Key Insights

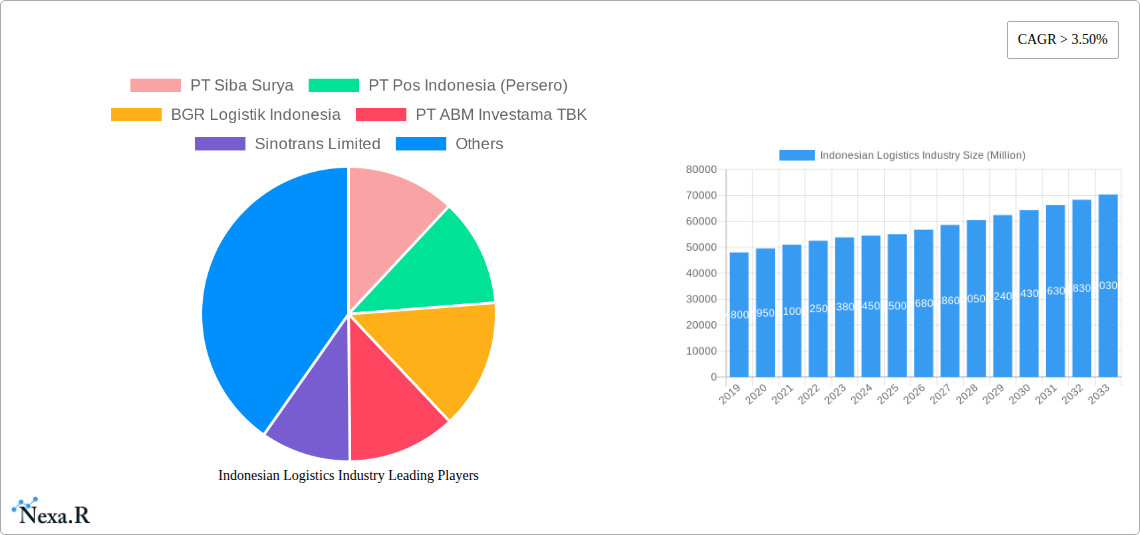

Indonesia's logistics sector is projected for significant growth, supported by a dynamic economy and increasing trade. The market is estimated to reach 72.4 billion by 2025, with a projected Compound Annual Growth Rate (CAGR) of 6.91% through 2033. This expansion is primarily driven by the booming e-commerce sector, demanding advanced last-mile delivery and warehousing. Government investments in infrastructure, including ports, roads, and rail networks, are improving connectivity and streamlining supply chains. Indonesia's deeper integration into global trade and its expanding manufacturing base are also fueling demand for comprehensive logistics solutions.

Indonesian Logistics Industry Market Size (In Billion)

Key demand drivers include the manufacturing, wholesale & retail trade, and construction industries. The market segments include Courier, Express, and Parcel (CEP) services, with international shipments seeing rapid growth due to cross-border e-commerce. Freight forwarding (air and sea) and domestic distribution via road and rail are essential components. Warehousing and storage solutions, including cold chain, are also expanding. Leading players are investing in technology and infrastructure to capitalize on this growth, facing competition from both global and local entities. Emerging trends like AI for route optimization and blockchain for supply chain transparency are enhancing operational efficiency.

Indonesian Logistics Industry Company Market Share

Indonesian Logistics Industry: Market Dynamics, Growth Trends, and Future Outlook (2019-2033)

This comprehensive report provides an in-depth analysis of the Indonesian logistics industry, encompassing market dynamics, growth trajectories, dominant segments, product innovations, key players, and future opportunities. With a study period from 2019-2033, a base and estimated year of 2025, and a forecast period from 2025-2033, this report offers invaluable insights for industry stakeholders. The report is meticulously structured to enhance readability and deliver actionable intelligence, presenting all quantitative values in millions of units.

Indonesian Logistics Industry Market Dynamics & Structure

The Indonesian logistics industry is characterized by a moderately concentrated market, with a growing emphasis on technological innovation driven by the need for efficiency and cost reduction in a vast archipelagic nation. Regulatory frameworks are evolving to support infrastructure development and streamline customs processes, although bureaucratic hurdles remain. Competitive product substitutes are emerging, particularly in warehousing and last-mile delivery, fueled by digital platforms. End-user demographics are diverse, spanning vital sectors like manufacturing, wholesale and retail trade, and increasingly, e-commerce. Mergers and acquisitions (M&A) trends are on the rise as larger players seek to consolidate market share and expand their service portfolios.

- Market Concentration: Dominated by a few large domestic and international players, with a significant presence of medium and small enterprises offering specialized services.

- Technological Innovation Drivers: Digitalization of supply chains, adoption of AI for route optimization, automation in warehousing, and the rise of e-commerce logistics are key drivers.

- Regulatory Frameworks: Government initiatives focusing on infrastructure development (ports, roads), digital trade facilitation, and investment incentives are shaping the industry.

- Competitive Product Substitutes: Growth of third-party logistics (3PL) providers, specialized cold chain solutions, and on-demand delivery platforms.

- End-User Demographics: Strong demand from the manufacturing sector for inbound and outbound logistics, robust activity in wholesale and retail trade, and exponential growth in e-commerce fulfillment.

- M&A Trends: Strategic acquisitions are focused on expanding geographical reach, integrating technology, and diversifying service offerings, particularly in the Courier, Express, and Parcel (CEP) segment. The volume of M&A deals is expected to increase by approximately 15% from the historical period to the forecast period.

Indonesian Logistics Industry Growth Trends & Insights

The Indonesian logistics industry is poised for significant growth, driven by a burgeoning economy, increasing domestic consumption, and the government's focus on improving connectivity. The market size is projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 8.5% during the forecast period. Adoption rates of advanced logistics technologies, such as Warehouse Management Systems (WMS) and Transportation Management Systems (TMS), are steadily increasing, enhancing operational efficiency. Technological disruptions, including the widespread use of IoT devices for real-time tracking and data analytics, are transforming supply chain visibility. Shifts in consumer behavior, characterized by a strong preference for faster delivery and enhanced tracking capabilities, are compelling logistics providers to innovate their service offerings. The increasing penetration of e-commerce is a major catalyst for growth in the CEP segment.

- Market Size Evolution: The Indonesian logistics market is expected to grow from an estimated value of $50,000 million in 2025 to over $85,000 million by 2033, reflecting robust expansion.

- Adoption Rates: Adoption of digital logistics solutions is projected to rise by 20% year-on-year, particularly in large enterprises.

- Technological Disruptions: IoT, AI-powered analytics, and blockchain technology are being integrated to optimize inventory management, predict demand, and enhance security.

- Consumer Behavior Shifts: Demand for same-day and next-day delivery, real-time tracking, and convenient return policies are influencing service design and operational strategies. The e-commerce penetration rate is forecasted to reach 30% by 2027, directly impacting the CEP segment.

Dominant Regions, Countries, or Segments in Indonesian Logistics Industry

The Wholesale and Retail Trade segment is currently the dominant end-user industry driving growth in the Indonesian logistics sector. This dominance is primarily attributed to the country's large population, increasing urbanization, and the explosive growth of e-commerce. Jakarta, as the economic and commercial hub, stands out as the most dominant region, followed by other major industrial centers like Surabaya and Bandung. Within the logistics functions, the Courier, Express, and Parcel (CEP) segment, particularly for Domestic deliveries, exhibits the most significant growth and market share.

- Dominant End-User Industry: Wholesale and Retail Trade

- Market Share: Accounts for an estimated 35% of the total logistics demand.

- Key Drivers: Rapid e-commerce expansion, rising disposable incomes, and a growing middle class fueling consumer spending.

- Growth Potential: Significant, driven by continued digital transformation and penetration into tier-2 and tier-3 cities.

- Dominant Logistics Function: Courier, Express, and Parcel (CEP) - Domestic

- Market Share: Represents approximately 40% of the logistics services market.

- Key Drivers: E-commerce fulfillment, same-day and next-day delivery expectations, and the need for efficient last-mile solutions across the archipelago.

- Growth Potential: Extremely high, with an anticipated CAGR of 12% for the next decade.

- Dominant Region: Jakarta

- Market Share: Generates over 40% of the total logistics revenue in Indonesia.

- Key Drivers: Concentration of businesses, major ports and airports, robust infrastructure, and a large consumer base.

- Growth Potential: Continues to be a major growth engine, with ongoing infrastructure upgrades and a thriving business ecosystem.

- Other Contributing Segments:

- Manufacturing: Remains a crucial segment, requiring efficient inbound and outbound logistics for raw materials and finished goods. Expected to contribute 25% of the logistics demand.

- Freight Forwarding (Sea): Essential for international trade, handling significant volumes of goods, particularly manufactured products and raw materials. Expected to maintain a 20% share.

Indonesian Logistics Industry Product Landscape

The Indonesian logistics industry is witnessing a surge in innovative product offerings aimed at enhancing efficiency, transparency, and customer satisfaction. These include advanced Warehouse Management Systems (WMS) offering real-time inventory tracking and automated picking, and Transportation Management Systems (TMS) optimizing route planning and fleet management. The Courier, Express, and Parcel (CEP) segment is characterized by the introduction of eco-friendly delivery options and smart lockers for convenient parcel pickup. Freight forwarding services are increasingly integrated with digital platforms, providing end-to-end visibility and streamlined documentation. Warehousing solutions are evolving with the introduction of smart, temperature-controlled facilities catering to the growing demand for pharmaceuticals and perishable goods.

Key Drivers, Barriers & Challenges in Indonesian Logistics Industry

Key Drivers:

- Economic Growth and E-commerce Boom: Indonesia's robust economic expansion and the exponential growth of its e-commerce sector are significant drivers, increasing demand for logistics services across all segments.

- Government Infrastructure Investment: The government's commitment to developing ports, roads, and digital infrastructure is crucial for improving connectivity and reducing transit times.

- Technological Adoption: Increasing investment in digital logistics solutions, automation, and data analytics enhances efficiency and reduces operational costs.

- Growing Middle Class and Urbanization: This demographic shift fuels consumer spending, particularly on goods requiring efficient distribution networks.

Barriers & Challenges:

- Geographical Complexity: The archipelagic nature of Indonesia presents significant challenges in terms of connectivity, last-mile delivery, and infrastructure development across scattered islands.

- Infrastructure Gaps: Despite improvements, significant disparities in infrastructure quality and accessibility exist, particularly outside major urban centers.

- Regulatory Hurdles and Bureaucracy: Complex customs procedures, differing regional regulations, and bureaucratic inefficiencies can lead to delays and increased costs.

- Talent Shortage: A lack of skilled logistics professionals, particularly in areas like supply chain management and advanced technology, hinders industry growth and innovation.

- High Operating Costs: Fuel prices, vehicle maintenance, and fragmented logistics networks contribute to higher operating costs compared to more developed markets. The operational cost for road freight is estimated to be 15% higher than regional averages due to these factors.

Emerging Opportunities in Indonesian Logistics Industry

Emerging opportunities in the Indonesian logistics industry lie in the expansion of cold chain logistics to cater to the growing pharmaceutical and food & beverage sectors, with an estimated market potential of $5,000 million. The development of integrated logistics hubs and special economic zones offers streamlined operations and incentives for investors. There is significant potential in leveraging technology for optimizing inter-island shipping and developing efficient last-mile delivery solutions in remote areas. Furthermore, the demand for sustainable logistics practices, including green transportation and energy-efficient warehousing, presents a growing niche. The "Other Services" category, including reverse logistics and value-added services, is also an untapped market with significant growth potential.

Growth Accelerators in the Indonesian Logistics Industry Industry

Growth in the Indonesian logistics industry is being accelerated by several key factors. Strategic partnerships between domestic and international players are crucial for knowledge transfer and market expansion, exemplified by the increasing number of joint ventures. Technological breakthroughs in AI for predictive analytics and blockchain for supply chain transparency are enhancing operational efficiency and trust. Market expansion strategies, including the penetration into underserved regions and the development of specialized logistics solutions for emerging industries, are also significant accelerators. The continuous government support through policy reforms and investment in digital infrastructure acts as a foundational growth accelerator.

Key Players Shaping the Indonesian Logistics Industry Market

- PT Siba Surya

- PT Pos Indonesia (Persero)

- BGR Logistik Indonesia

- PT ABM Investama TBK

- Sinotrans Limited

- PT Lautan Luas TBK

- United Parcel Service of America Inc (UPS)

- PT Satria Antaran Prima Tbk (SAPX Express)

- PT Samudera Indonesia Tangguh

- NYK (Nippon Yusen Kaisha) Line

- DHL Group

- LOGWIN

- DSV A/S (De Sammensluttede Vognmænd af Air and Sea)

- FedEx

- PT Repex Wahana (RPX)

- Puninar Logistics

- PT Bina Sinar Amity (BSA Logistics Indonesia)

- Kuehne + Nagel

- Pancaran Group

- PT Kamadjaja Logistics

- Linfox Pty Ltd

- Agility Public Warehousing Company K S C P

- PT Soechi Lines Tbk

- PT Cardig International

- PT Jalur Nugraha Ekakurir (JNE Express)

- PT Citrabati Logistik International

- PT Pandu Siwi Group (Pandu Logistics)

- PT Dunia Express Transindo

- Ninja Logistics

- DB Schenker (PT Schenker Logistics Indonesia)

- Expeditors International of Washington Inc

- Kerry Logistics Network Limited

Notable Milestones in Indonesian Logistics Industry Sector

- March 2024: Kerry Logistics Network Limited acquired a majority stake in Business By Air SAS ('BBA'), an upstream supply chain specialist in air freight services for diverse industrial clients in verticals including automotive, aerospace and pharmaceutical, as well as an established player in the African market, to strengthen KLN's position in the EMEA region and international freight forwarding ('IFF') capabilities across the globe. This move is expected to enhance KLN's global reach and capabilities in specialized air freight.

- January 2024: DHL Express commenced services for the final Boeing 777 freighter deployed at the South Asia Hub in Singapore. With a payload capability of 102 tons, the aircraft joins four other Boeing 777 freighters already deployed in Singapore to boost inter-continental connectivity between the Asia Pacific and the Americas. This expansion significantly increases DHL's air freight capacity by 1,224 tons, meeting growing international express shipping demand.

- January 2024: Kuehne + Nagel announced its Book & Claim insetting solution for electric vehicles, to improve its decarbonization solutions. Developing Book & Claim insetting solutions for road freight was a strategic priority for Kuehne + Nagel. Customers who use Kuehne + Nagel's road transport services can now claim the carbon reductions of electric trucks when it is not possible to physically move their goods on these vehicles. This innovation addresses growing demand for sustainable logistics.

In-Depth Indonesian Logistics Industry Market Outlook

The Indonesian logistics industry is on a strong growth trajectory, driven by the digital economy and government support for infrastructure. Future market potential is immense, particularly in optimizing inter-island connectivity and developing specialized logistics for high-growth sectors like e-commerce and cold chain. Strategic opportunities lie in the adoption of advanced technologies such as AI and IoT for enhanced supply chain visibility and efficiency, and the development of sustainable logistics solutions to meet global environmental standards. Continued investment in digital infrastructure, coupled with supportive policy frameworks, will be pivotal in realizing this potential and solidifying Indonesia's position as a regional logistics powerhouse. The market is projected to grow at a CAGR of 8.5% from 2025-2033.

Indonesian Logistics Industry Segmentation

-

1. End User Industry

- 1.1. Agriculture, Fishing, and Forestry

- 1.2. Construction

- 1.3. Manufacturing

- 1.4. Oil and Gas, Mining and Quarrying

- 1.5. Wholesale and Retail Trade

- 1.6. Others

-

2. Logistics Function

-

2.1. Courier, Express, and Parcel (CEP)

-

2.1.1. By Destination Type

- 2.1.1.1. Domestic

- 2.1.1.2. International

-

2.1.1. By Destination Type

-

2.2. Freight Forwarding

-

2.2.1. By Mode Of Transport

- 2.2.1.1. Air

- 2.2.1.2. Sea and Inland Waterways

- 2.2.1.3. Others

-

2.2.1. By Mode Of Transport

-

2.3. Freight Transport

- 2.3.1. Pipelines

- 2.3.2. Rail

- 2.3.3. Road

-

2.4. Warehousing and Storage

-

2.4.1. By Temperature Control

- 2.4.1.1. Non-Temperature Controlled

-

2.4.1. By Temperature Control

- 2.5. Other Services

-

2.1. Courier, Express, and Parcel (CEP)

Indonesian Logistics Industry Segmentation By Geography

- 1. Indonesia

Indonesian Logistics Industry Regional Market Share

Geographic Coverage of Indonesian Logistics Industry

Indonesian Logistics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.91% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Agriculture, Fishing, and Forestry

- 5.1.2. Construction

- 5.1.3. Manufacturing

- 5.1.4. Oil and Gas, Mining and Quarrying

- 5.1.5. Wholesale and Retail Trade

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Logistics Function

- 5.2.1. Courier, Express, and Parcel (CEP)

- 5.2.1.1. By Destination Type

- 5.2.1.1.1. Domestic

- 5.2.1.1.2. International

- 5.2.1.1. By Destination Type

- 5.2.2. Freight Forwarding

- 5.2.2.1. By Mode Of Transport

- 5.2.2.1.1. Air

- 5.2.2.1.2. Sea and Inland Waterways

- 5.2.2.1.3. Others

- 5.2.2.1. By Mode Of Transport

- 5.2.3. Freight Transport

- 5.2.3.1. Pipelines

- 5.2.3.2. Rail

- 5.2.3.3. Road

- 5.2.4. Warehousing and Storage

- 5.2.4.1. By Temperature Control

- 5.2.4.1.1. Non-Temperature Controlled

- 5.2.4.1. By Temperature Control

- 5.2.5. Other Services

- 5.2.1. Courier, Express, and Parcel (CEP)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Indonesia

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. Indonesian Logistics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 6.1.1. Agriculture, Fishing, and Forestry

- 6.1.2. Construction

- 6.1.3. Manufacturing

- 6.1.4. Oil and Gas, Mining and Quarrying

- 6.1.5. Wholesale and Retail Trade

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Logistics Function

- 6.2.1. Courier, Express, and Parcel (CEP)

- 6.2.1.1. By Destination Type

- 6.2.1.1.1. Domestic

- 6.2.1.1.2. International

- 6.2.1.1. By Destination Type

- 6.2.2. Freight Forwarding

- 6.2.2.1. By Mode Of Transport

- 6.2.2.1.1. Air

- 6.2.2.1.2. Sea and Inland Waterways

- 6.2.2.1.3. Others

- 6.2.2.1. By Mode Of Transport

- 6.2.3. Freight Transport

- 6.2.3.1. Pipelines

- 6.2.3.2. Rail

- 6.2.3.3. Road

- 6.2.4. Warehousing and Storage

- 6.2.4.1. By Temperature Control

- 6.2.4.1.1. Non-Temperature Controlled

- 6.2.4.1. By Temperature Control

- 6.2.5. Other Services

- 6.2.1. Courier, Express, and Parcel (CEP)

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 PT Siba Surya

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 PT Pos Indonesia (Persero)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 BGR Logistik Indonesia

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 PT ABM Investama TBK

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Sinotrans Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 PT Lautan Luas TBK

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 United Parcel Service of America Inc (UPS

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 PT Satria Antaran Prima Tbk (SAPX Express)

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 PT Samudera Indonesia Tangguh

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 NYK (Nippon Yusen Kaisha) Line

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 DHL Group

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 LOGWIN

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 DSV A/S (De Sammensluttede Vognmænd af Air and Sea)

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 FedEx

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 PT Repex Wahana (RPX)

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Puninar Logistics

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 PT Bina Sinar Amity (BSA Logistics Indonesia)

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.18 Kuehne + Nagel

- 7.1.18.1. Company Overview

- 7.1.18.2. Products

- 7.1.18.3. Company Financials

- 7.1.18.4. SWOT Analysis

- 7.1.19 Pancaran Group

- 7.1.19.1. Company Overview

- 7.1.19.2. Products

- 7.1.19.3. Company Financials

- 7.1.19.4. SWOT Analysis

- 7.1.20 PT Kamadjaja Logistics

- 7.1.20.1. Company Overview

- 7.1.20.2. Products

- 7.1.20.3. Company Financials

- 7.1.20.4. SWOT Analysis

- 7.1.21 Linfox Pty Ltd

- 7.1.21.1. Company Overview

- 7.1.21.2. Products

- 7.1.21.3. Company Financials

- 7.1.21.4. SWOT Analysis

- 7.1.22 Agility Public Warehousing Company K S C P

- 7.1.22.1. Company Overview

- 7.1.22.2. Products

- 7.1.22.3. Company Financials

- 7.1.22.4. SWOT Analysis

- 7.1.23 PT Soechi Lines Tbk

- 7.1.23.1. Company Overview

- 7.1.23.2. Products

- 7.1.23.3. Company Financials

- 7.1.23.4. SWOT Analysis

- 7.1.24 PT Cardig International

- 7.1.24.1. Company Overview

- 7.1.24.2. Products

- 7.1.24.3. Company Financials

- 7.1.24.4. SWOT Analysis

- 7.1.25 PT Jalur Nugraha Ekakurir (JNE Express)

- 7.1.25.1. Company Overview

- 7.1.25.2. Products

- 7.1.25.3. Company Financials

- 7.1.25.4. SWOT Analysis

- 7.1.26 PT Citrabati Logistik International

- 7.1.26.1. Company Overview

- 7.1.26.2. Products

- 7.1.26.3. Company Financials

- 7.1.26.4. SWOT Analysis

- 7.1.27 PT Pandu Siwi Group (Pandu Logistics)

- 7.1.27.1. Company Overview

- 7.1.27.2. Products

- 7.1.27.3. Company Financials

- 7.1.27.4. SWOT Analysis

- 7.1.28 PT Dunia Express Transindo

- 7.1.28.1. Company Overview

- 7.1.28.2. Products

- 7.1.28.3. Company Financials

- 7.1.28.4. SWOT Analysis

- 7.1.29 Ninja Logistics

- 7.1.29.1. Company Overview

- 7.1.29.2. Products

- 7.1.29.3. Company Financials

- 7.1.29.4. SWOT Analysis

- 7.1.30 DB Schenker (PT Schenker Logistics Indonesia)

- 7.1.30.1. Company Overview

- 7.1.30.2. Products

- 7.1.30.3. Company Financials

- 7.1.30.4. SWOT Analysis

- 7.1.31 Expeditors International of Washington Inc

- 7.1.31.1. Company Overview

- 7.1.31.2. Products

- 7.1.31.3. Company Financials

- 7.1.31.4. SWOT Analysis

- 7.1.32 Kerry Logistics Network Limited

- 7.1.32.1. Company Overview

- 7.1.32.2. Products

- 7.1.32.3. Company Financials

- 7.1.32.4. SWOT Analysis

- 7.1.1 PT Siba Surya

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Indonesian Logistics Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Indonesian Logistics Industry Share (%) by Company 2025

List of Tables

- Table 1: Indonesian Logistics Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 2: Indonesian Logistics Industry Revenue billion Forecast, by Logistics Function 2020 & 2033

- Table 3: Indonesian Logistics Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Indonesian Logistics Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 5: Indonesian Logistics Industry Revenue billion Forecast, by Logistics Function 2020 & 2033

- Table 6: Indonesian Logistics Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indonesian Logistics Industry?

The projected CAGR is approximately 6.91%.

2. Which companies are prominent players in the Indonesian Logistics Industry?

Key companies in the market include PT Siba Surya, PT Pos Indonesia (Persero), BGR Logistik Indonesia, PT ABM Investama TBK, Sinotrans Limited, PT Lautan Luas TBK, United Parcel Service of America Inc (UPS, PT Satria Antaran Prima Tbk (SAPX Express), PT Samudera Indonesia Tangguh, NYK (Nippon Yusen Kaisha) Line, DHL Group, LOGWIN, DSV A/S (De Sammensluttede Vognmænd af Air and Sea), FedEx, PT Repex Wahana (RPX), Puninar Logistics, PT Bina Sinar Amity (BSA Logistics Indonesia), Kuehne + Nagel, Pancaran Group, PT Kamadjaja Logistics, Linfox Pty Ltd, Agility Public Warehousing Company K S C P, PT Soechi Lines Tbk, PT Cardig International, PT Jalur Nugraha Ekakurir (JNE Express), PT Citrabati Logistik International, PT Pandu Siwi Group (Pandu Logistics), PT Dunia Express Transindo, Ninja Logistics, DB Schenker (PT Schenker Logistics Indonesia), Expeditors International of Washington Inc, Kerry Logistics Network Limited.

3. What are the main segments of the Indonesian Logistics Industry?

The market segments include End User Industry, Logistics Function.

4. Can you provide details about the market size?

The market size is estimated to be USD 72.4 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing volume of international trade4.; The rise of trade agreements between nations.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

4.; Surge in fuel costs affecting the market4.; Increasing trade tension.

8. Can you provide examples of recent developments in the market?

March 2024: Kerry Logistics Network Limited had acquired a majority stake in Business By Air SAS ('BBA'), an upstream supply chain specialist in air freight services for diverse industrial clients in verticals including automotive, aerospace and pharmaceutical, as well as an established player in the African market, to strengthen KLN's position in the EMEA region and international freight forwarding ('IFF') capabilities across the globe.January 2024: DHL Express has commenced services for the final Boeing 777 freighter deployed at the South Asia Hub in Singapore. With a payload capability of 102 tons, the aircraft joins the four other Boeing 777 freighters already deployed in Singapore to boost inter-continental connectivity between the Asia Pacific and the Americas. Sporting a dual DHL-Singapore Airlines (SIA) livery, these five freighters provide a total of 1,224 tons of payload capacity to meet growing customer demand for international express shipping services.January 2024: Kuehne + Nagel has announced its Book & Claim insetting solution for electric vehicles, to improve its decarbonization solutions. Developing Book & Claim insetting solutions for road freight was a strategic priority for Kuehne + Nagel. Customers who use Kuehne + Nagel's road transport services can now claim the carbon reductions of electric trucks when it is not possible to physically move their goods on these vehicles.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indonesian Logistics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indonesian Logistics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indonesian Logistics Industry?

To stay informed about further developments, trends, and reports in the Indonesian Logistics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence