Key Insights

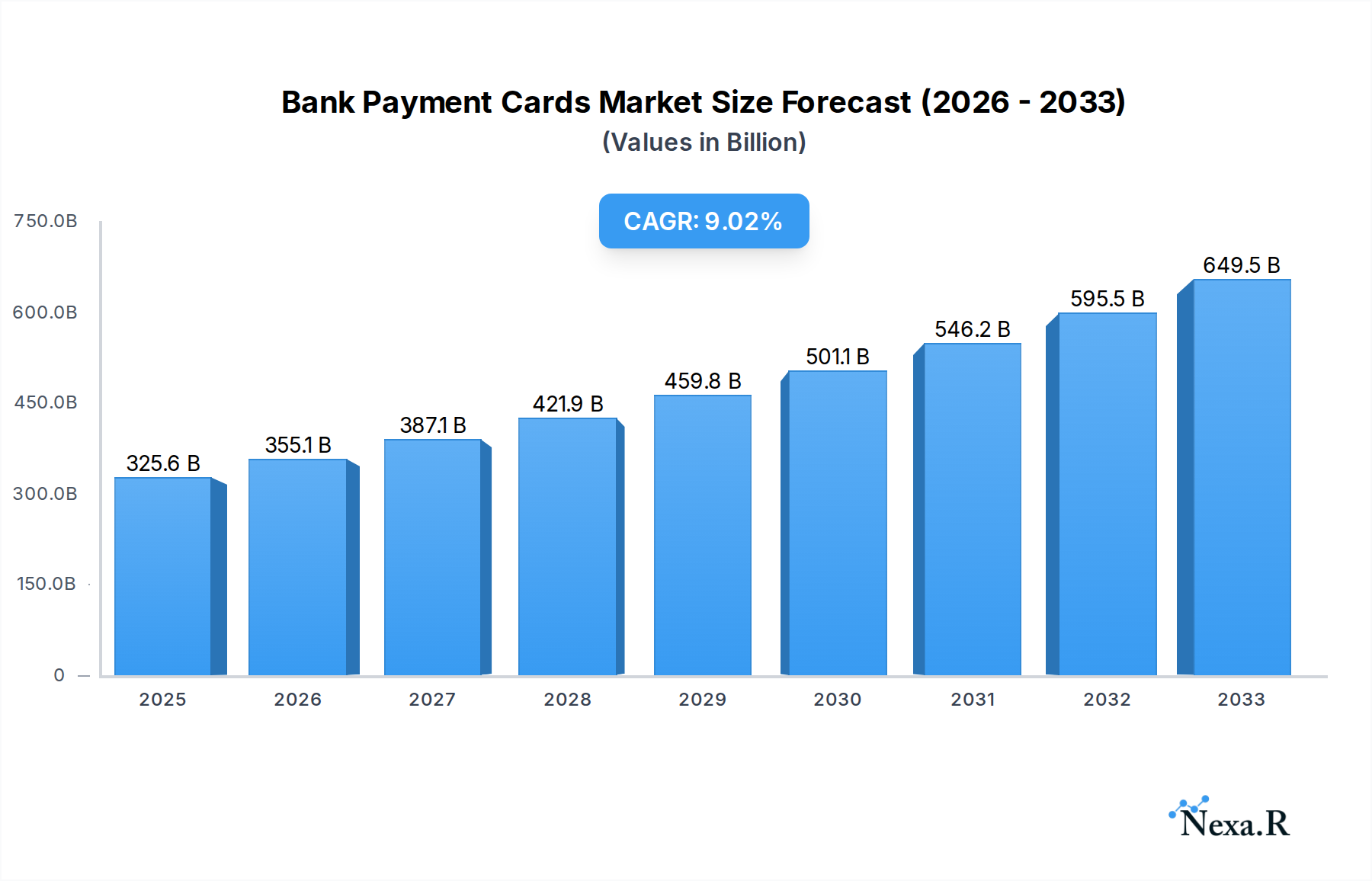

The global market for bank payment cards is poised for substantial expansion, projected to reach an estimated $325.6 billion in 2025, exhibiting a robust compound annual growth rate (CAGR) of 9.3% through 2033. This dynamic growth is fueled by a confluence of factors, including the increasing adoption of digital payment solutions, the continuous innovation in card technologies such as contactless and EMV chips, and the growing consumer preference for secure and convenient transaction methods. The personal use segment, driven by expanding e-commerce and mobile payment integration, is a significant contributor, while the business use segment benefits from the need for streamlined corporate expense management and B2B transaction efficiency. Key players like Gemalto, IDEMIA, and Giesecke & Devrient are at the forefront of this market, investing heavily in research and development to offer advanced security features and personalized card solutions.

Bank Payment Cards Market Size (In Billion)

The market's trajectory is further shaped by emerging trends such as the integration of biometric authentication, the rise of tokenization for enhanced security, and the increasing demand for specialized cards catering to specific demographics and financial needs. While the convenience and security offered by bank payment cards are primary drivers, potential restraints include increasing concerns around data privacy and security breaches, as well as regulatory hurdles in certain regions. Geographically, Asia Pacific, led by China and India, is anticipated to witness the most significant growth due to its large, increasingly affluent population and rapid digital transformation. North America and Europe remain mature markets with high penetration rates, focusing on innovation and enhanced user experience. The ongoing shift from traditional payment methods to secure, card-based transactions underpins the optimistic outlook for this vital sector of the financial industry.

Bank Payment Cards Company Market Share

Comprehensive Report: Global Bank Payment Cards Market Outlook 2024-2033

Uncover the dynamic landscape of the global bank payment cards market, a critical component of modern financial ecosystems. This in-depth report analyzes market size, growth drivers, regional dominance, and key players, providing essential insights for strategic decision-making. With a study period spanning 2019–2033, a base year of 2025, and a forecast period from 2025–2033, this report offers a forward-looking perspective on this rapidly evolving industry.

Bank Payment Cards Market Dynamics & Structure

The global bank payment cards market exhibits a moderately concentrated structure, driven by continuous technological innovation and evolving regulatory frameworks. Key companies like Gemalto, IDEMIA, and Giesecke and Devrient hold significant market share, primarily through their advanced card manufacturing, personalization, and security solutions. Technological innovation is a paramount driver, encompassing the widespread adoption of EMV chips, contactless payment technologies (NFC), and the increasing integration of biometric authentication for enhanced security. Regulatory frameworks, such as those governing data privacy (e.g., GDPR) and payment security standards (e.g., PCI DSS), significantly influence market operations and product development. Competitive product substitutes, including mobile payment solutions and digital wallets, pose an evolving challenge, pushing card manufacturers to enhance the value proposition of physical cards through added security features and loyalty integrations. End-user demographics are shifting, with a growing demand for personalized and secure payment options from both individuals and businesses. Mergers and acquisitions (M&A) trends are active, with larger players acquiring smaller, specialized firms to expand their technology portfolios and geographic reach. For instance, significant M&A activity in the past has seen consolidation in the card manufacturing and personalization services sector, with an estimated XX billion in deal volumes during the historical period. Barriers to innovation include the high cost of developing and implementing new security technologies and the long certification processes required by financial institutions.

- Market Concentration: Moderately concentrated with key players like Gemalto, IDEMIA, and Giesecke and Devrient.

- Technological Drivers: EMV chip technology, NFC contactless payments, biometric authentication, tokenization.

- Regulatory Frameworks: GDPR, PCI DSS, evolving central bank digital currency (CBDC) initiatives.

- Competitive Substitutes: Mobile wallets, digital payment apps, buy now, pay later (BNPL) services.

- End-User Demographics: Growing demand for personalized, secure, and convenient payment solutions across personal and business segments.

- M&A Trends: Active consolidation, particularly in card manufacturing and personalization.

- Innovation Barriers: High R&D costs, lengthy certification cycles, legacy system integration.

Bank Payment Cards Growth Trends & Insights

The global bank payment cards market is poised for robust growth, propelled by a confluence of economic, technological, and behavioral shifts. The market size is projected to reach an estimated $XXX billion by 2033, exhibiting a compound annual growth rate (CAGR) of approximately XX% from the base year of 2025. This expansion is driven by increasing global financial inclusion, the growing preference for cashless transactions, and the continuous evolution of payment technologies. Adoption rates of advanced payment cards, particularly those equipped with contactless capabilities and enhanced security features, are steadily rising across both developed and emerging economies. Technological disruptions, such as the integration of AI for fraud detection and personalized offers, are further enhancing the value and utility of payment cards. Consumer behavior is a critical factor, with an increasing reliance on digital payment methods for everyday purchases, online shopping, and business expenditures. The convenience and security offered by payment cards, especially in comparison to managing large amounts of cash, are key drivers of this shift. Furthermore, the rise of prepaid and gift cards, catering to specific consumer needs for budgeting and gifting, adds another layer of market dynamism. The expansion of e-commerce and the digital economy further fuels the demand for secure and reliable payment instruments. By 2025, the market is expected to witness a significant penetration of dual-interface cards, supporting both contact and contactless transactions, thereby streamlining the payment experience. The increasing issuance of credit cards for online transactions and debit cards for everyday spending will continue to dominate market share. Other types of cards, including gift cards, loyalty cards, and transit cards, will also see substantial growth, driven by niche applications and partnerships. The evolution of payment infrastructure, with a greater emphasis on interoperability and real-time transaction processing, will also contribute to sustained market expansion. The increasing adoption of EMV chip technology globally has already laid a strong foundation for secure transactions, and future growth will be shaped by the seamless integration of these cards into broader digital payment ecosystems. The parent market, encompassing all forms of payment instruments, will see the bank payment cards segment capture a substantial and growing portion due to their versatility and widespread acceptance.

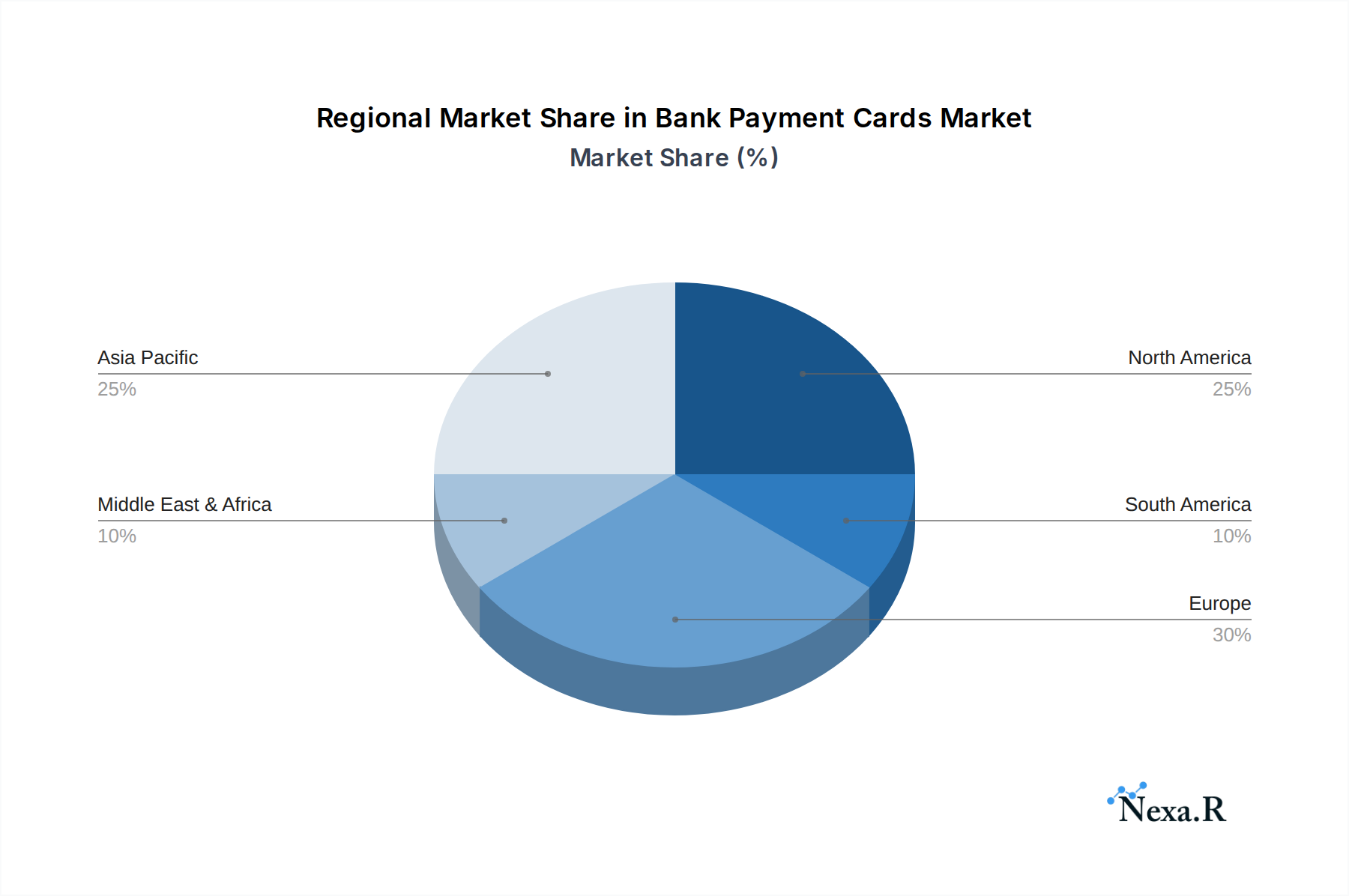

Dominant Regions, Countries, or Segments in Bank Payment Cards

The Asia Pacific region is projected to be the dominant force in the global bank payment cards market, driven by a confluence of rapidly expanding economies, a burgeoning middle class, and a significant push towards digital transformation. Countries like China and India are at the forefront, fueled by government initiatives promoting financial inclusion, a substantial unbanked population transitioning to digital banking, and an explosion in e-commerce. China, in particular, with its advanced mobile payment infrastructure, is also seeing a parallel growth in card issuance to complement these digital services, especially for international transactions and specific merchant categories. India's vast population and increasing disposable income, coupled with widespread smartphone adoption, are creating an immense demand for payment cards across all segments.

In terms of Application, Personal Use will continue to be the largest segment. The increasing reliance on credit and debit cards for daily expenses, online shopping, travel, and entertainment by a growing global population underpins this dominance. However, Business Use is expected to exhibit a higher growth rate, driven by the digitalization of corporate expenses, the need for streamlined procurement, and the increasing adoption of commercial credit cards and fleet cards for operational efficiency. Businesses are actively seeking payment solutions that offer better expense management, control, and data analytics.

Analyzing the Types of cards, Debit Cards are anticipated to maintain their leading position due to their accessibility, ease of use for everyday transactions, and the inherent security of transacting with available funds, thereby appealing to a broad consumer base concerned about debt. Credit Cards will remain a crucial segment, vital for building credit history, facilitating larger purchases, and offering attractive rewards programs that incentivize consumer spending. The "Others" category, encompassing prepaid cards, gift cards, transit cards, and co-branded cards, will witness significant expansion, driven by their niche applications, gifting culture, and targeted loyalty programs. Prepaid cards, in particular, are gaining traction as a budgeting tool and for specific use cases like online gaming and international remittances. The parent market for payment instruments sees bank payment cards as the primary vehicle for formal financial transactions, driving significant value within the broader financial services industry.

- Dominant Region: Asia Pacific (especially China and India).

- Key Drivers (Regional): Economic growth, financial inclusion initiatives, e-commerce surge, digital payment adoption.

- Dominant Application: Personal Use.

- High Growth Application: Business Use (driven by corporate digitalization).

- Dominant Type: Debit Cards.

- Significant Segment: Credit Cards (for credit building and rewards).

- High Growth Type: Others (Prepaid, Gift, Co-branded cards).

Bank Payment Cards Product Landscape

The bank payment cards product landscape is characterized by continuous innovation focused on enhanced security, convenience, and personalization. Modern payment cards are increasingly featuring EMV chip technology for secure transactions, alongside NFC contactless capabilities for swift payments. Biometric authentication, such as fingerprint sensors embedded directly onto the card, is emerging as a significant differentiator, offering an unparalleled level of security and user experience. The integration of advanced security features like tokenization and dynamic data encryption further fortifies these cards against fraud. Beyond security, product differentiation is driven by co-branding opportunities with retailers, airlines, and other service providers, offering exclusive rewards and benefits. The material science of card production is also evolving, with a growing trend towards eco-friendly options like recycled plastics and biodegradable materials. Performance metrics are evaluated on transaction success rates, fraud detection effectiveness, and user adoption of advanced features.

Key Drivers, Barriers & Challenges in Bank Payment Cards

The bank payment cards market is propelled by several key drivers. Technological Advancements like EMV chip migration, contactless technology, and biometric authentication are central to enhancing security and user experience. Increasing Financial Inclusion globally, especially in emerging economies, is expanding the customer base for payment cards. The Growth of E-commerce and Digital Payments necessitates secure and convenient payment instruments. Government Initiatives promoting cashless economies and digital transactions also play a crucial role.

Conversely, the market faces significant barriers and challenges. Cybersecurity Threats and Data Breaches remain a constant concern, eroding consumer trust and necessitating continuous investment in security infrastructure. High Implementation Costs for new technologies and infrastructure upgrades can be a deterrent for smaller financial institutions. Regulatory Compliance with evolving data privacy and payment security standards adds complexity and cost. Intense Competition from alternative payment methods like mobile wallets and BNPL services requires continuous innovation and value proposition enhancement. Supply chain disruptions for raw materials like plastic and microchips can also impact production timelines and costs.

Emerging Opportunities in Bank Payment Cards

Emerging opportunities in the bank payment cards industry lie in the growing demand for contactless and mobile-integrated payment solutions. The proliferation of biometric authentication on cards presents a significant avenue for enhanced security and user convenience. The development of eco-friendly and sustainable card materials caters to a growing consumer consciousness. Furthermore, embedded payment functionalities within wearables and other IoT devices represent a nascent but promising area for expansion. Untapped markets in developing regions, coupled with the increasing adoption of digital currencies and tokenized assets, offer potential for innovative card-based solutions.

Growth Accelerators in the Bank Payment Cards Industry

Several catalysts are accelerating growth in the bank payment cards industry. The ongoing global shift towards cashless societies is a primary accelerator, as consumers and businesses increasingly favor digital transactions. Strategic partnerships between card issuers, technology providers, and retailers are fostering innovation and creating new revenue streams through co-branded cards and integrated loyalty programs. The expansion of e-commerce and cross-border digital trade directly fuels the demand for secure and universally accepted payment cards. Furthermore, advancements in AI and machine learning for fraud detection and personalized customer experiences are enhancing the value proposition of payment cards, driving adoption and retention.

Key Players Shaping the Bank Payment Cards Market

- Gemalto

- IDEMIA

- Giesecke and Devrient

- Perfect Plastic Printing

- ABCorp

- CPI Card

- Tianyu

- Goldpac

- Hengbao

- Watchdata Technologies

- Valid

- Kona I

- Eastcompeace

- Segments

Notable Milestones in Bank Payment Cards Sector

- 2019: Widespread global rollout of EMV chip technology becomes standard for most payment cards.

- 2020: Accelerated adoption of contactless payments driven by public health concerns and convenience.

- 2021: Increased investment in biometric card technology, with pilot programs and early product launches.

- 2022: Growing interest and initial deployments of cards supporting tokenized payments for enhanced online security.

- 2023: Expansion of co-branded card partnerships with focus on niche markets and loyalty programs.

- 2024: Emergence of sustainable and eco-friendly card materials gaining traction among consumers and issuers.

In-Depth Bank Payment Cards Market Outlook

The future of the bank payment cards market is exceptionally bright, driven by continued technological innovation and evolving consumer preferences. Growth accelerators like the global push towards cashless economies, strategic co-branding initiatives, and the expansion of e-commerce will fuel sustained expansion. The increasing integration of advanced security features, including biometrics and tokenization, will solidify payment cards as the trusted backbone of digital transactions. Opportunities in emerging markets and the potential for embedding payment functionalities into diverse devices present significant avenues for future growth, ensuring the bank payment cards sector remains a dynamic and indispensable part of the global financial landscape.

Bank Payment Cards Segmentation

-

1. Application

- 1.1. Personal Use

- 1.2. Business Use

-

2. Types

- 2.1. Credit Cards

- 2.2. Debit Cards

- 2.3. Others

Bank Payment Cards Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Bank Payment Cards Regional Market Share

Geographic Coverage of Bank Payment Cards

Bank Payment Cards REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Bank Payment Cards Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Personal Use

- 5.1.2. Business Use

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Credit Cards

- 5.2.2. Debit Cards

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Bank Payment Cards Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Personal Use

- 6.1.2. Business Use

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Credit Cards

- 6.2.2. Debit Cards

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Bank Payment Cards Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Personal Use

- 7.1.2. Business Use

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Credit Cards

- 7.2.2. Debit Cards

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Bank Payment Cards Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Personal Use

- 8.1.2. Business Use

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Credit Cards

- 8.2.2. Debit Cards

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Bank Payment Cards Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Personal Use

- 9.1.2. Business Use

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Credit Cards

- 9.2.2. Debit Cards

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Bank Payment Cards Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Personal Use

- 10.1.2. Business Use

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Credit Cards

- 10.2.2. Debit Cards

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Gemalto

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 IDEMIA

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Giesecke and Devrient

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Perfect Plastic Printing

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 ABCorp

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 CPI Card

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Tianyu

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Goldpac

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Hengbao

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Watchdata Technologies

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Valid

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Kona I

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Eastcompeace

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 Gemalto

List of Figures

- Figure 1: Global Bank Payment Cards Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Bank Payment Cards Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Bank Payment Cards Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Bank Payment Cards Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Bank Payment Cards Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Bank Payment Cards Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Bank Payment Cards Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Bank Payment Cards Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Bank Payment Cards Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Bank Payment Cards Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Bank Payment Cards Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Bank Payment Cards Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Bank Payment Cards Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Bank Payment Cards Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Bank Payment Cards Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Bank Payment Cards Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Bank Payment Cards Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Bank Payment Cards Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Bank Payment Cards Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Bank Payment Cards Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Bank Payment Cards Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Bank Payment Cards Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Bank Payment Cards Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Bank Payment Cards Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Bank Payment Cards Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Bank Payment Cards Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Bank Payment Cards Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Bank Payment Cards Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Bank Payment Cards Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Bank Payment Cards Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Bank Payment Cards Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Bank Payment Cards Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Bank Payment Cards Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Bank Payment Cards Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Bank Payment Cards Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Bank Payment Cards Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Bank Payment Cards Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Bank Payment Cards Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Bank Payment Cards Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Bank Payment Cards Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Bank Payment Cards Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Bank Payment Cards Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Bank Payment Cards Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Bank Payment Cards Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Bank Payment Cards Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Bank Payment Cards Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Bank Payment Cards Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Bank Payment Cards Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Bank Payment Cards Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Bank Payment Cards Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Bank Payment Cards?

The projected CAGR is approximately 9.3%.

2. Which companies are prominent players in the Bank Payment Cards?

Key companies in the market include Gemalto, IDEMIA, Giesecke and Devrient, Perfect Plastic Printing, ABCorp, CPI Card, Tianyu, Goldpac, Hengbao, Watchdata Technologies, Valid, Kona I, Eastcompeace.

3. What are the main segments of the Bank Payment Cards?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Bank Payment Cards," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Bank Payment Cards report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Bank Payment Cards?

To stay informed about further developments, trends, and reports in the Bank Payment Cards, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence