Key Insights

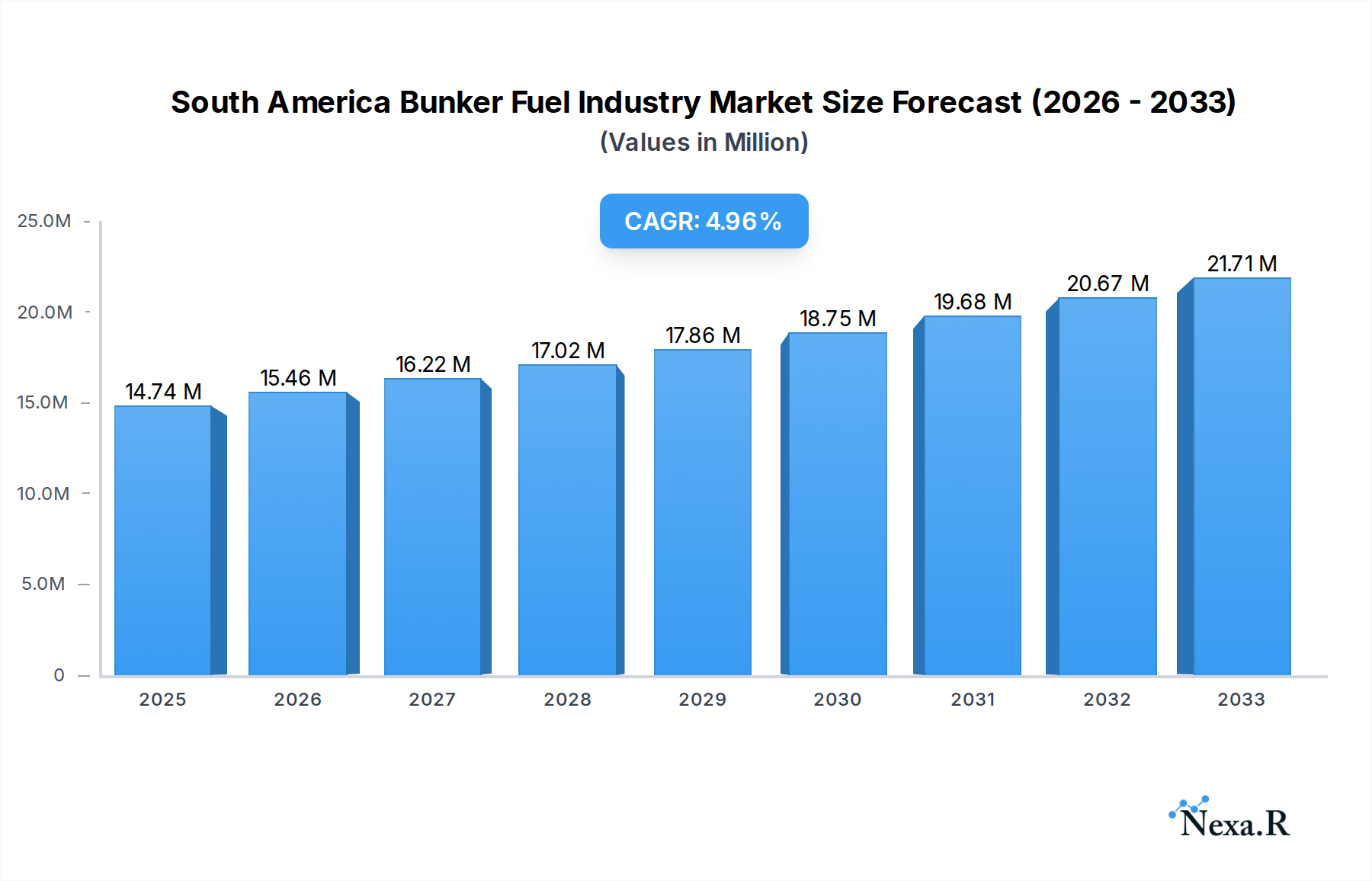

The South America Bunker Fuel Industry is poised for substantial growth, projected to reach $14.74 Million by 2025, with a Compound Annual Growth Rate (CAGR) of 4.80% over the forecast period of 2025-2033. This expansion is primarily driven by increasing maritime trade activities and the growing fleet sizes within the region. Key trends include a significant shift towards cleaner fuel types, with Very Low Sulfur Fuel Oil (VLSFO) and Liquefied Natural Gas (LNG) gaining traction due to stricter environmental regulations and the global push for decarbonization. This transition is not only influenced by regulatory bodies but also by major shipping companies and fuel suppliers actively investing in and promoting these more sustainable options. Furthermore, the burgeoning economies of countries like Brazil, Chile, and Argentina are contributing to higher demand for bunker fuels as they enhance their port infrastructure and expand their import/export capabilities, further solidifying the industry's upward trajectory.

South America Bunker Fuel Industry Market Size (In Million)

However, the industry faces certain restraints that could temper its full potential. The volatility of crude oil prices directly impacts bunker fuel costs, creating uncertainty for both suppliers and end-users. High capital expenditure required for retrofitting vessels to accommodate cleaner fuels like LNG, coupled with the limited availability of LNG bunkering infrastructure across South America, presents a significant hurdle. While the demand for cleaner fuels is a strong driver, the pace of adoption will depend on overcoming these infrastructure and cost challenges. Despite these constraints, the dominant fuel types are expected to remain High Sulfur Fuel Oil (HSFO) and Very Low Sulfur Fuel Oil (VLSFO), though the market share of LNG and other alternative fuels is anticipated to rise steadily throughout the forecast period. Container vessels and tankers represent the largest segments by vessel type, owing to their high volume of international trade.

South America Bunker Fuel Industry Company Market Share

Here's the SEO-optimized report description for the South America Bunker Fuel Industry, designed for maximum visibility and engagement.

Report Title: South America Bunker Fuel Market Analysis: Trends, Opportunities & Competitive Landscape (2019-2033)

Report Description:

Gain a comprehensive understanding of the dynamic South America Bunker Fuel Industry with this in-depth market analysis. Covering the period from 2019 to 2033, with a base year of 2025, this report dissects key market trends, growth drivers, and the competitive landscape. Explore evolving fuel types, including the rising importance of Very Low Sulfur Fuel Oil (VLSFO), Marine Gas Oil (MGO), and the nascent adoption of Liquefied Natural Gas (LNG), Methanol, and Biodiesel. Analyze the impact of these fuel shifts across major vessel types such as Containers, Tankers, and General Cargo, with detailed regional breakdowns for Brazil, Chile, Argentina, and the Rest of South America. This report is crucial for industry professionals, investors, and stakeholders seeking to navigate the complexities and capitalize on the significant opportunities within the South American marine fuel sector.

South America Bunker Fuel Industry Market Dynamics & Structure

The South America Bunker Fuel Industry is characterized by a complex interplay of factors shaping its current and future trajectory. Market concentration is a significant aspect, with major players vying for market share across different segments. Technological innovation is a key driver, particularly in the development and adoption of cleaner fuel alternatives like LNG and biofuels, spurred by increasing environmental regulations and a global push for decarbonization. Regulatory frameworks, including IMO 2020 and evolving regional environmental policies, are profoundly influencing fuel choices and operational standards. Competitive product substitutes are emerging, challenging traditional fuel oils, while the end-user demographics, primarily ship owners and fuel suppliers, are adapting to these changes. Mergers and Acquisitions (M&A) trends are also noteworthy, indicating consolidation and strategic repositioning within the industry.

- Market Concentration: Analysis of market share distribution among key players, including dominant fuel suppliers and shipping lines.

- Technological Innovation Drivers: Focus on advancements in cleaner fuel production, bunkering infrastructure, and emission reduction technologies.

- Regulatory Frameworks: Impact of IMO regulations, national environmental policies, and port state controls on fuel choices and operational compliance.

- Competitive Product Substitutes: Evaluation of the growing market penetration of VLSFO, MGO, LNG, Methanol, and Biodiesel against traditional HSFO.

- End-User Demographics: Insights into the evolving needs and purchasing behaviors of ship owners and charterers.

- M&A Trends: Examination of recent consolidations, partnerships, and strategic alliances shaping the industry's competitive landscape.

South America Bunker Fuel Industry Growth Trends & Insights

The South America Bunker Fuel Industry is poised for significant evolution, driven by a confluence of economic, regulatory, and technological forces. Market size is expected to witness consistent growth, fueled by increased maritime trade volumes and the ongoing transition towards more sustainable fuel options. The adoption rates of cleaner fuels, such as VLSFO and MGO, have accelerated post-IMO 2020, and the nascent but promising growth of LNG and alternative fuels will further shape market dynamics. Technological disruptions, including advancements in dual-fuel engine technology and improved bunkering infrastructure for new fuel types, are crucial enablers of this transition. Consumer behavior shifts are evident, with an increasing emphasis on environmental compliance, operational efficiency, and long-term cost predictability in fuel procurement.

The historical period (2019-2024) has seen the industry grapple with the implementation of stricter sulfur emission regulations, leading to a gradual but significant shift away from High Sulfur Fuel Oil (HSFO). The base year 2025 marks a critical point where the market has largely adapted to VLSFO and MGO, with increasing exploration and initial investments in LNG and other low-carbon alternatives. The forecast period (2025-2033) anticipates a sustained upward trend in the demand for cleaner marine fuels, driven by a growing global awareness of climate change and stringent international maritime regulations. The CAGR for the South American bunker fuel market is projected to be robust, reflecting this transformative phase. Market penetration of alternative fuels, while currently lower than traditional fuels, is expected to rise exponentially as infrastructure develops and their economic viability improves. The industry's ability to invest in and adapt to these new technologies will be a key determinant of success. Consumer behavior is shifting from a primary focus on cost to a more holistic approach that includes environmental performance, compliance, and supply chain resilience. This necessitates a strategic re-evaluation of bunker fuel offerings and operational models by suppliers and distributors.

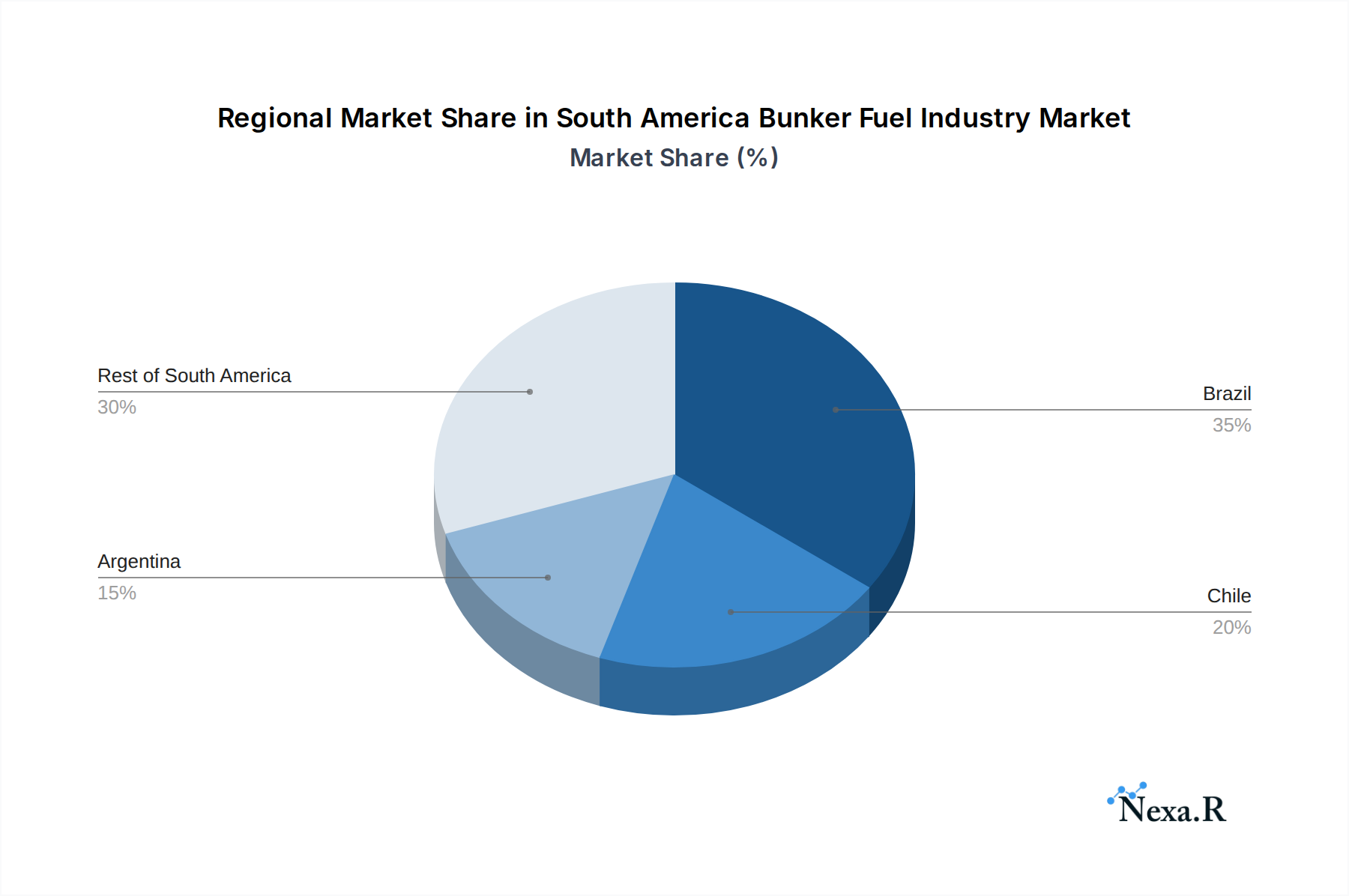

Dominant Regions, Countries, or Segments in South America Bunker Fuel Industry

Within the South America Bunker Fuel Industry, Brazil emerges as the dominant geographical segment, driven by its extensive coastline, significant port infrastructure, and its role as a major hub for both domestic and international maritime trade. The country's proactive stance on embracing cleaner energy solutions, exemplified by initiatives like Petrobras' first renewable content bunker delivery, positions it at the forefront of industry evolution. The dominance of Brazil is further amplified by its substantial consumption of bunker fuels across various vessel types, particularly for its thriving container shipping and tanker fleets servicing its vast natural resources exports.

- Brazil:

- Key Drivers: Robust economic activity, extensive port network (e.g., Santos, Rio Grande), significant oil and gas production, and government support for cleaner maritime fuels.

- Market Share: Consistently holds the largest share of the South American bunker fuel market.

- Growth Potential: High, driven by increasing trade volumes and the ongoing energy transition.

- Fuel Type Dominance: While Very Low Sulfur Fuel Oil (VLSFO) and Marine Gas Oil (MGO) are currently dominant due to regulatory mandates, Liquefied Natural Gas (LNG) is gaining traction as a future-proof alternative, especially in Brazil, with partnerships aimed at developing small-scale LNG bunkering solutions.

- Vessel Type Impact: Container ships and Tankers represent the largest consumers of bunker fuel, reflecting the primary trade routes and commodity movements within South America.

- Rest of South America: Countries like Chile and Argentina also contribute significantly, with their own unique port infrastructures and trade patterns influencing regional demand for various fuel types. The "Rest of South America" segment, encompassing countries like Peru, Colombia, and Uruguay, represents a growing market with increasing demand for cleaner fuel options.

South America Bunker Fuel Industry Product Landscape

The product landscape in the South America Bunker Fuel Industry is undergoing a significant transformation. Traditional High Sulfur Fuel Oil (HSFO) is steadily being replaced by Very Low Sulfur Fuel Oil (VLSFO) and Marine Gas Oil (MGO) to comply with global sulfur emission regulations. The unique selling proposition of these cleaner fuels lies in their compliance and reduced environmental impact. Innovations are also emerging in the realm of alternative fuels, with Liquefied Natural Gas (LNG) gaining traction, offering a substantial reduction in sulfur dioxide and nitrogen oxide emissions. Furthermore, the development and testing of methanol and biodiesel as marine fuels represent the industry's commitment to decarbonization, offering promising performance metrics in terms of emissions reduction and potential for scalability.

Key Drivers, Barriers & Challenges in South America Bunker Fuel Industry

Key Drivers:

- Stringent Environmental Regulations: The global and regional push for cleaner maritime operations, particularly IMO 2020 and future decarbonization targets, is the primary driver for the adoption of low-sulfur and alternative fuels.

- Increasing Maritime Trade Volumes: Growth in international and intra-regional trade necessitates a larger and more efficient shipping fleet, directly boosting demand for bunker fuels.

- Technological Advancements: Development of dual-fuel engines and improved bunkering infrastructure for cleaner fuels makes their adoption more feasible and cost-effective.

- Government Initiatives and Support: Policies promoting cleaner energy adoption and investments in port infrastructure for alternative fuels create a conducive environment for growth.

Barriers & Challenges:

- High Cost of New Fuels and Infrastructure: The initial investment in LNG bunkering facilities, dual-fuel vessels, and the premium price of alternative fuels present a significant financial hurdle.

- Supply Chain and Availability Concerns: Ensuring a consistent and reliable supply of new fuel types across diverse South American ports is a major logistical challenge.

- Regulatory Uncertainty and Harmonization: Variations in regional regulations and the evolving nature of future emissions standards can create investment uncertainty.

- Competition from Traditional Fuels: The established infrastructure and lower cost of traditional fuel oils continue to pose a challenge to the rapid adoption of alternatives, particularly for cost-sensitive operators.

Emerging Opportunities in South America Bunker Fuel Industry

Emerging opportunities in the South America Bunker Fuel Industry are centered on the growing demand for sustainable and compliant marine fuels. The expansion of Liquefied Natural Gas (LNG) bunkering infrastructure, particularly in key trading hubs like Brazil, presents a significant opportunity for both fuel suppliers and technology providers. The increasing interest in biofuels and methanol as alternative low-carbon fuels opens avenues for new partnerships and product development. Furthermore, the potential for small-scale LNG solutions to serve regional routes and smaller vessels offers an untapped market segment. The development of advanced logistical solutions for efficient and cost-effective bunkering of these new fuel types will also be a key area of growth.

Growth Accelerators in the South America Bunker Fuel Industry Industry

Several factors are accelerating the growth of the South America Bunker Fuel Industry. The relentless drive towards decarbonization, propelled by international agreements and corporate sustainability goals, is a paramount accelerator. Strategic partnerships between fuel suppliers, shipping companies, and technology providers are fostering the development and deployment of new fuel solutions. Investments in upgrading port infrastructure to accommodate LNG and other alternative fuels are critical enablers. Moreover, the increasing focus on operational efficiency and the potential cost savings offered by certain cleaner fuels over their lifecycle are contributing to market expansion. The growing awareness and demand for environmentally responsible shipping practices among cargo owners are also indirectly fueling the demand for greener bunker fuels.

Key Players Shaping the South America Bunker Fuel Industry Market

- Ocean Network Express

- Chevron Corporation

- Monjasa Holding A/S

- Vitol Holding BV

- AP Moeller Maersk A/S

- China COSCO Holdings Company Limited

- Mediterranean Shipping Company SA

- TotalEnergies SA

- World Fuel Services Corp

- CMA CGM Group

- Peninsula Petroleum Ltd

- Bunker Holding A/S

- Hapag-Lloyd AG

Notable Milestones in South America Bunker Fuel Industry Sector

- January 2023: Brazilian state-controlled oil and gas producer Petrobras carried out the country's first bunker delivery with renewable content at the Rio Grande Terminal (Terig) in Rio Grande do Sul, signaling a significant step towards sustainable marine fuels.

- November 2022: Nimofast Brasil SA, a natural gas trader, signed a partnership agreement with Norwegian company Kanfer Shipping AS, aiming to provide small and medium-scale LNG shipping, floating storage units, and LNG bunkering solutions for Kanfer's clients in Brazil, highlighting the growing focus on LNG infrastructure.

- October 2022: Trinidad and Tobago's state-owned gas company (NGC) began designing a small-scale liquefied natural gas (LNG) hub, indicating regional efforts to diversify energy sources and support the adoption of LNG in the maritime sector, with potential spillover effects for nearby South American markets.

In-Depth South America Bunker Fuel Industry Market Outlook

The in-depth market outlook for the South America Bunker Fuel Industry reveals a sector on the cusp of substantial transformation, driven by sustainability imperatives and technological innovation. Growth accelerators, such as intensified regulatory pressures for emissions reduction and strategic collaborations between major industry players, are paving the way for a significant shift towards cleaner fuel alternatives. The expanding network of LNG bunkering facilities and the increasing viability of biofuels and methanol present lucrative opportunities for market expansion and diversification. Future market potential is strongly tied to continued investment in advanced bunkering technologies and infrastructure, alongside proactive adaptation to evolving global maritime environmental standards. Stakeholders who can effectively navigate these changes and embrace sustainable solutions are poised for significant success in this dynamic market.

South America Bunker Fuel Industry Segmentation

-

1. Fuel Type

- 1.1. High Sulfur Fuel Oil (HSFO)

- 1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 1.3. Marine Gas Oil (MGO)

- 1.4. Liquefied Natural Gas (LNG)

- 1.5. Other Fuel Types (Methanol, LPG, and Biodiesel)

-

2. Vessel Type

- 2.1. Containers

- 2.2. Tankers

- 2.3. General Cargo

- 2.4. Bulk Container

- 2.5. Other Vessel Types

-

3. Geography

- 3.1. Brazil

- 3.2. Chile

- 3.3. Argentina

- 3.4. Rest of South America

South America Bunker Fuel Industry Segmentation By Geography

- 1. Brazil

- 2. Chile

- 3. Argentina

- 4. Rest of South America

South America Bunker Fuel Industry Regional Market Share

Geographic Coverage of South America Bunker Fuel Industry

South America Bunker Fuel Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.80% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 5.1.1. High Sulfur Fuel Oil (HSFO)

- 5.1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 5.1.3. Marine Gas Oil (MGO)

- 5.1.4. Liquefied Natural Gas (LNG)

- 5.1.5. Other Fuel Types (Methanol, LPG, and Biodiesel)

- 5.2. Market Analysis, Insights and Forecast - by Vessel Type

- 5.2.1. Containers

- 5.2.2. Tankers

- 5.2.3. General Cargo

- 5.2.4. Bulk Container

- 5.2.5. Other Vessel Types

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Brazil

- 5.3.2. Chile

- 5.3.3. Argentina

- 5.3.4. Rest of South America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Brazil

- 5.4.2. Chile

- 5.4.3. Argentina

- 5.4.4. Rest of South America

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6. South America Bunker Fuel Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6.1.1. High Sulfur Fuel Oil (HSFO)

- 6.1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 6.1.3. Marine Gas Oil (MGO)

- 6.1.4. Liquefied Natural Gas (LNG)

- 6.1.5. Other Fuel Types (Methanol, LPG, and Biodiesel)

- 6.2. Market Analysis, Insights and Forecast - by Vessel Type

- 6.2.1. Containers

- 6.2.2. Tankers

- 6.2.3. General Cargo

- 6.2.4. Bulk Container

- 6.2.5. Other Vessel Types

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. Brazil

- 6.3.2. Chile

- 6.3.3. Argentina

- 6.3.4. Rest of South America

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7. Brazil South America Bunker Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7.1.1. High Sulfur Fuel Oil (HSFO)

- 7.1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 7.1.3. Marine Gas Oil (MGO)

- 7.1.4. Liquefied Natural Gas (LNG)

- 7.1.5. Other Fuel Types (Methanol, LPG, and Biodiesel)

- 7.2. Market Analysis, Insights and Forecast - by Vessel Type

- 7.2.1. Containers

- 7.2.2. Tankers

- 7.2.3. General Cargo

- 7.2.4. Bulk Container

- 7.2.5. Other Vessel Types

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. Brazil

- 7.3.2. Chile

- 7.3.3. Argentina

- 7.3.4. Rest of South America

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8. Chile South America Bunker Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8.1.1. High Sulfur Fuel Oil (HSFO)

- 8.1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 8.1.3. Marine Gas Oil (MGO)

- 8.1.4. Liquefied Natural Gas (LNG)

- 8.1.5. Other Fuel Types (Methanol, LPG, and Biodiesel)

- 8.2. Market Analysis, Insights and Forecast - by Vessel Type

- 8.2.1. Containers

- 8.2.2. Tankers

- 8.2.3. General Cargo

- 8.2.4. Bulk Container

- 8.2.5. Other Vessel Types

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. Brazil

- 8.3.2. Chile

- 8.3.3. Argentina

- 8.3.4. Rest of South America

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9. Argentina South America Bunker Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9.1.1. High Sulfur Fuel Oil (HSFO)

- 9.1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 9.1.3. Marine Gas Oil (MGO)

- 9.1.4. Liquefied Natural Gas (LNG)

- 9.1.5. Other Fuel Types (Methanol, LPG, and Biodiesel)

- 9.2. Market Analysis, Insights and Forecast - by Vessel Type

- 9.2.1. Containers

- 9.2.2. Tankers

- 9.2.3. General Cargo

- 9.2.4. Bulk Container

- 9.2.5. Other Vessel Types

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. Brazil

- 9.3.2. Chile

- 9.3.3. Argentina

- 9.3.4. Rest of South America

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 10. Rest of South America South America Bunker Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Fuel Type

- 10.1.1. High Sulfur Fuel Oil (HSFO)

- 10.1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 10.1.3. Marine Gas Oil (MGO)

- 10.1.4. Liquefied Natural Gas (LNG)

- 10.1.5. Other Fuel Types (Methanol, LPG, and Biodiesel)

- 10.2. Market Analysis, Insights and Forecast - by Vessel Type

- 10.2.1. Containers

- 10.2.2. Tankers

- 10.2.3. General Cargo

- 10.2.4. Bulk Container

- 10.2.5. Other Vessel Types

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. Brazil

- 10.3.2. Chile

- 10.3.3. Argentina

- 10.3.4. Rest of South America

- 10.1. Market Analysis, Insights and Forecast - by Fuel Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 6 Ocean Network Express*List Not Exhaustive 6 4 Market Ranking/Share (%) Analysi

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 7 Chevron Corporation

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 2 Monjasa Holding A/S

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 1 Vitol Holding BV

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 1 AP Moeller Maersk A/S

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 3 China COSCO Holdings Company Limited

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 2 Mediterranean Shipping Company SA

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Ship Owners

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Fuel Suppliers

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 6 TotalEnergies SA

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 4 World Fuel Services Corp

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 4 CMA CGM Group

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 5 Peninsula Petroleum Ltd

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.14 3 Bunker Holding A/S

- 11.1.14.1. Company Overview

- 11.1.14.2. Products

- 11.1.14.3. Company Financials

- 11.1.14.4. SWOT Analysis

- 11.1.15 5 Hapag-Lloyd AG

- 11.1.15.1. Company Overview

- 11.1.15.2. Products

- 11.1.15.3. Company Financials

- 11.1.15.4. SWOT Analysis

- 11.1.1 6 Ocean Network Express*List Not Exhaustive 6 4 Market Ranking/Share (%) Analysi

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: South America Bunker Fuel Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: South America Bunker Fuel Industry Share (%) by Company 2025

List of Tables

- Table 1: South America Bunker Fuel Industry Revenue Million Forecast, by Fuel Type 2020 & 2033

- Table 2: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 3: South America Bunker Fuel Industry Revenue Million Forecast, by Vessel Type 2020 & 2033

- Table 4: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 5: South America Bunker Fuel Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2020 & 2033

- Table 7: South America Bunker Fuel Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Region 2020 & 2033

- Table 9: South America Bunker Fuel Industry Revenue Million Forecast, by Fuel Type 2020 & 2033

- Table 10: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 11: South America Bunker Fuel Industry Revenue Million Forecast, by Vessel Type 2020 & 2033

- Table 12: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 13: South America Bunker Fuel Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 14: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2020 & 2033

- Table 15: South America Bunker Fuel Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2020 & 2033

- Table 17: South America Bunker Fuel Industry Revenue Million Forecast, by Fuel Type 2020 & 2033

- Table 18: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 19: South America Bunker Fuel Industry Revenue Million Forecast, by Vessel Type 2020 & 2033

- Table 20: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 21: South America Bunker Fuel Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 22: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2020 & 2033

- Table 23: South America Bunker Fuel Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2020 & 2033

- Table 25: South America Bunker Fuel Industry Revenue Million Forecast, by Fuel Type 2020 & 2033

- Table 26: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 27: South America Bunker Fuel Industry Revenue Million Forecast, by Vessel Type 2020 & 2033

- Table 28: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 29: South America Bunker Fuel Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 30: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2020 & 2033

- Table 31: South America Bunker Fuel Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 32: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2020 & 2033

- Table 33: South America Bunker Fuel Industry Revenue Million Forecast, by Fuel Type 2020 & 2033

- Table 34: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 35: South America Bunker Fuel Industry Revenue Million Forecast, by Vessel Type 2020 & 2033

- Table 36: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 37: South America Bunker Fuel Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 38: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2020 & 2033

- Table 39: South America Bunker Fuel Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 40: South America Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Bunker Fuel Industry?

The projected CAGR is approximately 4.80%.

2. Which companies are prominent players in the South America Bunker Fuel Industry?

Key companies in the market include 6 Ocean Network Express*List Not Exhaustive 6 4 Market Ranking/Share (%) Analysi, 7 Chevron Corporation, 2 Monjasa Holding A/S, 1 Vitol Holding BV, 1 AP Moeller Maersk A/S, 3 China COSCO Holdings Company Limited, 2 Mediterranean Shipping Company SA, Ship Owners, Fuel Suppliers, 6 TotalEnergies SA, 4 World Fuel Services Corp, 4 CMA CGM Group, 5 Peninsula Petroleum Ltd, 3 Bunker Holding A/S, 5 Hapag-Lloyd AG.

3. What are the main segments of the South America Bunker Fuel Industry?

The market segments include Fuel Type, Vessel Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.74 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Rising Marine Transportation of Essential Commodities in South America4.; Supportive Policies for Cleaner Bunker Fuel.

6. What are the notable trends driving market growth?

Very Low Sulfur Fuel Oil (VLSFO) to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Volatile Nature of Oil Market.

8. Can you provide examples of recent developments in the market?

In January 2023, Brazilian state-controlled oil and gas producer Petrobras carried out the country's first bunker delivery with renewable content at the Rio Grande Terminal (Terig) in Rio Grande do Sul.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in metric tonnes.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Bunker Fuel Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Bunker Fuel Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Bunker Fuel Industry?

To stay informed about further developments, trends, and reports in the South America Bunker Fuel Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence