Key Insights

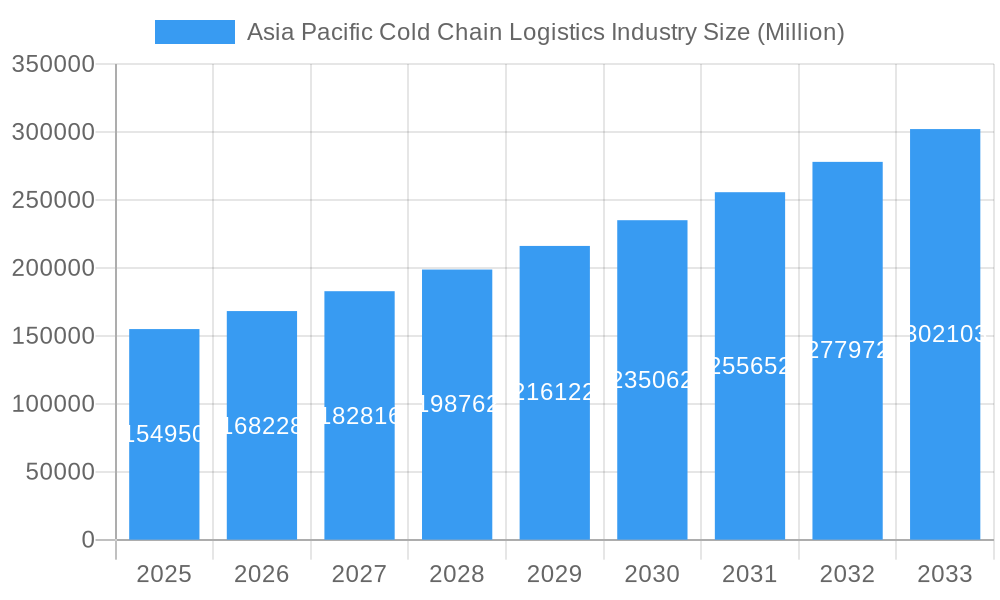

The Asia-Pacific cold chain logistics market is experiencing robust growth, driven by rising disposable incomes, expanding e-commerce, and a growing preference for fresh and processed foods across the region. The market, valued at $154.95 billion in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 8.58% from 2025 to 2033. This expansion is fueled by several key factors. Firstly, the burgeoning middle class in countries like China, India, and Indonesia is driving increased demand for temperature-sensitive products, necessitating efficient cold chain solutions. Secondly, the rapid growth of e-commerce, particularly for grocery and pharmaceuticals, is creating a significant need for reliable and scalable cold chain logistics networks to ensure product quality and safety during delivery. Furthermore, government initiatives promoting food safety and infrastructure development in several Asia-Pacific nations are further stimulating market growth. Significant segments within the market include refrigerated transportation, warehousing, and value-added services such as blast freezing and inventory management. The horticulture sector, particularly fresh fruits and vegetables, constitutes a substantial portion of the market, alongside dairy, meat, and processed food applications.

Asia Pacific Cold Chain Logistics Industry Market Size (In Billion)

The competitive landscape is marked by a mix of large multinational players and regional logistics providers. Companies like SCG Logistics, CWT, and SF Express are key players, competing on factors such as network reach, technological capabilities, and service offerings. While challenges exist, such as infrastructure limitations in certain regions and the need for cold chain technology advancements, the overall outlook remains positive. Continued investment in infrastructure, technological innovation, and a focus on sustainability will be crucial for companies to capitalize on the long-term growth opportunities presented by this expanding market. The increasing adoption of advanced technologies such as IoT sensors for real-time monitoring and data analytics will also play a crucial role in optimizing cold chain efficiency and minimizing losses. Specific growth will be seen across the various temperature types (chilled and frozen) and applications, with significant expansion anticipated in countries beyond the major economies.

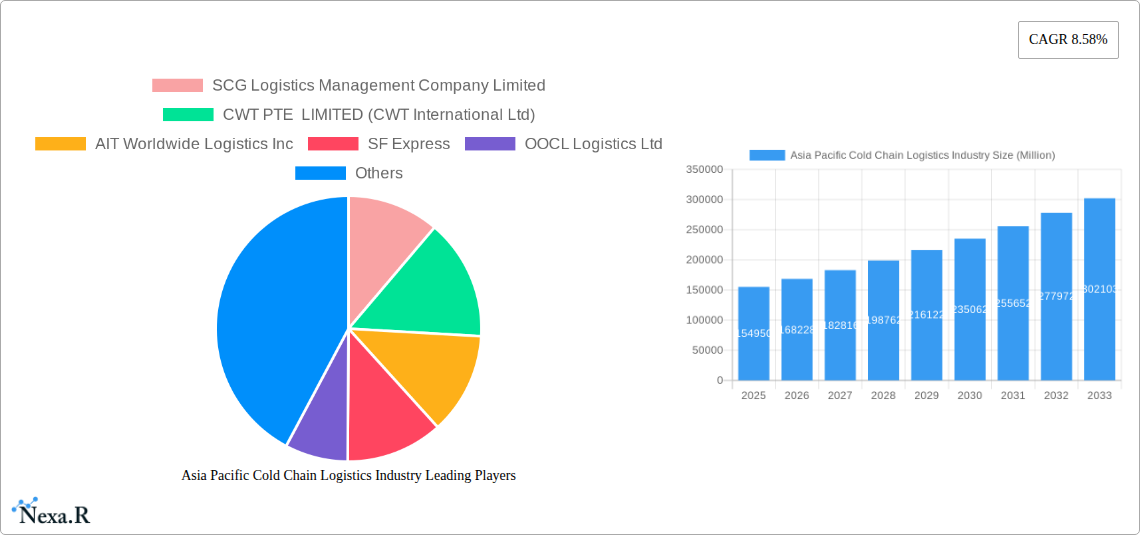

Asia Pacific Cold Chain Logistics Industry Company Market Share

This comprehensive report offers an in-depth analysis of the Asia Pacific cold chain logistics industry, providing invaluable insights for industry professionals, investors, and strategic planners. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report leverages extensive data analysis to deliver a clear understanding of market dynamics, growth trends, and future opportunities. The report covers key segments including storage, transportation, and value-added services, across various temperature types and applications, and analyzes the performance of key players like SCG Logistics, CWT, and others. This report is crucial for navigating the complexities of this rapidly evolving market and capitalizing on emerging opportunities.

Asia Pacific Cold Chain Logistics Industry Market Dynamics & Structure

The Asia Pacific cold chain logistics market is a dynamic and evolving sector, characterized by a blend of established global players and agile regional specialists, leading to a moderately concentrated landscape. The industry's trajectory is significantly influenced by relentless technological innovation, particularly in the realms of advanced temperature monitoring systems and increasing automation within warehouses and during transportation. This technological push is complemented by a robust and evolving regulatory framework, with a sharp focus on ensuring food safety standards and the integrity of pharmaceutical and healthcare product handling. Emerging competitive substitutes, such as advanced insulated packaging solutions and the integration of data analytics for predictive maintenance, are also reshaping competitive strategies. The fundamental undercurrent of demand is powerfully driven by favorable end-user demographics, prominently featuring a burgeoning middle class with rising disposable incomes and a growing appetite for high-quality, temperature-sensitive goods. Mergers and acquisitions (M&A) remain a moderately active strategy, with companies actively pursuing opportunities to expand their geographical service reach, bolster their technological capabilities, and achieve greater economies of scale.

- Market Concentration: Moderately concentrated, with the top 5 players holding an estimated market share of approximately 40-50%.

- Technological Innovation: Significant focus on the integration of IoT for real-time data collection, AI-powered predictive analytics for route optimization and demand forecasting, and advancements in automated storage and retrieval systems (AS/RS).

- Regulatory Landscape: Increasingly stringent global and regional regulations concerning food safety (e.g., HACCP, FSSC 22000) and pharmaceutical handling (e.g., Good Distribution Practices - GDP) are shaping operational standards, necessitating higher investment in compliance and advanced monitoring.

- M&A Activity: Approximately 30-40 strategic deals were recorded between 2019-2024, with an average deal value in the range of USD 50-150 million, reflecting consolidation and expansion efforts.

- Innovation Barriers: Significant barriers include the substantial initial investment costs for adopting cutting-edge technologies, the persistent challenge of a lack of adequately skilled workforce in certain developing regions, and navigating diverse and evolving regulatory requirements across multiple countries.

Asia Pacific Cold Chain Logistics Industry Growth Trends & Insights

The Asia Pacific cold chain logistics market experienced a period of remarkable and robust growth between 2019 and 2024. This expansion was propelled by a confluence of powerful economic and societal shifts: a significant rise in disposable incomes across the region, evolving consumer preferences leaning towards fresh, high-quality, and processed food items, and the explosive growth of e-commerce, which necessitates more sophisticated last-mile delivery solutions for temperature-sensitive products. This impressive growth momentum is projected to continue through the forecast period of 2025-2033, although it is anticipated to mature and potentially moderate slightly as the market becomes more established. A pivotal catalyst for this sustained expansion is the rapid adoption of advanced technologies, notably the integration of the Internet of Things (IoT) for granular tracking and the implementation of blockchain technology to ensure unprecedented levels of transparency and traceability throughout the supply chain. Furthermore, the escalating global demand for temperature-sensitive pharmaceuticals and biologics, driven by advancements in healthcare and an aging population, represents a critical and growing segment contributing significantly to the overall market's upward trajectory.

- Market Size (2024): Estimated at USD 45-55 Billion

- Market Size (2033): Projected to reach USD 90-110 Billion

- CAGR (2025-2033): Approximately 7-9%

- Market Penetration (2024): Estimated at 30-40% of the total logistics market

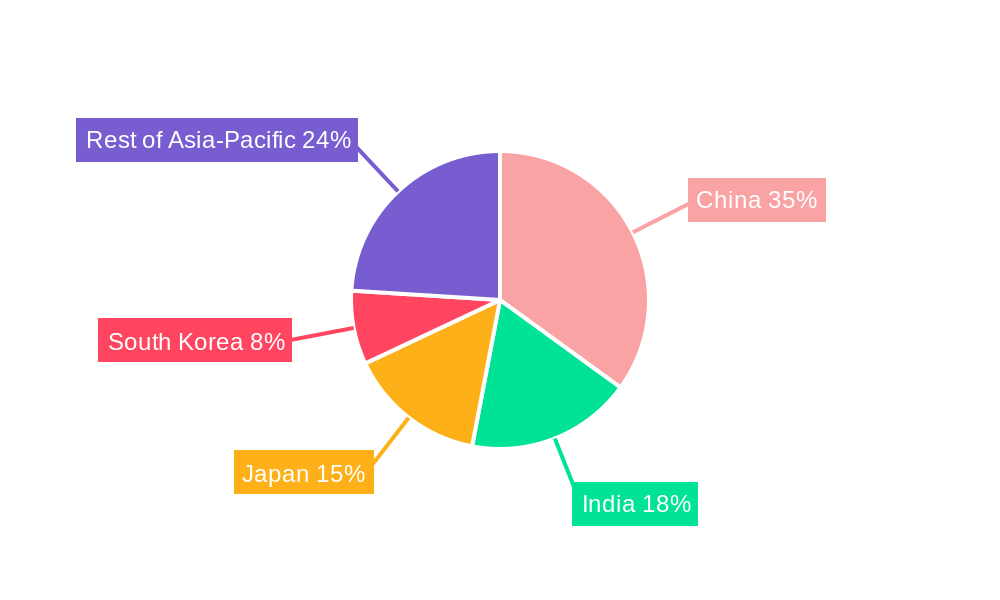

Dominant Regions, Countries, or Segments in Asia Pacific Cold Chain Logistics Industry

China remains the dominant market, driven by its massive population, robust food processing industry, and expanding e-commerce sector. India and other Southeast Asian nations are experiencing rapid growth fueled by economic expansion and infrastructure development. Within segments, the refrigerated transportation segment holds the largest market share, followed by storage and value-added services. The food and beverage industry remains the largest application segment.

- Leading Countries: China (xx% market share), India (xx%), Japan (xx%).

- Leading Segments (By Services): Transportation (xx%), Storage (xx%), Value-added Services (xx%)

- Leading Segments (By Temperature): Frozen (xx%), Chilled (xx%)

- Leading Segments (By Application): Food & Beverage (xx%), Pharmaceuticals (xx%).

- Growth Drivers: Rising disposable incomes, increasing urbanization, expanding e-commerce, government support for cold chain infrastructure development.

Asia Pacific Cold Chain Logistics Industry Product Landscape

The product landscape within the Asia Pacific cold chain logistics industry is defined by continuous and strategic innovation, with a primary focus on delivering enhanced and reliable temperature control, enabling real-time monitoring capabilities, and optimizing the efficiency of the entire logistics management process. Key innovations include the development and widespread adoption of 'smart' containers and reefer units, meticulously equipped with advanced GPS tracking for precise location monitoring and integrated temperature sensors that transmit data continuously. Complementing these hardware advancements are sophisticated software platforms designed to intelligently optimize delivery routes, manage inventory levels dynamically, and provide predictive insights into potential disruptions. These integrated technological solutions are instrumental in dramatically improving supply chain visibility, significantly reducing product spoilage and waste, and ultimately enhancing the overall operational efficiency and reliability of cold chain operations.

Key Drivers, Barriers & Challenges in Asia Pacific Cold Chain Logistics Industry

Key Drivers:

- Increasing consumer demand for a wider variety of fresh produce, dairy, frozen foods, and ready-to-eat meals across the region.

- The rapid expansion of e-commerce platforms and the burgeoning online grocery delivery sector, which necessitates robust cold chain capabilities for timely and safe delivery.

- A growing middle class with rising disposable incomes leading to increased consumption of premium and perishable goods.

- Proactive government initiatives and investments aimed at modernizing and expanding cold chain infrastructure, including ports, airports, and distribution centers, particularly in developing economies.

- The escalating demand for the secure and reliable transportation of temperature-sensitive pharmaceuticals, vaccines, and biologics.

Challenges:

- High capital expenditure required for developing and maintaining adequate cold chain infrastructure, including refrigerated warehouses, specialized transportation fleets, and last-mile delivery solutions, especially in regions with underdeveloped facilities.

- A persistent lack of a sufficiently skilled and trained workforce capable of operating and maintaining advanced cold chain equipment and adhering to stringent operational protocols.

- Navigating and complying with a complex and often disparate web of regulatory requirements across different countries within the Asia Pacific region, impacting operational costs and timelines.

- The critical challenge of maintaining consistent and precise temperature control throughout the entire supply chain, from origin to destination, with significant annual losses estimated at USD 5-10 billion due to temperature excursions and product spoilage.

- Geopolitical instability and evolving trade policies can create disruptions and uncertainties in cross-border cold chain logistics.

Emerging Opportunities in Asia Pacific Cold Chain Logistics Industry

- Expansion into underserved rural markets

- Growth in specialized cold chain solutions for pharmaceuticals and other temperature-sensitive products

- Increasing demand for value-added services such as packaging, labeling, and inventory management

- Adoption of sustainable and eco-friendly cold chain technologies.

Growth Accelerators in the Asia Pacific Cold Chain Logistics Industry Industry

Technological advancements, strategic partnerships, and government policies supporting infrastructure development are key catalysts for long-term growth. Investments in IoT, AI, and blockchain technologies are transforming the efficiency and transparency of cold chain operations, leading to improved logistics management, reduced spoilage, and enhanced customer satisfaction.

Key Players Shaping the Asia Pacific Cold Chain Logistics Industry Market

- SCG Logistics Management Company Limited

- CWT PTE LIMITED (CWT International Ltd)

- AIT Worldwide Logistics Inc

- SF Express

- OOCL Logistics Ltd

- CJ Rokin Logistics

- Nichirei Logistics Group Inc

- United Parcel Service of America

- X2 Logistics Network (X2 GROUP)

- JWD Infologistics Public Company Ltd

Notable Milestones in Asia Pacific Cold Chain Logistics Industry Sector

- September 2022: SCG Logistics, in collaboration with DENSO Sales (Thailand) and Toyota Tsusho Thailand, announced a significant partnership aimed at enhancing Thailand's refrigeration ecosystem and promoting sustainable cold chain solutions.

- October 2022: UPS strategically expanded its specialized Premier service, designed for time-sensitive and high-value shipments, to include key markets like Thailand and Singapore, bolstering its capabilities in the Asia Pacific region.

- Early 2023: Major logistics providers have been investing heavily in expanding their refrigerated warehousing capacity and upgrading their fleets with advanced temperature-monitoring technology to meet the growing demand for pharmaceutical and perishable goods.

- Mid 2023: Several governments within Southeast Asia have unveiled new policies and incentives to encourage private sector investment in cold chain infrastructure development, recognizing its importance for food security and economic growth.

- Late 2023: The integration of AI and IoT solutions has become more prominent, with companies reporting increased efficiency and reduced spoilage rates through predictive analytics and real-time data management.

In-Depth Asia Pacific Cold Chain Logistics Industry Market Outlook

The Asia Pacific cold chain logistics market is poised for significant growth, driven by technological advancements, infrastructure development, and rising consumer demand. Strategic partnerships, investments in innovative technologies, and expansion into new markets will be crucial for companies seeking to capitalize on this growth. The continued focus on enhancing efficiency, improving temperature control, and strengthening supply chain resilience will shape the future of this dynamic industry.

Asia Pacific Cold Chain Logistics Industry Segmentation

-

1. Services

- 1.1. Storage

- 1.2. Transportation

- 1.3. Value-ad

-

2. Temperature Type

- 2.1. Chilled

- 2.2. Frozen

-

3. Application

- 3.1. Horticulture (Fresh Fruits and Vegetables)

- 3.2. Dairy Products (Milk, Ice-cream, Butter, Etc.)

- 3.3. Meats, Fish, Poultry

- 3.4. Processed Food Products

- 3.5. Pharma, Life Sciences, and Chemicals

- 3.6. Other Applications

Asia Pacific Cold Chain Logistics Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia Pacific Cold Chain Logistics Industry Regional Market Share

Geographic Coverage of Asia Pacific Cold Chain Logistics Industry

Asia Pacific Cold Chain Logistics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.58% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Services

- 5.1.1. Storage

- 5.1.2. Transportation

- 5.1.3. Value-ad

- 5.2. Market Analysis, Insights and Forecast - by Temperature Type

- 5.2.1. Chilled

- 5.2.2. Frozen

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Horticulture (Fresh Fruits and Vegetables)

- 5.3.2. Dairy Products (Milk, Ice-cream, Butter, Etc.)

- 5.3.3. Meats, Fish, Poultry

- 5.3.4. Processed Food Products

- 5.3.5. Pharma, Life Sciences, and Chemicals

- 5.3.6. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Services

- 6. Asia Pacific Cold Chain Logistics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Services

- 6.1.1. Storage

- 6.1.2. Transportation

- 6.1.3. Value-ad

- 6.2. Market Analysis, Insights and Forecast - by Temperature Type

- 6.2.1. Chilled

- 6.2.2. Frozen

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Horticulture (Fresh Fruits and Vegetables)

- 6.3.2. Dairy Products (Milk, Ice-cream, Butter, Etc.)

- 6.3.3. Meats, Fish, Poultry

- 6.3.4. Processed Food Products

- 6.3.5. Pharma, Life Sciences, and Chemicals

- 6.3.6. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Services

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 SCG Logistics Management Company Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 CWT PTE LIMITED (CWT International Ltd)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 AIT Worldwide Logistics Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 SF Express

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 OOCL Logistics Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 CJ Rokin Logistics**List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Nichirei Logistics Group Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 United Parcel Service of America

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 X2 Logistics Network (X2 GROUP)

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 JWD Infologistics Public Company Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 SCG Logistics Management Company Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia Pacific Cold Chain Logistics Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia Pacific Cold Chain Logistics Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Services 2020 & 2033

- Table 2: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Temperature Type 2020 & 2033

- Table 3: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Services 2020 & 2033

- Table 6: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Temperature Type 2020 & 2033

- Table 7: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 8: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: China Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Japan Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: South Korea Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: India Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Australia Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: New Zealand Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Indonesia Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Malaysia Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Singapore Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Thailand Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Vietnam Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Philippines Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia Pacific Cold Chain Logistics Industry?

The projected CAGR is approximately 8.58%.

2. Which companies are prominent players in the Asia Pacific Cold Chain Logistics Industry?

Key companies in the market include SCG Logistics Management Company Limited, CWT PTE LIMITED (CWT International Ltd), AIT Worldwide Logistics Inc, SF Express, OOCL Logistics Ltd, CJ Rokin Logistics**List Not Exhaustive, Nichirei Logistics Group Inc, United Parcel Service of America, X2 Logistics Network (X2 GROUP), JWD Infologistics Public Company Ltd.

3. What are the main segments of the Asia Pacific Cold Chain Logistics Industry?

The market segments include Services, Temperature Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 154.95 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing international trade; Advancements in technology.

6. What are the notable trends driving market growth?

Decreasing Volume of Domestic Water Freight Transport in Japan.

7. Are there any restraints impacting market growth?

Geopolitical uncertainities; Changing trade policies.

8. Can you provide examples of recent developments in the market?

October 2022: Express giant UPS expanded its Premier service for time and temperature-sensitive shipments to Thailand and Singapore. The service offers to track and prioritize loads and has three tiers, with Premier Gold service available in two locations.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia Pacific Cold Chain Logistics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia Pacific Cold Chain Logistics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia Pacific Cold Chain Logistics Industry?

To stay informed about further developments, trends, and reports in the Asia Pacific Cold Chain Logistics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence