Key Insights

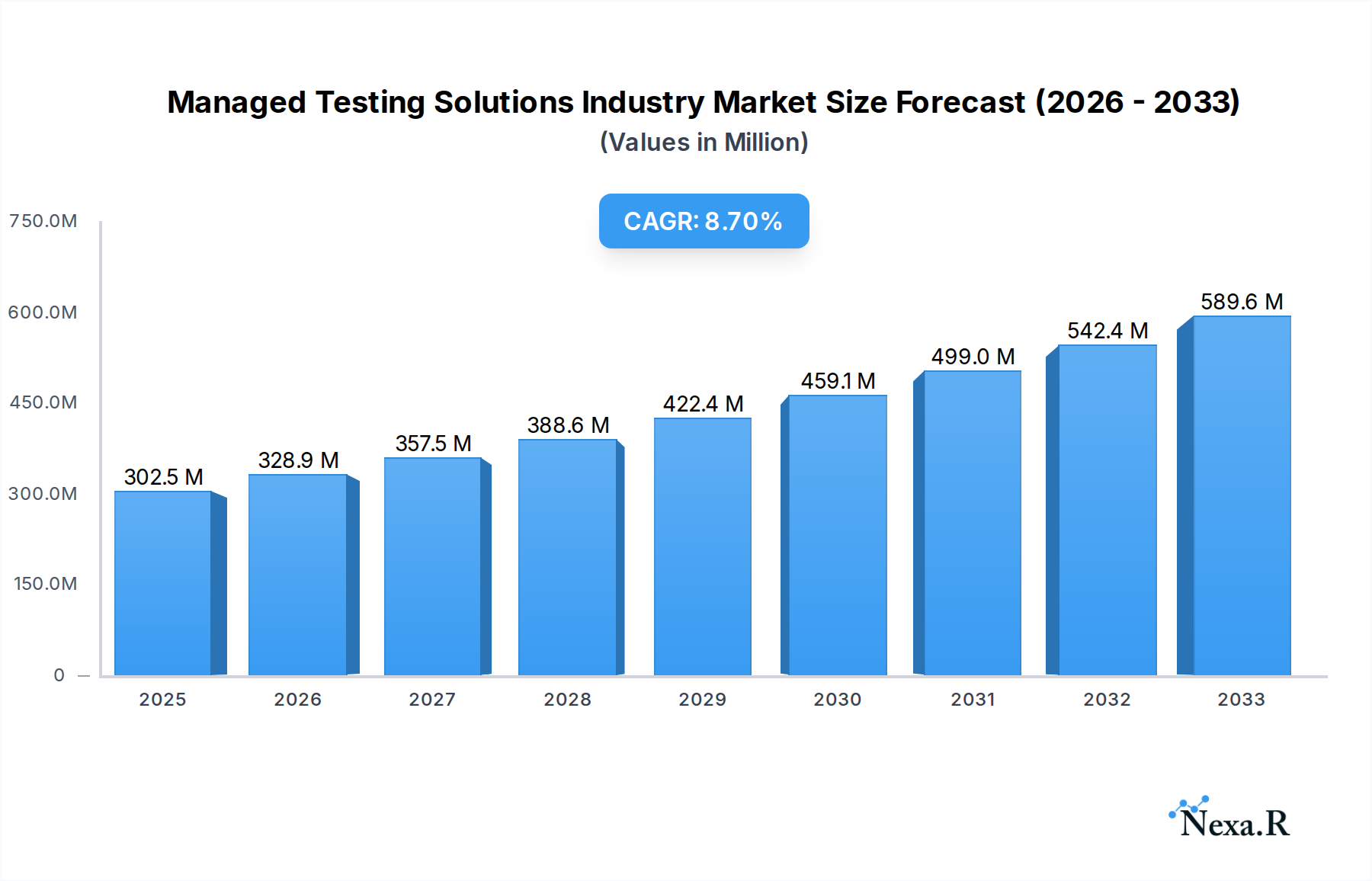

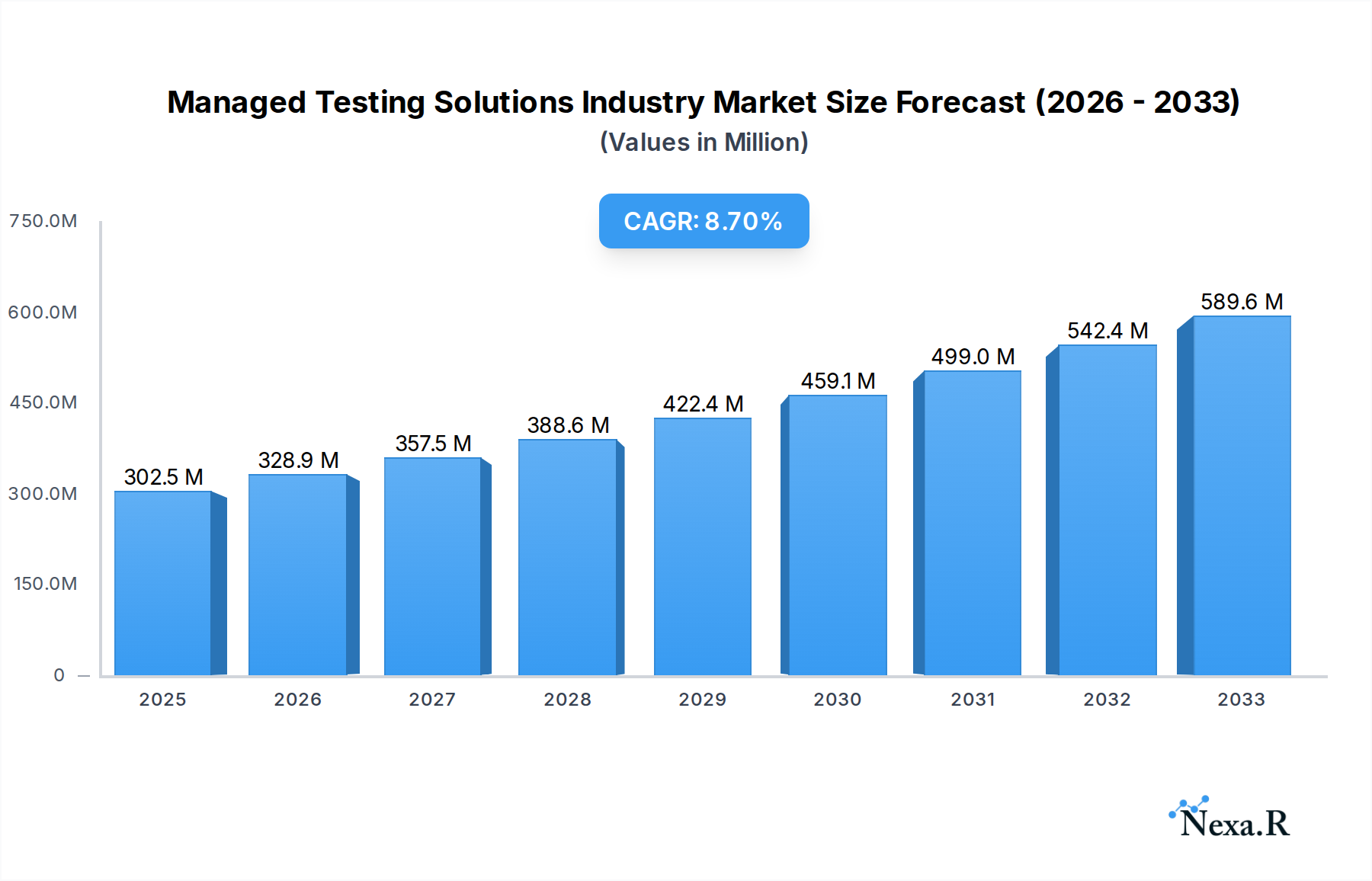

The Managed Testing Solutions industry is poised for significant expansion, with the market size projected to reach USD 302.53 Million and exhibit a robust Compound Annual Growth Rate (CAGR) of 8.70% during the forecast period of 2025-2033. This growth is primarily propelled by an increasing demand for high-quality software and applications across diverse industries, coupled with the escalating complexity of IT environments. Businesses are increasingly recognizing the strategic advantage of outsourcing their testing functions to specialized managed service providers to ensure cost-efficiency, scalability, and access to cutting-edge testing expertise and tools. The rise of digital transformation initiatives and the need to accelerate time-to-market for new products and services are further fueling this market trajectory. Furthermore, the growing adoption of Agile and DevOps methodologies necessitates continuous testing, which managed solutions are well-equipped to provide, thereby driving the market forward.

Managed Testing Solutions Industry Market Size (In Million)

The market landscape is characterized by a dynamic interplay of key drivers, emerging trends, and certain restraints. Key drivers include the escalating need for cost optimization in IT operations, the shortage of skilled testing professionals within organizations, and the imperative to comply with stringent regulatory standards in sectors like BFSI and Healthcare. Emerging trends such as the proliferation of AI and ML in test automation, the growing adoption of cloud-based testing solutions, and the increasing focus on security testing and performance testing are shaping the industry's evolution. While the market demonstrates strong growth potential, it faces restraints such as concerns around data security and privacy when outsourcing, potential vendor lock-in, and the challenge of finding providers with deep domain expertise for niche industries. Nevertheless, the overarching benefits of managed testing solutions, including enhanced test coverage, reduced operational overhead, and improved product quality, are expected to outweigh these challenges, leading to sustained market growth.

Managed Testing Solutions Industry Company Market Share

Managed Testing Solutions Industry Report Description

**Unlock the future of quality assurance with our comprehensive *Managed Testing Solutions Industry* report. This in-depth analysis, spanning from 2019 to 2033, provides critical insights into market dynamics, growth trends, regional dominance, and the competitive landscape of the global managed testing services market. With a base year of 2025 and a robust forecast period of 2025–2033, this report is your essential guide to navigating the evolving software testing services, quality assurance, and managed QA sectors. Discover market segmentation by delivery model (Onshore, Offshore), organization size (Small & Medium Enterprises, Large Enterprises), and end-user verticals (Healthcare, BFSI, Telecom and IT, Retail, Government). Leverage actionable intelligence to capitalize on automation testing, API testing, and functional testing opportunities.

Managed Testing Solutions Industry Market Dynamics & Structure

The Managed Testing Solutions Industry is characterized by a moderate market concentration, with several key players vying for dominance. Technological innovation is a primary driver, fueled by the increasing adoption of Artificial Intelligence (AI) in testing, the demand for DevOps and Agile methodologies, and the growing complexity of software applications. Regulatory frameworks, particularly in sectors like BFSI and Healthcare, are also shaping the market by mandating stringent quality standards and compliance. Competitive product substitutes are emerging, including in-house testing teams and open-source testing tools, but dedicated managed testing solutions offer specialized expertise and scalability. End-user demographics are shifting towards organizations seeking cost-efficiency, faster time-to-market, and enhanced test coverage. Mergers and acquisitions (M&A) are a significant trend, with companies consolidating to expand service portfolios and geographic reach. For instance, the M&A volume in the broader IT services sector, which includes managed testing, saw approximately $25 million in disclosed deal value in the first half of 2024. Barriers to innovation include the high cost of advanced testing tools and the scarcity of skilled testing professionals.

- Market Concentration: Moderate, with leading players holding a significant, but not overwhelming, share.

- Technological Innovation Drivers: AI-powered testing, IoT testing, cloud testing, mobile testing, and shift-left testing methodologies.

- Regulatory Frameworks: GDPR, HIPAA, and industry-specific compliance standards necessitate robust testing.

- Competitive Product Substitutes: In-house testing teams, open-source tools, and hybrid testing models.

- End-User Demographics: Growing demand from SMEs seeking to optimize testing costs and large enterprises looking to accelerate digital transformation.

- M&A Trends: Consolidation for market expansion, talent acquisition, and service diversification.

- Innovation Barriers: Talent shortage, integration complexities with existing systems, and evolving technology landscapes.

Managed Testing Solutions Industry Growth Trends & Insights

The Managed Testing Solutions Industry is poised for significant expansion, projected to grow from an estimated $25,000 million in 2025 to over $50,000 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 7.5% during the forecast period. This growth is propelled by the accelerating digital transformation across all industries and the increasing reliance on sophisticated software applications. Adoption rates for specialized managed testing services are steadily rising as organizations recognize the benefits of outsourcing complex QA processes to gain access to specialized expertise, advanced tools, and a more agile testing approach. Technological disruptions, such as the widespread adoption of AI and machine learning in test automation, are fundamentally reshaping how testing is performed, leading to enhanced efficiency and accuracy. For instance, AI-driven test case generation and predictive analytics are becoming mainstream. Consumer behavior shifts are also playing a crucial role; businesses are demanding faster release cycles and higher quality, pushing for more efficient and effective testing strategies. The penetration of managed testing solutions is expected to increase from 30% in 2025 to over 45% by 2033 as more companies embrace the strategic advantages of these services. The increasing complexity of software, the proliferation of connected devices, and the growing emphasis on cybersecurity are further fueling the demand for comprehensive and specialized managed testing services. The market is witnessing a paradigm shift from traditional functional testing to proactive quality engineering, where testing is integrated throughout the software development lifecycle.

Dominant Regions, Countries, or Segments in Managed Testing Solutions Industry

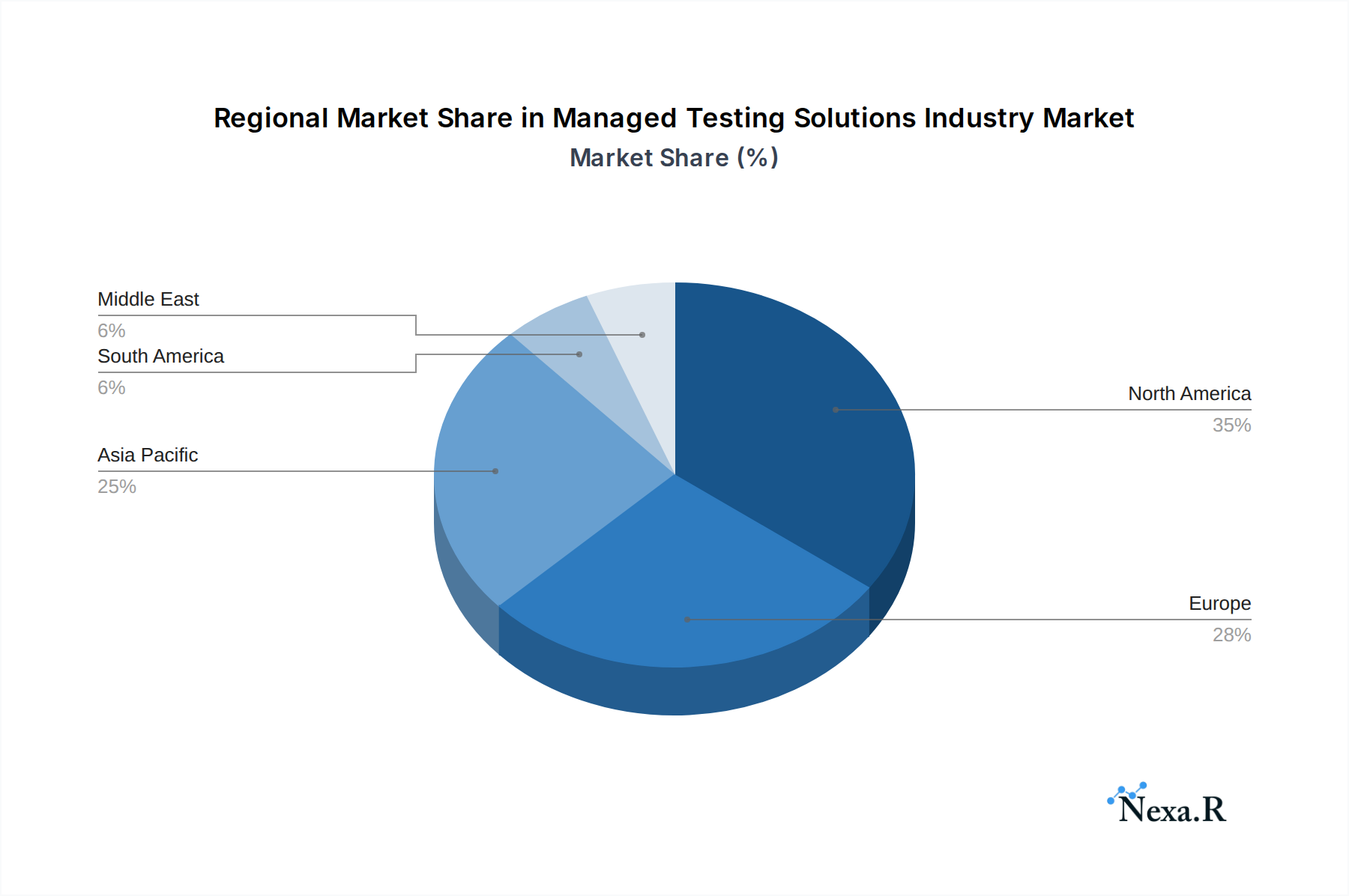

The North America region is currently the dominant force in the Managed Testing Solutions Industry, driven by its robust technological infrastructure, high adoption of advanced testing methodologies, and the presence of major IT hubs. The United States, in particular, leads with a significant market share due to its large enterprises in BFSI, Healthcare, and Telecom and IT sectors that are at the forefront of digital innovation and actively seek managed testing services to maintain a competitive edge. The Offshore delivery model is another critical segment driving market growth, especially from regions like India and Eastern Europe. This model offers significant cost advantages, enabling organizations to achieve end-to-end testing services at a reduced price point. The June 2023 engagement of TestingXperts (Tx) with an AI-based candidate screening services provider, utilizing an offshore delivery model for comprehensive API, functional, and automation testing, exemplifies this trend. The BFSI sector is a major end-user vertical, contributing substantially to market revenue, given the critical need for security, compliance, and reliability in financial applications. The Telecom and IT sector also represents a substantial segment, fueled by rapid technological advancements and the demand for continuous integration and delivery.

- Dominant Region: North America (USA, Canada).

- Key Drivers: High R&D investment, strong digital adoption, presence of global technology leaders.

- Market Share Contribution: Approximately 40% of the global market.

- Growth Potential: Steady growth driven by cloud adoption and AI integration.

- Dominant Delivery Model: Offshore.

- Key Drivers: Cost-effectiveness, access to a large talent pool, 24/7 testing capabilities.

- Market Share Contribution: Approximately 55% of the global market.

- Growth Potential: Sustained growth due to ongoing cost optimization initiatives.

- Dominant End-user Vertical: BFSI (Banking, Financial Services, and Insurance).

- Key Drivers: Stringent regulatory compliance, high security requirements, need for flawless application performance.

- Market Share Contribution: Approximately 25% of the global market.

- Growth Potential: Significant growth driven by digital banking and fintech innovation.

- Key Segment: Large Enterprises.

- Drivers: Complex IT landscapes, need for scalable testing solutions, focus on digital transformation.

- Market Share: Approximately 60% of the managed testing market.

Managed Testing Solutions Industry Product Landscape

The Managed Testing Solutions Industry product landscape is evolving rapidly, focusing on intelligent automation, AI-driven insights, and end-to-end quality engineering. Innovations include AI-powered test case generation, predictive analytics for defect identification, and self-healing automation scripts, significantly enhancing test efficiency and accuracy. Performance metrics are increasingly optimized through integrated performance and security testing within managed service offerings. Unique selling propositions revolve around specialized domain expertise, adherence to global quality standards, and the ability to seamlessly integrate with client DevOps pipelines. Technological advancements are enabling more comprehensive test coverage across web, mobile, cloud, and IoT platforms, ensuring a superior end-user experience.

Key Drivers, Barriers & Challenges in Managed Testing Solutions Industry

Key Drivers:

- Digital Transformation: The overarching push for digital adoption across all sectors fuels the need for robust and efficient testing.

- Cost Optimization: Outsourcing testing to managed service providers offers significant cost savings compared to building in-house capabilities.

- Demand for Quality & Speed: Enterprises require faster release cycles and higher application quality, which managed testing excels at delivering.

- Technological Advancements: AI, ML, and advanced automation tools enable more sophisticated and efficient testing strategies.

- Regulatory Compliance: Stringent industry regulations necessitate comprehensive testing to ensure adherence to standards.

Barriers & Challenges:

- Talent Shortage: A global scarcity of skilled testing professionals can hinder service delivery and innovation.

- Data Security Concerns: Organizations are often wary of sharing sensitive data with third-party providers, necessitating robust security protocols.

- Integration Complexity: Integrating managed testing solutions with existing client IT infrastructures can be challenging.

- Vendor Lock-in Perceptions: Companies may fear becoming overly reliant on a single vendor.

- Economic Downturns: Economic instability can lead to budget cuts in IT spending, impacting demand for managed services. The global IT services market experienced a marginal slowdown in growth by approximately 1.5% in Q1 2024 due to economic uncertainties.

Emerging Opportunities in Managed Testing Solutions Industry

Emerging opportunities within the Managed Testing Solutions Industry lie in the burgeoning demand for specialized testing in niche areas. The rapid growth of the Internet of Things (IoT) ecosystem presents a significant opportunity for comprehensive IoT testing services, ensuring device compatibility, security, and data integrity. The increasing adoption of cloud-native applications and microservices architectures requires sophisticated cloud testing and containerization testing expertise. Furthermore, the rise of the metaverse and extended reality (XR) technologies will necessitate specialized testing for immersive experiences, focusing on performance, user interaction, and sensory feedback. Untapped markets in emerging economies, with their accelerating digital adoption, also present substantial growth potential for managed testing providers. The continuous evolution of cybersecurity threats also creates an ongoing demand for advanced security testing services as part of managed solutions.

Growth Accelerators in the Managed Testing Solutions Industry Industry

Several growth accelerators are propelling the Managed Testing Solutions Industry forward. The pervasive integration of Artificial Intelligence and Machine Learning into testing processes, enabling predictive defect analysis and intelligent automation, is a significant catalyst. Strategic partnerships between managed service providers and technology vendors are crucial for accessing cutting-edge tools and expanding service portfolios. Market expansion strategies, particularly into underserved geographic regions and emerging industry verticals like the gaming and esports sector, are driving revenue growth. The increasing emphasis on digital transformation initiatives by enterprises, coupled with the need for accelerated product development cycles, directly translates into higher demand for efficient and scalable managed testing solutions. The growing maturity of offshore delivery models, enhanced by improved communication technologies and robust project management frameworks, also contributes significantly to sustained growth.

Key Players Shaping the Managed Testing Solutions Industry Market

- QualiTest

- Testhouse Ltd

- Infosys Limited

- Accenture Plc

- Wipro Limited

- Cognizant

- TATA Consultancy Services Limited

- Hexaware Technologies

- Capgemini SE

- International Business Machines Corporation (IBM)

Notable Milestones in Managed Testing Solutions Industry Sector

- July 2023: TestingXperts (Tx) announced further expansion into Canada, strengthening its presence in the North American market and addressing the growing demand for Quality Engineering and software testing services.

- June 2023: TestingXperts (Tx) was chosen as a QA partner by an AI-based candidate screening services provider, opting for an offshore delivery model to provide end-to-end API, functional, database, and automation testing for the client’s automated talent screening application.

In-Depth Managed Testing Solutions Industry Market Outlook

The future outlook for the Managed Testing Solutions Industry is exceptionally promising, driven by sustained digital transformation and the ever-increasing demand for high-quality, secure, and performant software. Growth accelerators such as AI integration, strategic partnerships, and market expansion into new verticals and geographies will continue to fuel the industry's trajectory. The increasing complexity of software systems, coupled with the imperative for faster time-to-market, ensures that the need for specialized managed testing services will only intensify. Organizations will increasingly rely on outsourcing to gain access to cutting-edge testing technologies and specialized expertise, driving further market penetration. The industry is set to witness a significant evolution towards proactive quality engineering and continuous testing embedded within development lifecycles, presenting substantial strategic opportunities for growth and innovation.

Managed Testing Solutions Industry Segmentation

-

1. Type of Delivery Model

- 1.1. Onshore

- 1.2. Offshore

-

2. Size of Organization

- 2.1. Small & Medium Enterprises

- 2.2. Large Enterprises

-

3. End-user Vertical

- 3.1. Healthcare

- 3.2. BFSI

- 3.3. Telecom and IT

- 3.4. Retail

- 3.5. Government

- 3.6. Other End-user Verticals

Managed Testing Solutions Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. South America

- 5. Middle East

Managed Testing Solutions Industry Regional Market Share

Geographic Coverage of Managed Testing Solutions Industry

Managed Testing Solutions Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.70% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type of Delivery Model

- 5.1.1. Onshore

- 5.1.2. Offshore

- 5.2. Market Analysis, Insights and Forecast - by Size of Organization

- 5.2.1. Small & Medium Enterprises

- 5.2.2. Large Enterprises

- 5.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.3.1. Healthcare

- 5.3.2. BFSI

- 5.3.3. Telecom and IT

- 5.3.4. Retail

- 5.3.5. Government

- 5.3.6. Other End-user Verticals

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. South America

- 5.4.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Type of Delivery Model

- 6. Global Managed Testing Solutions Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type of Delivery Model

- 6.1.1. Onshore

- 6.1.2. Offshore

- 6.2. Market Analysis, Insights and Forecast - by Size of Organization

- 6.2.1. Small & Medium Enterprises

- 6.2.2. Large Enterprises

- 6.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.3.1. Healthcare

- 6.3.2. BFSI

- 6.3.3. Telecom and IT

- 6.3.4. Retail

- 6.3.5. Government

- 6.3.6. Other End-user Verticals

- 6.1. Market Analysis, Insights and Forecast - by Type of Delivery Model

- 7. North America Managed Testing Solutions Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type of Delivery Model

- 7.1.1. Onshore

- 7.1.2. Offshore

- 7.2. Market Analysis, Insights and Forecast - by Size of Organization

- 7.2.1. Small & Medium Enterprises

- 7.2.2. Large Enterprises

- 7.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 7.3.1. Healthcare

- 7.3.2. BFSI

- 7.3.3. Telecom and IT

- 7.3.4. Retail

- 7.3.5. Government

- 7.3.6. Other End-user Verticals

- 7.1. Market Analysis, Insights and Forecast - by Type of Delivery Model

- 8. Europe Managed Testing Solutions Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type of Delivery Model

- 8.1.1. Onshore

- 8.1.2. Offshore

- 8.2. Market Analysis, Insights and Forecast - by Size of Organization

- 8.2.1. Small & Medium Enterprises

- 8.2.2. Large Enterprises

- 8.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 8.3.1. Healthcare

- 8.3.2. BFSI

- 8.3.3. Telecom and IT

- 8.3.4. Retail

- 8.3.5. Government

- 8.3.6. Other End-user Verticals

- 8.1. Market Analysis, Insights and Forecast - by Type of Delivery Model

- 9. Asia Pacific Managed Testing Solutions Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type of Delivery Model

- 9.1.1. Onshore

- 9.1.2. Offshore

- 9.2. Market Analysis, Insights and Forecast - by Size of Organization

- 9.2.1. Small & Medium Enterprises

- 9.2.2. Large Enterprises

- 9.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 9.3.1. Healthcare

- 9.3.2. BFSI

- 9.3.3. Telecom and IT

- 9.3.4. Retail

- 9.3.5. Government

- 9.3.6. Other End-user Verticals

- 9.1. Market Analysis, Insights and Forecast - by Type of Delivery Model

- 10. South America Managed Testing Solutions Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type of Delivery Model

- 10.1.1. Onshore

- 10.1.2. Offshore

- 10.2. Market Analysis, Insights and Forecast - by Size of Organization

- 10.2.1. Small & Medium Enterprises

- 10.2.2. Large Enterprises

- 10.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 10.3.1. Healthcare

- 10.3.2. BFSI

- 10.3.3. Telecom and IT

- 10.3.4. Retail

- 10.3.5. Government

- 10.3.6. Other End-user Verticals

- 10.1. Market Analysis, Insights and Forecast - by Type of Delivery Model

- 11. Middle East Managed Testing Solutions Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type of Delivery Model

- 11.1.1. Onshore

- 11.1.2. Offshore

- 11.2. Market Analysis, Insights and Forecast - by Size of Organization

- 11.2.1. Small & Medium Enterprises

- 11.2.2. Large Enterprises

- 11.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 11.3.1. Healthcare

- 11.3.2. BFSI

- 11.3.3. Telecom and IT

- 11.3.4. Retail

- 11.3.5. Government

- 11.3.6. Other End-user Verticals

- 11.1. Market Analysis, Insights and Forecast - by Type of Delivery Model

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 QualiTest

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Testhouse Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Infosys Limited

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Accenture Plc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Wipro Limited

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Cognizant

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 TATA Consultancy Services Limited

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Hexaware Technologies

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Capgemini SE

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 International Business Machines Corporation (IBM)

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 QualiTest

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Managed Testing Solutions Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Managed Testing Solutions Industry Revenue (Million), by Type of Delivery Model 2025 & 2033

- Figure 3: North America Managed Testing Solutions Industry Revenue Share (%), by Type of Delivery Model 2025 & 2033

- Figure 4: North America Managed Testing Solutions Industry Revenue (Million), by Size of Organization 2025 & 2033

- Figure 5: North America Managed Testing Solutions Industry Revenue Share (%), by Size of Organization 2025 & 2033

- Figure 6: North America Managed Testing Solutions Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 7: North America Managed Testing Solutions Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 8: North America Managed Testing Solutions Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Managed Testing Solutions Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Managed Testing Solutions Industry Revenue (Million), by Type of Delivery Model 2025 & 2033

- Figure 11: Europe Managed Testing Solutions Industry Revenue Share (%), by Type of Delivery Model 2025 & 2033

- Figure 12: Europe Managed Testing Solutions Industry Revenue (Million), by Size of Organization 2025 & 2033

- Figure 13: Europe Managed Testing Solutions Industry Revenue Share (%), by Size of Organization 2025 & 2033

- Figure 14: Europe Managed Testing Solutions Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 15: Europe Managed Testing Solutions Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 16: Europe Managed Testing Solutions Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Managed Testing Solutions Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Managed Testing Solutions Industry Revenue (Million), by Type of Delivery Model 2025 & 2033

- Figure 19: Asia Pacific Managed Testing Solutions Industry Revenue Share (%), by Type of Delivery Model 2025 & 2033

- Figure 20: Asia Pacific Managed Testing Solutions Industry Revenue (Million), by Size of Organization 2025 & 2033

- Figure 21: Asia Pacific Managed Testing Solutions Industry Revenue Share (%), by Size of Organization 2025 & 2033

- Figure 22: Asia Pacific Managed Testing Solutions Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 23: Asia Pacific Managed Testing Solutions Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 24: Asia Pacific Managed Testing Solutions Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Managed Testing Solutions Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Managed Testing Solutions Industry Revenue (Million), by Type of Delivery Model 2025 & 2033

- Figure 27: South America Managed Testing Solutions Industry Revenue Share (%), by Type of Delivery Model 2025 & 2033

- Figure 28: South America Managed Testing Solutions Industry Revenue (Million), by Size of Organization 2025 & 2033

- Figure 29: South America Managed Testing Solutions Industry Revenue Share (%), by Size of Organization 2025 & 2033

- Figure 30: South America Managed Testing Solutions Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 31: South America Managed Testing Solutions Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 32: South America Managed Testing Solutions Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: South America Managed Testing Solutions Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East Managed Testing Solutions Industry Revenue (Million), by Type of Delivery Model 2025 & 2033

- Figure 35: Middle East Managed Testing Solutions Industry Revenue Share (%), by Type of Delivery Model 2025 & 2033

- Figure 36: Middle East Managed Testing Solutions Industry Revenue (Million), by Size of Organization 2025 & 2033

- Figure 37: Middle East Managed Testing Solutions Industry Revenue Share (%), by Size of Organization 2025 & 2033

- Figure 38: Middle East Managed Testing Solutions Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 39: Middle East Managed Testing Solutions Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 40: Middle East Managed Testing Solutions Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Middle East Managed Testing Solutions Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Managed Testing Solutions Industry Revenue Million Forecast, by Type of Delivery Model 2020 & 2033

- Table 2: Global Managed Testing Solutions Industry Revenue Million Forecast, by Size of Organization 2020 & 2033

- Table 3: Global Managed Testing Solutions Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 4: Global Managed Testing Solutions Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Managed Testing Solutions Industry Revenue Million Forecast, by Type of Delivery Model 2020 & 2033

- Table 6: Global Managed Testing Solutions Industry Revenue Million Forecast, by Size of Organization 2020 & 2033

- Table 7: Global Managed Testing Solutions Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 8: Global Managed Testing Solutions Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Managed Testing Solutions Industry Revenue Million Forecast, by Type of Delivery Model 2020 & 2033

- Table 10: Global Managed Testing Solutions Industry Revenue Million Forecast, by Size of Organization 2020 & 2033

- Table 11: Global Managed Testing Solutions Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 12: Global Managed Testing Solutions Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Managed Testing Solutions Industry Revenue Million Forecast, by Type of Delivery Model 2020 & 2033

- Table 14: Global Managed Testing Solutions Industry Revenue Million Forecast, by Size of Organization 2020 & 2033

- Table 15: Global Managed Testing Solutions Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 16: Global Managed Testing Solutions Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: Global Managed Testing Solutions Industry Revenue Million Forecast, by Type of Delivery Model 2020 & 2033

- Table 18: Global Managed Testing Solutions Industry Revenue Million Forecast, by Size of Organization 2020 & 2033

- Table 19: Global Managed Testing Solutions Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 20: Global Managed Testing Solutions Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global Managed Testing Solutions Industry Revenue Million Forecast, by Type of Delivery Model 2020 & 2033

- Table 22: Global Managed Testing Solutions Industry Revenue Million Forecast, by Size of Organization 2020 & 2033

- Table 23: Global Managed Testing Solutions Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 24: Global Managed Testing Solutions Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Managed Testing Solutions Industry?

The projected CAGR is approximately 8.70%.

2. Which companies are prominent players in the Managed Testing Solutions Industry?

Key companies in the market include QualiTest, Testhouse Ltd, Infosys Limited, Accenture Plc, Wipro Limited, Cognizant, TATA Consultancy Services Limited, Hexaware Technologies, Capgemini SE, International Business Machines Corporation (IBM).

3. What are the main segments of the Managed Testing Solutions Industry?

The market segments include Type of Delivery Model, Size of Organization, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 302.53 Million as of 2022.

5. What are some drivers contributing to market growth?

Adopting artificial intelligence (AI) and cloud management is eventually helping organizations meet various functional business requirements while driving business process optimization.; The growing preference for outsourcing management functions to cloud service providers and managed service providers is expected to drive market growth..

6. What are the notable trends driving market growth?

Healthcare to Witness the Highest Growth.

7. Are there any restraints impacting market growth?

The market's need for more skilled labor is a significant challenge. Understanding customer requirements and selecting the best testing method required specialized knowledge..

8. Can you provide examples of recent developments in the market?

July 2023 - TestingXperts, a software testing and quality assurance company, is pleased to announce its further expansion into Canada, strengthening its presence in the North American market. The decision to expand into Canada aligns with the company's strategic vision to cater to the region's growing demand for Quality Engineering and software testing services.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Managed Testing Solutions Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Managed Testing Solutions Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Managed Testing Solutions Industry?

To stay informed about further developments, trends, and reports in the Managed Testing Solutions Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence