Key Insights

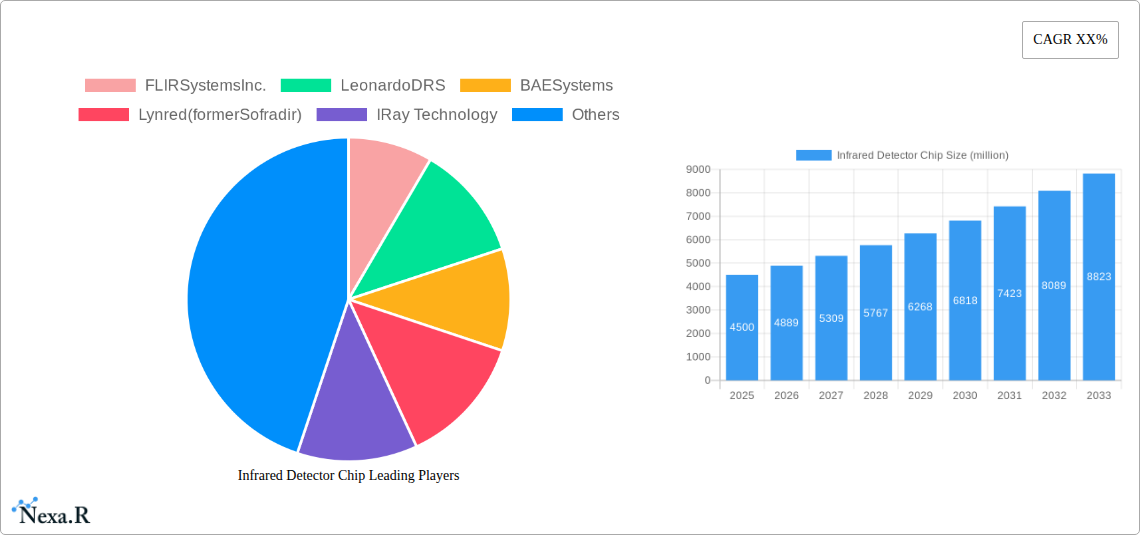

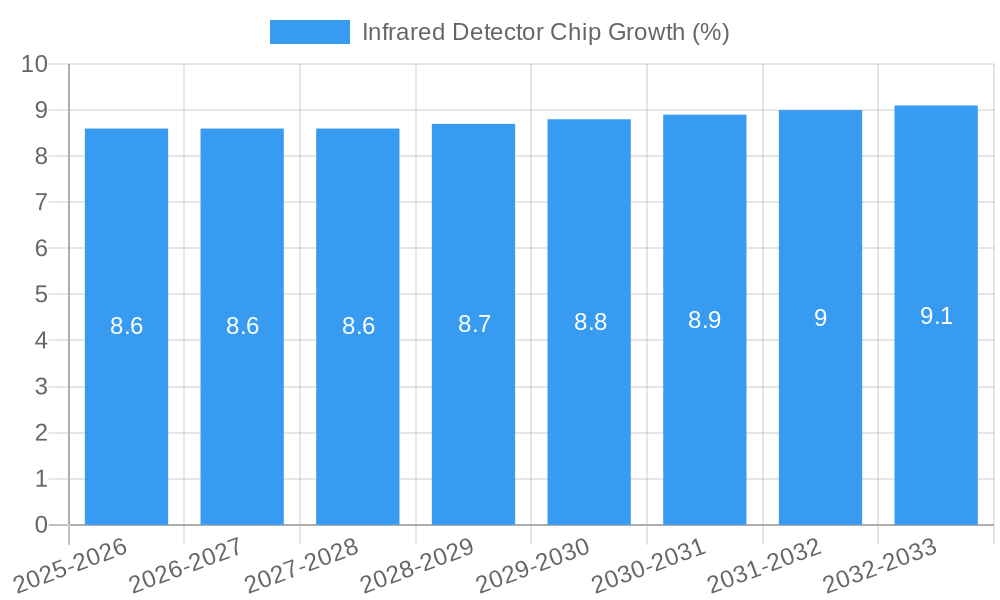

The global Infrared Detector Chip market is projected to reach a substantial valuation of approximately $4,500 million by 2025, driven by an estimated Compound Annual Growth Rate (CAGR) of around 8.5% throughout the forecast period. This robust expansion is underpinned by the escalating demand for advanced thermal imaging solutions across a multitude of critical sectors. Key growth drivers include the increasing adoption of infrared detector chips in public safety for surveillance and border protection, the burgeoning use in medical diagnostics for non-invasive patient monitoring and early disease detection, and the critical role they play in enhancing safety and operational efficiency within the transportation and aerospace industries, particularly in autonomous driving and aircraft systems. Furthermore, the defense sector continues to be a significant consumer, investing in advanced infrared technologies for target acquisition and situational awareness. The market's trajectory is further propelled by continuous technological advancements, leading to more sensitive, compact, and cost-effective infrared detector chip solutions, which are expanding their application scope and accessibility.

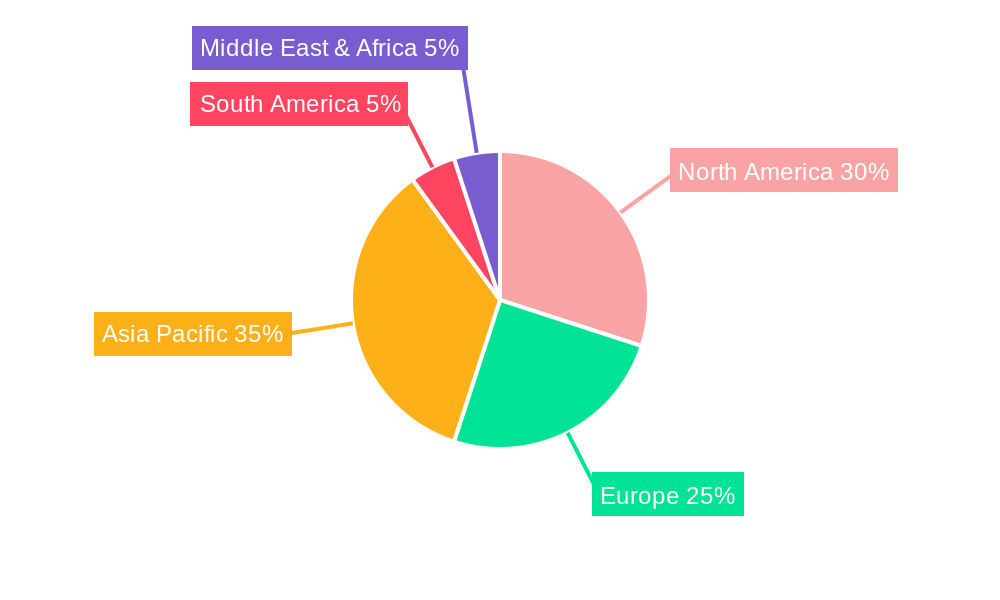

The market is segmented by type into Refrigeration Type and Uncooled infrared detector chips, with the Uncooled segment experiencing more rapid adoption due to its lower cost and portability, making it ideal for a wider range of commercial and consumer applications. Geographically, the Asia Pacific region, particularly China, is anticipated to emerge as a dominant force, owing to its substantial manufacturing capabilities and growing end-user industries. North America and Europe also represent mature yet significant markets, driven by innovation and stringent safety regulations. However, the market faces certain restraints, including the high initial cost of some advanced infrared technologies and the complex manufacturing processes involved, which can limit widespread adoption in price-sensitive applications. Despite these challenges, the inherent benefits of infrared detection, such as its ability to operate in complete darkness and through obscurants, coupled with ongoing research and development initiatives, are expected to propel sustained market growth and innovation in the coming years, with companies like FLIR Systems, Leonardo DRS, and BAE Systems at the forefront of this evolution.

Infrared Detector Chip Market Research Report

This comprehensive report provides an in-depth analysis of the global Infrared Detector Chip market, offering critical insights into market dynamics, growth trends, regional dominance, product landscape, key drivers, challenges, opportunities, and a detailed outlook on the future. The report covers the study period from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033, leveraging historical data from 2019-2024.

Infrared Detector Chip Market Dynamics & Structure

The global Infrared Detector Chip market is characterized by a moderately concentrated landscape, with key players like FLIR Systems Inc., Leonardo DRS, BAE Systems, Lynred (former Sofradir), IRay Technology, Zhejiang Dali Technology, L3Harris Technologies, Inc., SemiConductor Devices (SCD), Wuhan Guide Infrared, GWIC, Hamamatsu Photonics, New Infrared Technologies (NIT), and Soreq Nuclear Research Center (SNRC) dominating significant market shares. Technological innovation serves as a primary growth driver, with continuous advancements in uncooled detector technology and miniaturization pushing the boundaries of performance and affordability. Regulatory frameworks, particularly concerning defense and public safety applications, also play a crucial role in shaping market demand. Competitive product substitutes, such as advanced thermal imaging cameras and other sensing technologies, present a dynamic competitive environment. End-user demographics are diverse, spanning industrial, commercial, and governmental sectors, each with unique application needs. Mergers and acquisitions (M&A) trends, while not at an extremely high volume, indicate strategic consolidation and expansion efforts by established players to enhance their product portfolios and market reach. For instance, anticipated M&A activity in the next 5 years is estimated at approximately 2-3 significant deals, impacting market share by 5-8% collectively. Innovation barriers are primarily associated with high R&D costs and the complexity of semiconductor manufacturing processes.

- Market Concentration: Moderately concentrated with key players holding substantial market shares.

- Technological Innovation Drivers: Advancements in uncooled technology, miniaturization, and improved resolution.

- Regulatory Frameworks: Stringent regulations in defense and public safety influencing product development and adoption.

- Competitive Product Substitutes: Advanced thermal imaging systems, other non-infrared sensing technologies.

- End-User Demographics: Diverse, including industrial maintenance, medical diagnostics, homeland security, automotive safety, and defense systems.

- M&A Trends: Strategic consolidation for portfolio expansion and market share enhancement, with an estimated 2-3 major deals annually anticipated.

- Innovation Barriers: High R&D expenditure, complex fabrication processes, and stringent qualification requirements.

Infrared Detector Chip Growth Trends & Insights

The global Infrared Detector Chip market is poised for robust growth, driven by an increasing demand for advanced sensing capabilities across a multitude of industries. The market size is projected to expand significantly, with an estimated market value of USD 2,500 million in the base year of 2025, and anticipated to reach USD 4,800 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 8.5% during the forecast period. Adoption rates of infrared detector chips are escalating, fueled by the growing awareness of their capabilities in non-contact temperature measurement, surveillance, and diagnostics. Technological disruptions, such as the development of higher resolution, more sensitive, and lower-cost uncooled infrared detector chips, are democratizing access to this technology. Consumer behavior shifts are also contributing to market expansion, with a growing preference for enhanced safety features in transportation, more precise medical diagnostic tools, and more efficient industrial monitoring systems. The penetration of infrared detector chips in consumer electronics, though still nascent, is expected to witness a substantial surge, indicating a broader market acceptance and integration. Furthermore, the evolving landscape of smart cities and the Internet of Things (IoT) is creating new avenues for infrared sensing applications, contributing to sustained market penetration. The increasing emphasis on predictive maintenance in industrial sectors, where early detection of anomalies through thermal imaging is crucial, will further propel market growth. In the defense sector, the continuous need for advanced surveillance and targeting systems will remain a significant growth pillar. The medical sector's adoption of infrared imaging for non-invasive diagnostics and patient monitoring is also expected to rise.

Dominant Regions, Countries, or Segments in Infrared Detector Chip

The global Infrared Detector Chip market exhibits significant dominance and growth potential across various regions and application segments. North America, particularly the United States, is a leading region in the market, primarily driven by robust demand from its advanced defense and aerospace industries, coupled with significant investments in public safety and industrial automation. The presence of major defense contractors and a strong emphasis on technological innovation contribute to its leading position.

In terms of applications, the Defense segment stands out as a primary growth engine. The escalating geopolitical tensions and the increasing need for sophisticated surveillance, targeting, and reconnaissance systems worldwide fuel the demand for high-performance infrared detector chips. Governments across the globe are investing heavily in advanced military technologies, where infrared detection plays a pivotal role in enhancing operational capabilities in all weather and light conditions. The market size for infrared detector chips in the defense application is estimated to be around USD 750 million in 2025.

Key drivers for this dominance include:

- Technological Advancement: Continuous innovation in detector performance, resolution, and spectral sensitivity tailored for military applications.

- Government Procurement: Substantial defense budgets allocated for advanced sensor technologies.

- National Security Imperatives: The ongoing need for enhanced border security, threat detection, and intelligence gathering.

- Strategic Partnerships: Collaborations between defense manufacturers and detector chip developers to create bespoke solutions.

Within the Types of infrared detector chips, Uncooled detectors are experiencing a surge in demand and market share, projected to account for approximately 75% of the total market revenue by 2025. Their cost-effectiveness, reduced size, and lower power consumption compared to their cooled counterparts make them increasingly attractive for a wider range of commercial and industrial applications, thereby driving significant growth. The market size for uncooled infrared detector chips is estimated to be USD 1,875 million in 2025.

The Electricity segment also presents a substantial market, driven by the need for predictive maintenance of electrical infrastructure, thermal management in industrial processes, and energy efficiency monitoring. The market size for infrared detector chips in the electricity application is estimated at USD 350 million in 2025.

- Electricity: Predictive maintenance, thermal imaging for fault detection, energy audits.

- Medical Treatment: Non-invasive diagnostics, fever screening, patient monitoring.

- Public Safety: Surveillance, border security, fire detection, search and rescue.

- Transportation: Advanced driver-assistance systems (ADAS), autonomous driving, night vision.

- Defense: Target acquisition, surveillance, missile guidance, thermal sights.

- Aerospace: Satellite imaging, thermal management, navigation systems.

- Others: Industrial automation, environmental monitoring, scientific research.

The Asia Pacific region, particularly China, is also emerging as a significant market for infrared detector chips, driven by rapid industrialization, increasing defense spending, and a growing adoption of thermal imaging in various sectors. The market size for infrared detector chips in the Asia Pacific region is projected to grow at a CAGR of over 9.0% during the forecast period.

Infrared Detector Chip Product Landscape

The infrared detector chip product landscape is characterized by rapid innovation, leading to enhanced performance, miniaturization, and cost-effectiveness. Advancements are primarily focused on improving sensitivity, resolution, and spectral response across a wide range of infrared wavelengths. Product innovations include higher pixel count uncooled microbolometer arrays, more efficient cooled detector technologies for specialized applications, and hybrid detector architectures offering unique capabilities. Unique selling propositions revolve around reduced noise equivalent temperature difference (NETD), faster response times, broader operating temperature ranges, and integrated signal processing for ease of implementation. Technological advancements are enabling the development of smaller, lighter, and more power-efficient infrared detector chips, paving the way for their integration into a wider array of devices, from handheld inspection tools to advanced automotive sensors and wearable medical devices.

Key Drivers, Barriers & Challenges in Infrared Detector Chip

The infrared detector chip market is propelled by several key drivers. Technological advancements in uncooled detector technology, leading to improved performance and reduced costs, are a primary catalyst. The growing demand for thermal imaging in industrial automation, predictive maintenance, and safety applications significantly boosts market growth. Furthermore, the increasing adoption of infrared sensors in defense and aerospace for surveillance and targeting purposes provides a substantial growth avenue. The expanding use of infrared technology in medical diagnostics and public safety applications, such as fever detection and security surveillance, also contributes to market expansion.

However, the market faces several barriers and challenges. High research and development costs associated with creating cutting-edge infrared detector chip technology can limit the entry of new players and slow down innovation cycles. Stringent regulatory requirements, particularly in defense and sensitive commercial applications, necessitate extensive testing and validation, increasing product development timelines and costs. Supply chain complexities and the reliance on specialized raw materials can also pose challenges, especially during periods of global disruption. Intense competition among established players and emerging manufacturers can lead to price pressures, impacting profit margins.

Emerging Opportunities in Infrared Detector Chip

Emerging opportunities in the infrared detector chip sector lie in the expansion of their application in the consumer electronics market, including smartphones for thermal imaging capabilities and smart home devices for environmental monitoring. The burgeoning field of autonomous vehicles presents a significant opportunity, with infrared sensors crucial for enhanced perception and safety in adverse weather conditions and low-light environments. The development of next-generation medical devices for non-invasive diagnostics, personalized healthcare, and early disease detection offers a promising avenue for growth. Furthermore, the increasing focus on environmental monitoring and industrial IoT is creating demand for more compact, low-power, and cost-effective infrared detector chips for a wide range of sensing applications.

Growth Accelerators in the Infrared Detector Chip Industry

Several factors are accelerating growth in the Infrared Detector Chip industry. Continuous innovation in uncooled bolometer technology is driving down costs and improving performance, making infrared detection more accessible for a broader range of applications. Strategic partnerships between chip manufacturers and end-product developers are fostering the creation of highly integrated and application-specific solutions. The increasing global emphasis on industrial automation and predictive maintenance is a significant growth accelerator, as companies seek to improve efficiency and reduce downtime through thermal monitoring. Furthermore, government initiatives and funding for defense modernization and public safety infrastructure are creating sustained demand for advanced infrared sensing capabilities. The expanding market for advanced driver-assistance systems (ADAS) and the development of autonomous driving technologies are also acting as powerful growth accelerators.

Key Players Shaping the Infrared Detector Chip Market

- FLIR Systems Inc.

- Leonardo DRS

- BAE Systems

- Lynred (former Sofradir)

- IRay Technology

- Zhejiang Dali Technology

- L3Harris Technologies, Inc.

- SemiConductor Devices (SCD)

- Wuhan Guide Infrared

- GWIC

- Hamamatsu Photonics

- New Infrared Technologies (NIT)

- Soreq Nuclear Research Center (SNRC)

Notable Milestones in Infrared Detector Chip Sector

- 2019: Lynred's acquisition of ULIS, consolidating its position in uncooled infrared detector technology.

- 2020: FLIR Systems Inc. announces the development of a new generation of high-performance, uncooled thermal cameras, expanding their product portfolio.

- 2021: IRay Technology launches a series of high-resolution infrared detector chips, enhancing imaging capabilities for various applications.

- 2022: BAE Systems secures significant contracts for infrared sensors for defense applications, highlighting continued demand in the defense sector.

- 2023: Hamamatsu Photonics introduces advanced photodiodes with improved spectral response for specialized infrared detection.

- 2024: New Infrared Technologies (NIT) patents a novel approach to improve the detectivity of infrared detector chips, potentially leading to significant performance gains.

In-Depth Infrared Detector Chip Market Outlook

The future outlook for the Infrared Detector Chip market is exceptionally promising, driven by persistent technological innovation and the expanding scope of applications. Growth accelerators such as advancements in artificial intelligence and machine learning, which increasingly leverage thermal data for enhanced analysis and decision-making, will further propel adoption. Strategic collaborations between sensor manufacturers and leading technology companies are anticipated to unlock novel use cases in areas like smart agriculture and building management. The market is poised for sustained expansion as infrared detector chips become more integrated into everyday devices, contributing to enhanced safety, efficiency, and well-being across various sectors. The increasing demand for non-contact measurement solutions and the continuous evolution of miniaturized and cost-effective infrared sensing technologies will solidify the market's upward trajectory.

Infrared Detector Chip Segmentation

-

1. Application

- 1.1. Electricity

- 1.2. Medical Treatment

- 1.3. Public Safety

- 1.4. Transportation

- 1.5. Defense

- 1.6. Aerospace

- 1.7. Others

-

2. Types

- 2.1. Refrigeration Type

- 2.2. Uncooled

Infrared Detector Chip Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Infrared Detector Chip REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Infrared Detector Chip Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Electricity

- 5.1.2. Medical Treatment

- 5.1.3. Public Safety

- 5.1.4. Transportation

- 5.1.5. Defense

- 5.1.6. Aerospace

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Refrigeration Type

- 5.2.2. Uncooled

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Infrared Detector Chip Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Electricity

- 6.1.2. Medical Treatment

- 6.1.3. Public Safety

- 6.1.4. Transportation

- 6.1.5. Defense

- 6.1.6. Aerospace

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Refrigeration Type

- 6.2.2. Uncooled

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Infrared Detector Chip Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Electricity

- 7.1.2. Medical Treatment

- 7.1.3. Public Safety

- 7.1.4. Transportation

- 7.1.5. Defense

- 7.1.6. Aerospace

- 7.1.7. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Refrigeration Type

- 7.2.2. Uncooled

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Infrared Detector Chip Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Electricity

- 8.1.2. Medical Treatment

- 8.1.3. Public Safety

- 8.1.4. Transportation

- 8.1.5. Defense

- 8.1.6. Aerospace

- 8.1.7. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Refrigeration Type

- 8.2.2. Uncooled

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Infrared Detector Chip Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Electricity

- 9.1.2. Medical Treatment

- 9.1.3. Public Safety

- 9.1.4. Transportation

- 9.1.5. Defense

- 9.1.6. Aerospace

- 9.1.7. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Refrigeration Type

- 9.2.2. Uncooled

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Infrared Detector Chip Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Electricity

- 10.1.2. Medical Treatment

- 10.1.3. Public Safety

- 10.1.4. Transportation

- 10.1.5. Defense

- 10.1.6. Aerospace

- 10.1.7. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Refrigeration Type

- 10.2.2. Uncooled

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 FLIRSystemsInc.

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 LeonardoDRS

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 BAESystems

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Lynred(formerSofradir)

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 IRay Technology

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Zhejiang Dali Technology

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 L3HarrisTechnologies,Inc.

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 SemiConductorDevices(SCD)

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Wuhan Guide Infrared

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 GWIC

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 HamamatsuPhotonics

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 SoreqNuclearResearchCenter(SNRC)

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 NewInfraredTechnologies(NIT)

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 FLIRSystemsInc.

List of Figures

- Figure 1: Global Infrared Detector Chip Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Infrared Detector Chip Revenue (million), by Application 2024 & 2032

- Figure 3: North America Infrared Detector Chip Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Infrared Detector Chip Revenue (million), by Types 2024 & 2032

- Figure 5: North America Infrared Detector Chip Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Infrared Detector Chip Revenue (million), by Country 2024 & 2032

- Figure 7: North America Infrared Detector Chip Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Infrared Detector Chip Revenue (million), by Application 2024 & 2032

- Figure 9: South America Infrared Detector Chip Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Infrared Detector Chip Revenue (million), by Types 2024 & 2032

- Figure 11: South America Infrared Detector Chip Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Infrared Detector Chip Revenue (million), by Country 2024 & 2032

- Figure 13: South America Infrared Detector Chip Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Infrared Detector Chip Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Infrared Detector Chip Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Infrared Detector Chip Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Infrared Detector Chip Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Infrared Detector Chip Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Infrared Detector Chip Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Infrared Detector Chip Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Infrared Detector Chip Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Infrared Detector Chip Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Infrared Detector Chip Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Infrared Detector Chip Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Infrared Detector Chip Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Infrared Detector Chip Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Infrared Detector Chip Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Infrared Detector Chip Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Infrared Detector Chip Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Infrared Detector Chip Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Infrared Detector Chip Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Infrared Detector Chip Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Infrared Detector Chip Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Infrared Detector Chip Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Infrared Detector Chip Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Infrared Detector Chip Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Infrared Detector Chip Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Infrared Detector Chip Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Infrared Detector Chip Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Infrared Detector Chip Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Infrared Detector Chip Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Infrared Detector Chip Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Infrared Detector Chip Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Infrared Detector Chip Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Infrared Detector Chip Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Infrared Detector Chip Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Infrared Detector Chip Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Infrared Detector Chip Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Infrared Detector Chip Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Infrared Detector Chip Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Infrared Detector Chip Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Infrared Detector Chip?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Infrared Detector Chip?

Key companies in the market include FLIRSystemsInc., LeonardoDRS, BAESystems, Lynred(formerSofradir), IRay Technology, Zhejiang Dali Technology, L3HarrisTechnologies,Inc., SemiConductorDevices(SCD), Wuhan Guide Infrared, GWIC, HamamatsuPhotonics, SoreqNuclearResearchCenter(SNRC), NewInfraredTechnologies(NIT).

3. What are the main segments of the Infrared Detector Chip?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Infrared Detector Chip," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Infrared Detector Chip report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Infrared Detector Chip?

To stay informed about further developments, trends, and reports in the Infrared Detector Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence