Key Insights

The global non-gluten products market is poised for robust expansion, estimated at USD 7.75 billion in 2024, and is projected to surge at a Compound Annual Growth Rate (CAGR) of 10% throughout the forecast period of 2025-2033. This substantial growth is propelled by a confluence of escalating health consciousness among consumers, a significant rise in celiac disease diagnoses and gluten sensitivity, and an increasing demand for healthier lifestyle choices. The perception of non-gluten products as beneficial for overall well-being, beyond just managing specific dietary needs, is further fueling their adoption across a wider consumer base. Furthermore, advancements in food technology have enabled manufacturers to develop innovative and palatable non-gluten alternatives for traditional staples like bakery products, pizzas, pastas, cereals, and snacks, broadening the appeal and accessibility of these products. The expanding distribution networks, including conventional stores, hotels, restaurants, and specialty retailers, are also playing a crucial role in making these products readily available to a global audience.

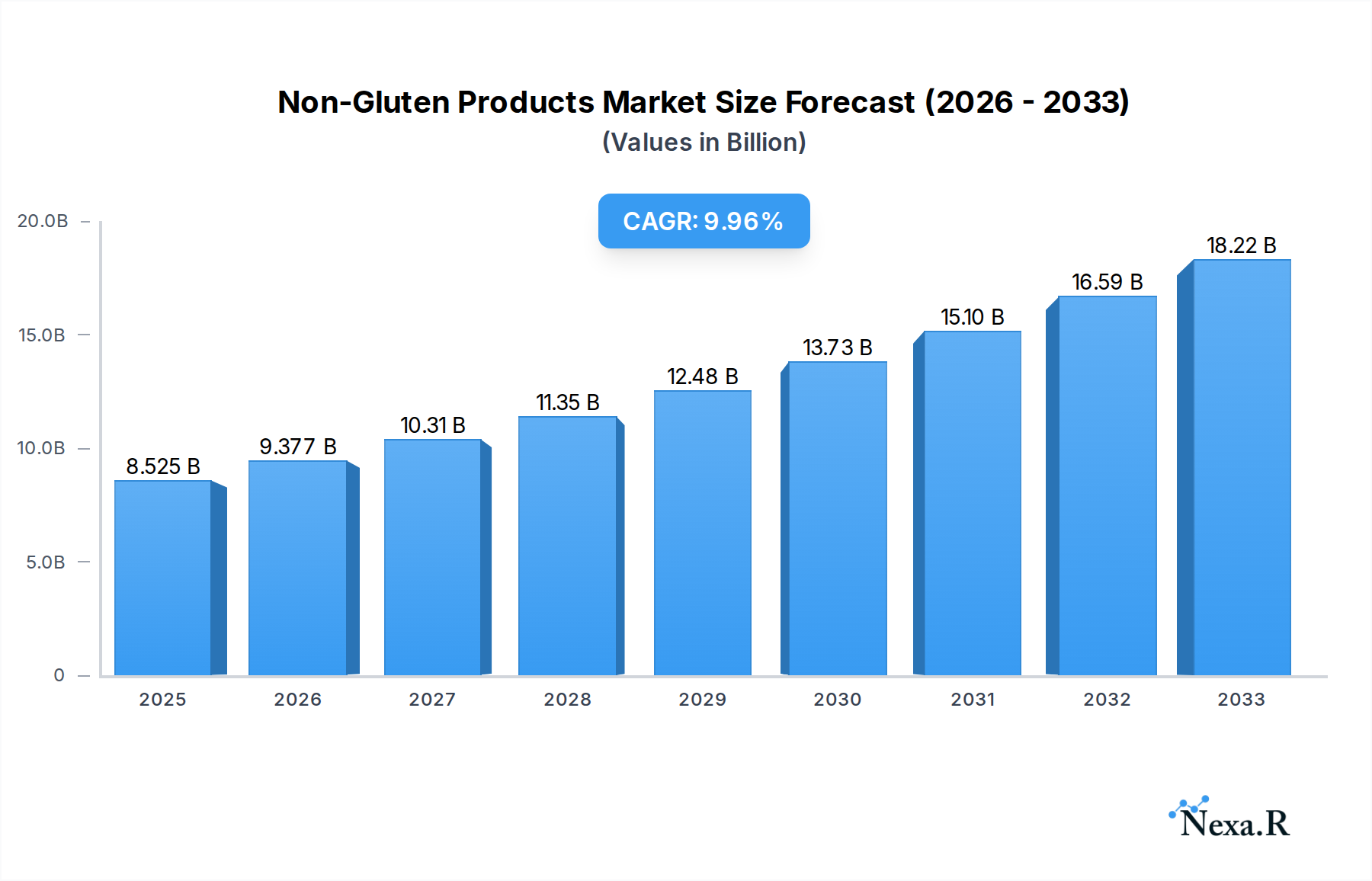

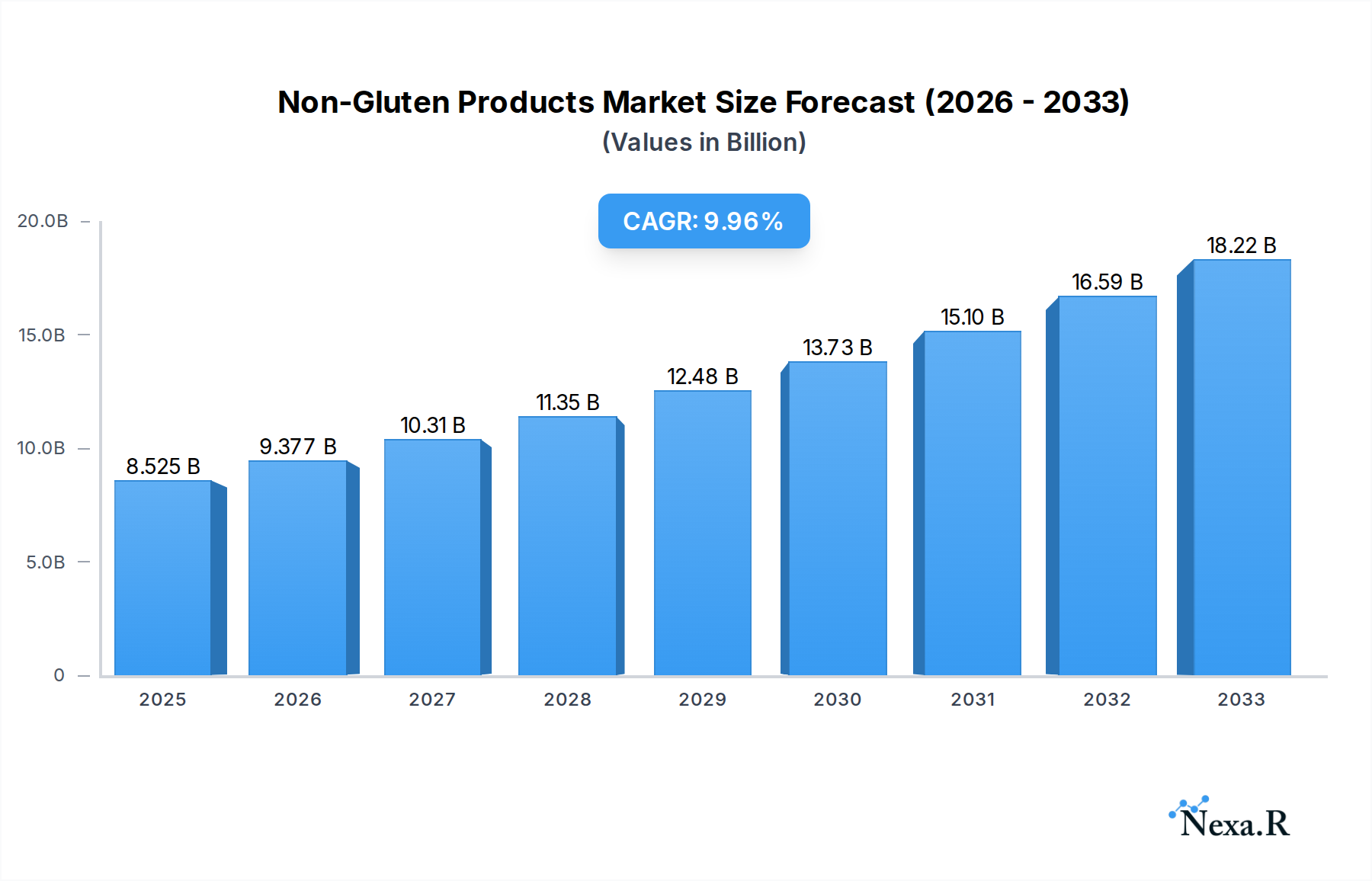

Non-Gluten Products Market Size (In Billion)

The market is witnessing a dynamic interplay of drivers and restraints, with key growth drivers including the increasing prevalence of food allergies and intolerances, a growing preference for natural and organic food options, and the proactive marketing efforts by key players highlighting the health benefits of non-gluten diets. Leading companies like Boulder Brands, Dr. Schär AG/SPA, General Mills, Inc., and The Hain Celestial Group are actively investing in research and development to introduce new product lines and expand their market reach. However, challenges such as the higher cost of production for non-gluten ingredients, potential taste and texture limitations compared to their gluten-containing counterparts, and the need for greater consumer education regarding the true benefits and necessity of a non-gluten diet, present hurdles to widespread adoption. Despite these restraints, the prevailing trend towards health and wellness, coupled with a continually evolving product landscape, suggests a promising and expansive future for the non-gluten products market.

Non-Gluten Products Company Market Share

Unlock unparalleled insights into the rapidly expanding non-gluten products market with our definitive, SEO-optimized report. This comprehensive analysis delves deep into the market dynamics, growth trends, and future outlook for gluten-free foods, a sector experiencing exponential growth driven by rising health consciousness, celiac disease prevalence, and a growing demand for healthier alternatives. We provide an in-depth examination of the parent market (food and beverage) and its crucial child market (non-gluten products), offering a holistic view of opportunities and challenges. This report is essential for industry professionals, manufacturers, ingredient suppliers, distributors, and investors seeking to capitalize on this lucrative market.

Non-Gluten Products Market Dynamics & Structure

The global non-gluten products market is characterized by a moderate to high level of concentration, with key players investing heavily in research and development to drive innovation. Technological advancements in ingredient processing, alternative flours, and specialized manufacturing techniques are critical drivers, enabling the production of high-quality, palatable gluten-free alternatives. Stringent regulatory frameworks surrounding food labeling and allergen declarations contribute to market transparency and consumer trust. While the demand for non-gluten products is robust, the market faces competition from a wide array of naturally gluten-free food options and the ongoing innovation in products designed to mimic the texture and taste of gluten-containing counterparts. End-user demographics are increasingly diverse, encompassing not only individuals with celiac disease or gluten sensitivity but also health-conscious consumers seeking perceived wellness benefits. Merger and acquisition (M&A) trends are prevalent as larger food conglomerates strategically expand their gluten-free portfolios to capture market share.

- Market Concentration: Dominated by a mix of established food giants and specialized gluten-free manufacturers.

- Technological Innovation: Focus on improving taste, texture, shelf-life, and cost-effectiveness of gluten-free products.

- Regulatory Frameworks: Strict labeling laws and allergen certifications enhance consumer confidence and market integrity.

- Competitive Product Substitutes: Vigorous competition from naturally gluten-free foods and innovative gluten-mimicking products.

- End-User Demographics: Expanding beyond celiac patients to include health-conscious consumers and those opting for lifestyle dietary changes.

- M&A Trends: Strategic acquisitions and partnerships by major food companies to enhance their gluten-free offerings.

Non-Gluten Products Growth Trends & Insights

The non-gluten products market is projected to witness substantial growth from USD 28.7 billion in 2025 to an estimated USD 45.9 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 6.0% during the forecast period (2025-2033). This robust expansion is fueled by a confluence of factors, including the increasing diagnosis of celiac disease and gluten intolerance worldwide, a growing trend towards health and wellness, and a broader consumer awareness regarding the potential benefits of a gluten-free diet, even for those without medical necessity. The historical period (2019-2024) has already laid a strong foundation, with the market demonstrating consistent upward momentum. Technological disruptions in food science have significantly improved the palatability and accessibility of gluten-free products, bridging the gap in taste and texture that once deterred widespread adoption. Consumer behavior shifts are evident, with a greater willingness to experiment with and integrate gluten-free options into their regular diets. The base year (2025) represents a critical juncture where current market trends are solidifying, providing a benchmark for future projections. This evolving landscape indicates a sustained demand for a wider variety of gluten-free options across all food categories.

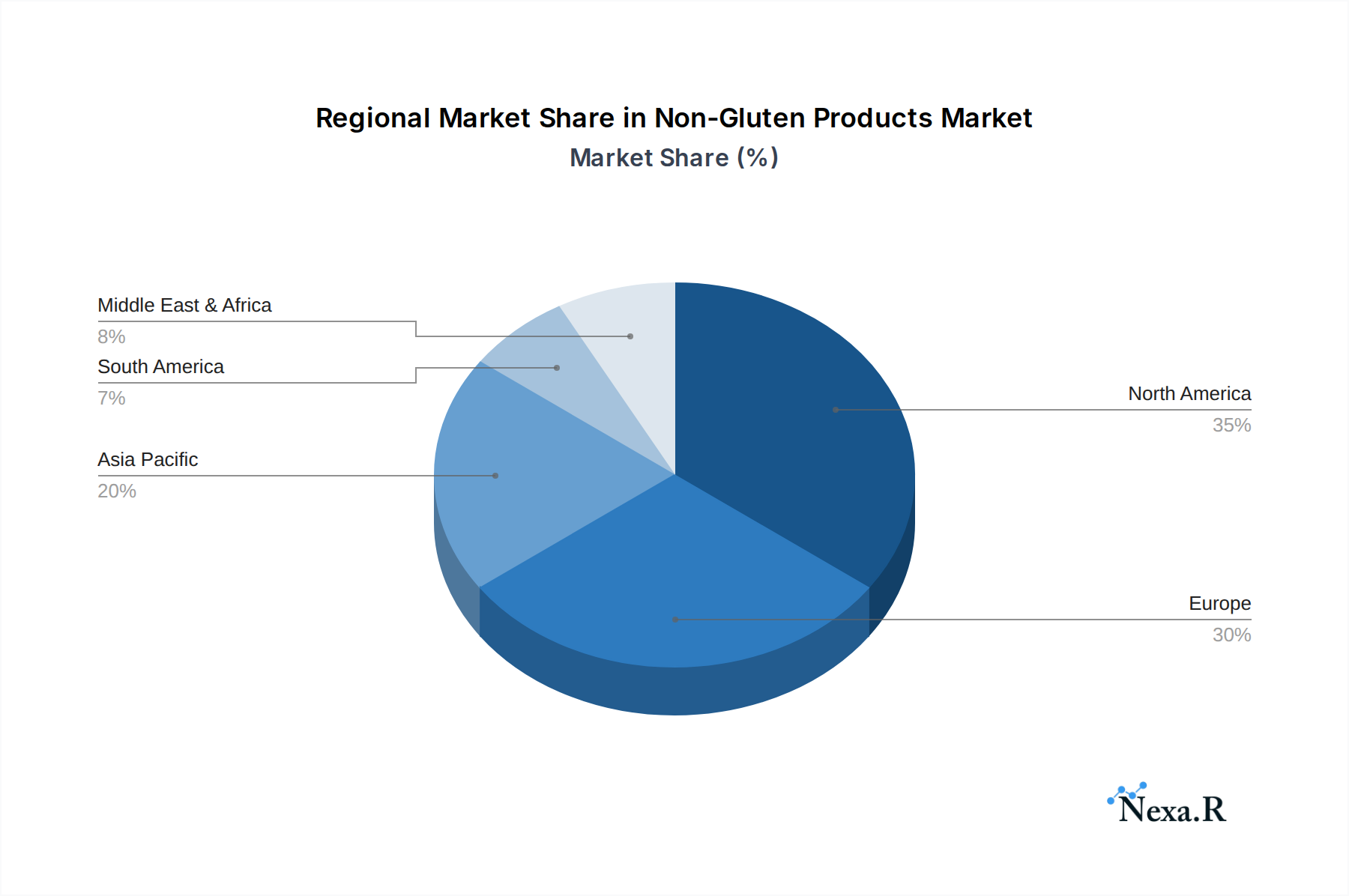

Dominant Regions, Countries, or Segments in Non-Gluten Products

North America currently dominates the global non-gluten products market, primarily driven by the United States and Canada. This dominance is attributed to high consumer awareness regarding gluten-related disorders, advanced healthcare infrastructure facilitating diagnosis, and a strong presence of leading gluten-free product manufacturers. The Application segment of Conventional Stores is the most significant channel, accounting for a substantial market share due to widespread availability and consumer familiarity. However, the Hotels & Restaurants segment is exhibiting rapid growth as culinary establishments increasingly cater to dietary restrictions and preferences, offering a wider array of gluten-free options on their menus.

In terms of Types, Bakery Products hold the largest share within the non-gluten market, encompassing breads, cakes, cookies, and pastries, which have historically been the most challenging to replicate without gluten. This segment is consistently driven by innovation in alternative flours and baking techniques. Pizzas & Pastas are also experiencing significant demand, with an increasing number of brands offering gluten-free versions that rival their traditional counterparts in taste and texture. The Cereals & Snacks category continues to expand as consumers seek convenient and healthy gluten-free breakfast and snacking solutions.

- Dominant Region: North America (particularly the United States and Canada) leads due to high awareness, robust healthcare, and strong industry presence.

- Leading Application Segment: Conventional Stores offer broad accessibility, while Hotels & Restaurants show accelerated growth due to increased demand for inclusive dining.

- Key Type Segment: Bakery Products command the largest share, with ongoing advancements in gluten-free flour blends and baking technologies.

- Growth Drivers: Rising health consciousness, increasing prevalence of celiac disease and gluten sensitivity, and a strong preference for convenient and palatable gluten-free options.

- Market Share: North America accounts for approximately 35% of the global non-gluten products market.

- Growth Potential: Emerging economies in Asia-Pacific and Latin America are showing significant growth potential driven by increasing awareness and market penetration.

Non-Gluten Products Product Landscape

The non-gluten products landscape is characterized by a constant stream of innovative offerings designed to meet diverse consumer needs and preferences. Product innovations focus on enhancing taste, texture, and nutritional profiles while utilizing a variety of gluten-free grains such as rice, corn, quinoa, almond, and tapioca. Key applications range from staple foods like breads and pastas to specialized items such as dairy alternatives, ready-to-eat meals, and premium snacks. Performance metrics are improving, with gluten-free products now comparable in quality and appeal to their gluten-containing counterparts. Unique selling propositions often revolve around allergen-free claims, natural ingredients, and enhanced nutritional value, appealing to a growing segment of health-conscious consumers. Technological advancements are continuously driving the development of novel ingredients and processing methods to further elevate the consumer experience.

Key Drivers, Barriers & Challenges in Non-Gluten Products

The non-gluten products market is propelled by several key drivers. The increasing prevalence of celiac disease and gluten sensitivity globally, coupled with a growing consumer awareness of potential health benefits associated with gluten-free diets, are significant motivators. Technological advancements in ingredient processing and product formulation have drastically improved the taste and texture of gluten-free alternatives, making them more appealing to a wider audience. Furthermore, rising disposable incomes in emerging economies are enabling greater access to specialized food products.

However, the market also faces substantial barriers and challenges. The cost of production for gluten-free products often remains higher than conventional alternatives due to specialized ingredients and manufacturing processes, leading to premium pricing that can limit affordability for some consumers. Maintaining consistent taste and texture, particularly in baked goods, continues to be a technical challenge. Additionally, the potential for cross-contamination during manufacturing and handling poses a significant risk, necessitating stringent quality control measures. Regulatory complexities and varying labeling standards across regions can also present hurdles for manufacturers. Supply chain management for specialized gluten-free ingredients can be intricate, impacting availability and cost.

Emerging Opportunities in Non-Gluten Products

Emerging opportunities within the non-gluten products sector are abundant and diverse. The burgeoning trend of plant-based and allergen-free diets presents a significant avenue for innovation, with opportunities to develop gluten-free products that are also vegan, dairy-free, or soy-free. Untapped markets in developing regions, where awareness is growing but product availability is limited, represent substantial growth potential. The expansion of e-commerce platforms provides a direct-to-consumer channel, allowing for wider reach and personalized product offerings. Furthermore, advancements in personalized nutrition and the development of functional gluten-free foods, enriched with specific vitamins, minerals, or probiotics, are poised to capture the interest of health-conscious consumers.

Growth Accelerators in the Non-Gluten Products Industry

Several catalysts are accelerating the growth of the non-gluten products industry. Technological breakthroughs in alternative flour development, such as the use of ancient grains and novel plant-based proteins, are enhancing the quality and affordability of gluten-free products. Strategic partnerships between ingredient suppliers and food manufacturers are fostering collaborative innovation, leading to improved product formulations and wider market penetration. The increasing demand for convenience is driving the development of ready-to-eat gluten-free meals and on-the-go snack options. Furthermore, aggressive marketing campaigns by leading brands, highlighting the health benefits and delicious taste of their gluten-free offerings, are effectively shaping consumer perception and driving demand.

Key Players Shaping the Non-Gluten Products Market

- Boulder Brands

- DR. SCHÄR AG/SPA

- ENJOY LIFE NATURAL

- General Mills, Inc

- The Hain Celestial Group

- Kraft Heinz

- HERO GROUP AG

- KELKIN LTD

- NQPC

- RAISIO PLC

- Kellogg’s Company

- Big Oz Industries

- Domino’s Pizza

Notable Milestones in Non-Gluten Products Sector

- 2019: Increased focus on clean label and minimally processed gluten-free ingredients.

- 2020: Significant surge in demand for home-baking gluten-free products due to the pandemic.

- 2021: Advancements in plant-based gluten-free protein sources and their incorporation into various food categories.

- 2022: Expansion of gluten-free pizza and pasta options with improved texture and taste profiles.

- 2023: Growing emphasis on sustainability in sourcing and packaging for gluten-free products.

- 2024: Increased investment in R&D for allergen-free and multi-benefit gluten-free functional foods.

In-Depth Non-Gluten Products Market Outlook

The future outlook for the non-gluten products market remains exceptionally promising, driven by a sustained increase in health consciousness and a growing acceptance of gluten-free diets as a lifestyle choice. Growth accelerators, including continuous technological innovation in product formulation and the expansion of distribution channels, will further fuel market expansion. Strategic partnerships and mergers will continue to consolidate the market, bringing more accessible and diverse gluten-free options to consumers worldwide. Emerging opportunities in developing nations and the demand for specialized, functional gluten-free products will pave the way for sustained double-digit growth over the coming decade. The market is expected to witness an increased focus on premiumization, offering high-quality, indulgent gluten-free experiences that rival traditional counterparts.

Non-Gluten Products Segmentation

-

1. Application

- 1.1. Conventional Stores

- 1.2. Hotels & Restaurants

- 1.3. Educational Institutions

- 1.4. Hospitals & Drug Stores

- 1.5. Specialty Services

-

2. Types

- 2.1. Bakery Products

- 2.2. Pizzas & Pastas

- 2.3. Cereals & Snacks

- 2.4. Savories

- 2.5. Others

Non-Gluten Products Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Non-Gluten Products Regional Market Share

Geographic Coverage of Non-Gluten Products

Non-Gluten Products REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Non-Gluten Products Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Conventional Stores

- 5.1.2. Hotels & Restaurants

- 5.1.3. Educational Institutions

- 5.1.4. Hospitals & Drug Stores

- 5.1.5. Specialty Services

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Bakery Products

- 5.2.2. Pizzas & Pastas

- 5.2.3. Cereals & Snacks

- 5.2.4. Savories

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Non-Gluten Products Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Conventional Stores

- 6.1.2. Hotels & Restaurants

- 6.1.3. Educational Institutions

- 6.1.4. Hospitals & Drug Stores

- 6.1.5. Specialty Services

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Bakery Products

- 6.2.2. Pizzas & Pastas

- 6.2.3. Cereals & Snacks

- 6.2.4. Savories

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Non-Gluten Products Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Conventional Stores

- 7.1.2. Hotels & Restaurants

- 7.1.3. Educational Institutions

- 7.1.4. Hospitals & Drug Stores

- 7.1.5. Specialty Services

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Bakery Products

- 7.2.2. Pizzas & Pastas

- 7.2.3. Cereals & Snacks

- 7.2.4. Savories

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Non-Gluten Products Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Conventional Stores

- 8.1.2. Hotels & Restaurants

- 8.1.3. Educational Institutions

- 8.1.4. Hospitals & Drug Stores

- 8.1.5. Specialty Services

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Bakery Products

- 8.2.2. Pizzas & Pastas

- 8.2.3. Cereals & Snacks

- 8.2.4. Savories

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Non-Gluten Products Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Conventional Stores

- 9.1.2. Hotels & Restaurants

- 9.1.3. Educational Institutions

- 9.1.4. Hospitals & Drug Stores

- 9.1.5. Specialty Services

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Bakery Products

- 9.2.2. Pizzas & Pastas

- 9.2.3. Cereals & Snacks

- 9.2.4. Savories

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Non-Gluten Products Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Conventional Stores

- 10.1.2. Hotels & Restaurants

- 10.1.3. Educational Institutions

- 10.1.4. Hospitals & Drug Stores

- 10.1.5. Specialty Services

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Bakery Products

- 10.2.2. Pizzas & Pastas

- 10.2.3. Cereals & Snacks

- 10.2.4. Savories

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Boulder Brands

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 DR. SCHÄR AG/SPA

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 ENJOY LIFE NATURAL

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 General Mills

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Inc

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 The Hain Celestial Group

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Kraft Heinz

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 HERO GROUP AG

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 KELKIN LTD

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 NQPC

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 RAISIO PLC

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Kellogg’s Company

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Big Oz Industries

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Domino’s Pizza

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 Boulder Brands

List of Figures

- Figure 1: Global Non-Gluten Products Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Non-Gluten Products Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Non-Gluten Products Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Non-Gluten Products Volume (K), by Application 2025 & 2033

- Figure 5: North America Non-Gluten Products Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Non-Gluten Products Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Non-Gluten Products Revenue (billion), by Types 2025 & 2033

- Figure 8: North America Non-Gluten Products Volume (K), by Types 2025 & 2033

- Figure 9: North America Non-Gluten Products Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Non-Gluten Products Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Non-Gluten Products Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Non-Gluten Products Volume (K), by Country 2025 & 2033

- Figure 13: North America Non-Gluten Products Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Non-Gluten Products Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Non-Gluten Products Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Non-Gluten Products Volume (K), by Application 2025 & 2033

- Figure 17: South America Non-Gluten Products Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Non-Gluten Products Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Non-Gluten Products Revenue (billion), by Types 2025 & 2033

- Figure 20: South America Non-Gluten Products Volume (K), by Types 2025 & 2033

- Figure 21: South America Non-Gluten Products Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Non-Gluten Products Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Non-Gluten Products Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Non-Gluten Products Volume (K), by Country 2025 & 2033

- Figure 25: South America Non-Gluten Products Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Non-Gluten Products Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Non-Gluten Products Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Non-Gluten Products Volume (K), by Application 2025 & 2033

- Figure 29: Europe Non-Gluten Products Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Non-Gluten Products Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Non-Gluten Products Revenue (billion), by Types 2025 & 2033

- Figure 32: Europe Non-Gluten Products Volume (K), by Types 2025 & 2033

- Figure 33: Europe Non-Gluten Products Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Non-Gluten Products Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Non-Gluten Products Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Non-Gluten Products Volume (K), by Country 2025 & 2033

- Figure 37: Europe Non-Gluten Products Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Non-Gluten Products Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Non-Gluten Products Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Non-Gluten Products Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Non-Gluten Products Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Non-Gluten Products Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Non-Gluten Products Revenue (billion), by Types 2025 & 2033

- Figure 44: Middle East & Africa Non-Gluten Products Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Non-Gluten Products Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Non-Gluten Products Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Non-Gluten Products Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Non-Gluten Products Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Non-Gluten Products Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Non-Gluten Products Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Non-Gluten Products Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Non-Gluten Products Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Non-Gluten Products Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Non-Gluten Products Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Non-Gluten Products Revenue (billion), by Types 2025 & 2033

- Figure 56: Asia Pacific Non-Gluten Products Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Non-Gluten Products Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Non-Gluten Products Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Non-Gluten Products Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Non-Gluten Products Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Non-Gluten Products Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Non-Gluten Products Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Non-Gluten Products Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Non-Gluten Products Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Non-Gluten Products Revenue billion Forecast, by Types 2020 & 2033

- Table 4: Global Non-Gluten Products Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Non-Gluten Products Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Non-Gluten Products Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Non-Gluten Products Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Non-Gluten Products Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Non-Gluten Products Revenue billion Forecast, by Types 2020 & 2033

- Table 10: Global Non-Gluten Products Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Non-Gluten Products Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Non-Gluten Products Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Non-Gluten Products Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Non-Gluten Products Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Non-Gluten Products Revenue billion Forecast, by Types 2020 & 2033

- Table 22: Global Non-Gluten Products Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Non-Gluten Products Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Non-Gluten Products Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Non-Gluten Products Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Non-Gluten Products Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Non-Gluten Products Revenue billion Forecast, by Types 2020 & 2033

- Table 34: Global Non-Gluten Products Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Non-Gluten Products Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Non-Gluten Products Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Non-Gluten Products Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Non-Gluten Products Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Non-Gluten Products Revenue billion Forecast, by Types 2020 & 2033

- Table 58: Global Non-Gluten Products Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Non-Gluten Products Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Non-Gluten Products Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Non-Gluten Products Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Non-Gluten Products Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Non-Gluten Products Revenue billion Forecast, by Types 2020 & 2033

- Table 76: Global Non-Gluten Products Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Non-Gluten Products Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Non-Gluten Products Volume K Forecast, by Country 2020 & 2033

- Table 79: China Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Non-Gluten Products Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Non-Gluten Products Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Non-Gluten Products?

The projected CAGR is approximately 10%.

2. Which companies are prominent players in the Non-Gluten Products?

Key companies in the market include Boulder Brands, DR. SCHÄR AG/SPA, ENJOY LIFE NATURAL, General Mills, Inc, The Hain Celestial Group, Kraft Heinz, HERO GROUP AG, KELKIN LTD, NQPC, RAISIO PLC, Kellogg’s Company, Big Oz Industries, Domino’s Pizza.

3. What are the main segments of the Non-Gluten Products?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.75 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Non-Gluten Products," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Non-Gluten Products report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Non-Gluten Products?

To stay informed about further developments, trends, and reports in the Non-Gluten Products, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence