Key Insights

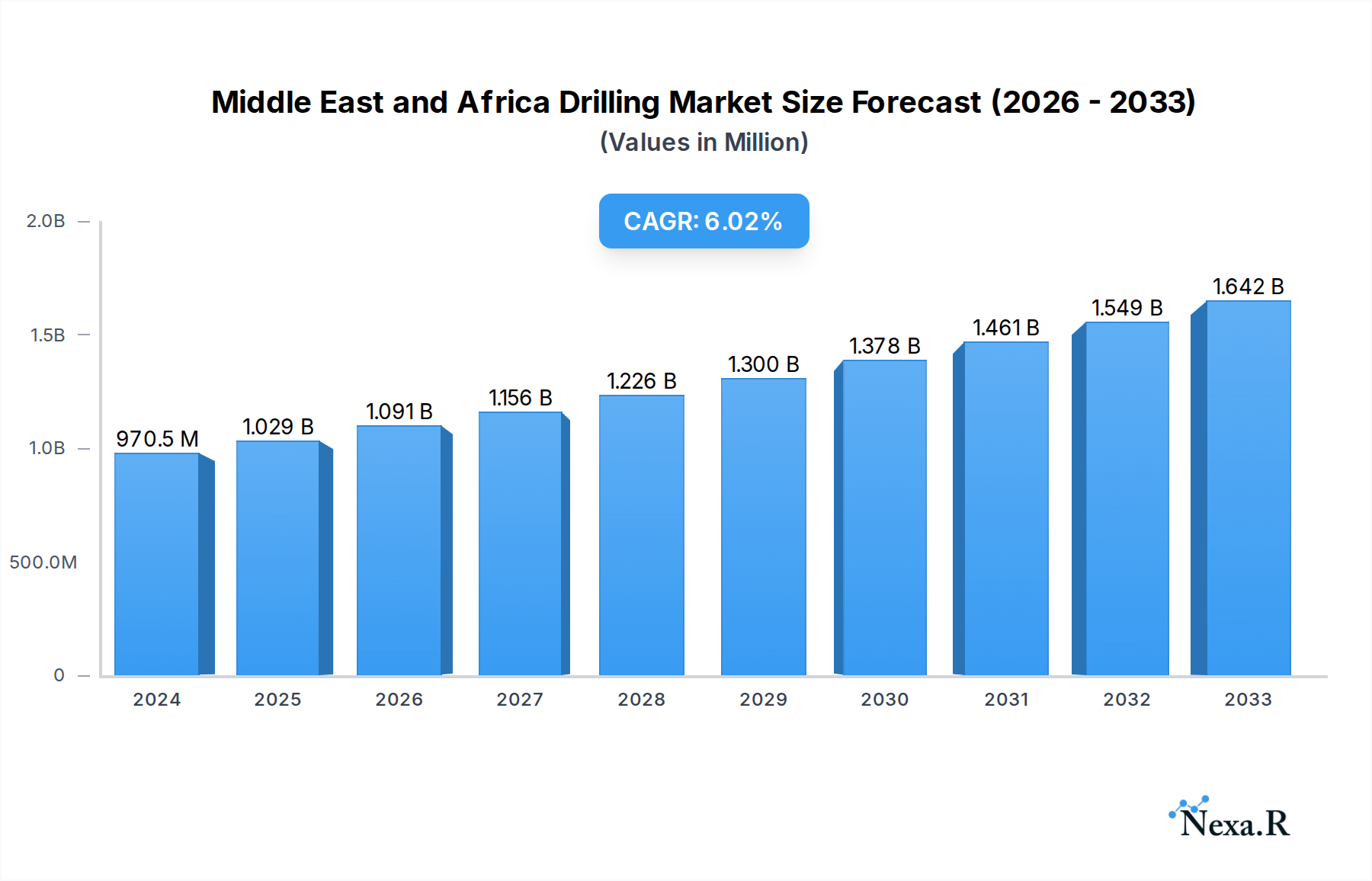

The Middle East and Africa (MEA) drilling market is poised for robust expansion, driven by a confluence of factors including increasing energy demand, significant investments in oil and gas exploration, and the strategic importance of the region in global energy supply. In 2024, the market is estimated at USD 970.5 million, and is projected to witness a Compound Annual Growth Rate (CAGR) of 6% from 2025 to 2033. This sustained growth is largely fueled by the region's vast hydrocarbon reserves and ongoing efforts to enhance production capacity and explore new frontiers, particularly in offshore and onshore domains. Companies are investing heavily in advanced drilling technologies and operational efficiencies to tap into these resources more effectively and sustainably. The Middle East, with its dominant position in global oil production, is a primary engine for this market's dynamism, while other regions like South Africa are also seeing increased activity due to their own energy needs and resource potential.

Middle East and Africa Drilling Market Market Size (In Million)

The MEA drilling market is characterized by a strategic shift towards optimizing existing assets and exploring deeper and more complex reserves. Key trends include the adoption of digitalization and automation in drilling operations, leading to improved safety, efficiency, and cost-effectiveness. Investments in enhanced oil recovery (EOR) techniques and the development of unconventional resources are also contributing to market expansion. However, the market faces certain restraints, including geopolitical instabilities in specific sub-regions, stringent environmental regulations, and fluctuating crude oil prices that can impact capital expenditure. Despite these challenges, the inherent energy wealth of the MEA region, coupled with a growing population and industrialization, ensures a persistent demand for drilling services, making it a crucial and dynamic sector within the global energy landscape.

Middle East and Africa Drilling Market Company Market Share

Middle East and Africa Drilling Market Report: Comprehensive Analysis and Future Outlook (2019–2033)

This report offers an in-depth analysis of the Middle East and Africa (MEA) Drilling Market, a dynamic sector crucial for energy production. Covering the period from 2019 to 2033, with a base year of 2025, this study provides invaluable insights into market size, growth trends, competitive landscape, and future opportunities. We analyze key segments including Onshore and Offshore drilling, and regional hotspots like Saudi Arabia, United Arab Emirates, and South Africa. Essential for oil and gas operators, drilling contractors, equipment manufacturers, and investors, this report equips you with the data and foresight needed to navigate this evolving market. Discover market dynamics, technological innovations, and strategic imperatives for success in the MEA drilling arena.

Middle East and Africa Drilling Market Market Dynamics & Structure

The Middle East and Africa (MEA) Drilling Market exhibits a moderately consolidated structure, with a few dominant players controlling a significant share of the onshore drilling and offshore drilling segments. Technological innovation is primarily driven by the increasing demand for efficient and cost-effective exploration and production (E&P) activities. Advanced drilling techniques, such as hydraulic fracturing, directional drilling, and managed pressure drilling (MPD), are gaining traction across the region. Regulatory frameworks, while evolving, often prioritize local content development and environmental impact assessments. Competitive product substitutes are limited in core drilling services, but advancements in automation and digitalization are emerging as disruptors. End-user demographics are dominated by national oil companies (NOCs) and international oil companies (IOCs) seeking to enhance their hydrocarbon reserves. Mergers and acquisitions (M&A) trends are moderately active, driven by the pursuit of economies of scale and access to new technologies and markets. For instance, recent M&A activities have focused on consolidating drilling rig fleets and specialized service providers.

- Market Concentration: Moderately concentrated, with key players like Schlumberger Limited, Baker Hughes Company, and Weatherford International PLC holding significant market shares.

- Technological Innovation Drivers: Demand for enhanced oil recovery (EOR), exploration of challenging reserves (deepwater, unconventional), and digitalization for operational efficiency.

- Regulatory Frameworks: Increasing emphasis on environmental sustainability, local content policies, and adherence to international safety standards.

- Competitive Product Substitutes: Limited direct substitutes for core drilling services, but automation and digital solutions are enhancing operational efficiency and reducing reliance on certain manual processes.

- End-User Demographics: Predominantly NOCs such as Saudi Aramco Oil Co. and ADES International Holding, alongside IOCs like CNOOC International Ltd. and Total Energies.

- M&A Trends: Focus on strategic partnerships, acquisitions of specialized service providers, and consolidation to enhance fleet utilization and service capabilities.

Middle East and Africa Drilling Market Growth Trends & Insights

The Middle East and Africa Drilling Market is poised for substantial growth, driven by persistent global energy demand and significant untapped hydrocarbon reserves. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of approximately XX% from the base year 2025 through 2033. This expansion is fueled by substantial investments in exploration and production activities, particularly in the onshore drilling sector which currently holds a larger market share but is expected to see robust growth in its offshore drilling counterpart. The adoption rate of advanced drilling technologies, including automated drilling systems and data analytics for real-time decision-making, is accelerating. Technological disruptions are centered around improving drilling efficiency, reducing operational costs, and minimizing environmental impact. For example, the implementation of AI-powered predictive maintenance for drilling equipment is becoming more prevalent. Consumer behavior shifts are observed in the increasing preference for integrated drilling services and sustainable operational practices. The market penetration of unconventional drilling techniques, while still nascent in some parts of MEA, is expected to grow. The robust reserve base in countries like Saudi Arabia and the UAE continues to be a primary driver, with ongoing projects to maximize production from existing fields and explore new frontiers. The demand for offshore drilling is also on the rise, particularly in deeper waters, as companies seek to exploit newly discovered reserves. This necessitates the deployment of sophisticated drillships and subsea technologies. The historical data from 2019-2024 indicates a fluctuating trend influenced by global oil prices and geopolitical events, but the underlying demand for energy has remained a constant. Looking forward, strategic investments in infrastructure and a favorable regulatory environment in key MEA nations will further catalyze market expansion. The focus on technological advancements aims to unlock more challenging reserves and improve the overall economics of E&P operations.

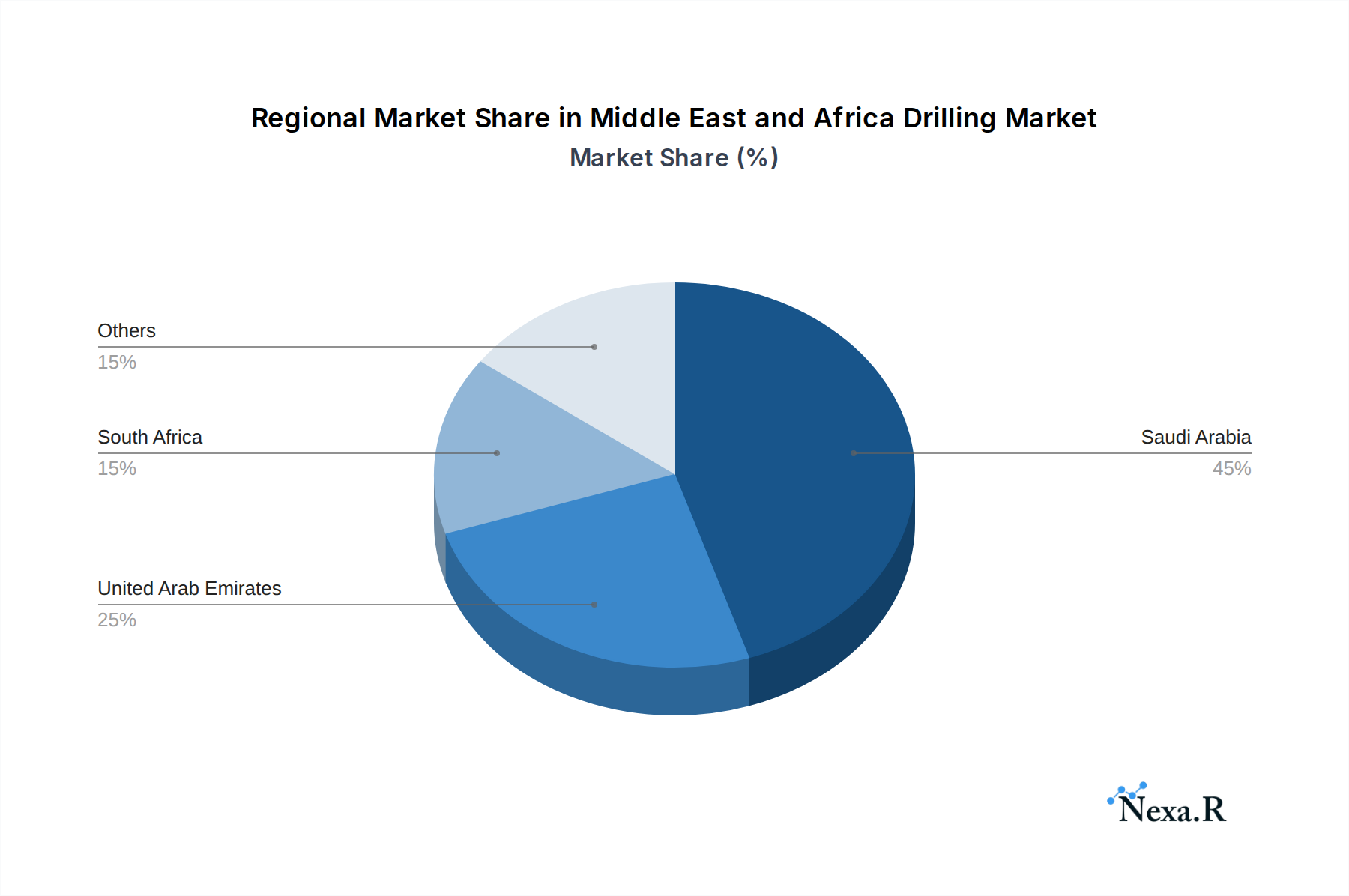

Dominant Regions, Countries, or Segments in Middle East and Africa Drilling Market

The Saudi Arabia segment within the Middle East and Africa Drilling Market is the undeniable dominant force, significantly outpacing other regions and segments in terms of market share and projected growth. This dominance is underpinned by the Kingdom's vast proven hydrocarbon reserves and its strategic imperative to maintain its position as a leading global oil producer. The country’s commitment to large-scale E&P projects, coupled with consistent government support for the oil and gas sector, makes it a prime destination for drilling activities. Both onshore drilling and offshore drilling operations in Saudi Arabia are extensive, with massive investments directed towards enhancing production capacity and exploring new fields.

- Dominant Country: Saudi Arabia leads the MEA Drilling Market due to its immense hydrocarbon reserves and strategic production policies.

- Market Share: Estimated to hold over XX% of the total MEA drilling market share by 2025.

- Growth Potential: Driven by aggressive production targets and significant investments in upstream activities.

- Key Drivers: National transformation plans, ongoing mega-projects, and a focus on maintaining oil market stability.

- Onshore Drilling Dominance: While offshore operations are significant, onshore activities in Saudi Arabia, particularly in the Ghawar field, represent the largest portion of drilling expenditure.

- Infrastructure: Extensive existing infrastructure and continuous development of new well pads and associated facilities.

- Technological Adoption: High adoption rates for advanced onshore drilling techniques to maximize recovery and efficiency.

- Offshore Drilling Expansion: The UAE, with its significant offshore reserves in the Persian Gulf, is a strong contender and shows substantial growth potential, particularly in shallow and deep-water exploration.

- Market Share: Estimated to contribute XX% to the MEA drilling market by 2025.

- Key Drivers: Strategic diversification of energy sources and expansion into offshore gas fields.

- South Africa's Emerging Role: While currently a smaller contributor, South Africa's offshore potential, particularly in deep-water exploration, presents significant long-term growth opportunities, attracting major international players.

- Growth Potential: Driven by exploratory drilling and potential discoveries in its vast offshore basins.

- Challenges: Regulatory hurdles and environmental concerns are key factors influencing the pace of development.

Middle East and Africa Drilling Market Product Landscape

The Middle East and Africa Drilling Market is characterized by a robust landscape of advanced drilling equipment and specialized services. Innovations are focused on enhancing efficiency, safety, and environmental compliance. Key product categories include drilling rigs (both onshore and offshore, including jack-ups, semi-submersibles, and drillships), drill bits, drilling fluids, casing, tubing, and cementing services. Performance metrics are continually being pushed by technological advancements, leading to faster drilling speeds, improved wellbore integrity, and reduced non-productive time (NPT). Unique selling propositions often revolve around automation, digitalization, and the ability to operate in extreme conditions, such as high-pressure, high-temperature (HPHT) environments and ultra-deep waters.

Key Drivers, Barriers & Challenges in Middle East and Africa Drilling Market

Key Drivers:

- Vast Hydrocarbon Reserves: The region possesses some of the world's largest proven oil and gas reserves, driving sustained exploration and production efforts.

- Global Energy Demand: Continued reliance on oil and gas for global energy needs fuels investment in drilling activities.

- Technological Advancements: Adoption of advanced drilling techniques like directional drilling, MPD, and automation enhances efficiency and cost-effectiveness.

- Government Support and Investment: Favorable policies and significant capital investment from national oil companies (NOCs) in key MEA nations.

Barriers & Challenges:

- Geopolitical Instability: Regional conflicts and political uncertainties can disrupt operations and deter investment.

- Price Volatility: Fluctuations in global oil and gas prices directly impact drilling budgets and project feasibility.

- Environmental Regulations: Increasing stringency of environmental regulations and the growing pressure for sustainable practices.

- Skilled Workforce Shortages: A persistent challenge in finding and retaining qualified personnel for complex drilling operations.

- Infrastructure Limitations: In certain remote onshore and deepwater offshore locations, infrastructure development remains a significant hurdle.

- Supply Chain Disruptions: Global and regional supply chain issues can impact the availability of equipment and specialized services, leading to project delays and cost overruns.

Emerging Opportunities in Middle East and Africa Drilling Market

Emerging opportunities in the MEA Drilling Market lie in the exploration of unconventional resources, particularly shale gas, and the development of complex offshore fields in deeper waters. The increasing focus on decarbonization is also creating opportunities for drilling technologies that support carbon capture, utilization, and storage (CCUS) projects. Furthermore, digitalization and AI are opening avenues for enhanced operational efficiency, predictive maintenance, and optimized drilling performance. Untapped markets in sub-Saharan Africa, with their nascent but significant resource potential, represent a substantial growth frontier.

Growth Accelerators in the Middle East and Africa Drilling Market Industry

Several catalysts are accelerating long-term growth in the MEA Drilling Market. Technological breakthroughs in drilling automation, artificial intelligence, and data analytics are enabling more efficient and cost-effective operations, especially in challenging environments. Strategic partnerships between international oil companies (IOCs), national oil companies (NOCs), and service providers are fostering knowledge transfer and access to capital. Market expansion strategies, including the development of new exploration blocks and the optimization of existing fields, are crucial growth drivers. The ongoing energy transition, while posing long-term challenges, also presents opportunities for drilling technologies that can support the development of offshore wind foundations and geothermal energy projects.

Key Players Shaping the Middle East and Africa Drilling Market Market

- VALLOUREC

- Saudi Aramco Oil Co

- CNOOC International Ltd

- Weatherford International PLC

- Transocean Ltd

- Baker Hughes Company

- ADES International Holding

- Arabian Drilling Company (ADC)

- Volgaburmash Middle East & Africa

- Schlumberger Limited

Notable Milestones in Middle East and Africa Drilling Market Sector

- April 2022: Total Energies and Shell announced plans to drill exploratory oil wells on the South-West coast of South Africa, employing SLR consulting for environmental assessment.

- April 2022: Saipem secured a contract with Eni in North-Western Africa to conduct a drilling campaign using the ultra-deep-water drillship Saipem 12,000.

In-Depth Middle East and Africa Drilling Market Market Outlook

The MEA Drilling Market is set for sustained growth, driven by the region's strategic importance in global energy supply and ongoing investments in hydrocarbon exploration and production. Future market potential is amplified by the exploration of untapped deepwater reserves and the increasing adoption of advanced drilling technologies. Strategic opportunities lie in leveraging digitalization for enhanced operational efficiency and in developing solutions that support the energy transition, such as CCUS initiatives. The continued commitment of key stakeholders to innovation and sustainability will be pivotal in shaping the market's trajectory towards a more robust and resilient future.

Middle East and Africa Drilling Market Segmentation

-

1. Location of Deployment

- 1.1. Onshore

- 1.2. Offshore

-

2. Geography

- 2.1. Saudi Arabia

- 2.2. United Arab Emirates

- 2.3. South Africa

- 2.4. Others

Middle East and Africa Drilling Market Segmentation By Geography

- 1. Saudi Arabia

- 2. United Arab Emirates

- 3. South Africa

- 4. Others

Middle East and Africa Drilling Market Regional Market Share

Geographic Coverage of Middle East and Africa Drilling Market

Middle East and Africa Drilling Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 5.1.1. Onshore

- 5.1.2. Offshore

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. Saudi Arabia

- 5.2.2. United Arab Emirates

- 5.2.3. South Africa

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Saudi Arabia

- 5.3.2. United Arab Emirates

- 5.3.3. South Africa

- 5.3.4. Others

- 5.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 6. Middle East and Africa Drilling Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 6.1.1. Onshore

- 6.1.2. Offshore

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. Saudi Arabia

- 6.2.2. United Arab Emirates

- 6.2.3. South Africa

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 7. Saudi Arabia Middle East and Africa Drilling Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 7.1.1. Onshore

- 7.1.2. Offshore

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. Saudi Arabia

- 7.2.2. United Arab Emirates

- 7.2.3. South Africa

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 8. United Arab Emirates Middle East and Africa Drilling Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 8.1.1. Onshore

- 8.1.2. Offshore

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. Saudi Arabia

- 8.2.2. United Arab Emirates

- 8.2.3. South Africa

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 9. South Africa Middle East and Africa Drilling Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 9.1.1. Onshore

- 9.1.2. Offshore

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. Saudi Arabia

- 9.2.2. United Arab Emirates

- 9.2.3. South Africa

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 10. Others Middle East and Africa Drilling Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 10.1.1. Onshore

- 10.1.2. Offshore

- 10.2. Market Analysis, Insights and Forecast - by Geography

- 10.2.1. Saudi Arabia

- 10.2.2. United Arab Emirates

- 10.2.3. South Africa

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 VALLOUREC *List Not Exhaustive

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Saudi Aramco Oil Co

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 CNOOC International Ltd

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Weatherford International PLC

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Transocean Ltd

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Baker Hughes Company

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 ADES International Holding

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Arabian Drilling Company (ADC)

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Volgaburmash Middle East & Africa

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Schlumberger Limited

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 VALLOUREC *List Not Exhaustive

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Middle East and Africa Drilling Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Middle East and Africa Drilling Market Share (%) by Company 2025

List of Tables

- Table 1: Middle East and Africa Drilling Market Revenue million Forecast, by Location of Deployment 2020 & 2033

- Table 2: Middle East and Africa Drilling Market Revenue million Forecast, by Geography 2020 & 2033

- Table 3: Middle East and Africa Drilling Market Revenue million Forecast, by Region 2020 & 2033

- Table 4: Middle East and Africa Drilling Market Revenue million Forecast, by Location of Deployment 2020 & 2033

- Table 5: Middle East and Africa Drilling Market Revenue million Forecast, by Geography 2020 & 2033

- Table 6: Middle East and Africa Drilling Market Revenue million Forecast, by Country 2020 & 2033

- Table 7: Middle East and Africa Drilling Market Revenue million Forecast, by Location of Deployment 2020 & 2033

- Table 8: Middle East and Africa Drilling Market Revenue million Forecast, by Geography 2020 & 2033

- Table 9: Middle East and Africa Drilling Market Revenue million Forecast, by Country 2020 & 2033

- Table 10: Middle East and Africa Drilling Market Revenue million Forecast, by Location of Deployment 2020 & 2033

- Table 11: Middle East and Africa Drilling Market Revenue million Forecast, by Geography 2020 & 2033

- Table 12: Middle East and Africa Drilling Market Revenue million Forecast, by Country 2020 & 2033

- Table 13: Middle East and Africa Drilling Market Revenue million Forecast, by Location of Deployment 2020 & 2033

- Table 14: Middle East and Africa Drilling Market Revenue million Forecast, by Geography 2020 & 2033

- Table 15: Middle East and Africa Drilling Market Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East and Africa Drilling Market?

The projected CAGR is approximately 6%.

2. Which companies are prominent players in the Middle East and Africa Drilling Market?

Key companies in the market include VALLOUREC *List Not Exhaustive, Saudi Aramco Oil Co, CNOOC International Ltd, Weatherford International PLC, Transocean Ltd, Baker Hughes Company, ADES International Holding, Arabian Drilling Company (ADC), Volgaburmash Middle East & Africa, Schlumberger Limited.

3. What are the main segments of the Middle East and Africa Drilling Market?

The market segments include Location of Deployment, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 970.5 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Proven Shale Gas Reserves 4.; Technological Advancement in Horizontal Drilling and Hydraulic Fracturing.

6. What are the notable trends driving market growth?

Offshore Segment Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; High Exploration Cost.

8. Can you provide examples of recent developments in the market?

In April 2022, Total Energies and Shell announced plans to drill exploratory oil wells on the South-West coast of South Africa. The duo has decided to employ SLR consulting for the environmental assessment of the proposed exploration program.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East and Africa Drilling Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East and Africa Drilling Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East and Africa Drilling Market?

To stay informed about further developments, trends, and reports in the Middle East and Africa Drilling Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence