Key Insights

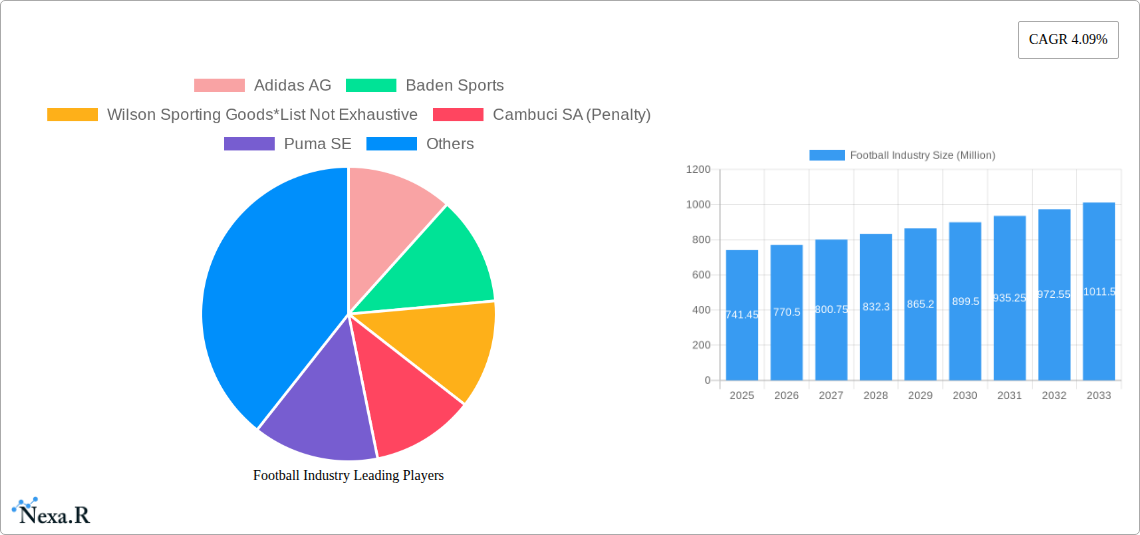

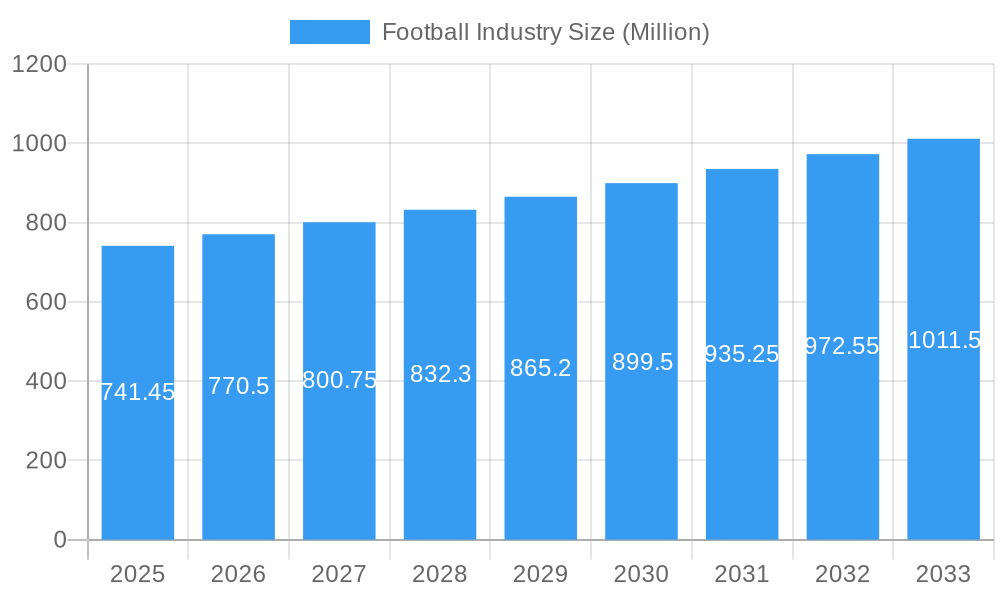

The global Football Industry is poised for robust growth, projected to reach a substantial USD 741.45 million by 2025, exhibiting a Compound Annual Growth Rate (CAGR) of 4.09% throughout the forecast period of 2025-2033. This expansion is fueled by a confluence of dynamic factors, including the ever-increasing global popularity of football as a spectator and participation sport, significant investments in infrastructure development and professional leagues worldwide, and the growing influence of digital media and e-commerce in expanding market reach. Key drivers include a rising youth population actively engaged in the sport, enhanced marketing and sponsorship opportunities, and the continuous innovation in sports equipment and apparel. The increasing professionalization of leagues and the surge in international tournaments like the FIFA World Cup and continental championships are also playing a pivotal role in driving market expansion and consumer engagement.

Football Industry Market Size (In Million)

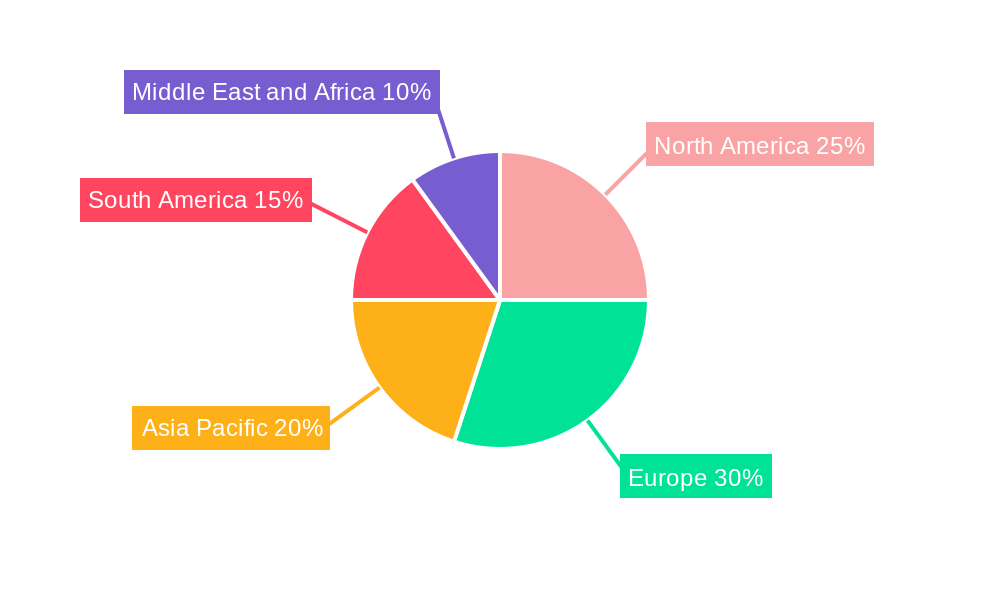

The market's growth trajectory will be further shaped by emerging trends such as the rise of fan engagement technologies, including virtual reality and augmented reality experiences, and a growing emphasis on sustainability within the sports industry, from manufacturing to event management. However, certain restraints, such as economic downturns affecting consumer disposable income and intense competition among established and emerging players, could present challenges. The market segments are diverse, spanning various product sizes and distribution channels, with specialty stores, supermarkets, hypermarkets, and online platforms all contributing to market accessibility. Geographically, North America and Europe are expected to remain significant markets, while the Asia Pacific region, particularly China and India, presents substantial untapped growth potential due to a burgeoning interest in football and a growing middle class.

Football Industry Company Market Share

Here is a comprehensive, SEO-optimized report description for the Football Industry, designed for maximum visibility and engagement:

Football Industry Market Analysis: Size, Growth, Trends, and Forecast (2019–2033)

Gain unparalleled insights into the global football industry with this definitive market research report. Spanning the historical period of 2019–2024, the base and estimated year of 2025, and a robust forecast period of 2025–2033, this report offers a granular view of market dynamics, growth trajectories, and key strategic opportunities. It meticulously analyzes the parent football market and its child segments, providing actionable intelligence for manufacturers, distributors, sports organizations, and investors. Discover current market size, projected growth rates (CAGR), and critical trends impacting this dynamic sector.

Football Industry Market Dynamics & Structure

The global football industry is characterized by a moderately concentrated market, with key players like Nike Inc. and Adidas AG holding significant shares. Technological innovation, particularly in material science and aerodynamic design for footballs, acts as a primary driver, enhancing player performance and fan engagement. Regulatory frameworks established by FIFA and continental confederations play a crucial role in standardizing equipment and competition. Competitive product substitutes, while limited in the core football market, can emerge from alternative sports or training equipment. End-user demographics are increasingly diverse, driven by the sport's global popularity and grassroots participation. Mergers and acquisitions (M&A) activity, while not as frequent as in other industries, occurs strategically to consolidate market positions or acquire innovative technologies.

- Market Concentration: Dominated by a few major sportswear giants, but with significant opportunities for niche players.

- Technological Drivers: Aerodynamic ball design, durable and sustainable materials, smart ball technology.

- Regulatory Frameworks: FIFA, UEFA, CONMEBOL, etc., dictate ball specifications and safety standards.

- Competitive Landscape: Intense competition focused on product innovation, branding, and athlete endorsements.

- End-User Demographics: Wide appeal across professional athletes, amateur players, youth leagues, and casual enthusiasts.

- M&A Trends: Strategic acquisitions to expand product portfolios or gain access to advanced manufacturing capabilities.

Football Industry Growth Trends & Insights

The global football market is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 6.5% over the forecast period. This expansion is fueled by increasing participation rates worldwide, driven by growing disposable incomes in emerging economies and widespread grassroots development initiatives. The adoption rate of premium footballs, incorporating advanced technologies for enhanced performance and durability, is steadily rising. Technological disruptions, such as the integration of smart sensors for performance tracking and analysis, are beginning to redefine the product landscape. Consumer behavior shifts are evident, with a greater emphasis on sustainability in manufacturing, personalized products, and online purchasing channels. The rising popularity of professional football leagues and tournaments globally continues to act as a significant market penetrator, influencing demand for official match balls and replica products.

- Market Size Evolution: Projected to reach a market value exceeding $15,000 million by 2033.

- Adoption Rates: Increasing demand for technologically advanced and high-performance footballs.

- Technological Disruptions: Integration of smart technology, data analytics in ball design.

- Consumer Behavior Shifts: Growing preference for sustainable materials, online retail, and authentic merchandise.

- Market Penetration: Driven by global sporting events and the increasing popularity of organized football at all levels.

Dominant Regions, Countries, or Segments in Football Industry

Europe stands as the dominant region in the global football industry, accounting for over 40% of the total market share. This dominance is attributed to the established infrastructure of professional leagues, high disposable incomes, and a deep-rooted cultural affinity for the sport. The Size 5 football segment, representing the standard match ball size for adults, consistently drives market growth, with an estimated market share of over 70%. Within distribution channels, Online Stores are rapidly gaining prominence, projected to capture a significant portion of sales by 2030, driven by convenience and wider product availability. However, Specialty Stores retain a strong hold, particularly for professional-grade equipment, offering expert advice and a curated selection.

- Leading Region: Europe, driven by strong professional leagues and widespread participation.

- Dominant Country: Germany, the United Kingdom, and Spain are key markets within Europe.

- Key Segment (Size): Size 5 footballs, catering to the adult professional and amateur player base.

- Growth Driver (Distribution Channel): Rapid expansion of Online Stores due to e-commerce growth and consumer convenience.

- Market Share (Size 5): Exceeding 70% of the global football market.

- Dominance Factors: Economic policies supporting sports infrastructure, strong fan engagement, and extensive retail networks.

Football Industry Product Landscape

The product landscape in the football industry is defined by continuous innovation, with a focus on enhancing performance, durability, and player comfort. Key product advancements include the development of aerodynamic panel designs that ensure a truer flight path, such as Nike's Aerowsculpt technology. Innovations in material science have led to the creation of lighter yet more robust footballs, capable of withstanding diverse playing conditions. The application of these technologies ranges from official match balls used in top-tier professional leagues to training equipment designed for skill development. Performance metrics are increasingly scrutinized, with manufacturers aiming for consistent bounce, optimal weight distribution, and superior water resistance.

Key Drivers, Barriers & Challenges in Football Industry

Key Drivers: The primary forces propelling the football industry include the immense global popularity of the sport, leading to consistent demand from professional leagues to grassroots players. Technological advancements in ball manufacturing, offering improved aerodynamics and durability, are significant drivers. The growing influence of social media and digital marketing campaigns effectively reaches wider consumer bases. Economic growth in emerging markets also fuels increased participation and spending on football-related products.

Barriers & Challenges: Supply chain disruptions, particularly for specialized materials, can pose significant challenges. Intense competition among major brands and the cost of developing and marketing new technologies present competitive pressures. Regulatory hurdles, such as adherence to FIFA's stringent ball specifications, require substantial investment in research and development. Furthermore, fluctuating raw material prices can impact manufacturing costs and profit margins.

Emerging Opportunities in Football Industry

Emerging opportunities lie in the burgeoning demand for sustainable and eco-friendly footballs, utilizing recycled materials and ethical manufacturing processes. The integration of smart technology in footballs, offering real-time performance data for players and coaches, presents a significant untapped market. Expansion into developing regions with rapidly growing football fan bases and increasing disposable incomes offers substantial growth potential. Furthermore, the development of specialized footballs catering to niche training needs or adaptive sports presents unique product development avenues.

Growth Accelerators in the Football Industry Industry

Long-term growth in the football industry will be significantly accelerated by continued technological breakthroughs in material science and ball design, enhancing player performance and game experience. Strategic partnerships between sportswear manufacturers, football federations, and leagues will further drive market penetration and brand visibility. The expanding e-commerce landscape and direct-to-consumer (DTC) models will allow for more efficient market reach and personalized product offerings. Moreover, increased investment in grassroots football development programs globally will foster a larger base of future consumers.

Key Players Shaping the Football Industry Market

- Adidas AG

- Baden Sports

- Wilson Sporting Goods

- Cambuci SA (Penalty)

- Puma SE

- Decathlon Sports Pvt Ltd

- Mitre International

- Umbro

- Nike Inc

- Select Sport AS

Notable Milestones in Football Industry Sector

- October 2022: Nike launched a new High Visibility Premier League ball for the 2022-23 season, featuring enhanced visibility and Aerowsculpt technology for winter conditions.

- June 2022: PUMA and Lega Serie partnered to launch a new match ball, marking the beginning of their collaboration.

- April 2021: LFP and Decathlon announced that Kipsta would become the official ball supplier for French soccer's two highest divisions.

In-Depth Football Industry Market Outlook

The future of the football industry is exceptionally promising, with continued growth fueled by innovation and global expansion. Key accelerators include the ongoing digital transformation of retail, enabling wider accessibility and personalized consumer experiences. Investments in grassroots development, particularly in Asia and Africa, are set to unlock significant new markets and consumer bases. The increasing focus on sports science and data analytics will drive demand for technologically advanced equipment, creating opportunities for companies that can integrate smart features into their products. Overall, the market outlook is characterized by sustained demand, driven by the enduring passion for the sport and the continuous pursuit of enhanced performance.

Football Industry Segmentation

-

1. Size

- 1.1. Size 1

- 1.2. Size 2

- 1.3. Size 3

- 1.4. Size 4

- 1.5. Size 5

-

2. Distribution Channel

- 2.1. Specialty Stores

- 2.2. Supermarkets and Hypermarkets

- 2.3. Online Stores

- 2.4. Other Distribution Channels

Football Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Spain

- 2.5. Italy

- 2.6. Russia

- 2.7. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. South Africa

- 5.2. Saudi Arabia

- 5.3. Rest of Middle East and Africa

Football Industry Regional Market Share

Geographic Coverage of Football Industry

Football Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.09% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Size

- 5.1.1. Size 1

- 5.1.2. Size 2

- 5.1.3. Size 3

- 5.1.4. Size 4

- 5.1.5. Size 5

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Specialty Stores

- 5.2.2. Supermarkets and Hypermarkets

- 5.2.3. Online Stores

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Size

- 6. Global Football Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Size

- 6.1.1. Size 1

- 6.1.2. Size 2

- 6.1.3. Size 3

- 6.1.4. Size 4

- 6.1.5. Size 5

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Specialty Stores

- 6.2.2. Supermarkets and Hypermarkets

- 6.2.3. Online Stores

- 6.2.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Size

- 7. North America Football Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Size

- 7.1.1. Size 1

- 7.1.2. Size 2

- 7.1.3. Size 3

- 7.1.4. Size 4

- 7.1.5. Size 5

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Specialty Stores

- 7.2.2. Supermarkets and Hypermarkets

- 7.2.3. Online Stores

- 7.2.4. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Size

- 8. Europe Football Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Size

- 8.1.1. Size 1

- 8.1.2. Size 2

- 8.1.3. Size 3

- 8.1.4. Size 4

- 8.1.5. Size 5

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Specialty Stores

- 8.2.2. Supermarkets and Hypermarkets

- 8.2.3. Online Stores

- 8.2.4. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Size

- 9. Asia Pacific Football Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Size

- 9.1.1. Size 1

- 9.1.2. Size 2

- 9.1.3. Size 3

- 9.1.4. Size 4

- 9.1.5. Size 5

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Specialty Stores

- 9.2.2. Supermarkets and Hypermarkets

- 9.2.3. Online Stores

- 9.2.4. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Size

- 10. South America Football Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Size

- 10.1.1. Size 1

- 10.1.2. Size 2

- 10.1.3. Size 3

- 10.1.4. Size 4

- 10.1.5. Size 5

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Specialty Stores

- 10.2.2. Supermarkets and Hypermarkets

- 10.2.3. Online Stores

- 10.2.4. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Size

- 11. Middle East and Africa Football Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Size

- 11.1.1. Size 1

- 11.1.2. Size 2

- 11.1.3. Size 3

- 11.1.4. Size 4

- 11.1.5. Size 5

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Specialty Stores

- 11.2.2. Supermarkets and Hypermarkets

- 11.2.3. Online Stores

- 11.2.4. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Size

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Adidas AG

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Baden Sports

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Wilson Sporting Goods*List Not Exhaustive

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Cambuci SA (Penalty)

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Puma SE

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Decathlon Sports Pvt Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Mitre International

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Umbro

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Nike Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Select Sport AS

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Adidas AG

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Football Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Football Industry Revenue (Million), by Size 2025 & 2033

- Figure 3: North America Football Industry Revenue Share (%), by Size 2025 & 2033

- Figure 4: North America Football Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 5: North America Football Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 6: North America Football Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Football Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Football Industry Revenue (Million), by Size 2025 & 2033

- Figure 9: Europe Football Industry Revenue Share (%), by Size 2025 & 2033

- Figure 10: Europe Football Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 11: Europe Football Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 12: Europe Football Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Football Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Football Industry Revenue (Million), by Size 2025 & 2033

- Figure 15: Asia Pacific Football Industry Revenue Share (%), by Size 2025 & 2033

- Figure 16: Asia Pacific Football Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 17: Asia Pacific Football Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 18: Asia Pacific Football Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Football Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Football Industry Revenue (Million), by Size 2025 & 2033

- Figure 21: South America Football Industry Revenue Share (%), by Size 2025 & 2033

- Figure 22: South America Football Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 23: South America Football Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 24: South America Football Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: South America Football Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Football Industry Revenue (Million), by Size 2025 & 2033

- Figure 27: Middle East and Africa Football Industry Revenue Share (%), by Size 2025 & 2033

- Figure 28: Middle East and Africa Football Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 29: Middle East and Africa Football Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 30: Middle East and Africa Football Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Football Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Football Industry Revenue Million Forecast, by Size 2020 & 2033

- Table 2: Global Football Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 3: Global Football Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Football Industry Revenue Million Forecast, by Size 2020 & 2033

- Table 5: Global Football Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Global Football Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Rest of North America Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Global Football Industry Revenue Million Forecast, by Size 2020 & 2033

- Table 12: Global Football Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 13: Global Football Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 14: Germany Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: United Kingdom Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: France Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Spain Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Italy Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Russia Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Global Football Industry Revenue Million Forecast, by Size 2020 & 2033

- Table 22: Global Football Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 23: Global Football Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: China Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Japan Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: India Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Australia Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Rest of Asia Pacific Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Global Football Industry Revenue Million Forecast, by Size 2020 & 2033

- Table 30: Global Football Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 31: Global Football Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 32: Brazil Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Argentina Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Rest of South America Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Global Football Industry Revenue Million Forecast, by Size 2020 & 2033

- Table 36: Global Football Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 37: Global Football Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 38: South Africa Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Saudi Arabia Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Rest of Middle East and Africa Football Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Football Industry?

The projected CAGR is approximately 4.09%.

2. Which companies are prominent players in the Football Industry?

Key companies in the market include Adidas AG, Baden Sports, Wilson Sporting Goods*List Not Exhaustive, Cambuci SA (Penalty), Puma SE, Decathlon Sports Pvt Ltd, Mitre International, Umbro, Nike Inc, Select Sport AS.

3. What are the main segments of the Football Industry?

The market segments include Size, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 741.45 Million as of 2022.

5. What are some drivers contributing to market growth?

The Rise of Athleisure; Influence of Social Media.

6. What are the notable trends driving market growth?

Rising Active Participation in Football Leagues.

7. Are there any restraints impacting market growth?

Presence of Counterfeit Products.

8. Can you provide examples of recent developments in the market?

In October 2022, Nike launched a new High Visibility Premier League ball for the season 2022-23. The new winter ball provides increased visibility with the same Aerowsculpt technology as the regular Premier League 2022-23 ball.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Football Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Football Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Football Industry?

To stay informed about further developments, trends, and reports in the Football Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence