Key Insights

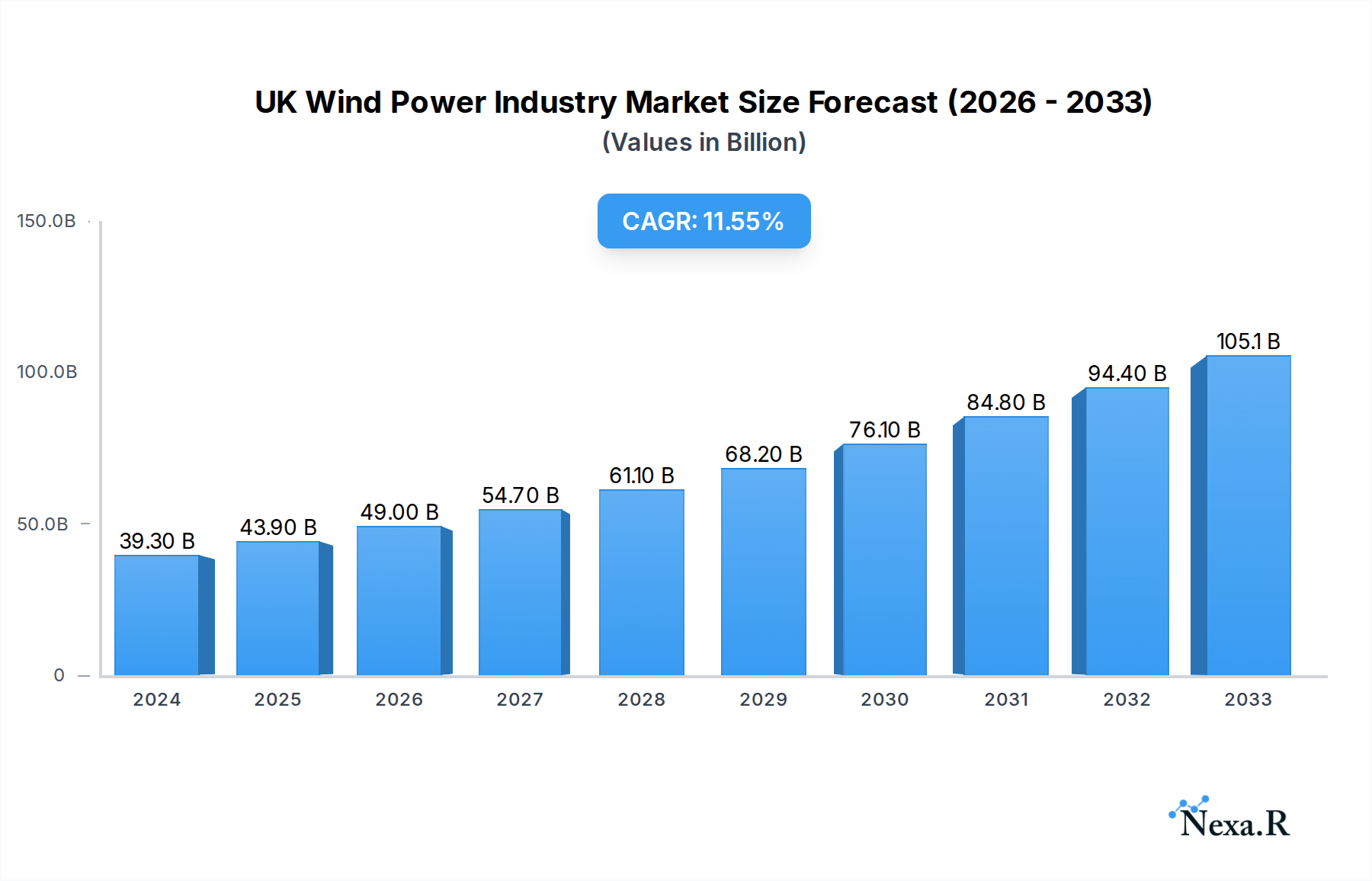

The UK wind power industry is poised for significant expansion, driven by a strong commitment to renewable energy targets and a robust offshore wind development pipeline. As of 2024, the market is valued at an estimated $39.3 billion, a testament to its established presence and ongoing investment. This growth trajectory is further underscored by a projected Compound Annual Growth Rate (CAGR) of 11.7% from 2025 to 2033. Key drivers fueling this expansion include supportive government policies, increasing investor confidence, and the declining cost of wind energy technology, making it a more competitive and attractive energy source. The UK's strategic geographical location, with its extensive coastline and favorable wind conditions, particularly for offshore developments, positions it as a global leader in wind power generation. This inherent advantage, coupled with ambitious decarbonization goals, is spurring substantial investment in both onshore and offshore wind farms.

UK Wind Power Industry Market Size (In Billion)

Emerging trends within the UK wind power sector include advancements in turbine technology, such as larger and more efficient designs, and the development of floating offshore wind platforms, which unlock new deep-water sites. Innovations in grid integration and energy storage solutions are also critical for managing the intermittency of wind power and ensuring grid stability. While the market is characterized by strong growth, potential restraints could include supply chain bottlenecks, grid connection challenges, and evolving regulatory frameworks. However, the overwhelming momentum towards a greener energy future, coupled with the UK's proactive stance on renewable energy, suggests these challenges will be managed. The industry is witnessing substantial activity from major players like Ørsted, Siemens Gamesa, and Vestas, underscoring the competitive landscape and the significant opportunities for continued market penetration and technological advancement.

UK Wind Power Industry Company Market Share

UK Wind Power Industry Market Dynamics & Structure

The UK wind power industry exhibits a dynamic market structure, characterized by a moderate level of concentration with key players dominating significant portions of the market. Technological innovation remains a primary driver, with advancements in turbine efficiency, grid integration, and energy storage continuously shaping the landscape. Regulatory frameworks, particularly government targets for renewable energy generation and carbon emission reductions, play a crucial role in steering investment and development. Competitive product substitutes, while present in the form of other renewable energy sources like solar and hydro, are increasingly outpaced by the cost-effectiveness and scalability of wind power, especially offshore wind. End-user demographics are shifting towards a greater demand for green energy solutions from both industrial and residential sectors, influenced by environmental consciousness and rising energy costs. Mergers and acquisitions (M&A) trends are active, as larger utilities and energy companies consolidate their portfolios and acquire smaller developers to expand their reach and capitalize on economies of scale.

- Market Concentration: While a few major players hold substantial market share, the industry is not entirely monolithic, allowing for niche opportunities and regional specialization.

- Technological Innovation Drivers: Enhanced rotor blade design, floating offshore wind platforms, and advanced predictive maintenance are key areas of innovation.

- Regulatory Frameworks: The Contracts for Difference (CfD) scheme is a critical policy underpinning the sector's growth, providing revenue certainty for developers.

- Competitive Product Substitutes: While solar PV is a competitor, offshore wind's capacity factor and large-scale potential position it favorably.

- End-User Demographics: Growing corporate power purchase agreements (PPAs) and increasing consumer awareness are fueling demand.

- M&A Trends: Expect continued consolidation as companies seek to achieve critical mass and integrate supply chains. The M&A deal volume in the historical period (2019-2024) is estimated to be in the range of £15-£25 billion.

UK Wind Power Industry Growth Trends & Insights

The UK wind power industry is experiencing robust growth, driven by a clear political will to achieve net-zero emissions and secure energy independence. The market size has seen a significant expansion over the historical period (2019-2024), with total investments estimated to have reached £85 billion. This growth is underpinned by consistent adoption rates of new wind energy projects, both onshore and offshore, spurred by supportive government policies and decreasing levelized cost of energy (LCOE) for wind technologies. Technological disruptions, such as the development of larger and more efficient wind turbines, are enhancing the industry's capacity and economic viability. Consumer behavior is also shifting, with an increasing preference for electricity generated from renewable sources, leading to a higher demand for green energy tariffs and corporate power purchase agreements.

The forecast period (2025-2033) is poised for even more accelerated growth. The CAGR for the UK wind power industry is projected to be a remarkable 12.5% over this period, indicating a sustained and strong upward trajectory. By the base year 2025, the total market size is estimated to be £120 billion, and this is projected to escalate to £280 billion by 2033. Market penetration is expected to deepen considerably, with wind power playing an increasingly dominant role in the UK's overall energy mix. This expansion will be fueled by continued investment in large-scale offshore wind farms, which offer the greatest potential for capacity growth and cost reduction. Onshore wind, despite facing some planning challenges, will also continue to contribute significantly, benefiting from technological advancements that improve efficiency and reduce visual impact.

Adoption rates for offshore wind are particularly noteworthy, as the UK solidifies its position as a global leader in this segment. The development of new offshore wind farms, coupled with the repowering of older ones, will significantly boost installed capacity. The impact of technological disruptions cannot be overstated; advancements in blade aerodynamics, foundation designs for deeper waters, and grid connection technologies are making offshore wind more accessible and cost-effective than ever before. These innovations are not only increasing the energy output per turbine but also reducing the environmental footprint and operational costs.

Consumer behavior shifts are also a key growth accelerator. A growing awareness of climate change and the desire for energy security are driving both individual and corporate decisions to invest in or procure renewable energy. This trend is evident in the increasing number of corporate PPAs being signed with wind farm developers, providing long-term revenue certainty and supporting new project developments. Furthermore, the rising volatility of fossil fuel prices makes wind power, with its predictable operating costs, an increasingly attractive and stable energy source. The transition to electric vehicles and the electrification of heating systems will further amplify the demand for clean electricity, solidifying wind power's central role in the UK's decarbonization efforts.

Dominant Regions, Countries, or Segments in UK Wind Power Industry

The UK wind power industry is predominantly driven by the Offshore segment, which has emerged as the key growth engine and the most dominant force in shaping the market's trajectory. This dominance is attributable to a confluence of favorable economic policies, substantial investments in infrastructure, and the unique geographical advantages offered by the UK's extensive coastline. The sheer scale of offshore wind farms, coupled with their higher capacity factors due to consistent wind speeds over the sea, allows for significant energy generation, making it a cornerstone of the UK's renewable energy targets.

The market share of offshore wind within the total UK wind power industry is substantial and projected to grow further. In the base year 2025, offshore wind is estimated to account for approximately 65% of the total market value, projected to be £78 billion out of £120 billion. By 2033, this share is expected to expand to over 70%, representing a market value of approximately £196 billion out of the projected £280 billion. This expansion is not merely about increasing installed capacity but also about technological advancements that are making offshore wind farms more efficient and cost-effective in increasingly challenging marine environments.

Key drivers for the dominance of the offshore segment include:

- Government Policy and Support: The UK government's commitment to ambitious offshore wind targets, enshrined in policies like the Contracts for Difference (CfD) scheme, provides crucial revenue certainty for developers, de-risking large-scale investments.

- Technological Innovation: Advances in turbine technology, including larger rotor diameters and floating offshore wind platforms, are opening up new areas for development in deeper waters, significantly expanding the potential resource.

- Economic Policies and Incentives: Tax incentives, access to finance, and government-backed research and development programs have fostered a supportive ecosystem for offshore wind development.

- Infrastructure Development: Significant investment has been made in port facilities, grid connections, and supply chain capabilities specifically tailored for the offshore wind sector, creating a robust and integrated infrastructure.

- Resource Availability: The UK possesses some of the best wind resources in Europe, particularly in the North Sea, providing a consistent and powerful energy source for offshore installations.

- Market Size and Growth Potential: The sheer scale of potential offshore wind deployment in the UK dwarfs that of onshore wind, offering greater opportunities for large-scale projects and economies of scale.

While onshore wind remains a vital component of the UK's renewable energy mix, contributing an estimated 35% of the market value in 2025 (£42 billion) and projected to reach £84 billion by 2033, its growth is more constrained by land availability and planning regulations compared to the vast expanse available for offshore development. Therefore, the offshore segment is unequivocally the dominant force, driving the majority of new capacity additions and investment in the UK wind power industry.

UK Wind Power Industry Product Landscape

The UK wind power industry's product landscape is defined by increasingly sophisticated and powerful wind turbine technology. Innovations focus on enhancing energy capture through larger rotor diameters, advanced aerodynamic blade designs, and optimized power electronics for grid integration. For offshore wind, developments include floating foundation technologies to access deeper waters and improved corrosion resistance for harsh marine environments. Performance metrics are marked by rising capacity factors, reduced downtime through predictive maintenance, and lower levelized costs of electricity (LCOE), making wind power increasingly competitive. Unique selling propositions lie in their scalability, contribution to energy security, and zero-emission power generation, aligning with the UK's net-zero ambitions.

Key Drivers, Barriers & Challenges in UK Wind Power Industry

Key Drivers:

- Government Decarbonization Targets: Ambitious net-zero commitments drive substantial investment in renewable energy, with wind power being a cornerstone.

- Energy Security: Reducing reliance on imported fossil fuels makes domestic wind power an attractive strategic asset.

- Cost Competitiveness: Declining LCOE for both onshore and offshore wind makes it economically favorable compared to fossil fuels.

- Technological Advancements: Continued innovation in turbine efficiency and installation methods enhances performance and reduces costs.

- Corporate PPA Demand: Growing numbers of businesses are seeking green energy solutions, driving demand for new wind projects.

Barriers & Challenges:

- Supply Chain Constraints: Rapid growth can strain existing supply chains for components and skilled labor, leading to delays and increased costs, estimated to add 5-10% to project timelines and budgets.

- Regulatory Hurdles and Planning Permissions: Lengthy and complex planning processes for onshore wind can delay or derail projects.

- Grid Infrastructure Limitations: The existing grid may require significant upgrades to accommodate the increasing output from wind farms, posing a substantial infrastructure challenge and potential cost of £10-£15 billion over the forecast period for necessary upgrades.

- Public Perception and Environmental Concerns: While generally positive, localized opposition to onshore wind farms and concerns about avian impacts can create challenges.

- Intermittency and Storage Solutions: Managing the intermittent nature of wind power requires significant investment in grid-scale battery storage and grid flexibility solutions.

Emerging Opportunities in UK Wind Power Industry

Emerging opportunities in the UK wind power industry lie in the expansion of floating offshore wind technology, which unlocks vast untapped deep-water resources. The development of innovative energy storage solutions, such as advanced battery systems and green hydrogen production powered by wind, presents a significant avenue for growth, addressing intermittency challenges. Furthermore, repowering older onshore wind farms with more efficient turbines offers a pathway to increased energy generation from existing sites. Growing demand for industrial decarbonization through direct renewable energy sourcing also presents new market segments.

Growth Accelerators in the UK Wind Power Industry Industry

Several catalysts are accelerating the long-term growth of the UK wind power industry. Technological breakthroughs in turbine design and manufacturing, particularly the scaling up of offshore wind turbine capacities to 15MW and beyond, are continuously pushing the boundaries of efficiency and cost-effectiveness. Strategic partnerships between energy developers, technology providers, and industrial consumers are fostering integrated energy solutions and securing long-term investment. Market expansion strategies, including the development of new offshore wind farms in previously unexplored regions and the optimization of existing sites, are further driving growth.

Key Players Shaping the UK Wind Power Industry Market

- Vattenfall AB

- Siemens Gamesa Renewable Energy SA

- Electricite de France S

- Suzlon Energy Ltd

- Vestas Wind Systems AS

- General Electric Company

- Orsted AS

Notable Milestones in UK Wind Power Industry Sector

- 2019: Launch of the Crown Estate's seabed leasing round for floating offshore wind, signaling a new era of development.

- 2020: Hornsea Two, the world's largest offshore wind farm at the time, began construction, demonstrating large-scale project capabilities.

- 2021: Record annual auction results for Contracts for Difference (CfD) demonstrated strong government commitment and competitive pricing for offshore wind.

- 2022: Significant advancements in floating wind technology and supply chain development, with several projects reaching key milestones.

- 2023: The UK government announced accelerated targets for offshore wind deployment, further bolstering industry confidence and investment.

- 2024: Continued progress in grid infrastructure upgrades and the integration of energy storage solutions to support the expanding renewable capacity.

In-Depth UK Wind Power Industry Market Outlook

The future outlook for the UK wind power industry is exceptionally bright, characterized by sustained growth and innovation. The commitment to net-zero emissions, coupled with increasing energy security concerns, will continue to drive substantial investment in both onshore and offshore wind technologies. The ongoing development and deployment of larger, more efficient turbines, particularly in the offshore sector, will further reduce costs and expand the potential for clean energy generation, projected to be in the range of £100-£120 billion in new investments over the forecast period. Emerging opportunities in energy storage and green hydrogen production, powered by wind energy, represent significant growth accelerators, transforming the industry into a more holistic energy solution provider. Strategic partnerships and continued government support will be pivotal in navigating challenges and unlocking the full potential of this critical sector for the UK's sustainable future.

UK Wind Power Industry Segmentation

- 1. Onshore

- 2. Offshore

UK Wind Power Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

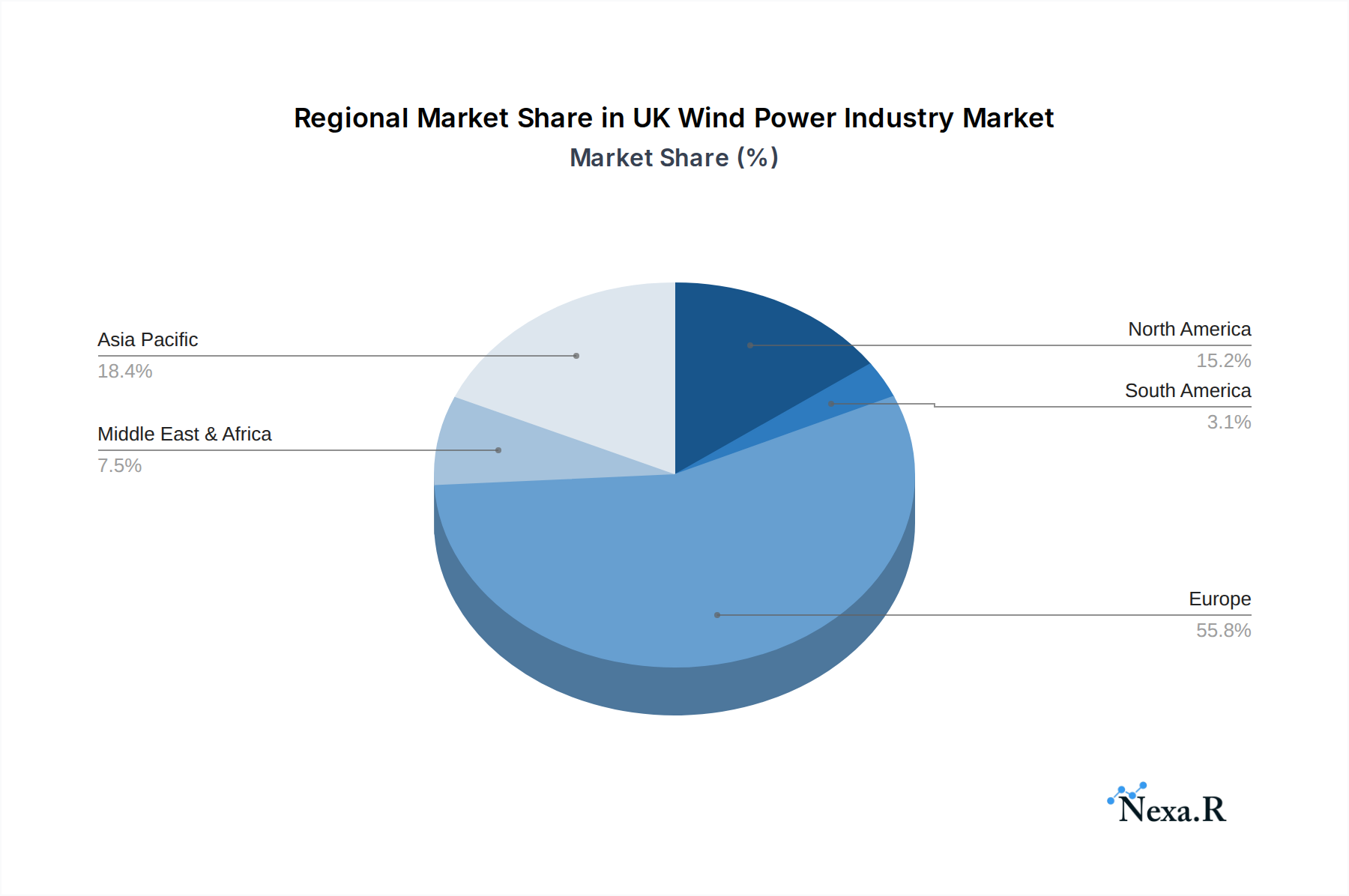

UK Wind Power Industry Regional Market Share

Geographic Coverage of UK Wind Power Industry

UK Wind Power Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Onshore

- 5.2. Market Analysis, Insights and Forecast - by Offshore

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 6. Global UK Wind Power Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Onshore

- 6.2. Market Analysis, Insights and Forecast - by Offshore

- 7. North America UK Wind Power Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Onshore

- 7.2. Market Analysis, Insights and Forecast - by Offshore

- 8. South America UK Wind Power Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Onshore

- 8.2. Market Analysis, Insights and Forecast - by Offshore

- 9. Europe UK Wind Power Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Onshore

- 9.2. Market Analysis, Insights and Forecast - by Offshore

- 10. Middle East & Africa UK Wind Power Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Onshore

- 10.2. Market Analysis, Insights and Forecast - by Offshore

- 11. Asia Pacific UK Wind Power Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Onshore

- 11.2. Market Analysis, Insights and Forecast - by Offshore

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Vattenfall AB

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Siemens Gamesa Renewable Energy SA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Electricite de France S

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Suzlon Energy Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Vestas Wind Systems AS

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 General Electric Company

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Orsted AS

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.1 Vattenfall AB

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global UK Wind Power Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global UK Wind Power Industry Volume Breakdown (Gigawatt, %) by Region 2025 & 2033

- Figure 3: North America UK Wind Power Industry Revenue (billion), by Onshore 2025 & 2033

- Figure 4: North America UK Wind Power Industry Volume (Gigawatt), by Onshore 2025 & 2033

- Figure 5: North America UK Wind Power Industry Revenue Share (%), by Onshore 2025 & 2033

- Figure 6: North America UK Wind Power Industry Volume Share (%), by Onshore 2025 & 2033

- Figure 7: North America UK Wind Power Industry Revenue (billion), by Offshore 2025 & 2033

- Figure 8: North America UK Wind Power Industry Volume (Gigawatt), by Offshore 2025 & 2033

- Figure 9: North America UK Wind Power Industry Revenue Share (%), by Offshore 2025 & 2033

- Figure 10: North America UK Wind Power Industry Volume Share (%), by Offshore 2025 & 2033

- Figure 11: North America UK Wind Power Industry Revenue (billion), by Country 2025 & 2033

- Figure 12: North America UK Wind Power Industry Volume (Gigawatt), by Country 2025 & 2033

- Figure 13: North America UK Wind Power Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America UK Wind Power Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: South America UK Wind Power Industry Revenue (billion), by Onshore 2025 & 2033

- Figure 16: South America UK Wind Power Industry Volume (Gigawatt), by Onshore 2025 & 2033

- Figure 17: South America UK Wind Power Industry Revenue Share (%), by Onshore 2025 & 2033

- Figure 18: South America UK Wind Power Industry Volume Share (%), by Onshore 2025 & 2033

- Figure 19: South America UK Wind Power Industry Revenue (billion), by Offshore 2025 & 2033

- Figure 20: South America UK Wind Power Industry Volume (Gigawatt), by Offshore 2025 & 2033

- Figure 21: South America UK Wind Power Industry Revenue Share (%), by Offshore 2025 & 2033

- Figure 22: South America UK Wind Power Industry Volume Share (%), by Offshore 2025 & 2033

- Figure 23: South America UK Wind Power Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: South America UK Wind Power Industry Volume (Gigawatt), by Country 2025 & 2033

- Figure 25: South America UK Wind Power Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America UK Wind Power Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe UK Wind Power Industry Revenue (billion), by Onshore 2025 & 2033

- Figure 28: Europe UK Wind Power Industry Volume (Gigawatt), by Onshore 2025 & 2033

- Figure 29: Europe UK Wind Power Industry Revenue Share (%), by Onshore 2025 & 2033

- Figure 30: Europe UK Wind Power Industry Volume Share (%), by Onshore 2025 & 2033

- Figure 31: Europe UK Wind Power Industry Revenue (billion), by Offshore 2025 & 2033

- Figure 32: Europe UK Wind Power Industry Volume (Gigawatt), by Offshore 2025 & 2033

- Figure 33: Europe UK Wind Power Industry Revenue Share (%), by Offshore 2025 & 2033

- Figure 34: Europe UK Wind Power Industry Volume Share (%), by Offshore 2025 & 2033

- Figure 35: Europe UK Wind Power Industry Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe UK Wind Power Industry Volume (Gigawatt), by Country 2025 & 2033

- Figure 37: Europe UK Wind Power Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe UK Wind Power Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa UK Wind Power Industry Revenue (billion), by Onshore 2025 & 2033

- Figure 40: Middle East & Africa UK Wind Power Industry Volume (Gigawatt), by Onshore 2025 & 2033

- Figure 41: Middle East & Africa UK Wind Power Industry Revenue Share (%), by Onshore 2025 & 2033

- Figure 42: Middle East & Africa UK Wind Power Industry Volume Share (%), by Onshore 2025 & 2033

- Figure 43: Middle East & Africa UK Wind Power Industry Revenue (billion), by Offshore 2025 & 2033

- Figure 44: Middle East & Africa UK Wind Power Industry Volume (Gigawatt), by Offshore 2025 & 2033

- Figure 45: Middle East & Africa UK Wind Power Industry Revenue Share (%), by Offshore 2025 & 2033

- Figure 46: Middle East & Africa UK Wind Power Industry Volume Share (%), by Offshore 2025 & 2033

- Figure 47: Middle East & Africa UK Wind Power Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa UK Wind Power Industry Volume (Gigawatt), by Country 2025 & 2033

- Figure 49: Middle East & Africa UK Wind Power Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa UK Wind Power Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific UK Wind Power Industry Revenue (billion), by Onshore 2025 & 2033

- Figure 52: Asia Pacific UK Wind Power Industry Volume (Gigawatt), by Onshore 2025 & 2033

- Figure 53: Asia Pacific UK Wind Power Industry Revenue Share (%), by Onshore 2025 & 2033

- Figure 54: Asia Pacific UK Wind Power Industry Volume Share (%), by Onshore 2025 & 2033

- Figure 55: Asia Pacific UK Wind Power Industry Revenue (billion), by Offshore 2025 & 2033

- Figure 56: Asia Pacific UK Wind Power Industry Volume (Gigawatt), by Offshore 2025 & 2033

- Figure 57: Asia Pacific UK Wind Power Industry Revenue Share (%), by Offshore 2025 & 2033

- Figure 58: Asia Pacific UK Wind Power Industry Volume Share (%), by Offshore 2025 & 2033

- Figure 59: Asia Pacific UK Wind Power Industry Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific UK Wind Power Industry Volume (Gigawatt), by Country 2025 & 2033

- Figure 61: Asia Pacific UK Wind Power Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific UK Wind Power Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global UK Wind Power Industry Revenue billion Forecast, by Onshore 2020 & 2033

- Table 2: Global UK Wind Power Industry Volume Gigawatt Forecast, by Onshore 2020 & 2033

- Table 3: Global UK Wind Power Industry Revenue billion Forecast, by Offshore 2020 & 2033

- Table 4: Global UK Wind Power Industry Volume Gigawatt Forecast, by Offshore 2020 & 2033

- Table 5: Global UK Wind Power Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global UK Wind Power Industry Volume Gigawatt Forecast, by Region 2020 & 2033

- Table 7: Global UK Wind Power Industry Revenue billion Forecast, by Onshore 2020 & 2033

- Table 8: Global UK Wind Power Industry Volume Gigawatt Forecast, by Onshore 2020 & 2033

- Table 9: Global UK Wind Power Industry Revenue billion Forecast, by Offshore 2020 & 2033

- Table 10: Global UK Wind Power Industry Volume Gigawatt Forecast, by Offshore 2020 & 2033

- Table 11: Global UK Wind Power Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global UK Wind Power Industry Volume Gigawatt Forecast, by Country 2020 & 2033

- Table 13: United States UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 15: Canada UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 17: Mexico UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 19: Global UK Wind Power Industry Revenue billion Forecast, by Onshore 2020 & 2033

- Table 20: Global UK Wind Power Industry Volume Gigawatt Forecast, by Onshore 2020 & 2033

- Table 21: Global UK Wind Power Industry Revenue billion Forecast, by Offshore 2020 & 2033

- Table 22: Global UK Wind Power Industry Volume Gigawatt Forecast, by Offshore 2020 & 2033

- Table 23: Global UK Wind Power Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global UK Wind Power Industry Volume Gigawatt Forecast, by Country 2020 & 2033

- Table 25: Brazil UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 27: Argentina UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 31: Global UK Wind Power Industry Revenue billion Forecast, by Onshore 2020 & 2033

- Table 32: Global UK Wind Power Industry Volume Gigawatt Forecast, by Onshore 2020 & 2033

- Table 33: Global UK Wind Power Industry Revenue billion Forecast, by Offshore 2020 & 2033

- Table 34: Global UK Wind Power Industry Volume Gigawatt Forecast, by Offshore 2020 & 2033

- Table 35: Global UK Wind Power Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global UK Wind Power Industry Volume Gigawatt Forecast, by Country 2020 & 2033

- Table 37: United Kingdom UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 39: Germany UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 41: France UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 43: Italy UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 45: Spain UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 47: Russia UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 49: Benelux UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 51: Nordics UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 55: Global UK Wind Power Industry Revenue billion Forecast, by Onshore 2020 & 2033

- Table 56: Global UK Wind Power Industry Volume Gigawatt Forecast, by Onshore 2020 & 2033

- Table 57: Global UK Wind Power Industry Revenue billion Forecast, by Offshore 2020 & 2033

- Table 58: Global UK Wind Power Industry Volume Gigawatt Forecast, by Offshore 2020 & 2033

- Table 59: Global UK Wind Power Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global UK Wind Power Industry Volume Gigawatt Forecast, by Country 2020 & 2033

- Table 61: Turkey UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 63: Israel UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 65: GCC UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 67: North Africa UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 69: South Africa UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 73: Global UK Wind Power Industry Revenue billion Forecast, by Onshore 2020 & 2033

- Table 74: Global UK Wind Power Industry Volume Gigawatt Forecast, by Onshore 2020 & 2033

- Table 75: Global UK Wind Power Industry Revenue billion Forecast, by Offshore 2020 & 2033

- Table 76: Global UK Wind Power Industry Volume Gigawatt Forecast, by Offshore 2020 & 2033

- Table 77: Global UK Wind Power Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global UK Wind Power Industry Volume Gigawatt Forecast, by Country 2020 & 2033

- Table 79: China UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 81: India UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 83: Japan UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 85: South Korea UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 87: ASEAN UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 89: Oceania UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific UK Wind Power Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific UK Wind Power Industry Volume (Gigawatt) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the UK Wind Power Industry?

The projected CAGR is approximately 11.7%.

2. Which companies are prominent players in the UK Wind Power Industry?

Key companies in the market include Vattenfall AB, Siemens Gamesa Renewable Energy SA, Electricite de France S, Suzlon Energy Ltd, Vestas Wind Systems AS, General Electric Company, Orsted AS.

3. What are the main segments of the UK Wind Power Industry?

The market segments include Onshore, Offshore.

4. Can you provide details about the market size?

The market size is estimated to be USD 39.3 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Reduction in Energy Bills Due to Self-Power Consumption4.; Increasing Installation of Solar PV Modules in Residential Segment.

6. What are the notable trends driving market growth?

Offshore Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; High Installation Cost as Compared to Rooftop PV Systems.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in Gigawatt.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "UK Wind Power Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the UK Wind Power Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the UK Wind Power Industry?

To stay informed about further developments, trends, and reports in the UK Wind Power Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence