Key Insights

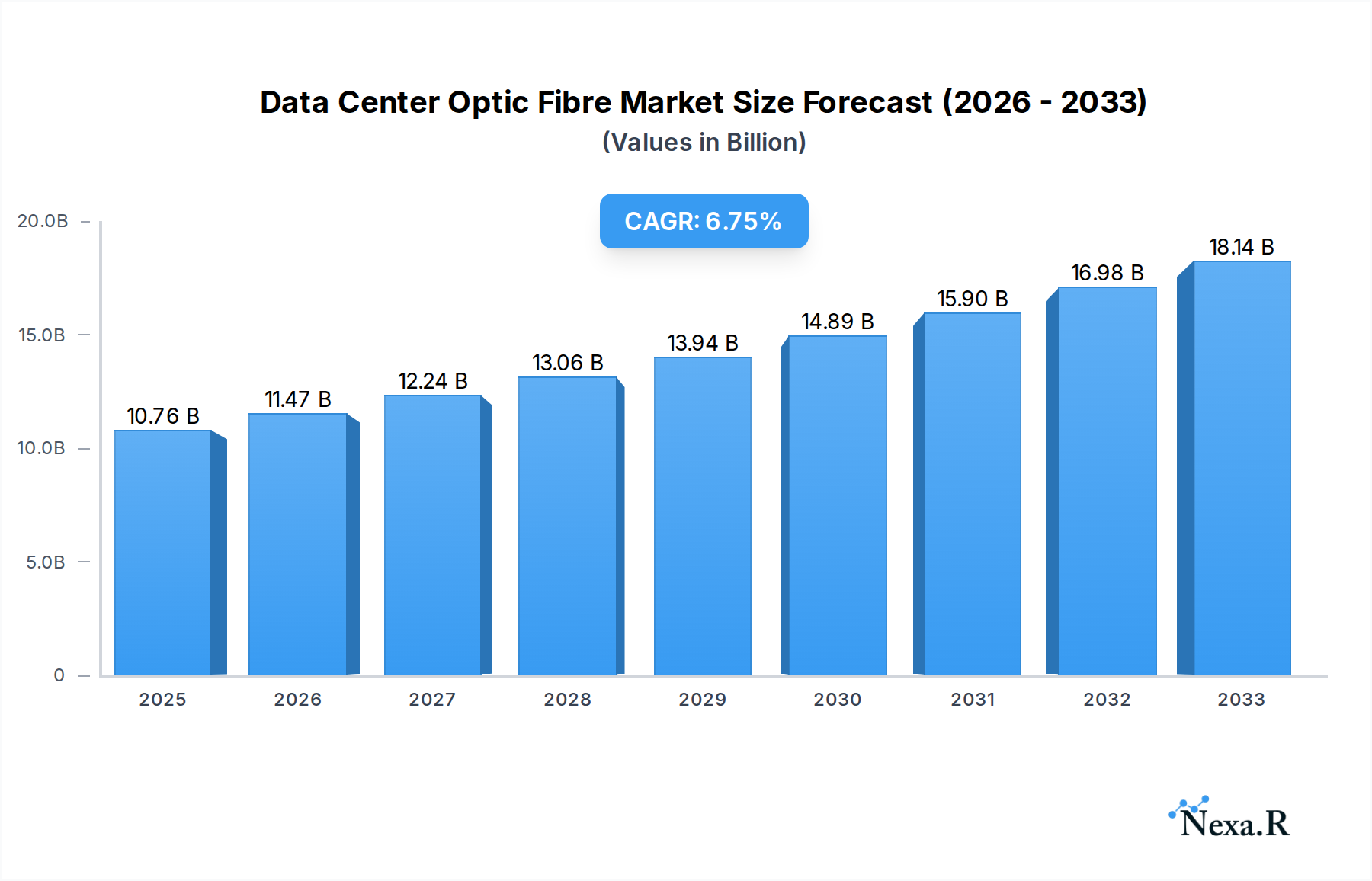

The global Data Center Optic Fibre market is poised for significant expansion, currently valued at approximately $10.76 billion in 2025. This robust growth is propelled by a compelling Compound Annual Growth Rate (CAGR) of 6.6% throughout the forecast period of 2025-2033. The primary drivers fueling this surge include the escalating demand for cloud computing services, the relentless expansion of enterprise data centers to accommodate burgeoning data volumes, and the continuous technological advancements in fiber optic technology, enabling higher bandwidth and faster data transmission speeds. The increasing adoption of AI, big data analytics, and the Internet of Things (IoT) further intensifies the need for high-performance data center infrastructure, directly translating to a greater requirement for advanced optic fiber solutions. Emerging applications in edge computing and the ongoing 5G network rollout also contribute to this upward trajectory, necessitating more distributed and powerful data center capabilities.

Data Center Optic Fibre Market Size (In Billion)

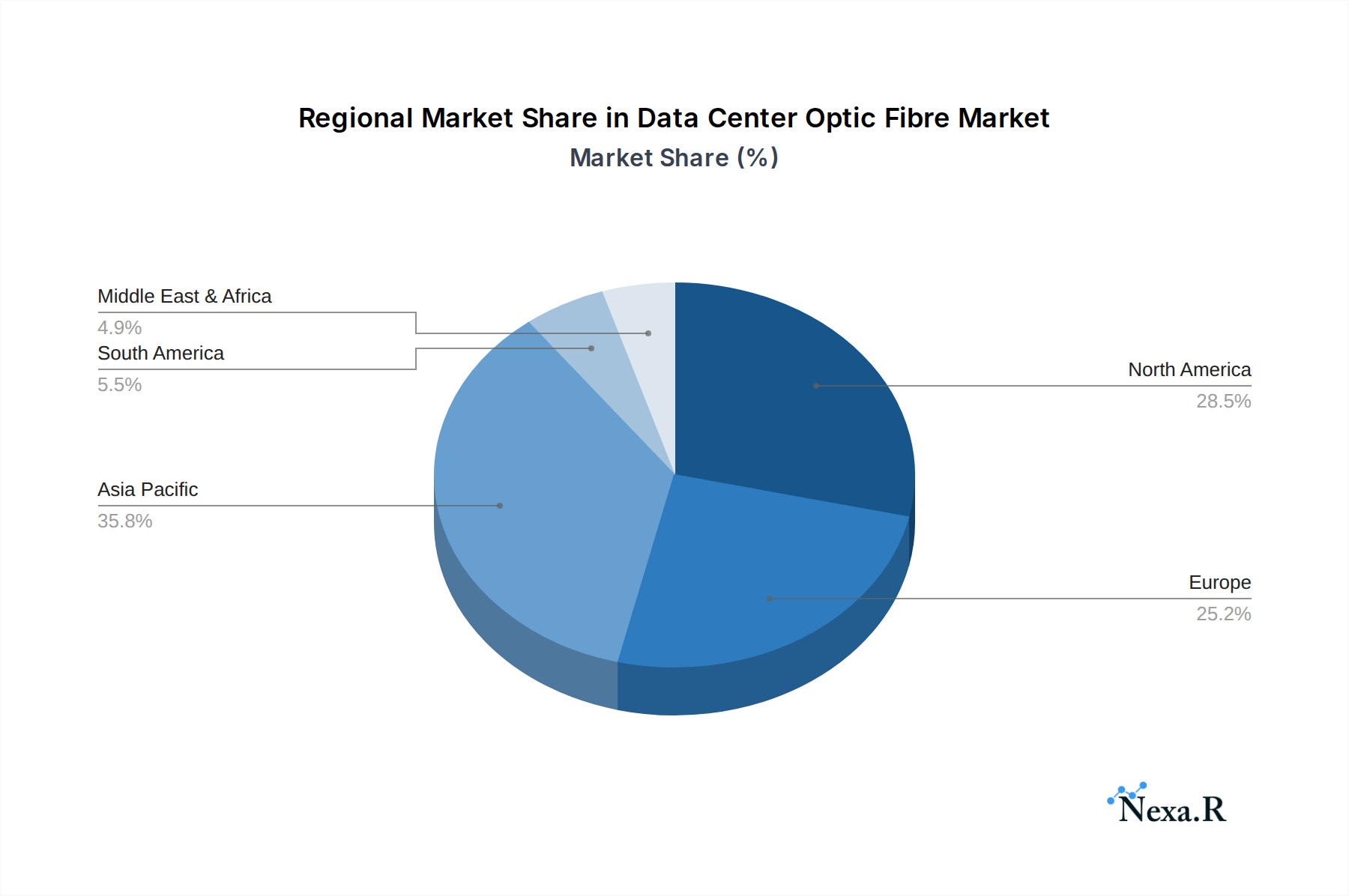

The market is segmented into key applications, with Enterprise Data Centers and Cloud Computing Data Centers dominating the demand landscape. The "Others" segment, encompassing specialized or emerging data center types, also presents growth opportunities. In terms of product types, both Single Mode and Multi Mode fiber optics are crucial, catering to different distance and bandwidth requirements within data centers. Geographically, Asia Pacific, particularly China and India, is expected to be a major growth engine due to rapid digital transformation and substantial investments in data center infrastructure. North America and Europe remain significant markets, driven by established cloud providers and a strong enterprise presence. Key players such as Corning, YOFC, Prysmian Group, and CommScope are actively investing in research and development to introduce innovative solutions that enhance data transmission efficiency and reduce latency, thereby shaping the competitive landscape and driving market evolution.

Data Center Optic Fibre Company Market Share

This comprehensive report provides an in-depth analysis of the global Data Center Optic Fibre market, offering critical insights into its evolving landscape from 2019 to 2033. With the base year set at 2025, the report meticulously examines market size, growth drivers, competitive strategies, and regional dominance, equipping industry stakeholders with actionable intelligence for strategic decision-making. The study integrates high-traffic SEO keywords to maximize visibility and attract professionals across enterprise data centers, cloud computing, and other critical infrastructure sectors.

Data Center Optic Fibre Market Dynamics & Structure

The Data Center Optic Fibre market exhibits a moderately concentrated structure, with key players like Corning, YOFC, Prysmian Group, and CommScope dominating a significant portion of the market share. Technological innovation remains the primary driver, fueled by the insatiable demand for higher bandwidth and lower latency to support the exponential growth of cloud computing, AI, and big data analytics. The relentless pursuit of faster data transmission speeds, such as 400 Gbps, 800 Gbps, and beyond, compels continuous R&D in advanced fibre optic technologies. Regulatory frameworks, while generally supportive of infrastructure development, can influence deployment timelines and standards, particularly concerning network security and interoperability. Competitive product substitutes, though limited in core fibre optic performance, include advancements in copper cabling for shorter distances and emerging wireless technologies for specific niche applications. End-user demographics are increasingly dominated by hyperscale cloud providers and large enterprises investing heavily in data center expansion and upgrades. Mergers and acquisition (M&A) trends are observed as larger players seek to consolidate market presence, acquire innovative technologies, and expand their geographical reach. For instance, the acquisition of specialized fibre optic manufacturers by integrated cable solutions providers aims to create end-to-end network infrastructure offerings. Innovation barriers primarily stem from the significant capital investment required for advanced manufacturing processes and the lengthy qualification cycles for new fibre optic products in mission-critical data center environments.

- Market Concentration: Moderately concentrated with a few key players holding substantial market share.

- Technological Innovation Drivers: Demand for higher bandwidth (400 Gbps, 800 Gbps), lower latency, AI, big data, and cloud computing.

- Regulatory Frameworks: Influences deployment, security, and interoperability standards.

- Competitive Product Substitutes: Limited for core fibre optic performance; emerging wireless and advanced copper for niche use cases.

- End-User Demographics: Dominated by hyperscale cloud providers and large enterprises.

- M&A Trends: Consolidation of market presence, technology acquisition, and geographical expansion.

- Innovation Barriers: High capital investment for advanced manufacturing, lengthy product qualification cycles.

Data Center Optic Fibre Growth Trends & Insights

The global Data Center Optic Fibre market is poised for substantial expansion, projected to witness a robust Compound Annual Growth Rate (CAGR) of approximately 9.5% from the base year 2025 through 2033. This significant growth trajectory is underpinned by a confluence of powerful market forces and evolving technological paradigms. The increasing adoption of cloud computing, an indispensable component of modern digital infrastructure, directly fuels the demand for high-capacity fibre optic cabling within data centers. As businesses across all sectors migrate their operations and data storage to cloud environments, the need for seamless, high-speed connectivity becomes paramount. Hyperscale data centers, the backbone of major cloud service providers, are continuously expanding their footprints and upgrading their internal networks to accommodate escalating data traffic. This expansion is a primary engine driving the demand for optic fibre cables.

Furthermore, the proliferation of data-intensive applications, including artificial intelligence (AI), machine learning (ML), the Internet of Things (IoT), and real-time analytics, necessitates significantly greater bandwidth and lower latency than ever before. Optic fibre, with its inherent superiority in data transmission speed and capacity, is the only viable solution to meet these demanding requirements. The ongoing transition from 100 Gbps to 400 Gbps and the emerging push towards 800 Gbps and 1.6 Tbps connectivity within data center architectures are direct catalysts for increased fibre optic deployment. Market penetration of advanced fibre optic technologies is deepening as organizations recognize the long-term benefits of investing in future-proof infrastructure.

Consumer behavior shifts, such as the increasing reliance on streaming services, online gaming, and remote work, also contribute indirectly by placing greater strain on internet infrastructure, which in turn requires robust data center capabilities. This cascading effect reinforces the need for advanced fibre optic solutions. Technological disruptions, such as advancements in fibre manufacturing processes, the development of higher-performance fibre types (e.g., low-loss fibres), and innovations in fibre optic connector and transceiver technologies, are further optimizing performance and reducing costs, thereby accelerating adoption. The estimated market size for Data Center Optic Fibre in 2025 is expected to be in the range of $15.8 billion, with projections indicating a significant surge to over $31.2 billion by 2033. The historical period from 2019 to 2024 saw a steady but less explosive growth as the market consolidated its position as the primary data center connectivity solution. This period laid the groundwork for the accelerated adoption witnessed in the forecast period. The shift towards higher-density cabling solutions and improved installation techniques also plays a crucial role in accommodating the increasing fibre counts within confined data center spaces.

Dominant Regions, Countries, or Segments in Data Center Optic Fibre

The Cloud Computing Data Center segment stands as the most dominant force driving growth in the global Data Center Optic Fibre market. This supremacy is directly attributed to the massive scale of infrastructure development and continuous upgrades undertaken by hyperscale cloud providers, including industry giants such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud. These entities are perpetually expanding their data center capacities to cater to the ever-increasing global demand for cloud-based services, data storage, and processing power. The sheer volume of interconnectivity required within these colossal facilities, supporting millions of users and billions of data transactions, necessitates the extensive deployment of high-performance optic fibre. The market share within this segment is estimated to account for approximately 65% of the total Data Center Optic Fibre market in 2025, with projections indicating sustained dominance throughout the forecast period.

Geographically, North America and Asia-Pacific are the leading regions propelling market growth. North America benefits from the presence of major cloud providers’ headquarters and a mature market with substantial ongoing investments in data center expansion and modernization. The region's robust economy and early adoption of advanced technologies create a fertile ground for optic fibre deployment. The United States, in particular, represents a significant market due to its extensive cloud infrastructure and enterprise data center build-outs. Asia-Pacific, led by China, is experiencing an unprecedented surge in data center construction driven by rapid digitalization, a burgeoning middle class, and government initiatives promoting digital transformation and cloud adoption. The substantial investments in 5G network rollouts also indirectly contribute to data center growth, necessitating increased fibre optic connectivity.

Within the Types of optic fibre, Single Mode Fibre (SMF) holds a commanding position, particularly in long-haul and high-bandwidth applications prevalent in data centers. Its ability to transmit data over longer distances with minimal signal loss makes it indispensable for inter-data center connectivity and within large campus environments. While Multi-Mode Fibre (MMF) remains crucial for shorter-reach applications within racks and rows, the increasing distances and bandwidth demands within modern data centers are tilting the balance towards SMF. The market share for Single Mode Fibre in data center applications is estimated at around 60% in 2025, with continuous growth anticipated as data rates escalate.

- Dominant Application Segment: Cloud Computing Data Center (Estimated 65% market share in 2025).

- Key Drivers: Hyperscale cloud provider infrastructure expansion, increasing demand for cloud services, data storage, and processing.

- Growth Potential: Sustained dominance due to ongoing digital transformation and cloud adoption.

- Dominant Regions:

- North America: Strong enterprise adoption, major cloud provider presence, significant data center investments.

- Key Drivers: Advanced technology adoption, economic stability, continuous infrastructure upgrades.

- Asia-Pacific: Rapid digitalization, massive data center construction, government initiatives, 5G rollout spillover effects.

- Key Drivers: Emerging economies, increasing internet penetration, digital transformation policies.

- North America: Strong enterprise adoption, major cloud provider presence, significant data center investments.

- Dominant Fibre Type: Single Mode Fibre (SMF) (Estimated 60% market share in 2025).

- Key Drivers: Long-distance transmission, high bandwidth requirements, increasing data rates (400 Gbps, 800 Gbps).

- Growth Potential: Increased demand for longer reach and higher capacity within data centers.

Data Center Optic Fibre Product Landscape

The Data Center Optic Fibre product landscape is characterized by continuous innovation focused on enhancing bandwidth, reducing signal loss, and improving density. Leading companies are offering advanced fibre types, including bend-insensitive fibres and ultra-low-loss fibres, crucial for higher data rates and complex cabling architectures. Innovations in connector technologies, such as MPO/MTP connectors, enable higher fibre counts within smaller form factors, optimizing space utilization in high-density environments. Furthermore, advancements in fibre optic cable designs, including compact and robust cable constructions, cater to the specific demands of data center installations. Performance metrics like attenuation coefficients, modal bandwidth, and operational lifespan are constantly being improved to meet the stringent requirements of next-generation data center networks supporting applications like AI and 5G.

Key Drivers, Barriers & Challenges in Data Center Optic Fibre

Key Drivers:

- Explosive Data Growth: The relentless surge in data generation from AI, IoT, and big data analytics mandates higher bandwidth and capacity, directly driving optic fibre demand.

- Cloud Computing Expansion: The continuous growth of hyperscale and enterprise cloud data centers requires extensive fibre optic infrastructure for interconnections and internal networking.

- Technological Advancements: The push for faster data rates (400 Gbps, 800 Gbps) and lower latency necessitates the adoption of advanced fibre optic technologies.

- 5G Network Deployment: The proliferation of 5G requires robust backhaul and fronthaul infrastructure, indirectly fueling demand for fibre optics in data centers that support these networks.

Barriers & Challenges:

- High Initial Investment: The cost of deploying high-density, high-performance optic fibre cabling and associated equipment can be substantial for some organizations.

- Skilled Labor Shortage: A lack of adequately trained personnel for the installation, maintenance, and troubleshooting of complex fibre optic networks can hinder deployment.

- Supply Chain Disruptions: Geopolitical factors, raw material availability, and manufacturing capacity can lead to supply chain bottlenecks and price volatility.

- Standardization and Interoperability: Ensuring compatibility and interoperability across different vendors' products and evolving industry standards can be a challenge.

- Competitive Pressures: While fibre optics are dominant, intense competition among manufacturers can lead to price erosion, impacting profitability.

Emerging Opportunities in Data Center Optic Fibre

Emerging opportunities in the Data Center Optic Fibre sector are primarily driven by the expansion of edge computing, the growing adoption of optical switching technologies, and the development of novel fibre sensing applications within data centers. Edge data centers, distributed closer to end-users and IoT devices, will necessitate localized, high-speed fibre optic connectivity, creating new deployment grounds. The increasing interest in all-optical switching to bypass electronic bottlenecks presents a future pathway for enhanced data throughput, requiring specialized fibre optic components. Furthermore, innovative applications like fibre optic sensing for temperature and vibration monitoring within data centers can improve operational efficiency and predictive maintenance. The growing demand for specialized fibre optic solutions tailored for specific data center environments, such as colocation facilities and enterprise private clouds, also presents significant untapped market potential.

Growth Accelerators in the Data Center Optic Fibre Industry

Several key catalysts are accelerating the long-term growth of the Data Center Optic Fibre industry. The continuous evolution of network speeds, from 400 Gbps towards 800 Gbps and beyond, is a primary accelerator, compelling frequent upgrades and new deployments. Strategic partnerships between fibre optic manufacturers and network equipment vendors are crucial for developing integrated solutions and ensuring seamless interoperability. Market expansion strategies, particularly focusing on underserved emerging economies with rapidly growing digital footprints, will unlock new revenue streams. Furthermore, significant investments in research and development by leading companies to create next-generation fibre technologies with enhanced performance characteristics and reduced costs are vital growth engines. The increasing trend of data center consolidation and the construction of mega data centers also acts as a major accelerator, demanding massive quantities of optic fibre.

Key Players Shaping the Data Center Optic Fibre Market

- Corning

- YOFC

- Prysmian Group

- CommScope

- Southwire

- Belden

- Nexans

- Sumitomo Electric

- LS Cable & System

- Furukawa Electric

- AFL

- Fujikura

- Leoni

- Tongding

- Encore Wire

Notable Milestones in Data Center Optic Fibre Sector

- 2020: Introduction of widely adopted 400G optical transceivers, driving demand for higher-performance optic fibres.

- 2021: Significant investments in advanced fibre manufacturing facilities by key players to meet escalating demand.

- 2022: Increased adoption of bend-insensitive multimode fibres for higher density within data center racks.

- 2023: Growing interest and R&D in silicon photonics and their integration with fibre optic solutions for data centers.

- 2024: Emergence of standards and early deployments for 800Gbps data rates, pushing the boundaries of fibre optic capabilities.

- 2025 (Estimated): Continued growth in Single Mode Fibre adoption for high-speed, long-reach data center interconnects.

- 2026-2030 (Projected): Widespread deployment of 800Gbps and experimentation with 1.6Tbps connectivity, requiring new fibre optic technologies.

- 2031-2033 (Projected): Maturation of optical switching technologies and the continued expansion of edge data centers influencing fibre optic deployment strategies.

In-Depth Data Center Optic Fibre Market Outlook

The future outlook for the Data Center Optic Fibre market is exceptionally bright, driven by an unyielding demand for digital connectivity and processing power. Growth accelerators such as the relentless pursuit of higher data rates (800 Gbps and beyond), the foundational role of fibre optics in expanding cloud infrastructure, and the increasing adoption of AI and machine learning applications will continue to propel market expansion. Strategic partnerships between fibre manufacturers and technology integrators will streamline the deployment of next-generation networks, while expansion into nascent markets will further broaden the addressable market. The ongoing evolution of optical switching and the proliferation of edge computing further cement fibre optic's indispensable role. This sustained growth trajectory indicates a highly dynamic and promising market, ripe with opportunities for innovation and strategic investment, with the total market value projected to exceed $31.2 billion by 2033.

Data Center Optic Fibre Segmentation

-

1. Application

- 1.1. Enterprise Data Center

- 1.2. Cloud Computing Data Center

- 1.3. Others

-

2. Types

- 2.1. Single Mode

- 2.2. Multi Mode

Data Center Optic Fibre Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Data Center Optic Fibre Regional Market Share

Geographic Coverage of Data Center Optic Fibre

Data Center Optic Fibre REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Data Center Optic Fibre Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Enterprise Data Center

- 5.1.2. Cloud Computing Data Center

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Single Mode

- 5.2.2. Multi Mode

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Data Center Optic Fibre Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Enterprise Data Center

- 6.1.2. Cloud Computing Data Center

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Single Mode

- 6.2.2. Multi Mode

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Data Center Optic Fibre Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Enterprise Data Center

- 7.1.2. Cloud Computing Data Center

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Single Mode

- 7.2.2. Multi Mode

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Data Center Optic Fibre Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Enterprise Data Center

- 8.1.2. Cloud Computing Data Center

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Single Mode

- 8.2.2. Multi Mode

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Data Center Optic Fibre Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Enterprise Data Center

- 9.1.2. Cloud Computing Data Center

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Single Mode

- 9.2.2. Multi Mode

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Data Center Optic Fibre Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Enterprise Data Center

- 10.1.2. Cloud Computing Data Center

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Single Mode

- 10.2.2. Multi Mode

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Southwire

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Belden

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Prysmian Group

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Nexans

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Sumitomo Electric

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 LS Cable & System

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Furukawa Electric

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 AFL

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Corning

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 YOFC

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Fujikura

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Leoni

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Tongding

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 CommScope

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Encore Wire

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 Southwire

List of Figures

- Figure 1: Global Data Center Optic Fibre Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Data Center Optic Fibre Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Data Center Optic Fibre Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Data Center Optic Fibre Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Data Center Optic Fibre Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Data Center Optic Fibre Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Data Center Optic Fibre Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Data Center Optic Fibre Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Data Center Optic Fibre Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Data Center Optic Fibre Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Data Center Optic Fibre Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Data Center Optic Fibre Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Data Center Optic Fibre Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Data Center Optic Fibre Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Data Center Optic Fibre Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Data Center Optic Fibre Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Data Center Optic Fibre Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Data Center Optic Fibre Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Data Center Optic Fibre Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Data Center Optic Fibre Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Data Center Optic Fibre Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Data Center Optic Fibre Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Data Center Optic Fibre Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Data Center Optic Fibre Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Data Center Optic Fibre Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Data Center Optic Fibre Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Data Center Optic Fibre Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Data Center Optic Fibre Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Data Center Optic Fibre Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Data Center Optic Fibre Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Data Center Optic Fibre Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Data Center Optic Fibre Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Data Center Optic Fibre Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Data Center Optic Fibre Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Data Center Optic Fibre Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Data Center Optic Fibre Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Data Center Optic Fibre Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Data Center Optic Fibre Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Data Center Optic Fibre Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Data Center Optic Fibre Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Data Center Optic Fibre Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Data Center Optic Fibre Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Data Center Optic Fibre Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Data Center Optic Fibre Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Data Center Optic Fibre Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Data Center Optic Fibre Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Data Center Optic Fibre Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Data Center Optic Fibre Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Data Center Optic Fibre Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Data Center Optic Fibre Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Data Center Optic Fibre?

The projected CAGR is approximately 6.6%.

2. Which companies are prominent players in the Data Center Optic Fibre?

Key companies in the market include Southwire, Belden, Prysmian Group, Nexans, Sumitomo Electric, LS Cable & System, Furukawa Electric, AFL, Corning, YOFC, Fujikura, Leoni, Tongding, CommScope, Encore Wire.

3. What are the main segments of the Data Center Optic Fibre?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.76 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Data Center Optic Fibre," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Data Center Optic Fibre report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Data Center Optic Fibre?

To stay informed about further developments, trends, and reports in the Data Center Optic Fibre, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence