrastructure and smart city initiatives, which utilize connected streetlights for data collection, further fuels market expansion. The market is segmented into smart lighting solutions and conventional lighting, with a pronounced shift towards smart technologies. LEDs are the dominant light source due to their superior performance and longevity.

Europe Street Lighting Industry Market Size (In Billion)

Key trends include the move towards connected, IoT-enabled lighting systems for remote monitoring, predictive maintenance, and dynamic lighting control, optimizing energy usage and enabling new functionalities. Sustainability and circular economy principles are driving demand for eco-friendly and durable lighting solutions, supported by energy efficiency regulations and government incentives. Restraints include the significant upfront investment for smart infrastructure upgrades, the need for skilled personnel, and cybersecurity concerns. Despite these challenges, the substantial cost savings, environmental benefits, and improvements to urban living are expected to drive sustained market growth.

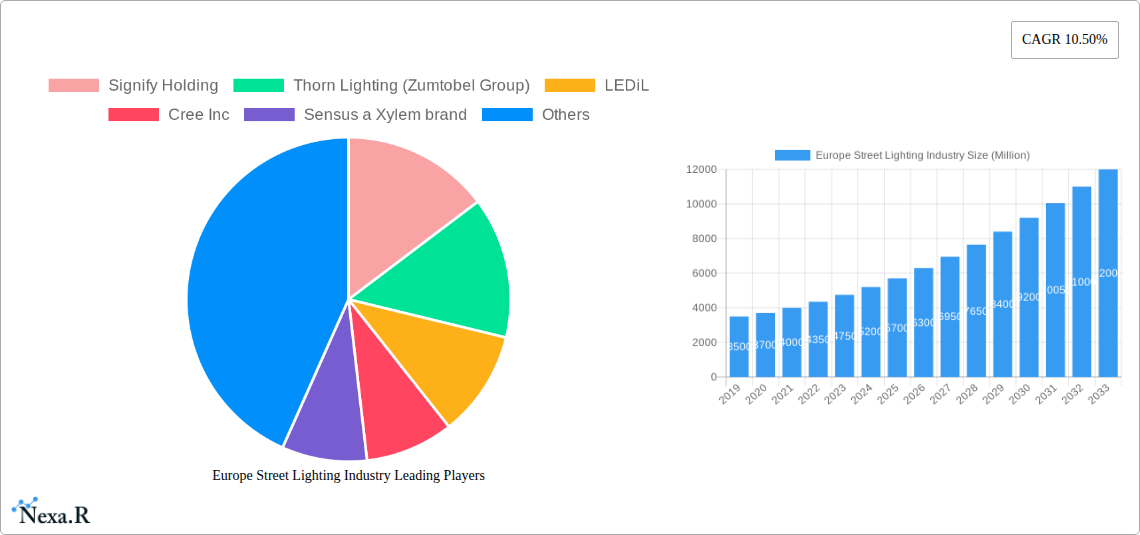

Europe Street Lighting Industry Company Market Share

Europe Street Lighting Industry Report Description: Smart & Sustainable Solutions for Urban Futures

This comprehensive report delves into the dynamic Europe Street Lighting Industry, offering an in-depth analysis of market trends, technological advancements, and growth projections for the period 2019–2033. With a base year of 2025 and a forecast period from 2025–2033, this study provides critical insights for stakeholders navigating the evolving landscape of urban illumination. We dissect the market by Lighting Type (Conventional Lighting vs. Smart Lighting), Light Source (LEDs, Fluorescent Lights, HID Lamps), and Offering (Hardware like Luminaries and Control Systems, alongside Software and Services). This report is essential for understanding the transition towards intelligent, energy-efficient, and sustainable street lighting solutions across the continent.

Europe Street Lighting Industry Market Dynamics & Structure

The Europe Street Lighting Industry is characterized by a moderately concentrated market, with key players investing heavily in R&D to drive technological innovation. The primary drivers for innovation include the growing demand for energy efficiency, smart city integration, and enhanced public safety. Regulatory frameworks, such as EU directives on energy performance and eco-design, are pivotal in shaping market trends and encouraging the adoption of advanced lighting solutions. While conventional lighting still holds a significant share, Smart Lighting is experiencing rapid adoption, driven by its ability to offer remote management, energy savings, and integration with other smart city services. Competitive product substitutes are emerging, particularly in the realm of advanced LED technologies and integrated sensor systems. End-user demographics are shifting towards municipalities and urban planners prioritizing sustainability and operational cost reduction. Mergers and Acquisitions (M&A) activity, such as Signify's acquisition of Telensa Holdings Ltd, are indicative of consolidation trends and strategic moves to enhance market position and expand service offerings. Barriers to innovation include high initial investment costs for smart infrastructure and the need for standardized interoperability protocols.

- Market Concentration: Moderately concentrated with a few dominant players.

- Technological Innovation Drivers: Energy efficiency, smart city integration, enhanced safety, IoT connectivity.

- Regulatory Frameworks: EU energy directives, eco-design standards, waste electrical and electronic equipment (WEEE) regulations.

- Competitive Product Substitutes: Advanced LED technologies, connected lighting systems, luminaire designs with integrated sensors.

- End-User Demographics: Municipalities, urban development authorities, infrastructure management companies.

- M&A Trends: Strategic acquisitions to gain smart city capabilities and expand product portfolios.

Europe Street Lighting Industry Growth Trends & Insights

The Europe Street Lighting Industry is poised for significant growth, driven by a confluence of factors including increasing urbanization, a strong regulatory push towards energy efficiency, and the rapid evolution of smart city technologies. The market size is projected to expand at a robust Compound Annual Growth Rate (CAGR) over the forecast period. The adoption of LEDs as the predominant light source is a key trend, offering superior energy savings, longer lifespan, and better controllability compared to traditional lighting technologies. This shift is further accelerated by government incentives and a growing public awareness of environmental concerns. Smart Lighting solutions are witnessing remarkable adoption rates, moving beyond mere illumination to become integral components of intelligent urban infrastructure. These systems enable real-time monitoring, fault detection, and dynamic adjustments based on traffic flow and environmental conditions, leading to substantial operational cost reductions for municipalities. Technological disruptions, such as the integration of Artificial Intelligence (AI) for predictive maintenance and the development of advanced sensor networks, are transforming the functionality and benefits of street lighting. Consumer behavior shifts are evident in the increasing demand from cities for integrated solutions that offer not just lighting but also data collection and connectivity capabilities for smart city applications. The market penetration of smart street lighting is expected to reach significant levels by 2033, as cities increasingly invest in digital transformation initiatives. The historical period (2019–2024) has laid the groundwork for this expansion, with continuous advancements in LED technology and the early adoption of pilot smart lighting projects. The estimated market value in 2025 is expected to reflect a strong upward trajectory.

Dominant Regions, Countries, or Segments in Europe Street Lighting Industry

The Europe Street Lighting Industry is witnessing robust growth across various segments, with Smart Lighting emerging as the dominant force driving market expansion. This segment's ascendancy is attributed to its multifaceted benefits, including significant energy savings, enhanced operational efficiency through remote management, and its crucial role in the broader development of smart cities. The LED light source segment also holds substantial dominance, having largely replaced conventional technologies like fluorescent and HID lamps due to its energy efficiency, longevity, and superior light quality. In terms of regions, Western Europe, particularly countries like Germany, the UK, France, and the Netherlands, consistently leads the market. This dominance is fueled by strong economic policies supporting green initiatives, substantial investments in urban infrastructure upgrades, and a high degree of technological adoption. Cities within these countries are actively implementing large-scale smart street lighting projects, leveraging advanced control systems and integrated sensor technologies. The Hardware offering, specifically Luminaries and Control Systems, forms the backbone of this growth, representing the core components of both conventional and smart lighting installations. However, the integration of Software and Services is increasingly becoming a critical differentiator, offering value-added functionalities such as data analytics, predictive maintenance, and seamless integration with other smart city platforms. Economic incentives, such as government grants for energy-efficient retrofits and smart city initiatives, act as key drivers, encouraging municipalities to upgrade their existing infrastructure. The market share of Smart Lighting and LEDs is projected to continue its upward trend, outperforming Conventional Lighting and other light sources. The growth potential in these dominant segments remains exceptionally high, driven by ongoing technological advancements and a steadfast commitment to sustainable urban development.

- Dominant Segment (Lighting Type): Smart Lighting

- Dominant Segment (Light Source): LEDs

- Dominant Offering: Hardware (Luminaries, Control Systems), Software and Services

- Leading Regions: Western Europe (Germany, UK, France, Netherlands)

- Key Drivers:

- Government incentives for energy efficiency and smart city development.

- Urban population growth necessitating modern infrastructure.

- Technological advancements in IoT and data analytics.

- Increasing focus on public safety and resource management.

Europe Street Lighting Industry Product Landscape

The Europe Street Lighting Industry is characterized by a continuous stream of product innovations focused on enhancing energy efficiency, connectivity, and functionality. Manufacturers are increasingly integrating advanced LED technologies with intelligent control systems, offering luminaires with superior photometric performance and extended lifespans. Products like Cyclone Lighting's Kanata luminaire exemplify this trend, providing a classic design suitable for historical urban settings while boasting outstanding photometric performance for diverse street applications. Furthermore, the market is seeing the rise of integrated systems that combine lighting with sensors for traffic monitoring, environmental data collection, and even public Wi-Fi. Software platforms are becoming sophisticated, enabling remote management, fault diagnosis, and dynamic lighting adjustments. The unique selling propositions revolve around cost savings through energy reduction, improved urban livability, and the seamless integration of lighting infrastructure into the broader smart city ecosystem.

Key Drivers, Barriers & Challenges in Europe Street Lighting Industry

Key Drivers: The Europe Street Lighting Industry is propelled by significant drivers. Foremost among these is the relentless pursuit of energy efficiency and cost reduction by municipalities, making LED and smart lighting solutions highly attractive. Government regulations and ambitious climate targets, such as those outlined by the EU, mandate the adoption of sustainable lighting technologies. The burgeoning growth of smart city initiatives globally positions street lighting as a critical infrastructure component for connectivity and data collection. Furthermore, advancements in LED technology continue to improve performance and reduce costs, making them increasingly accessible.

- Energy Efficiency Mandates: EU directives and national targets for energy savings.

- Smart City Integration: Demand for connected infrastructure and data-driven urban management.

- Technological Advancements: Improved LED performance, miniaturization of sensors, and enhanced control systems.

- Cost Savings: Reduced electricity consumption and lower maintenance expenses.

Barriers & Challenges: Despite robust growth, the industry faces several hurdles. The high initial investment cost for smart lighting infrastructure can be a significant barrier for some municipalities, particularly smaller ones. Interoperability issues between different manufacturers' systems and the lack of universally adopted standards can hinder seamless integration. Cybersecurity concerns associated with connected lighting systems require robust security measures. Long procurement cycles and complex tendering processes in public sectors can also slow down project implementation. Finally, legacy infrastructure and the need for extensive rewiring present considerable challenges during the transition to new technologies.

- High Upfront Investment: Significant capital expenditure for smart lighting and control systems.

- Interoperability and Standardization: Lack of universal standards for connected devices.

- Cybersecurity Risks: Protecting connected lighting networks from cyber threats.

- Regulatory and Bureaucratic Hurdles: Lengthy procurement processes and complex approval procedures.

- Infrastructure Replacement: The cost and complexity of upgrading existing street lighting networks.

Emerging Opportunities in Europe Street Lighting Industry

Emerging opportunities in the Europe Street Lighting Industry are manifold, driven by evolving urban needs and technological integration. The increasing demand for integrated smart city solutions presents a significant avenue, where streetlights serve as a platform for various IoT applications beyond illumination, such as environmental monitoring, public safety surveillance, and traffic management. The development and deployment of energy-harvesting street lighting technologies and bi-directional charging infrastructure for electric vehicles integrated into street furniture are gaining traction. Furthermore, the retrofitting of existing infrastructure in older urban centers with aesthetically pleasing yet technologically advanced luminaries offers substantial potential. The growing emphasis on circular economy principles is also opening doors for manufacturers focused on sustainable materials and product lifecycle management in lighting solutions.

Growth Accelerators in the Europe Street Lighting Industry Industry

Several catalysts are accelerating the growth of the Europe Street Lighting Industry. The continuous innovation in LED technology, leading to higher efficacy, improved color rendering, and enhanced controllability, is a primary accelerator. The expanding deployment of 5G networks and the increasing adoption of the Internet of Things (IoT) are creating a fertile ground for smart street lighting, enabling seamless connectivity and data exchange. Government initiatives and funding programs supporting energy efficiency and smart city development are significantly boosting market penetration. Strategic partnerships and acquisitions, such as Signify's acquisition of Telensa Holdings Ltd, are consolidating the market and expanding the capabilities of key players, driving further innovation and market reach.

Key Players Shaping the Europe Street Lighting Industry Market

- Signify Holding

- Thorn Lighting (Zumtobel Group)

- LEDiL

- Cree Inc

- Sensus a Xylem brand

- Eaton Corporation PLC

- Luxtella (Le-tehnika)

- Acuity Brands Inc

- OSRAM Gmbh

- General Electric Company

Notable Milestones in Europe Street Lighting Industry Sector

- April 2022: Cyclone Lighting released its Kanata luminaire, a sleek, classic outdoor luminaire designed to replace outdated Cobra Heads in historical urban settings, offering outstanding photometric performance for various street and roadway applications.

- July 2021: Signify acquired Telensa Holdings Ltd, a UK-based company specializing in smart city wireless monitoring and control systems. This acquisition bolsters Signify's smart city offerings with a narrow-band and TALQ-compliant solution, aiming to make smart city infrastructure more affordable.

In-Depth Europe Street Lighting Industry Market Outlook

The Europe Street Lighting Industry is set for robust expansion, driven by ongoing technological breakthroughs and strategic market plays. Growth accelerators such as advanced LED efficacy, the pervasive adoption of IoT, and supportive government policies will continue to fuel market penetration. The increasing integration of smart features, transforming streetlights into data hubs for smart cities, represents a significant opportunity. Strategic partnerships and M&A activities will likely shape the competitive landscape, fostering innovation and expanding service portfolios. The future market potential lies in developing more sustainable, interconnected, and versatile lighting solutions that address the evolving needs of urban environments, paving the way for smarter, safer, and more energy-efficient cities across Europe.

Europe Street Lighting Industry Segmentation

-

1. Lighting Type

- 1.1. Conventional Lighting

- 1.2. Smart Lighting

-

2. Light Source

- 2.1. LEDs

- 2.2. Fluorescent Lights

- 2.3. HID Lamps

-

3. Offering

-

3.1. Hardware

- 3.1.1. Lights and Bulbs

- 3.1.2. Luminaries

- 3.1.3. Control Systems

- 3.2. Software and Services

-

3.1. Hardware

Europe Street Lighting Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

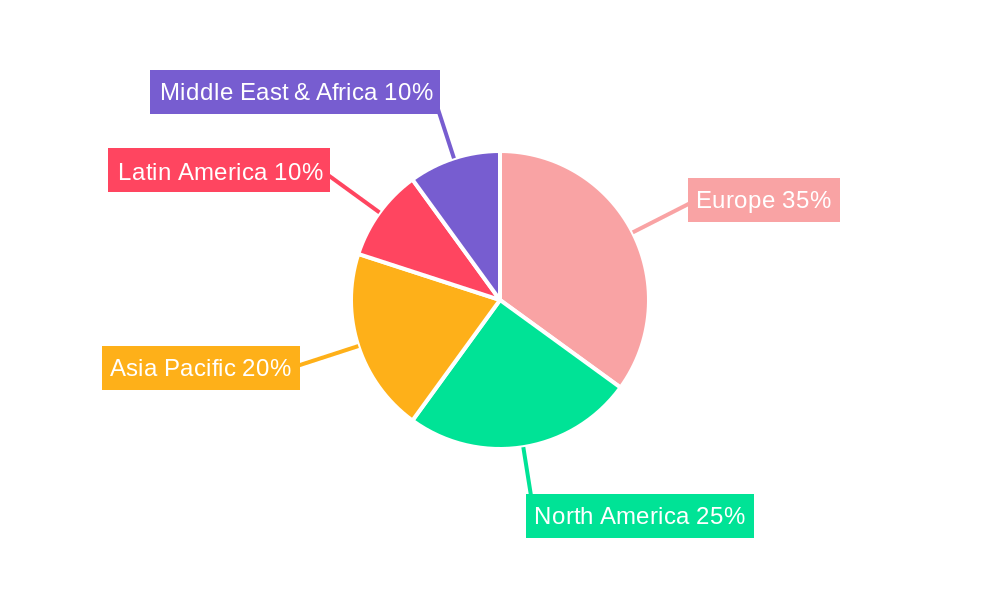

Europe Street Lighting Industry Regional Market Share

Geographic Coverage of Europe Street Lighting Industry

Europe Street Lighting Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Lighting Type

- 5.1.1. Conventional Lighting

- 5.1.2. Smart Lighting

- 5.2. Market Analysis, Insights and Forecast - by Light Source

- 5.2.1. LEDs

- 5.2.2. Fluorescent Lights

- 5.2.3. HID Lamps

- 5.3. Market Analysis, Insights and Forecast - by Offering

- 5.3.1. Hardware

- 5.3.1.1. Lights and Bulbs

- 5.3.1.2. Luminaries

- 5.3.1.3. Control Systems

- 5.3.2. Software and Services

- 5.3.1. Hardware

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Lighting Type

- 6. Europe Street Lighting Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Lighting Type

- 6.1.1. Conventional Lighting

- 6.1.2. Smart Lighting

- 6.2. Market Analysis, Insights and Forecast - by Light Source

- 6.2.1. LEDs

- 6.2.2. Fluorescent Lights

- 6.2.3. HID Lamps

- 6.3. Market Analysis, Insights and Forecast - by Offering

- 6.3.1. Hardware

- 6.3.1.1. Lights and Bulbs

- 6.3.1.2. Luminaries

- 6.3.1.3. Control Systems

- 6.3.2. Software and Services

- 6.3.1. Hardware

- 6.1. Market Analysis, Insights and Forecast - by Lighting Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Signify Holding

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Thorn Lighting (Zumtobel Group)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 LEDiL

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Cree Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Sensus a Xylem brand

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Eaton Corporation PLC

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Luxtella (Le-tehnika)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Acuity Brands Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 OSRAM Gmbh

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 General Electric Company

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Signify Holding

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Street Lighting Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Europe Street Lighting Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Street Lighting Industry Revenue million Forecast, by Lighting Type 2020 & 2033

- Table 2: Europe Street Lighting Industry Revenue million Forecast, by Light Source 2020 & 2033

- Table 3: Europe Street Lighting Industry Revenue million Forecast, by Offering 2020 & 2033

- Table 4: Europe Street Lighting Industry Revenue million Forecast, by Region 2020 & 2033

- Table 5: Europe Street Lighting Industry Revenue million Forecast, by Lighting Type 2020 & 2033

- Table 6: Europe Street Lighting Industry Revenue million Forecast, by Light Source 2020 & 2033

- Table 7: Europe Street Lighting Industry Revenue million Forecast, by Offering 2020 & 2033

- Table 8: Europe Street Lighting Industry Revenue million Forecast, by Country 2020 & 2033

- Table 9: United Kingdom Europe Street Lighting Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Germany Europe Street Lighting Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 11: France Europe Street Lighting Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 12: Italy Europe Street Lighting Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 13: Spain Europe Street Lighting Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Netherlands Europe Street Lighting Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Belgium Europe Street Lighting Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Sweden Europe Street Lighting Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 17: Norway Europe Street Lighting Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Poland Europe Street Lighting Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 19: Denmark Europe Street Lighting Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Street Lighting Industry?

The projected CAGR is approximately 2.8%.

2. Which companies are prominent players in the Europe Street Lighting Industry?

Key companies in the market include Signify Holding, Thorn Lighting (Zumtobel Group), LEDiL, Cree Inc, Sensus a Xylem brand, Eaton Corporation PLC, Luxtella (Le-tehnika), Acuity Brands Inc, OSRAM Gmbh, General Electric Company.

3. What are the main segments of the Europe Street Lighting Industry?

The market segments include Lighting Type, Light Source, Offering.

4. Can you provide details about the market size?

The market size is estimated to be USD 2445.6 million as of 2022.

5. What are some drivers contributing to market growth?

Increased Demand for Intelligent Solutions in Street Lighting Systems; Increasing Adoption of Smart City Infrastructure; Supportive regulatory framework and legislation by Governments.

6. What are the notable trends driving market growth?

Smart Lighting Segments Holds the Largest Market Share.

7. Are there any restraints impacting market growth?

Challenges Associated With LED Driver Failure and High Cost Associated With Installation.

8. Can you provide examples of recent developments in the market?

April 2022 - Cyclone Lighting, one of the leaders in manufacturing outdoor luminaires, announced that it had released its Kanata luminaire. The product's design is a sleek, classic take on a traditional favorite and has been introduced to replace outdated luminaries such as Cobra Heads in historical urban settings. With outstanding photometric performance, Kanata luminaires are suitable for multiple street and roadway applications, including urban boulevards and alleyways, city streets, historic districts, and residential neighborhoods.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Street Lighting Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Street Lighting Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Street Lighting Industry?

To stay informed about further developments, trends, and reports in the Europe Street Lighting Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence