Key Insights

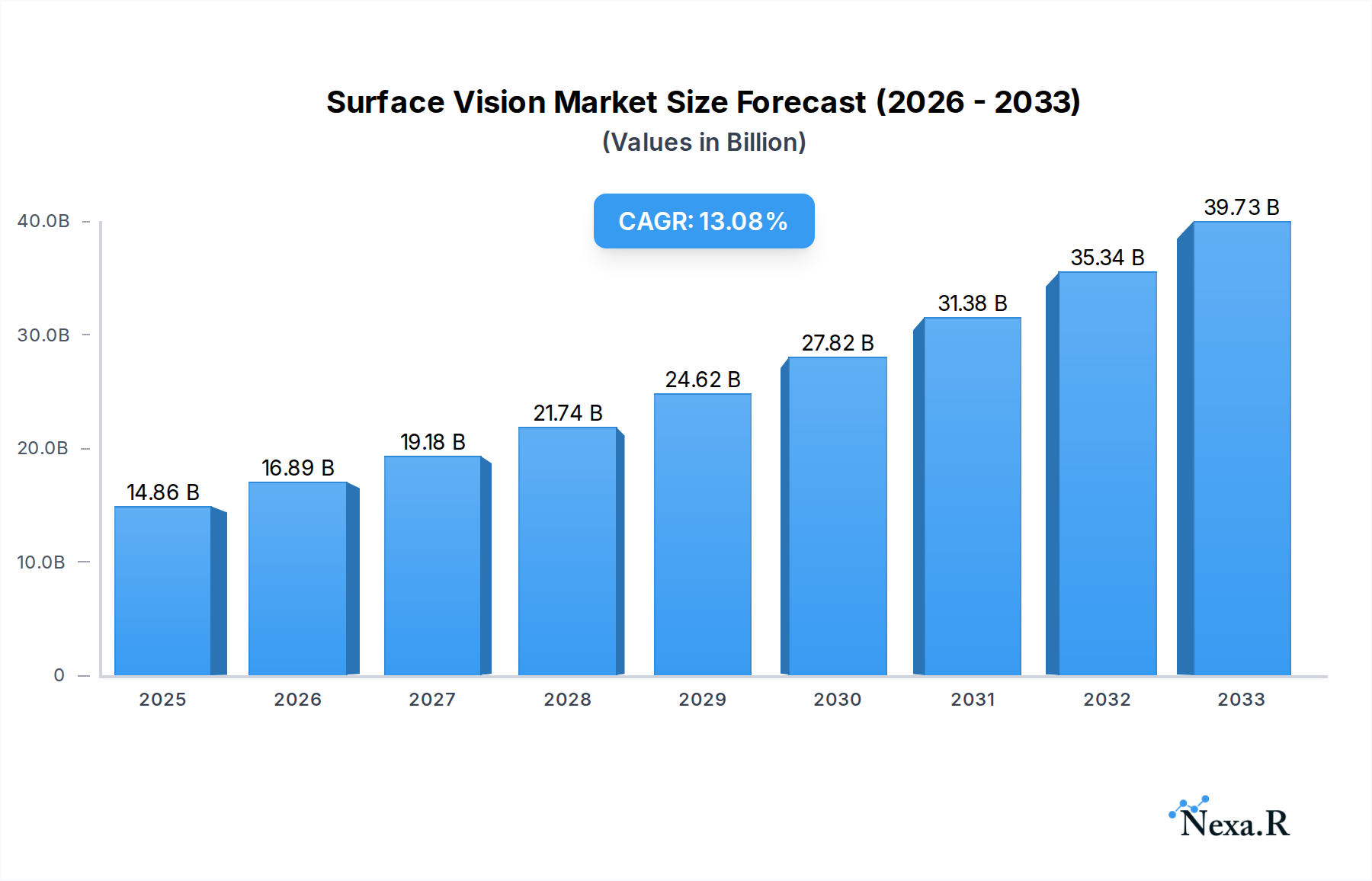

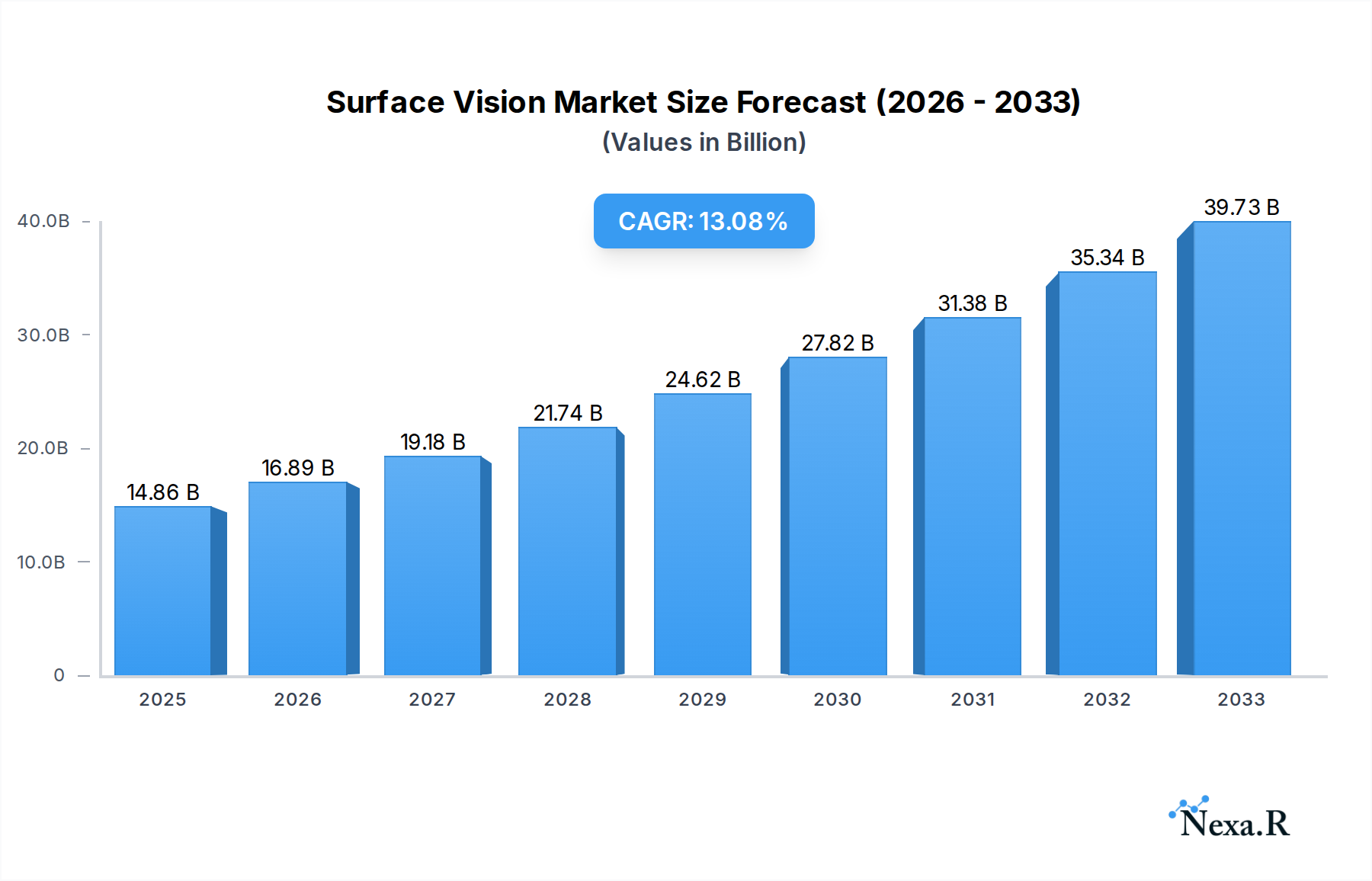

The global Surface Vision & Inspection Equipment market is poised for substantial growth, projected to reach a valuation of $14.86 billion by 2025. This robust expansion is underpinned by a remarkable Compound Annual Growth Rate (CAGR) of 14.56% during the forecast period. The primary drivers fueling this upward trajectory include the escalating demand for enhanced quality control across manufacturing sectors, driven by stringent regulatory requirements and the pursuit of zero-defect production. The integration of advanced technologies such as artificial intelligence (AI) and machine learning (ML) into vision systems is further accelerating adoption, enabling more sophisticated defect detection and process optimization. The automotive sector, with its increasing complexity and emphasis on safety, is a significant contributor, alongside the burgeoning electrical & electronics industry which relies heavily on precise inspection for component integrity and functionality. Furthermore, the medical & pharmaceuticals industry is witnessing increased investment in automated inspection to ensure product safety and compliance.

Surface Vision & Inspection Equipment Industry Market Size (In Billion)

Emerging trends like the adoption of 3D vision systems for detailed surface analysis and the growing implementation of robotic guidance systems are reshaping the market landscape. The increasing use of these sophisticated inspection techniques in the food & beverages and postal & logistics sectors, to ensure product quality, safety, and efficient sorting, further bolsters market demand. While the market is characterized by strong growth, certain restraints, such as the high initial investment cost for advanced systems and the need for skilled personnel for operation and maintenance, may pose challenges for smaller enterprises. However, the persistent drive towards automation, efficiency gains, and the inherent benefits of improved product quality and reduced waste are expected to outweigh these limitations, ensuring a dynamic and expanding market for surface vision and inspection equipment.

Surface Vision & Inspection Equipment Industry Company Market Share

Unlock critical insights into the Surface Vision & Inspection Equipment industry with this in-depth report. Spanning the study period of 2019–2033, with a base year of 2025, this comprehensive analysis delves into market dynamics, growth trends, regional dominance, and the competitive landscape. Essential for stakeholders, manufacturers, and investors, this report provides a granular view of market segmentation by component (Camera, Lighting Equipment, Optics, Other Components) and application (Automotive, Electrical & Electronics, Medical & Pharmaceuticals, Food & Beverages, Postal & Logistics, Other Applications). Discover the future of industrial automation and quality control with expert analysis and actionable intelligence.

Surface Vision & Inspection Equipment Industry Market Dynamics & Structure

The Surface Vision & Inspection Equipment market exhibits a moderately concentrated structure, with key players like Cognex Corporation, Keyence Corporation, and AMETEK Surface Vision holding significant market shares. Technological innovation, particularly in areas like AI-powered defect detection and high-speed imaging, serves as a primary driver for market growth. Emerging trends point towards the integration of machine learning algorithms for predictive maintenance and sophisticated anomaly detection. Regulatory frameworks, especially concerning product safety and quality in sectors like automotive and pharmaceuticals, are indirectly shaping the adoption of advanced vision systems. Competitive product substitutes, such as manual inspection and less advanced automated systems, are gradually being displaced by the superior accuracy and efficiency of modern vision solutions. End-user demographics are shifting towards industries demanding higher precision and reduced waste, necessitating sophisticated inspection capabilities. Merger and acquisition (M&A) activity is moderate, with strategic consolidations aimed at expanding product portfolios and geographical reach. For instance, the acquisition of specialized software companies by larger vision system providers aims to enhance integrated solutions.

- Market Concentration: Moderate, with a few dominant players and a growing number of specialized solution providers.

- Technological Innovation Drivers: AI/ML for defect detection, high-speed imaging, 3D vision, and data analytics integration.

- Regulatory Frameworks: Product safety standards (e.g., ISO) and industry-specific compliance requirements are indirect growth drivers.

- Competitive Product Substitutes: Manual inspection, basic automation, and less sophisticated machine vision systems.

- End-User Demographics: Growth driven by industries requiring high precision, zero-defect policies, and increased automation.

- M&A Trends: Strategic acquisitions to broaden technology offerings and market presence, fostering ecosystem development.

Surface Vision & Inspection Equipment Industry Growth Trends & Insights

The Surface Vision & Inspection Equipment industry is poised for substantial expansion, projected to grow from an estimated $XX billion in 2025 to $XX billion by 2033, exhibiting a compelling Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025–2033). This robust growth is fueled by the escalating demand for enhanced product quality, increased manufacturing efficiency, and the relentless pursuit of zero-defect production across diverse industrial sectors. The historical period (2019–2024) witnessed a steady upward trajectory, laying the groundwork for accelerated adoption. The base year, 2025, marks a critical juncture where the integration of AI and deep learning into vision systems is gaining significant traction, driving adoption rates for more intelligent and adaptable inspection solutions. Technological disruptions, such as the advent of smarter cameras, advanced lighting techniques, and sophisticated algorithms for complex surface defect identification, are revolutionizing inspection capabilities. Consumer behavior shifts towards higher quality and safer products, particularly in the automotive, medical, and food & beverage sectors, are directly translating into increased investment in high-performance vision and inspection equipment. For example, the automotive industry's drive for autonomous driving technologies necessitates exceptionally precise defect detection in critical components. The adoption of Industry 4.0 principles, emphasizing interconnectedness and data-driven decision-making, further amplifies the need for comprehensive visual inspection integrated into the manufacturing workflow. The market penetration of advanced surface vision systems is steadily increasing, moving beyond traditional quality control to encompass real-time process monitoring and optimization. The parent market for industrial automation is a significant influencer, with advancements in robotics and IoT creating synergistic growth opportunities for surface vision and inspection. Conversely, the child market segments, such as specialized camera sensors and AI-driven software, are experiencing explosive growth as enabling technologies.

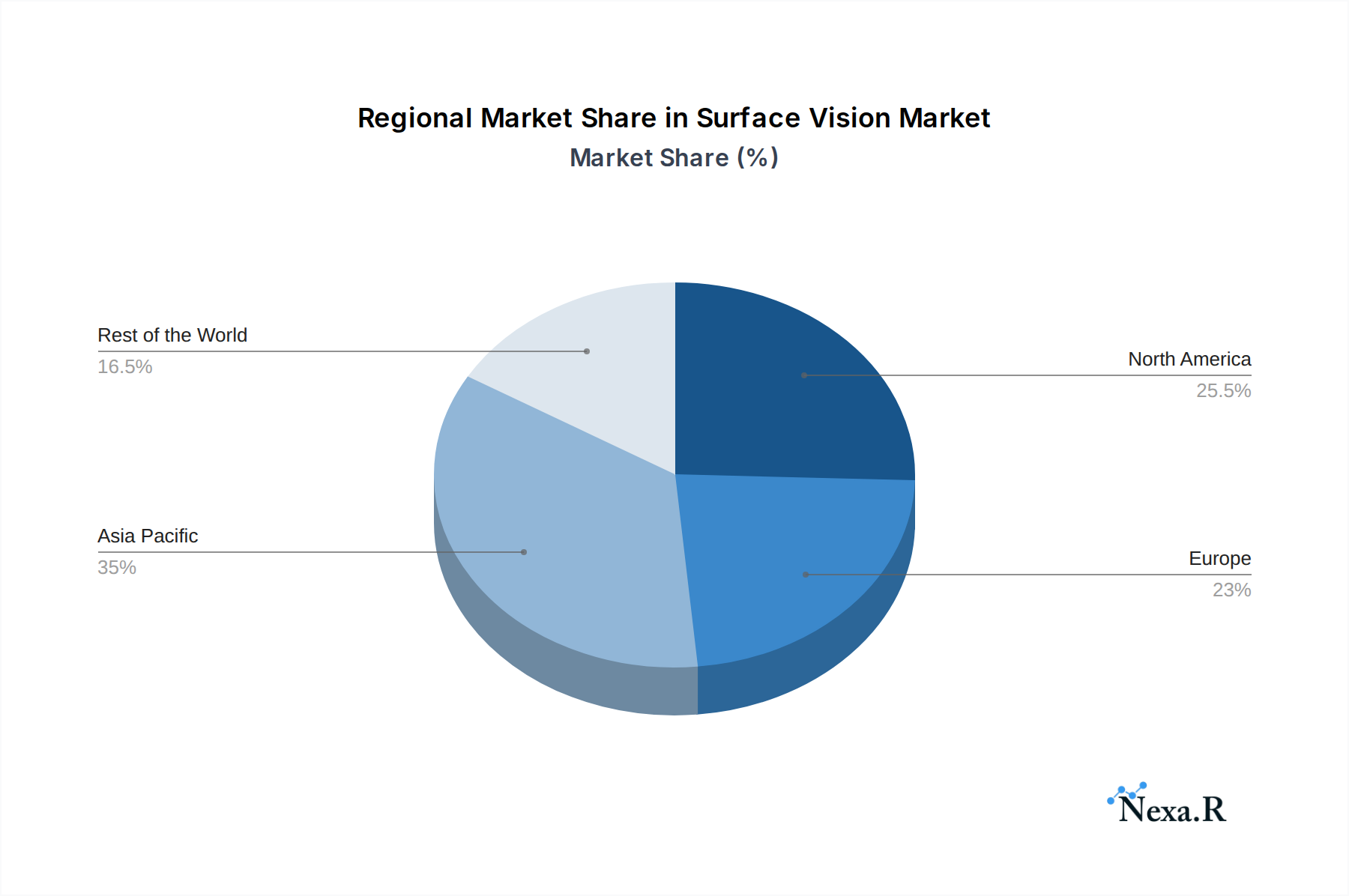

Dominant Regions, Countries, or Segments in Surface Vision & Inspection Equipment Industry

The Electrical & Electronics segment, particularly within the Asia-Pacific region, is currently the most dominant force driving the Surface Vision & Inspection Equipment industry. This dominance is underscored by the region's status as a global manufacturing hub for electronic components and finished goods, necessitating sophisticated quality control measures. China, in particular, stands out as a leading country due to its extensive manufacturing base, significant government investments in advanced manufacturing technologies, and a growing domestic market demanding high-quality electronics. The Camera component within the vision system is also a key driver of market growth, with continuous advancements in resolution, frame rates, and sensor technology enabling more precise and faster inspections. For instance, the increasing demand for high-resolution cameras in semiconductor inspection is a critical factor.

- Dominant Segment (Component): Camera: The increasing sophistication and miniaturization of camera technology, including high-resolution CMOS and CCD sensors, are crucial for detailed defect detection.

- Dominant Segment (Application): Electrical & Electronics: This sector's massive production volumes and stringent quality requirements for components like printed circuit boards (PCBs), semiconductors, and consumer electronics are major demand drivers.

- Dominant Region: Asia-Pacific, driven by its manufacturing prowess in electronics, automotive, and consumer goods.

- Leading Country: China, owing to its extensive manufacturing infrastructure, adoption of Industry 4.0 initiatives, and a large domestic market.

- Key Drivers in Asia-Pacific:

- Economic Policies: Government initiatives promoting advanced manufacturing and automation.

- Infrastructure: Well-developed industrial parks and logistics networks supporting manufacturing growth.

- Labor Costs: Rising labor costs incentivize automation and the adoption of vision inspection systems.

- Market Demand: Strong domestic and export demand for high-quality electronic products.

- Growth Potential in Electrical & Electronics: Continuous innovation in semiconductor manufacturing and the burgeoning 5G and IoT markets require ever-increasing levels of inspection precision.

- Market Share Insights: The Electrical & Electronics segment is estimated to hold approximately XX% of the global market share in 2025, with the Camera component contributing significantly to this.

Surface Vision & Inspection Equipment Industry Product Landscape

The Surface Vision & Inspection Equipment industry is characterized by a dynamic product landscape driven by continuous innovation. Advanced solutions now incorporate AI-powered algorithms for real-time defect classification and anomaly detection, significantly enhancing accuracy and reducing false positives. High-resolution cameras, specialized lighting equipment (e.g., structured light, UV illumination), and sophisticated optics are enabling the inspection of increasingly complex surfaces and microscopic defects. Products are tailored for specific applications, offering unique selling propositions such as ultra-fast inspection speeds for high-volume production lines in the Food & Beverages sector, or medical-grade compliance for the Pharmaceutical industry. Technological advancements are focused on creating integrated, smart vision systems that seamlessly connect with broader manufacturing execution systems (MES) for comprehensive quality management.

Key Drivers, Barriers & Challenges in Surface Vision & Inspection Equipment Industry

The Surface Vision & Inspection Equipment industry is propelled by several key drivers. The relentless pursuit of enhanced product quality and reduced manufacturing defects across industries like automotive and electronics is a primary catalyst. The growing adoption of Industry 4.0 and smart manufacturing initiatives, emphasizing automation and data-driven decision-making, necessitates sophisticated visual inspection capabilities. Furthermore, increasing regulatory compliance demands in sectors like pharmaceuticals and food & beverages are driving the need for highly reliable and traceable inspection processes.

However, the market also faces significant barriers and challenges. The high initial investment cost of advanced vision systems can be a restraint, particularly for small and medium-sized enterprises (SMEs). The complexity of integrating these systems into existing manufacturing workflows, requiring specialized expertise, presents another hurdle. Supply chain disruptions, impacting the availability of critical components like specialized sensors and processors, can lead to production delays and increased costs. Intense competition among established players and emerging startups also puts pressure on pricing and innovation cycles.

Emerging Opportunities in Surface Vision & Inspection Equipment Industry

Emerging opportunities in the Surface Vision & Inspection Equipment industry are abundant, particularly in the integration of advanced AI and machine learning for predictive quality assessment and anomaly detection. The growing demand for automated inspection in emerging industries such as renewable energy (solar panel inspection) and advanced materials presents untapped markets. Furthermore, the development of more portable and user-friendly vision inspection devices catering to field service and remote monitoring applications is an evolving consumer preference. The increasing need for cybersecurity in connected manufacturing environments also opens avenues for specialized secure vision solutions.

Growth Accelerators in the Surface Vision & Inspection Equipment Industry Industry

The Surface Vision & Inspection Equipment industry is experiencing significant growth acceleration driven by ongoing technological breakthroughs. The continuous evolution of AI and deep learning algorithms is enabling more accurate and efficient defect detection, moving beyond traditional rule-based systems. Strategic partnerships between hardware manufacturers and software developers are fostering the creation of comprehensive, end-to-end inspection solutions. Furthermore, market expansion strategies focusing on emerging economies and niche applications within established sectors are creating new avenues for growth. The increasing adoption of robotics in manufacturing also acts as a powerful accelerator, as vision systems are critical for robotic guidance and quality assurance.

Key Players Shaping the Surface Vision & Inspection Equipment Industry Market

- Matrox Imaging Ltd

- Keyence Corporation

- Shenzhen Sipotek Technology Co Ltd

- Isra Vision AG

- Cognex Corporation

- Stemmer Imaging AG

- AMETEK Surface Vision

- Omron Corporation

- Comvis AG

- Daitron Inc

- Flexfilm Ltd

- Edmund Scientific Corporation

- Panasonic Corporation

Notable Milestones in Surface Vision & Inspection Equipment Industry Sector

- 2021: Cognex Corporation launches a new generation of AI-powered vision systems for complex inspection tasks.

- 2022: Keyence Corporation expands its product line with advanced 3D vision sensors for enhanced surface profiling.

- 2022: Isra Vision AG announces a strategic partnership to integrate its inspection solutions with robotic automation platforms.

- 2023: AMETEK Surface Vision introduces innovative lighting solutions for detecting subtle surface defects in demanding environments.

- 2023: Stemmer Imaging AG enhances its software offerings with advanced machine learning libraries for image analysis.

- 2024: Omron Corporation unveils a new series of compact and high-performance vision controllers for embedded applications.

- 2024: Matrox Imaging Ltd launches enhanced imaging libraries optimized for deep learning inference on embedded systems.

In-Depth Surface Vision & Inspection Equipment Industry Market Outlook

The future outlook for the Surface Vision & Inspection Equipment industry is exceptionally bright, driven by the increasing imperative for automation, quality control, and efficiency across global manufacturing landscapes. Growth accelerators such as advancements in artificial intelligence and the proliferation of Industry 4.0 principles will continue to fuel demand. Strategic partnerships and market expansion into nascent applications and geographical regions represent significant opportunities for sustained expansion. The industry's ability to adapt to evolving technological paradigms and address the persistent need for superior product quality positions it for robust and long-term growth in the coming years.

Surface Vision & Inspection Equipment Industry Segmentation

-

1. Component

- 1.1. Camera

- 1.2. Lighting Equipment

- 1.3. Optics

- 1.4. Other Components

-

2. Application

- 2.1. Automotive

- 2.2. Electrical & Electronics

- 2.3. Medical & Pharmaceuticals

- 2.4. Food & Beverages

- 2.5. Postal & Logistics

- 2.6. Other Applications

Surface Vision & Inspection Equipment Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

Surface Vision & Inspection Equipment Industry Regional Market Share

Geographic Coverage of Surface Vision & Inspection Equipment Industry

Surface Vision & Inspection Equipment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.56% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Camera

- 5.1.2. Lighting Equipment

- 5.1.3. Optics

- 5.1.4. Other Components

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Automotive

- 5.2.2. Electrical & Electronics

- 5.2.3. Medical & Pharmaceuticals

- 5.2.4. Food & Beverages

- 5.2.5. Postal & Logistics

- 5.2.6. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Global Surface Vision & Inspection Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Camera

- 6.1.2. Lighting Equipment

- 6.1.3. Optics

- 6.1.4. Other Components

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Automotive

- 6.2.2. Electrical & Electronics

- 6.2.3. Medical & Pharmaceuticals

- 6.2.4. Food & Beverages

- 6.2.5. Postal & Logistics

- 6.2.6. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. North America Surface Vision & Inspection Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Camera

- 7.1.2. Lighting Equipment

- 7.1.3. Optics

- 7.1.4. Other Components

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Automotive

- 7.2.2. Electrical & Electronics

- 7.2.3. Medical & Pharmaceuticals

- 7.2.4. Food & Beverages

- 7.2.5. Postal & Logistics

- 7.2.6. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. Europe Surface Vision & Inspection Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Camera

- 8.1.2. Lighting Equipment

- 8.1.3. Optics

- 8.1.4. Other Components

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Automotive

- 8.2.2. Electrical & Electronics

- 8.2.3. Medical & Pharmaceuticals

- 8.2.4. Food & Beverages

- 8.2.5. Postal & Logistics

- 8.2.6. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Asia Pacific Surface Vision & Inspection Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Camera

- 9.1.2. Lighting Equipment

- 9.1.3. Optics

- 9.1.4. Other Components

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Automotive

- 9.2.2. Electrical & Electronics

- 9.2.3. Medical & Pharmaceuticals

- 9.2.4. Food & Beverages

- 9.2.5. Postal & Logistics

- 9.2.6. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Rest of the World Surface Vision & Inspection Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Camera

- 10.1.2. Lighting Equipment

- 10.1.3. Optics

- 10.1.4. Other Components

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Automotive

- 10.2.2. Electrical & Electronics

- 10.2.3. Medical & Pharmaceuticals

- 10.2.4. Food & Beverages

- 10.2.5. Postal & Logistics

- 10.2.6. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Matrox Imaging Ltd

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Keyence Corporation

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Shenzhen Sipotek Technology Co Ltd

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Isra Vision AG

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Cognex Corporation

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Stemmer Imaging AG

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 AMETEK Surface Vision

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Omron Corporation

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Comvis AG*List Not Exhaustive

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Daitron Inc

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Flexfilm Ltd

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Edmund Scientific Corporation

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 Panasonic Corporation

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.1 Matrox Imaging Ltd

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Surface Vision & Inspection Equipment Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Surface Vision & Inspection Equipment Industry Revenue (billion), by Component 2025 & 2033

- Figure 3: North America Surface Vision & Inspection Equipment Industry Revenue Share (%), by Component 2025 & 2033

- Figure 4: North America Surface Vision & Inspection Equipment Industry Revenue (billion), by Application 2025 & 2033

- Figure 5: North America Surface Vision & Inspection Equipment Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Surface Vision & Inspection Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Surface Vision & Inspection Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Surface Vision & Inspection Equipment Industry Revenue (billion), by Component 2025 & 2033

- Figure 9: Europe Surface Vision & Inspection Equipment Industry Revenue Share (%), by Component 2025 & 2033

- Figure 10: Europe Surface Vision & Inspection Equipment Industry Revenue (billion), by Application 2025 & 2033

- Figure 11: Europe Surface Vision & Inspection Equipment Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: Europe Surface Vision & Inspection Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Surface Vision & Inspection Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Surface Vision & Inspection Equipment Industry Revenue (billion), by Component 2025 & 2033

- Figure 15: Asia Pacific Surface Vision & Inspection Equipment Industry Revenue Share (%), by Component 2025 & 2033

- Figure 16: Asia Pacific Surface Vision & Inspection Equipment Industry Revenue (billion), by Application 2025 & 2033

- Figure 17: Asia Pacific Surface Vision & Inspection Equipment Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: Asia Pacific Surface Vision & Inspection Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Surface Vision & Inspection Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Surface Vision & Inspection Equipment Industry Revenue (billion), by Component 2025 & 2033

- Figure 21: Rest of the World Surface Vision & Inspection Equipment Industry Revenue Share (%), by Component 2025 & 2033

- Figure 22: Rest of the World Surface Vision & Inspection Equipment Industry Revenue (billion), by Application 2025 & 2033

- Figure 23: Rest of the World Surface Vision & Inspection Equipment Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Rest of the World Surface Vision & Inspection Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Rest of the World Surface Vision & Inspection Equipment Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Surface Vision & Inspection Equipment Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 2: Global Surface Vision & Inspection Equipment Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global Surface Vision & Inspection Equipment Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Surface Vision & Inspection Equipment Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 5: Global Surface Vision & Inspection Equipment Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global Surface Vision & Inspection Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Surface Vision & Inspection Equipment Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 8: Global Surface Vision & Inspection Equipment Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 9: Global Surface Vision & Inspection Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Surface Vision & Inspection Equipment Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 11: Global Surface Vision & Inspection Equipment Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 12: Global Surface Vision & Inspection Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Surface Vision & Inspection Equipment Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 14: Global Surface Vision & Inspection Equipment Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 15: Global Surface Vision & Inspection Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Surface Vision & Inspection Equipment Industry?

The projected CAGR is approximately 14.56%.

2. Which companies are prominent players in the Surface Vision & Inspection Equipment Industry?

Key companies in the market include Matrox Imaging Ltd, Keyence Corporation, Shenzhen Sipotek Technology Co Ltd, Isra Vision AG, Cognex Corporation, Stemmer Imaging AG, AMETEK Surface Vision, Omron Corporation, Comvis AG*List Not Exhaustive, Daitron Inc, Flexfilm Ltd, Edmund Scientific Corporation, Panasonic Corporation.

3. What are the main segments of the Surface Vision & Inspection Equipment Industry?

The market segments include Component, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.86 billion as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Need for Better Manufacturing Production Capacity at Reduced Cost; Growing Demand for Qualitative Products; Increasing Adoption of Industrial 4.0 and IoT.

6. What are the notable trends driving market growth?

Camera Segment is expected to Hold the Largest Market Size during the Forecast Period.

7. Are there any restraints impacting market growth?

; Lack of Skilled Labor.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Surface Vision & Inspection Equipment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Surface Vision & Inspection Equipment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Surface Vision & Inspection Equipment Industry?

To stay informed about further developments, trends, and reports in the Surface Vision & Inspection Equipment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence