Key Insights

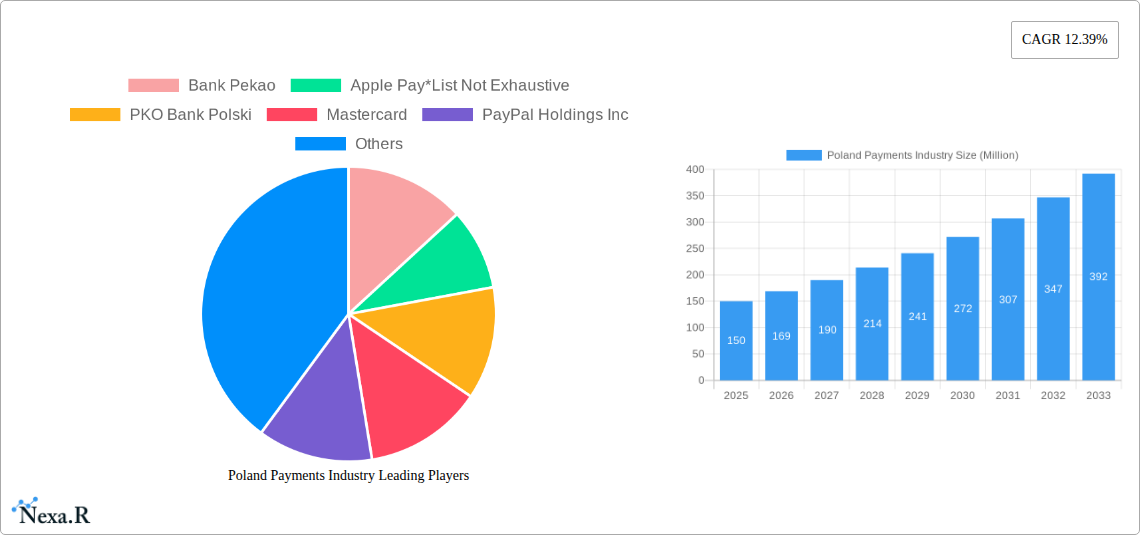

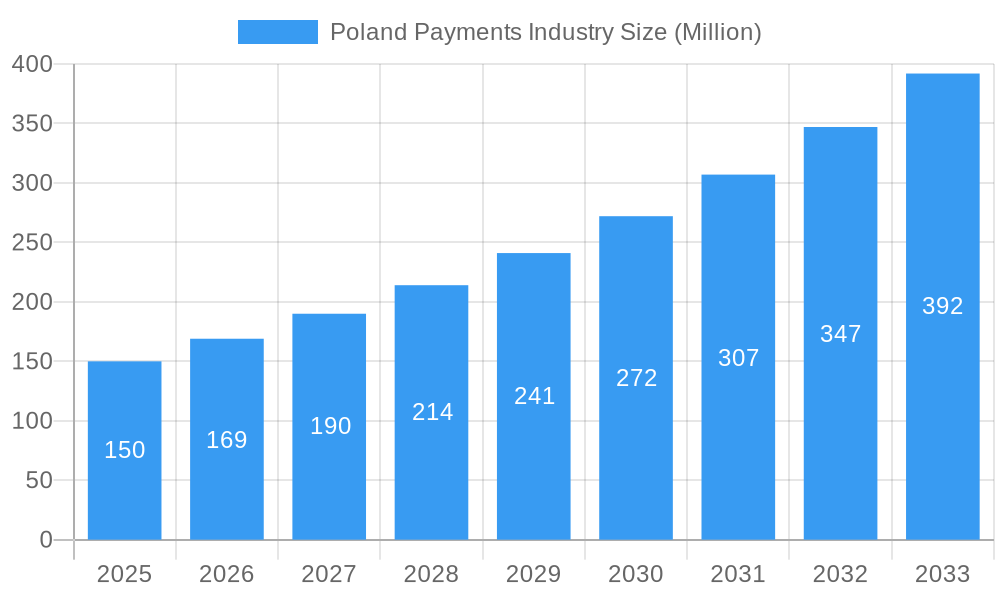

The Polish payments industry is experiencing robust growth, fueled by a burgeoning digital economy and increasing adoption of digital payment methods. The market, valued at approximately (estimated based on provided CAGR and assuming a 2025 value within a reasonable range for a country of Poland's size and economic development) 150 million USD in 2025, is projected to maintain a Compound Annual Growth Rate (CAGR) of 12.39% through 2033. This expansion is driven by several key factors. Firstly, rising smartphone penetration and improved internet infrastructure are facilitating the widespread adoption of mobile wallets and online payment platforms. Secondly, the Polish government's initiatives to promote digitalization and cashless transactions are further accelerating this shift. Thirdly, the increasing preference for contactless payment options, particularly among younger demographics, is bolstering the growth of card payments and digital wallets. Finally, the expansion of e-commerce and the growing popularity of online services across various sectors, including retail, entertainment, and healthcare, are creating a significant demand for secure and efficient payment solutions.

Poland Payments Industry Market Size (In Million)

However, the industry also faces certain challenges. While digital payments are gaining traction, cash remains a dominant payment method in Poland, particularly among older generations. Overcoming this inertia and encouraging wider adoption of digital payment solutions requires sustained efforts from both the public and private sectors. Furthermore, maintaining robust cybersecurity measures and addressing concerns related to data privacy are crucial for building consumer trust and ensuring the long-term sustainability of the industry. The competitive landscape is also dynamic, with both domestic and international players vying for market share. Key players like Bank Pekao, PKO Bank Polski, Mastercard, and PayPal are continuously innovating to enhance their offerings and cater to the evolving needs of Polish consumers and businesses. The segmentation of the market by payment mode (POS, online) and end-user industry highlights the diverse opportunities and challenges within this rapidly evolving sector.

Poland Payments Industry Company Market Share

This comprehensive report provides an in-depth analysis of the Poland payments industry, covering market dynamics, growth trends, key players, and future outlook. With a focus on the period 2019-2033 (Base Year: 2025, Forecast Period: 2025-2033), this report is essential for businesses, investors, and industry professionals seeking to understand and navigate this rapidly evolving market. The report segments the market by mode of payment (Point of Sale & Online Sale) and end-user industry, offering granular insights into various market segments. The market size is presented in Million units.

Keywords: Poland Payments Industry, Poland Payment Market, Digital Payments Poland, Cashless Payments Poland, Mobile Payments Poland, Online Payments Poland, Point of Sale Poland, Payment Processing Poland, Fintech Poland, Buy Now Pay Later Poland (BNPL), Payment Gateway Poland, Retail Payments Poland, Market Size Poland Payments, Poland Payments Market Growth, Payment Industry Trends Poland, PKO Bank Polski, Bank Pekao, Santander Bank Polska, Mastercard, Visa, PayPal, PayU, DotPay, Apple Pay

Poland Payments Industry Market Dynamics & Structure

The Polish payments landscape is characterized by a dynamic interplay of established players and emerging fintechs. Market concentration is moderate, with a few dominant banks alongside a thriving ecosystem of payment processors and digital wallet providers. Technological innovation, driven by increasing smartphone penetration and expanding internet access, is a key driver. The regulatory framework, while evolving, generally supports innovation. Consumers are increasingly adopting digital payment methods, presenting both opportunities and challenges for traditional players. M&A activity has been moderate, with larger players strategically acquiring smaller fintechs to expand their product offerings and capabilities.

- Market Concentration: Moderate, with several major banks and payment processors holding significant market share. xx% market share held by top 5 players in 2024.

- Technological Innovation: Rapid adoption of contactless payments, mobile wallets, and BNPL solutions.

- Regulatory Framework: Generally supportive of innovation, but subject to ongoing updates.

- Competitive Product Substitutes: Cash remains a significant competitor, though its usage is declining.

- End-User Demographics: Younger demographics are driving the adoption of digital payments.

- M&A Trends: Moderate activity, with strategic acquisitions by larger players to expand market reach. xx M&A deals in the last 5 years.

Poland Payments Industry Growth Trends & Insights

The Polish payments market has witnessed significant growth over the past few years, driven by rising digital adoption and favorable economic conditions. The market size is expected to show a steady CAGR of xx% during the forecast period (2025-2033), reaching xx million units by 2033. This growth is primarily fueled by the increasing penetration of digital payment methods, particularly mobile wallets and contactless payments, across various end-user industries. The shift from cash to digital payments is accelerating, with changing consumer behavior favoring convenience and security. Technological disruptions, such as the introduction of open banking and innovative payment solutions, further contribute to market expansion.

- Market Size Evolution: Steady growth from xx million units in 2019 to xx million units in 2024.

- Adoption Rates: Rapid increase in digital payment adoption, especially among younger demographics.

- Technological Disruptions: Open banking, BNPL, and mobile wallets are significantly impacting the market.

- Consumer Behavior Shifts: Preference for convenience, security, and seamless payment experiences.

Dominant Regions, Countries, or Segments in Poland Payments Industry

The largest segments within the Polish payments industry are driven by increasing urbanization, higher disposable incomes, and the rising prevalence of e-commerce. Major cities like Warsaw and Krakow show higher penetration of digital payment methods compared to rural areas. Within payment methods, card payments (both physical and contactless) and digital wallets are experiencing the most significant growth. The retail and e-commerce sectors are the largest end-user industries, closely followed by hospitality and entertainment.

- Dominant Mode of Payment: Card payments and digital wallets are witnessing robust growth at POS and Online.

- Dominant End-user Industry: Retail and e-commerce represent the largest share of transaction volume.

- Key Drivers: Growing smartphone penetration, increasing e-commerce adoption, and supportive government policies.

- Market Share and Growth Potential: Card payments hold the largest market share, followed by digital wallets. Growth potential is highest for digital wallets and BNPL solutions.

Poland Payments Industry Product Landscape

The Polish payments market is characterized by a diverse range of products, including traditional debit and credit cards, digital wallets (like Apple Pay, Google Pay), mobile payment apps, and online payment gateways. Recent innovations focus on improved security, enhanced user experience, and seamless integration with e-commerce platforms. The introduction of BNPL options has further expanded the product landscape. Key features include contactless payment capabilities, biometrics authentication, and loyalty programs integrated with payment systems.

Key Drivers, Barriers & Challenges in Poland Payments Industry

Key Drivers:

- Increasing smartphone and internet penetration.

- Growing e-commerce adoption.

- Government initiatives promoting cashless transactions.

- Innovation in payment technologies.

Key Challenges & Restraints:

- Security concerns related to digital payments.

- Infrastructure limitations in some regions.

- Regulatory complexities.

- Competition from traditional and new entrants. (e.g., xx% market share lost to new fintech entrants in 2024).

Emerging Opportunities in Poland Payments Industry

- Expansion of BNPL services.

- Growth in mobile payments.

- Increased adoption of open banking solutions.

- Development of innovative payment solutions tailored to specific industries (e.g., healthcare, hospitality).

Growth Accelerators in the Poland Payments Industry Industry

Technological advancements, strategic partnerships between banks and fintechs, and the increasing adoption of e-commerce are significant long-term growth accelerators. Government policies promoting digitalization and financial inclusion further enhance the positive outlook. The continuous improvement of payment infrastructure and cybersecurity measures will build consumer trust and drive wider adoption of digital payment solutions.

Key Players Shaping the Poland Payments Industry Market

- Bank Pekao

- Apple Pay

- PKO Bank Polski

- Mastercard

- PayPal Holdings Inc

- PayU

- Santander Bank Polska

- DotPay

- American Express

- Tap2Pay me

Notable Milestones in Poland Payments Industry Sector

- May 2022: Allegro launched a new card and smartphone payment option for cash-on-delivery orders via One Kurier.

- May 2022: PKO BP announced the completion of its BNPL solution, aiming for widespread online shop integration.

In-Depth Poland Payments Industry Market Outlook

The Polish payments market is poised for sustained growth, driven by ongoing technological advancements, increasing digital adoption, and supportive regulatory environments. Opportunities exist for businesses to leverage innovative payment solutions, targeting specific market segments and expanding into underserved regions. Strategic partnerships and investments in cybersecurity will be crucial for continued market expansion and building consumer trust. The long-term outlook remains positive, with significant potential for market expansion and further digitalization.

Poland Payments Industry Segmentation

-

1. Mode of Payment

-

1.1. Point of Sale

- 1.1.1. Card Pay

- 1.1.2. Digital Wallet (includes Mobile Wallets)

- 1.1.3. Cash

- 1.1.4. Others

-

1.2. Online Sale

- 1.2.1. Others (

-

1.1. Point of Sale

-

2. End-user Industry

- 2.1. Retail

- 2.2. Entertainment

- 2.3. Healthcare

- 2.4. Hospitality

- 2.5. Other End-user Industries

Poland Payments Industry Segmentation By Geography

- 1. Poland

Poland Payments Industry Regional Market Share

Geographic Coverage of Poland Payments Industry

Poland Payments Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 5.1.1. Point of Sale

- 5.1.1.1. Card Pay

- 5.1.1.2. Digital Wallet (includes Mobile Wallets)

- 5.1.1.3. Cash

- 5.1.1.4. Others

- 5.1.2. Online Sale

- 5.1.2.1. Others (

- 5.1.1. Point of Sale

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Retail

- 5.2.2. Entertainment

- 5.2.3. Healthcare

- 5.2.4. Hospitality

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Poland

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6. Poland Payments Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6.1.1. Point of Sale

- 6.1.1.1. Card Pay

- 6.1.1.2. Digital Wallet (includes Mobile Wallets)

- 6.1.1.3. Cash

- 6.1.1.4. Others

- 6.1.2. Online Sale

- 6.1.2.1. Others (

- 6.1.1. Point of Sale

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Retail

- 6.2.2. Entertainment

- 6.2.3. Healthcare

- 6.2.4. Hospitality

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Bank Pekao

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Apple Pay*List Not Exhaustive

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 PKO Bank Polski

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Mastercard

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 PayPal Holdings Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 PayU

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Santander Bank Polska

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 DotPay

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 American Express

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Tap2Pay me

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Bank Pekao

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Poland Payments Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Poland Payments Industry Share (%) by Company 2025

List of Tables

- Table 1: Poland Payments Industry Revenue billion Forecast, by Mode of Payment 2020 & 2033

- Table 2: Poland Payments Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Poland Payments Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Poland Payments Industry Revenue billion Forecast, by Mode of Payment 2020 & 2033

- Table 5: Poland Payments Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Poland Payments Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Poland Payments Industry?

The projected CAGR is approximately 12.5%.

2. Which companies are prominent players in the Poland Payments Industry?

Key companies in the market include Bank Pekao, Apple Pay*List Not Exhaustive, PKO Bank Polski, Mastercard, PayPal Holdings Inc, PayU, Santander Bank Polska, DotPay, American Express, Tap2Pay me.

3. What are the main segments of the Poland Payments Industry?

The market segments include Mode of Payment, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 210.15 billion as of 2022.

5. What are some drivers contributing to market growth?

Advancements in the Polish Payments Market; Initiatives by the Government to improve cashless payment methods.

6. What are the notable trends driving market growth?

Advancements in the Polish Payments Market.

7. Are there any restraints impacting market growth?

Lack of a standard legislative policy remains especially in the case of cross-border transactions.

8. Can you provide examples of recent developments in the market?

May 2022 - Allegro announced a new service implemented in one of the platform's delivery methods - One Kurier. Customers using this method and paying for cash-on-delivery purchases can pay by card or smartphone using the contactless method on the courier's device used to manage shipments.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Poland Payments Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Poland Payments Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Poland Payments Industry?

To stay informed about further developments, trends, and reports in the Poland Payments Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence