Key Insights

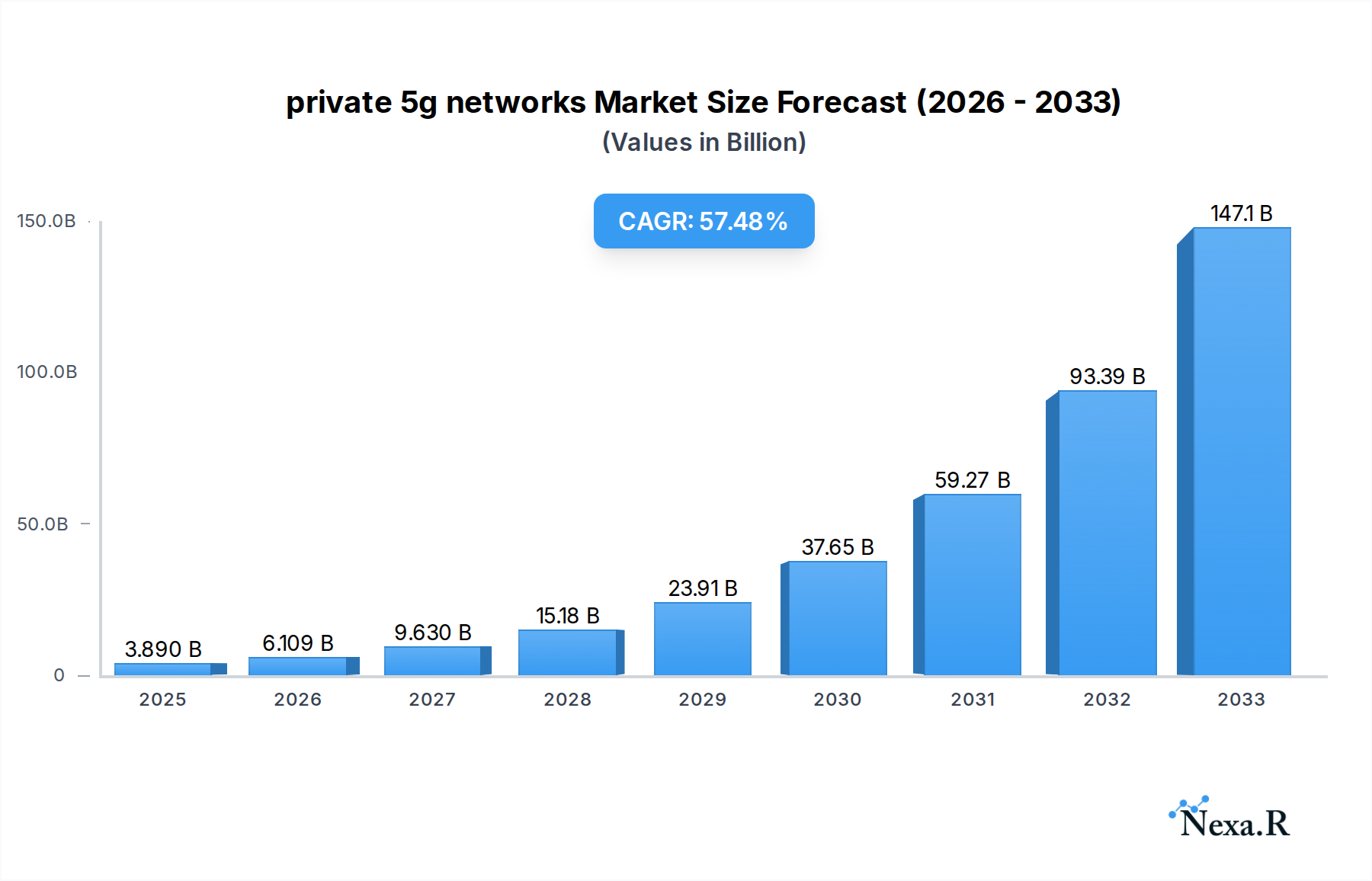

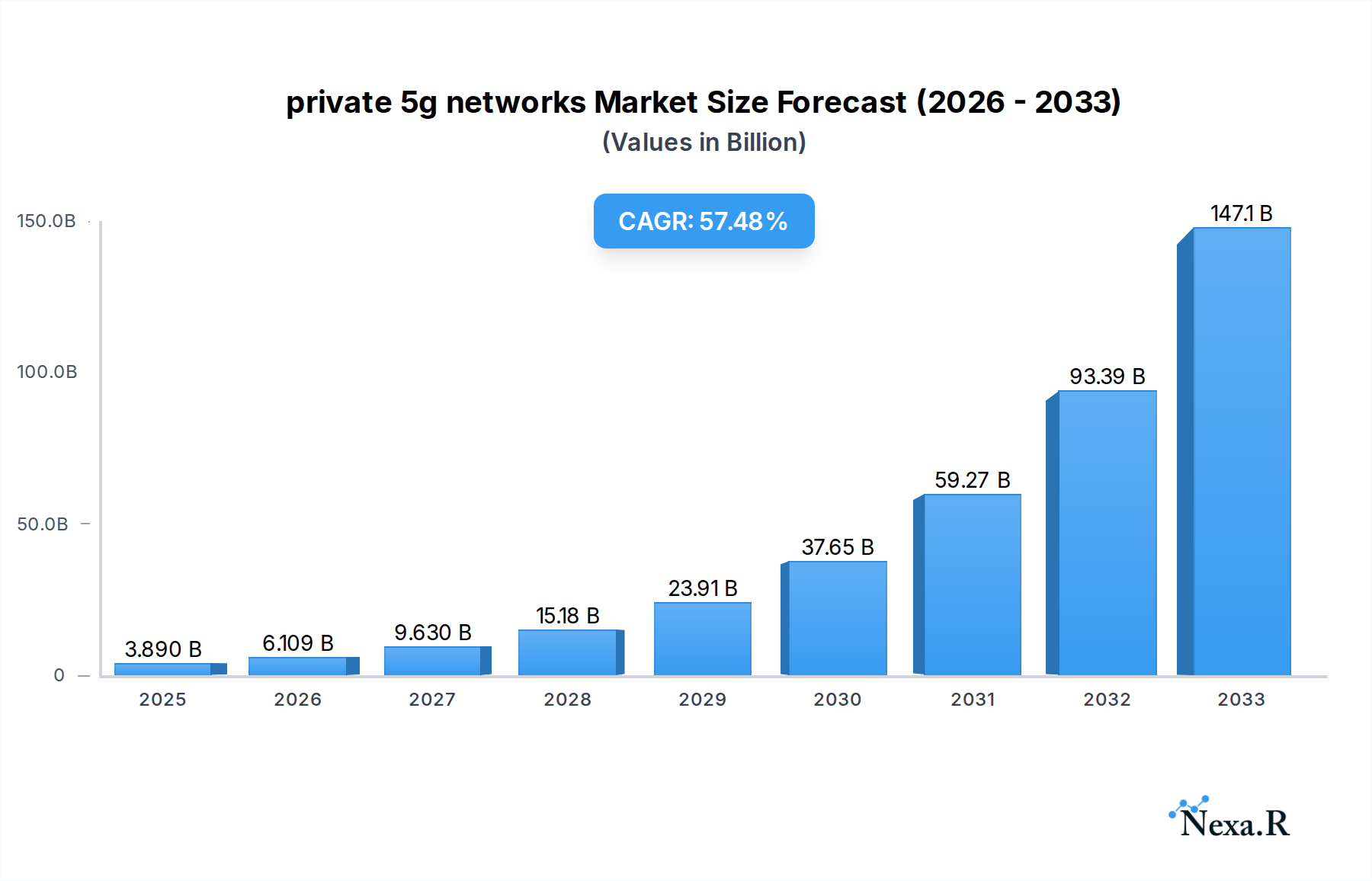

The global private 5G networks market is poised for extraordinary expansion, with an estimated market size of $3.89 billion in 2025. This burgeoning sector is projected to experience a staggering compound annual growth rate (CAGR) of 58.9% throughout the forecast period of 2025-2033, indicating a rapid and sustained surge in adoption. Key drivers fueling this explosive growth include the increasing demand for ultra-reliable low-latency communication (URLLC) capabilities across various industries, the need for enhanced operational efficiency, and the burgeoning deployment of Industrial IoT (IIoT) solutions. Furthermore, the growing emphasis on data security and sovereign control over critical infrastructure is compelling organizations to invest in dedicated private networks. The convergence of advanced technologies like AI, edge computing, and automation, all of which are significantly amplified by private 5G, is creating a powerful ecosystem for innovation and transformation.

private 5g networks Market Size (In Billion)

The market is segmented across diverse applications, with Manufacturing leading the charge due to its critical need for real-time monitoring, predictive maintenance, and enhanced automation. Other significant application areas include Energy, Utilities, and Mining, where private 5G enables remote operations and safety enhancements; Transportation & Logistics for optimized supply chain management; and Healthcare for remote diagnostics and robotic surgery. The technology itself is bifurcated into Sub-6 GHz and mmWave spectrums, each catering to different use cases based on coverage and bandwidth requirements. Restraints such as the complexity of deployment and integration, alongside regulatory hurdles and the initial capital expenditure, are being steadily overcome by technological advancements, evolving business models, and a growing understanding of the long-term ROI. Industry giants like Nokia, Ericsson, Huawei, Samsung, and Qualcomm are at the forefront of this evolution, driving innovation and shaping the competitive landscape.

private 5g networks Company Market Share

Comprehensive Report on the Global Private 5G Networks Market: Growth, Trends, and Opportunities (2019-2033)

This in-depth report provides a definitive analysis of the global private 5G networks market, charting its trajectory from 2019 to 2033. With a base year of 2025, the study offers granular insights into market dynamics, growth trends, regional dominance, product landscapes, and key players shaping this transformative sector. Leveraging extensive data and expert analysis, the report empowers stakeholders with actionable intelligence to navigate the evolving private 5G ecosystem, including the parent and child market segments. The report is structured to deliver maximum value and requires no further modification.

Private 5G Networks Market Dynamics & Structure

The global private 5G networks market is characterized by a dynamic interplay of technological innovation, evolving regulatory landscapes, and increasing demand from diverse industry verticals. Market concentration is moderate, with a few key players holding significant sway, while innovation is primarily driven by advancements in spectrum availability, edge computing integration, and enhanced security protocols. Regulatory frameworks are gradually maturing, facilitating deployment through spectrum allocation policies and enterprise-specific licensing. Competitive product substitutes, such as robust Wi-Fi 6/6E solutions and licensed LTE, are present but increasingly outpaced by the superior performance and latency of 5G. End-user demographics are shifting towards industrial enterprises, logistics providers, and healthcare institutions seeking dedicated, high-performance wireless connectivity. Mergers and acquisitions are on the rise as companies seek to consolidate their offerings and expand their market reach.

- Technological Innovation Drivers: Low latency, high bandwidth, massive device connectivity, network slicing capabilities.

- Regulatory Frameworks: Spectrum availability (e.g., CBRS in the US), national broadband plans, enterprise licensing models.

- Competitive Product Substitutes: Wi-Fi 6/6E, Private LTE, Public 5G slicing.

- End-User Demographics: Manufacturing (Industry 4.0), Transportation & Logistics, Healthcare, Energy & Utilities, Corporates.

- M&A Trends: Consolidation of network operators, technology providers, and system integrators; M&A deal volumes (2019-2024) estimated at over 15 billion.

- Innovation Barriers: High initial investment costs, spectrum availability challenges in certain regions, integration complexity.

Private 5G Networks Growth Trends & Insights

The private 5G networks market is poised for exponential growth, driven by an increasing recognition of its transformative potential across a wide array of industries. The market size evolution is projected to see a significant upward trend, moving from an estimated Market Size in 2025 of $18.5 billion to reach an estimated $XX billion by 2033. Adoption rates are accelerating as enterprises move beyond pilot projects to full-scale deployments, spurred by the promise of enhanced operational efficiency, real-time data analytics, and the enablement of next-generation applications. Technological disruptions, such as the convergence of 5G with AI, IoT, and edge computing, are redefining the possibilities for automation and intelligent systems. Consumer behavior shifts, while less direct, influence enterprise adoption as businesses strive to meet the demands of a digitally-native customer base through improved services and experiences enabled by private 5G. The CAGR for the forecast period (2025-2033) is projected to be in the range of 28-32%. Market penetration, currently in its nascent stages, is expected to deepen considerably as costs decrease and use cases become more clearly defined and widely adopted. The deployment of private 5G networks is not just an upgrade but a foundational shift for industries seeking to harness the full power of digital transformation. The ability to create bespoke, dedicated networks offers unparalleled control over performance, security, and reliability, which is becoming a critical differentiator in a competitive global market. The integration with cloud services and edge computing capabilities further amplifies the value proposition, allowing for localized data processing and reduced latency for critical applications. This synergy is a key driver in overcoming initial deployment hesitations and fostering widespread adoption.

Dominant Regions, Countries, or Segments in Private 5G Networks

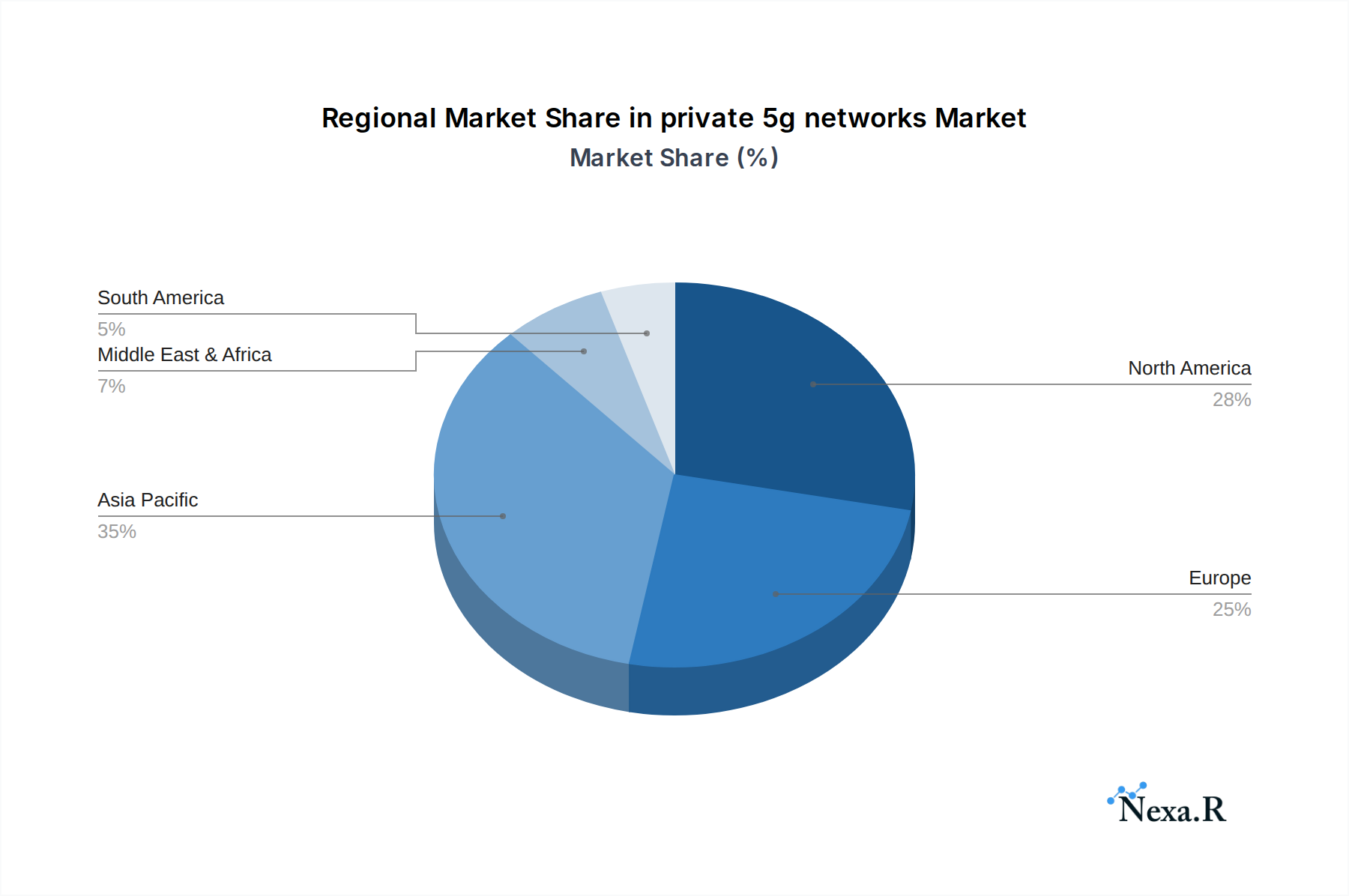

The global private 5G networks market exhibits distinct regional and segmental dominance, with North America and Europe currently leading in adoption, driven by robust industrial bases and supportive regulatory environments. However, the Asia-Pacific region, particularly China, is rapidly emerging as a significant growth engine, fueled by aggressive government initiatives and the rapid digitalization of its manufacturing and logistics sectors.

Dominant Segments:

- Application: Manufacturing: This sector is a primary driver, embracing private 5G for Industry 4.0 initiatives, automation, robotics, predictive maintenance, and real-time quality control. The need for ultra-reliable low-latency communication (URLLC) in factory settings makes private 5G an ideal solution. Market share within the manufacturing segment is estimated to be over 30%.

- Application: Corporates & Enterprises: Businesses across various sectors are leveraging private 5G for enhanced internal communications, secure Wi-Fi offloading, private cloud integration, and smart office environments. The demand for secure, dedicated connectivity for sensitive operations is a key enabler.

- Types: Sub-6 GHz: This frequency band offers a good balance of coverage and capacity, making it the preferred choice for widespread private 5G deployments, particularly in large industrial sites and campuses. Its ability to penetrate buildings effectively further solidifies its dominance.

Key Drivers of Dominance:

- Economic Policies: Government incentives for digital transformation, investment in advanced manufacturing, and support for 5G infrastructure development are crucial.

- Infrastructure Investment: The availability of advanced telecommunications infrastructure and the willingness of enterprises to invest in dedicated private networks.

- Industry-Specific Needs: The inherent requirements for high bandwidth, low latency, and robust security in sectors like manufacturing and logistics are perfectly met by private 5G.

- Technological Maturity: The increasing availability of mature 5G equipment and solutions from key vendors is facilitating broader adoption.

The market share of North America is estimated at around 35%, followed by Europe at approximately 30%, and Asia-Pacific at around 25%. Growth potential in Asia-Pacific is exceptionally high, projected to outpace other regions in the coming years due to rapid industrialization and government focus on advanced technologies. The healthcare sector, with its critical need for reliable and secure connectivity for remote patient monitoring, robotic surgery, and hospital operations, is also demonstrating significant growth potential.

Private 5G Networks Product Landscape

The private 5G networks product landscape is characterized by a sophisticated array of solutions designed to meet the bespoke connectivity needs of enterprises. Key product innovations include integrated network solutions that combine 5G core functionalities with edge computing capabilities, enabling real-time data processing closer to the source. Specialized 5G small cells and antennas are optimized for indoor and outdoor enterprise environments, ensuring reliable coverage even in challenging industrial settings. Network slicing technology allows for the creation of dedicated, virtualized network segments tailored to specific application requirements, such as ultra-low latency for robotic control or high bandwidth for video surveillance. Performance metrics are continuously improving, with latency figures dropping to single-digit milliseconds and throughput rates exceeding gigabits per second. Unique selling propositions revolve around enhanced security, guaranteed quality of service (QoS), and localized control, differentiating private 5G from public cellular networks. Technological advancements are also focusing on simplified deployment and management, making these complex networks more accessible to a wider range of businesses.

Key Drivers, Barriers & Challenges in Private 5G Networks

Key Drivers:

The primary forces propelling the private 5G networks market are the relentless pursuit of operational efficiency and the enablement of advanced digital transformation initiatives. Technological advancements, such as the inherent capabilities of 5G like low latency, high bandwidth, and massive device connectivity, are fundamental drivers. Economic factors, including the need to reduce operational costs and improve productivity, are pushing enterprises towards dedicated, high-performance networks. Policy-driven initiatives from governments worldwide, aimed at fostering innovation and digital sovereignty, further accelerate adoption. For instance, the availability of licensed or shared spectrum, like CBRS in the US, has significantly lowered the barrier to entry for many organizations. The demand for enhanced security and control over data traffic for sensitive operations also acts as a powerful catalyst.

Key Barriers & Challenges:

Despite the strong growth trajectory, the private 5G networks sector faces several hurdles. High initial investment costs for infrastructure and equipment remain a significant barrier for many small and medium-sized enterprises. Spectrum availability, while improving, can still be a challenge in certain regions, requiring complex licensing processes or reliance on shared spectrum models. Integration complexity with existing IT infrastructure and operational technology (OT) systems requires specialized expertise and careful planning. Regulatory hurdles, though diminishing, can still pose challenges in specific geographies. Supply chain issues for critical 5G components can lead to project delays and increased costs, impacting deployment timelines. Competitive pressures from existing wireless technologies and evolving public 5G offerings also require vendors and service providers to continuously innovate and demonstrate clear value propositions. Quantifiable impacts of these challenges can include project delays of up to 6-12 months and cost overruns of 10-20% for complex deployments.

Emerging Opportunities in Private 5G Networks

Emerging opportunities in the private 5G networks market are abundant and continue to expand as the technology matures and its applications diversify. The proliferation of Industrial IoT (IIoT) devices across sectors like manufacturing, energy, and logistics presents a vast untapped market for reliable, high-performance connectivity. Innovative applications are emerging in areas such as autonomous robotics, augmented reality (AR) and virtual reality (VR) for training and operations, and real-time asset tracking in complex environments. Evolving consumer preferences for seamless, high-speed connectivity are also indirectly influencing enterprise adoption, as businesses seek to enhance customer experiences through new digital services. The development of private 5G-as-a-service models is creating new business opportunities for service providers and reducing the upfront investment burden for enterprises. Furthermore, the integration of private 5G with other emerging technologies like AI and blockchain is opening doors for hyper-personalized solutions and enhanced data security. The smart city initiative is also a significant avenue, with private 5G forming the backbone for interconnected urban infrastructure.

Growth Accelerators in the Private 5G Networks Industry

Several key catalysts are driving the long-term growth of the private 5G networks industry. Technological breakthroughs in areas such as millimeter-wave (mmWave) spectrum utilization for higher capacity and advanced antenna technologies are enhancing network performance and expanding deployment possibilities. Strategic partnerships between telecommunications equipment manufacturers, cloud service providers, and enterprise software vendors are crucial for developing integrated, end-to-end solutions that address specific industry needs. Market expansion strategies, including the development of standardized deployment frameworks and the creation of skilled workforces, are essential for broadening the adoption base. The increasing demand for edge computing capabilities, which private 5G networks are ideally positioned to support, will further accelerate growth. Moreover, the ongoing digital transformation across all industries, coupled with the need for enhanced cybersecurity and operational resilience, will continue to fuel the demand for dedicated, high-performance wireless infrastructure. The development of robust private 5G ecosystems, including device manufacturers and application developers, will create a virtuous cycle of innovation and adoption.

Key Players Shaping the Private 5G Networks Market

- Nokia

- Ericsson

- Huawei

- Samsung

- ZTE

- China Mobile

- China Unicom

- Verizon

- Deutsche Telekom

- Vodafone

- Qualcomm

- NEC

- Fujitsu

- NTT

- Advantech

- Amazon Web Services (AWS)

- Cisco

- HPE

- AT&T

Notable Milestones in Private 5G Networks Sector

- 2019: Initial commercial deployments of private LTE networks begin to showcase the potential for dedicated enterprise connectivity.

- 2020: First pilot projects for private 5G networks in manufacturing and logistics environments demonstrate significant performance improvements.

- 2021: Standardization efforts for private 5G network architecture and deployment models gain momentum within industry bodies.

- 2022: Increased availability of 5G-enabled private network solutions and services from major telecommunications vendors.

- 2023: Significant growth in private 5G network deployments for Industry 4.0 applications and smart factory initiatives.

- 2024: Expansion of private 5G use cases into new sectors like healthcare and advanced transportation, with notable partnerships announced.

- 2025 (Estimated): Widespread adoption of private 5G for mission-critical enterprise applications, with an estimated market value exceeding $18.5 billion.

In-Depth Private 5G Networks Market Outlook

The future outlook for the private 5G networks market is exceptionally strong, driven by a confluence of technological advancements, evolving enterprise needs, and supportive regulatory environments. Growth accelerators, including the convergence of 5G with AI, IoT, and edge computing, will unlock novel applications and drive efficiency gains across industries. Strategic partnerships will be pivotal in delivering end-to-end solutions and fostering ecosystem development. The increasing focus on digital sovereignty and data security will further bolster the demand for private, controlled networks. As deployment costs continue to decrease and the benefits become more tangible, market penetration is projected to accelerate significantly. The report forecasts robust growth, with the market poised to become a cornerstone of digital transformation for enterprises worldwide, creating significant strategic opportunities for early adopters and innovative solution providers. The ability to tailor network performance, security, and coverage to exact enterprise requirements positions private 5G as an indispensable tool for future competitiveness.

private 5g networks Segmentation

-

1. Application

- 1.1. Manufacturing

- 1.2. Energy, Utilities and Mining

- 1.3. Transportation & Logistics

- 1.4. Education and Hospitality

- 1.5. Government & Public Safety

- 1.6. Corporates & Enterprises

- 1.7. Healthcare

- 1.8. Others

-

2. Types

- 2.1. Sub-6 GHz

- 2.2. mmWave

private 5g networks Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

private 5g networks Regional Market Share

Geographic Coverage of private 5g networks

private 5g networks REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 58.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Manufacturing

- 5.1.2. Energy, Utilities and Mining

- 5.1.3. Transportation & Logistics

- 5.1.4. Education and Hospitality

- 5.1.5. Government & Public Safety

- 5.1.6. Corporates & Enterprises

- 5.1.7. Healthcare

- 5.1.8. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Sub-6 GHz

- 5.2.2. mmWave

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global private 5g networks Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Manufacturing

- 6.1.2. Energy, Utilities and Mining

- 6.1.3. Transportation & Logistics

- 6.1.4. Education and Hospitality

- 6.1.5. Government & Public Safety

- 6.1.6. Corporates & Enterprises

- 6.1.7. Healthcare

- 6.1.8. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Sub-6 GHz

- 6.2.2. mmWave

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America private 5g networks Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Manufacturing

- 7.1.2. Energy, Utilities and Mining

- 7.1.3. Transportation & Logistics

- 7.1.4. Education and Hospitality

- 7.1.5. Government & Public Safety

- 7.1.6. Corporates & Enterprises

- 7.1.7. Healthcare

- 7.1.8. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Sub-6 GHz

- 7.2.2. mmWave

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America private 5g networks Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Manufacturing

- 8.1.2. Energy, Utilities and Mining

- 8.1.3. Transportation & Logistics

- 8.1.4. Education and Hospitality

- 8.1.5. Government & Public Safety

- 8.1.6. Corporates & Enterprises

- 8.1.7. Healthcare

- 8.1.8. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Sub-6 GHz

- 8.2.2. mmWave

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe private 5g networks Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Manufacturing

- 9.1.2. Energy, Utilities and Mining

- 9.1.3. Transportation & Logistics

- 9.1.4. Education and Hospitality

- 9.1.5. Government & Public Safety

- 9.1.6. Corporates & Enterprises

- 9.1.7. Healthcare

- 9.1.8. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Sub-6 GHz

- 9.2.2. mmWave

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa private 5g networks Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Manufacturing

- 10.1.2. Energy, Utilities and Mining

- 10.1.3. Transportation & Logistics

- 10.1.4. Education and Hospitality

- 10.1.5. Government & Public Safety

- 10.1.6. Corporates & Enterprises

- 10.1.7. Healthcare

- 10.1.8. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Sub-6 GHz

- 10.2.2. mmWave

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific private 5g networks Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Manufacturing

- 11.1.2. Energy, Utilities and Mining

- 11.1.3. Transportation & Logistics

- 11.1.4. Education and Hospitality

- 11.1.5. Government & Public Safety

- 11.1.6. Corporates & Enterprises

- 11.1.7. Healthcare

- 11.1.8. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Sub-6 GHz

- 11.2.2. mmWave

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Nokia

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Ericsson

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Huawei

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Samsung

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 ZTE

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 China Mobile

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 China Unicom

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Verizon

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Deutsche Telekom

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Vodafone

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Qualcomm

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 NEC

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Fujitsu

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 NTT

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Advantech

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Amazon Web Services (AWS)

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Cisco

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 HPE

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 AT&T

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.1 Nokia

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global private 5g networks Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America private 5g networks Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America private 5g networks Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America private 5g networks Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America private 5g networks Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America private 5g networks Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America private 5g networks Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America private 5g networks Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America private 5g networks Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America private 5g networks Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America private 5g networks Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America private 5g networks Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America private 5g networks Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe private 5g networks Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe private 5g networks Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe private 5g networks Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe private 5g networks Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe private 5g networks Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe private 5g networks Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa private 5g networks Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa private 5g networks Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa private 5g networks Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa private 5g networks Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa private 5g networks Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa private 5g networks Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific private 5g networks Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific private 5g networks Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific private 5g networks Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific private 5g networks Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific private 5g networks Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific private 5g networks Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global private 5g networks Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global private 5g networks Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global private 5g networks Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global private 5g networks Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global private 5g networks Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global private 5g networks Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global private 5g networks Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global private 5g networks Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global private 5g networks Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global private 5g networks Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global private 5g networks Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global private 5g networks Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global private 5g networks Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global private 5g networks Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global private 5g networks Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global private 5g networks Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global private 5g networks Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global private 5g networks Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific private 5g networks Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the private 5g networks?

The projected CAGR is approximately 58.9%.

2. Which companies are prominent players in the private 5g networks?

Key companies in the market include Nokia, Ericsson, Huawei, Samsung, ZTE, China Mobile, China Unicom, Verizon, Deutsche Telekom, Vodafone, Qualcomm, NEC, Fujitsu, NTT, Advantech, Amazon Web Services (AWS), Cisco, HPE, AT&T.

3. What are the main segments of the private 5g networks?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "private 5g networks," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the private 5g networks report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the private 5g networks?

To stay informed about further developments, trends, and reports in the private 5g networks, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence