Key Insights

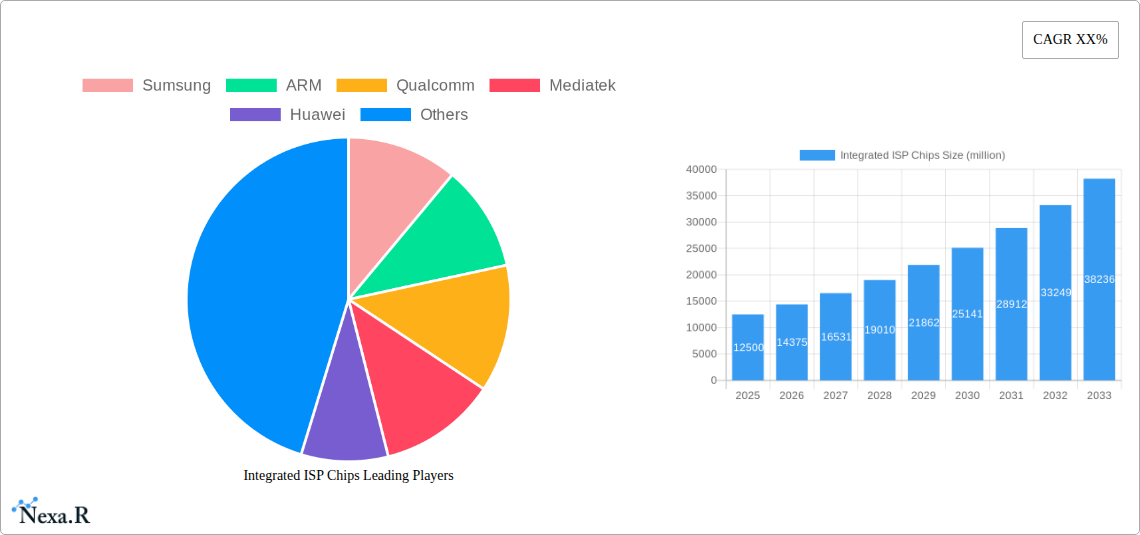

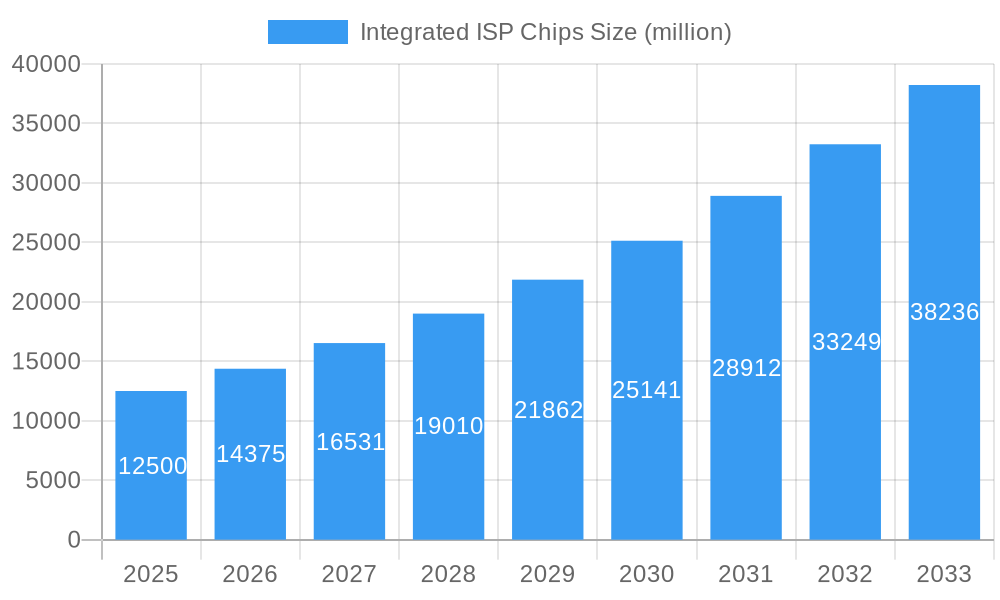

The global Integrated ISP (Image Signal Processor) Chips market is poised for substantial growth, projected to reach an estimated USD 12,500 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 15% during the forecast period of 2025-2033. This expansion is primarily fueled by the insatiable demand for enhanced image and video processing capabilities across a multitude of consumer electronics and automotive applications. Smartphone photography, a cornerstone of the market, continues to drive innovation with users expecting ever-higher quality images and advanced computational photography features. Concurrently, the burgeoning adoption of self-driving cars necessitates sophisticated ISP chips for real-time object detection, scene understanding, and overall sensor data fusion, making them a critical component for automotive safety and autonomy. The smart security sector is also a significant contributor, with the proliferation of high-resolution surveillance cameras and intelligent video analytics systems demanding powerful ISP solutions.

Integrated ISP Chips Market Size (In Billion)

Further propelling this market forward are several key trends. The miniaturization and integration of ISP functionalities directly into System-on-Chip (SoC) designs are becoming increasingly prevalent, leading to more power-efficient and cost-effective solutions, particularly for mobile devices. This integration also allows for tighter coupling with other processing units, enabling more complex AI-driven image enhancement algorithms. The development of advanced imaging technologies, such as higher pixel counts, improved low-light performance, and wider dynamic range (HDR), directly translates to a greater need for specialized ISP capabilities. While the market enjoys strong growth, potential restraints include the highly competitive landscape, characterized by intense price pressures and rapid technological obsolescence. Furthermore, the complex and lengthy R&D cycles associated with advanced semiconductor manufacturing can pose challenges for smaller players. Nevertheless, the continued evolution of digital imaging and the expanding applications for visual data processing indicate a bright and dynamic future for the Integrated ISP Chips market.

Integrated ISP Chips Company Market Share

Integrated ISP Chips Market Report: Unlocking the Future of Imaging and Processing

This comprehensive report, "Integrated ISP Chips Market: Global Analysis & Forecast 2019–2033," offers an in-depth examination of the dynamic and rapidly evolving Integrated Image Signal Processor (ISP) chip market. Spanning a historical period from 2019 to 2024, with a base year of 2025 and a robust forecast period extending to 2033, this report provides unparalleled insights into market dynamics, growth trends, regional dominance, product innovation, key drivers, challenges, emerging opportunities, and the influential players shaping this critical semiconductor segment. Leveraging high-traffic keywords and a structured approach, this report is designed for industry professionals, investors, and strategists seeking to understand and capitalize on the burgeoning opportunities within the integrated ISP chip ecosystem. The market is segmented by application, including Smartphone Photography, Self-Driving Cars, Smart Security, and Others, and by type, namely Integrated in SoC and Integrated in CIS.

Integrated ISP Chips Market Dynamics & Structure

The global integrated ISP chip market is characterized by a moderate to high concentration, with key players like Samsung, ARM, and Qualcomm holding significant market shares. Technological innovation is the primary driver, with continuous advancements in AI, machine learning, and computational photography directly impacting ISP capabilities. Regulatory frameworks, particularly those related to data privacy and AI ethics, are beginning to influence chip design and deployment. Competitive product substitutes, such as discrete ISPs or advanced software-based image processing, present a moderating factor, though integrated solutions offer significant advantages in terms of power efficiency and form factor. End-user demographics are increasingly sophisticated, demanding higher image quality, advanced features, and seamless integration across devices. Mergers and acquisitions (M&A) are a notable trend, as companies seek to consolidate their market position and acquire specialized technological expertise.

- Market Concentration: Dominated by a few key players, with a growing presence of specialized chip designers.

- Technological Innovation Drivers: AI acceleration, enhanced noise reduction, advanced HDR, and real-time video processing capabilities.

- Regulatory Frameworks: Evolving standards for data security and AI bias in imaging systems.

- Competitive Product Substitutes: Software-based image processing and discrete ISP solutions.

- End-User Demographics: Demanding superior image quality, advanced computational photography features, and seamless integration.

- M&A Trends: Strategic acquisitions to gain access to IP, talent, and emerging technologies.

Integrated ISP Chips Growth Trends & Insights

The integrated ISP chip market is poised for substantial growth, driven by the relentless demand for enhanced visual experiences across a multitude of applications. The market size is projected to expand significantly from an estimated $15,000 million in the base year of 2025, demonstrating a Compound Annual Growth Rate (CAGR) of approximately 12.5% during the forecast period of 2025–2033. Adoption rates are accelerating, particularly in the smartphone segment, where computational photography has become a key differentiator. Technological disruptions, such as the integration of neural processing units (NPUs) directly within ISPs, are transforming image processing capabilities, enabling real-time AI inferencing for features like scene recognition, object tracking, and advanced image enhancement. Consumer behavior shifts, prioritizing high-quality imaging for social media, content creation, and immersive experiences, are further fueling this demand.

The increasing prevalence of AI in image processing is a pivotal factor, enabling functionalities previously thought impossible. For instance, advanced deep learning algorithms are now being implemented directly into ISP hardware, allowing for on-device AI inference that enhances image quality, enables sophisticated editing capabilities, and supports real-time visual analysis. This has a direct impact on market penetration, with integrated ISP solutions becoming standard in premium and mid-range smartphones, and rapidly gaining traction in other sectors.

The evolution of Smartphone Photography remains a primary growth engine. Consumers expect professional-grade photos and videos from their mobile devices, pushing manufacturers to integrate more powerful and intelligent ISPs. This includes capabilities like improved low-light performance, enhanced dynamic range, and sophisticated portrait modes, all of which are heavily reliant on ISP processing power. The market penetration of these advanced ISPs in smartphones is nearing saturation in developed markets but continues to grow in emerging economies.

In the Self-Driving Cars sector, ISPs are critical for processing sensor data from cameras, enabling the vehicle to perceive its environment. This includes object detection, lane keeping, and understanding traffic signals. The increasing sophistication of autonomous driving systems directly translates to a higher demand for high-performance, low-latency ISPs capable of handling massive amounts of visual data. The growth in this segment is propelled by advancements in AI and sensor fusion technologies.

The Smart Security segment, encompassing surveillance cameras and smart home devices, is another significant contributor. The demand for higher resolution, better night vision, and intelligent analytics like facial recognition and anomaly detection is driving the adoption of advanced ISPs. These chips enable more efficient data processing and reduced bandwidth requirements for cloud storage and transmission.

The Others segment, which includes applications like drones, augmented reality (AR) and virtual reality (VR) devices, and industrial imaging, is experiencing nascent but rapid growth. As these technologies mature, the need for specialized, high-performance ISPs will escalate, presenting new avenues for market expansion. The integration of ISPs within System-on-Chips (SoCs) offers a significant cost and power advantage, making them the preferred choice for mass-market devices. Conversely, ISPs integrated directly into Image Sensors (CIS) provide optimized performance for specific sensor characteristics, catering to niche, high-performance applications.

The market penetration for integrated ISPs is estimated to reach 75% of all new camera-enabled devices by 2027, indicating a strong shift towards integrated solutions. The average selling price (ASP) of integrated ISP chips is expected to see a gradual increase, driven by the integration of more advanced features and AI capabilities. From an estimated $2.50 per unit in 2025, the ASP is projected to reach $3.80 per unit by 2033. This growth is underpinned by robust technological advancements and a widening array of applications, creating a fertile ground for sustained market expansion.

Dominant Regions, Countries, or Segments in Integrated ISP Chips

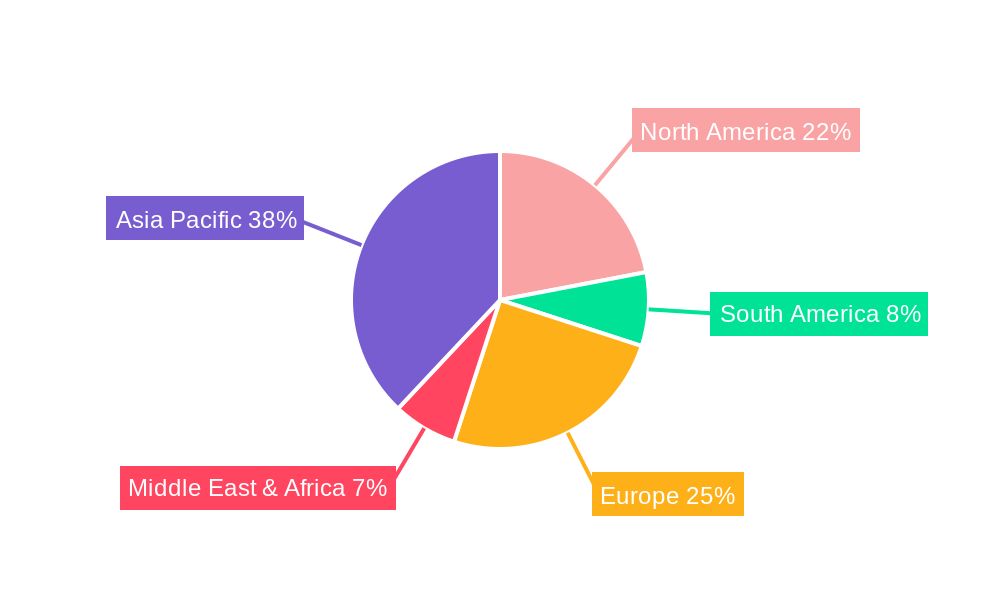

The integrated ISP chip market's dominance is currently driven by a confluence of technological adoption, manufacturing prowess, and end-user demand. Asia Pacific, particularly China, South Korea, and Taiwan, stands out as the leading region, accounting for an estimated 45% of the global market share in 2025. This dominance is fueled by the region's robust electronics manufacturing ecosystem, the presence of major smartphone manufacturers, and a significant domestic market for consumer electronics and emerging technologies like autonomous vehicles and smart cities. Countries like China are not only major consumers but also significant producers and innovators in the semiconductor space, with companies like Huawei and VeriSilicon Microelectronics (Shanghai) Co.,Ltd. playing crucial roles.

Within the application segments, Smartphone Photography remains the undisputed leader, contributing approximately 60% to the overall market revenue. This is driven by the fierce competition among smartphone manufacturers to offer superior camera experiences, pushing the boundaries of computational photography and image quality. The demand for higher resolution sensors, advanced AI-powered image processing, and features like 8K video recording directly translates to a need for more sophisticated integrated ISPs. The rapid upgrade cycles in the smartphone industry ensure a consistent demand for these chips.

The Integrated in SoC type is the predominant form factor, accounting for an estimated 70% of the market. This is due to the cost-effectiveness, power efficiency, and space-saving advantages offered by integrating the ISP onto the main processing chip. Major SoC manufacturers like Qualcomm, MediaTek, and Samsung leverage integrated ISPs to differentiate their chipsets and provide a complete solution for device manufacturers. This integration is crucial for the proliferation of smartphones, wearables, and other portable devices.

However, the Self-Driving Cars segment is emerging as a powerful growth driver, with an expected CAGR of 18% over the forecast period. The increasing complexity and safety requirements of autonomous driving necessitate powerful, specialized ISPs capable of real-time processing of vast amounts of visual data from multiple cameras and sensors. Countries leading in automotive innovation and investment in AI and autonomous driving technologies, such as the United States and Germany, are key markets for these high-performance ISPs. Government initiatives supporting the development of smart cities and autonomous transportation infrastructure are further accelerating adoption.

The Smart Security segment is also experiencing robust growth, driven by the expanding adoption of smart home devices, advanced surveillance systems, and enterprise security solutions. Increased demand for high-definition video, intelligent analytics like facial recognition and behavioral analysis, and improved low-light performance in security cameras are key factors. The growing focus on public safety and the smart city initiatives globally are significant economic policies driving this segment's expansion.

South Korea is a critical hub for display and semiconductor technology, with companies like Samsung at the forefront of ISP innovation. Their integrated solutions are vital for the global smartphone and display markets. Taiwan, with its dominant position in semiconductor manufacturing, particularly through TSMC, plays a pivotal role in the production of these advanced chips. The concentration of R&D and manufacturing capabilities in these regions, coupled with significant government investment in the semiconductor industry and emerging technologies, solidifies Asia Pacific's leadership.

The Integrated in CIS type, while smaller in market share at approximately 30%, is crucial for applications requiring highly optimized and specialized image processing. Companies like Sony and OMNIVISION, leading image sensor manufacturers, often integrate ISPs closely with their sensors to achieve unparalleled performance for specific use cases, such as high-speed imaging, scientific applications, or premium smartphone camera modules. The growth in this niche segment is driven by the pursuit of cutting-edge imaging performance and customized solutions.

In summary, while the smartphone segment and integrated-in-SoC type currently dominate, the rapidly evolving needs of self-driving cars and smart security applications, coupled with advancements in specialized integrated-in-CIS solutions, are reshaping the market landscape and driving diversified regional and segmental growth.

Integrated ISP Chips Product Landscape

The integrated ISP chip product landscape is characterized by increasing integration of AI and machine learning capabilities, leading to enhanced computational photography. Innovations focus on advanced noise reduction algorithms, superior High Dynamic Range (HDR) processing, and real-time video enhancement for stunning clarity and vibrant colors. Unique selling propositions include lower power consumption, smaller form factors, and improved processing speeds, enabling richer user experiences in smartphones, autonomous vehicles, and smart security systems. Technological advancements are pushing towards on-chip AI inferencing, real-time object recognition, and seamless integration with other processing units.

Key Drivers, Barriers & Challenges in Integrated ISP Chips

The integrated ISP chip market is propelled by several key drivers, including the escalating demand for high-quality imaging across consumer electronics, the rapid advancement of AI and machine learning for computational photography, and the growing adoption of smart devices in automotive and security sectors. Technological innovation in image processing, such as advanced noise reduction and HDR, further fuels market growth.

- Technological Advancement: Continuous innovation in AI, computational photography, and image sensor technology.

- Growing Demand: Increasing consumer preference for superior camera performance in smartphones and other devices.

- Emerging Applications: Proliferation of autonomous vehicles and smart security systems requiring sophisticated visual processing.

Conversely, the market faces significant barriers and challenges. Supply chain disruptions, particularly for critical raw materials and manufacturing capacity, can lead to production delays and increased costs. Stringent regulatory frameworks concerning data privacy and AI bias in imaging systems add complexity to product development. Intense competition from both established players and emerging startups can pressure profit margins.

- Supply Chain Volatility: Geopolitical factors and manufacturing bottlenecks impacting availability.

- Regulatory Hurdles: Evolving data privacy laws and AI ethics guidelines.

- Competitive Pressure: Price wars and the need for constant innovation to maintain market share.

Emerging Opportunities in Integrated ISP Chips

Emerging opportunities in the integrated ISP chip sector lie in the burgeoning fields of augmented and virtual reality (AR/VR), where high-fidelity image processing is paramount. The increasing adoption of drones for commercial and recreational purposes, demanding advanced image stabilization and real-time video analytics, presents another significant growth avenue. Furthermore, the expansion of the Internet of Things (IoT) ecosystem, particularly in smart home and industrial automation, creates a demand for cost-effective, low-power ISPs capable of basic image recognition and analysis. The development of specialized ISPs for medical imaging and scientific research also represents untapped potential.

Growth Accelerators in the Integrated ISP Chips Industry

Long-term growth in the integrated ISP chip industry is being accelerated by breakthroughs in AI hardware acceleration, enabling more powerful and efficient on-chip processing. Strategic partnerships between semiconductor manufacturers, device OEMs, and software developers are crucial for co-creating innovative imaging solutions and expanding market reach. The ongoing miniaturization of components and the drive for increased power efficiency are also critical factors, enabling the integration of advanced ISPs into an ever-wider array of compact and portable devices. Market expansion strategies focusing on emerging economies with rapidly growing smartphone penetration and smart device adoption will also contribute significantly to sustained growth.

Key Players Shaping the Integrated ISP Chips Market

- Samsung

- ARM

- Qualcomm

- MediaTek

- Huawei

- Sony

- OMNIVISION

- VeriSilicon Microelectronics (Shanghai) Co.,Ltd.

- ASR Microelectronics Co.,Ltd.

Notable Milestones in Integrated ISP Chips Sector

- 2019 Q3: Samsung introduces its Exynos 990 SoC featuring an advanced ISP with AI capabilities for enhanced mobile photography.

- 2020 Q1: ARM announces the Mali-G77 MC11 GPU, emphasizing its integrated ISP enhancements for improved mobile gaming and imaging.

- 2021 Q2: Qualcomm unveils its Snapdragon 8 Gen 1, highlighting a new generation of ISP with advanced computational photography features for premium smartphones.

- 2022 Q4: Sony launches its IMX600 series of image sensors with integrated ISP functionalities for flagship smartphone cameras.

- 2023 Q1: MediaTek's Dimensity 9200+ showcases significant ISP improvements for AI-driven imaging and video processing.

- 2023 Q3: VeriSilicon Microelectronics (Shanghai) Co.,Ltd. announces its new ISP IP portfolio targeting automotive and IoT applications.

- 2024 Q1: OMNIVISION introduces a new generation of ISP integrated into its automotive image sensors, promising enhanced ADAS performance.

- 2024 Q4: ASR Microelectronics Co.,Ltd. releases a new series of ISPs designed for cost-effective smart security cameras with AI capabilities.

In-Depth Integrated ISP Chips Market Outlook

The future outlook for the integrated ISP chip market is exceptionally promising, driven by an accelerating integration of AI, expanding applications in autonomous systems, and continuous consumer demand for superior visual experiences. Growth accelerators like on-chip AI inferencing and strategic collaborations will foster innovation and market penetration. Untapped markets in emerging economies and specialized sectors like medical imaging present significant opportunities for growth and diversification. The industry is poised for sustained expansion as these powerful processing units become indispensable across a vast and growing technological landscape.

Integrated ISP Chips Segmentation

-

1. Application

- 1.1. Smartphone Photography

- 1.2. Self - Driving Cars

- 1.3. Smart Security

- 1.4. Others

-

2. Types

- 2.1. Integrated in SoC

- 2.2. Integrated in CIS

Integrated ISP Chips Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Integrated ISP Chips Regional Market Share

Geographic Coverage of Integrated ISP Chips

Integrated ISP Chips REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Integrated ISP Chips Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Smartphone Photography

- 5.1.2. Self - Driving Cars

- 5.1.3. Smart Security

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Integrated in SoC

- 5.2.2. Integrated in CIS

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Integrated ISP Chips Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Smartphone Photography

- 6.1.2. Self - Driving Cars

- 6.1.3. Smart Security

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Integrated in SoC

- 6.2.2. Integrated in CIS

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Integrated ISP Chips Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Smartphone Photography

- 7.1.2. Self - Driving Cars

- 7.1.3. Smart Security

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Integrated in SoC

- 7.2.2. Integrated in CIS

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Integrated ISP Chips Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Smartphone Photography

- 8.1.2. Self - Driving Cars

- 8.1.3. Smart Security

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Integrated in SoC

- 8.2.2. Integrated in CIS

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Integrated ISP Chips Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Smartphone Photography

- 9.1.2. Self - Driving Cars

- 9.1.3. Smart Security

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Integrated in SoC

- 9.2.2. Integrated in CIS

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Integrated ISP Chips Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Smartphone Photography

- 10.1.2. Self - Driving Cars

- 10.1.3. Smart Security

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Integrated in SoC

- 10.2.2. Integrated in CIS

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Sumsung

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 ARM

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Qualcomm

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Mediatek

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Huawei

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Sony

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 OMNIVISION

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 VeriSilicon Microelectronics (Shanghai) Co.

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Ltd.

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 ASR Microelectronics Co.

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Ltd.

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Sumsung

List of Figures

- Figure 1: Global Integrated ISP Chips Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Integrated ISP Chips Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Integrated ISP Chips Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Integrated ISP Chips Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Integrated ISP Chips Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Integrated ISP Chips Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Integrated ISP Chips Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Integrated ISP Chips Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Integrated ISP Chips Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Integrated ISP Chips Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Integrated ISP Chips Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Integrated ISP Chips Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Integrated ISP Chips Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Integrated ISP Chips Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Integrated ISP Chips Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Integrated ISP Chips Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Integrated ISP Chips Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Integrated ISP Chips Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Integrated ISP Chips Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Integrated ISP Chips Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Integrated ISP Chips Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Integrated ISP Chips Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Integrated ISP Chips Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Integrated ISP Chips Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Integrated ISP Chips Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Integrated ISP Chips Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Integrated ISP Chips Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Integrated ISP Chips Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Integrated ISP Chips Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Integrated ISP Chips Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Integrated ISP Chips Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Integrated ISP Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Integrated ISP Chips Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Integrated ISP Chips Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Integrated ISP Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Integrated ISP Chips Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Integrated ISP Chips Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Integrated ISP Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Integrated ISP Chips Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Integrated ISP Chips Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Integrated ISP Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Integrated ISP Chips Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Integrated ISP Chips Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Integrated ISP Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Integrated ISP Chips Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Integrated ISP Chips Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Integrated ISP Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Integrated ISP Chips Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Integrated ISP Chips Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Integrated ISP Chips Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Integrated ISP Chips?

The projected CAGR is approximately 13.7%.

2. Which companies are prominent players in the Integrated ISP Chips?

Key companies in the market include Sumsung, ARM, Qualcomm, Mediatek, Huawei, Sony, OMNIVISION, VeriSilicon Microelectronics (Shanghai) Co., Ltd., ASR Microelectronics Co., Ltd..

3. What are the main segments of the Integrated ISP Chips?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Integrated ISP Chips," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Integrated ISP Chips report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Integrated ISP Chips?

To stay informed about further developments, trends, and reports in the Integrated ISP Chips, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence