Key Insights

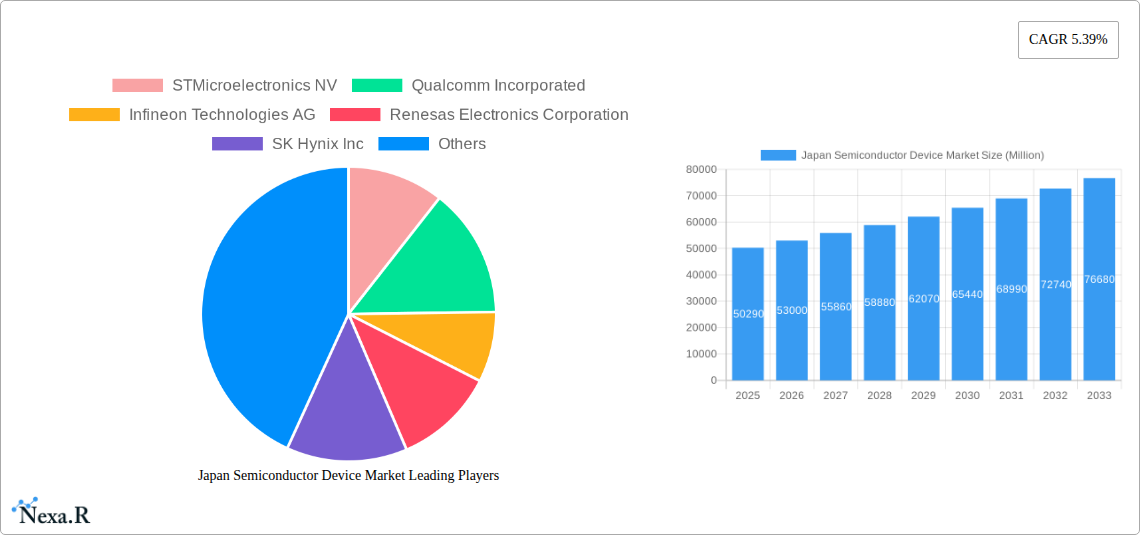

The Japan semiconductor device market, valued at $50.29 billion in 2025, is projected to experience robust growth, driven by a Compound Annual Growth Rate (CAGR) of 5.39% from 2025 to 2033. This expansion is fueled by several key factors. The burgeoning automotive sector in Japan, with its increasing reliance on advanced driver-assistance systems (ADAS) and electric vehicles (EVs), significantly boosts demand for semiconductors. Furthermore, the robust communication infrastructure, encompassing both wired and wireless technologies, fuels the need for high-performance integrated circuits and microprocessors. The consumer electronics sector, known for its innovation in Japan, further contributes to market growth, demanding advanced sensors and microcontrollers for improved functionality and user experience. While supply chain constraints and global economic uncertainties represent potential restraints, ongoing government investments in technological advancements and the strong presence of established semiconductor manufacturers within Japan mitigate these risks. The market's segmentation highlights the importance of integrated circuits, microprocessors, and microcontrollers across various end-user verticals. The regional concentration within Japan, focusing on key areas like Kanto, Kansai, and Chubu, signifies opportunities for targeted market penetration.

The forecast period (2025-2033) suggests a continued upward trajectory for the Japan semiconductor device market. While specific regional breakdowns beyond the provided Japanese prefectures are not available, the overall growth is expected to be consistent with global trends, though potentially influenced by Japan’s unique focus on specific technological sectors and its advanced manufacturing capabilities. The presence of major global players like STMicroelectronics, Qualcomm, and Renesas Electronics underscores Japan's importance in the global semiconductor landscape and positions the nation for continued competitiveness in this crucial technology sector. Specific growth within segments such as optoelectronics and sensors will likely mirror advancements in areas like robotics, automation, and the Internet of Things (IoT), creating further opportunities for market expansion.

Japan Semiconductor Device Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Japan semiconductor device market, encompassing market dynamics, growth trends, key players, and future outlook. With a study period spanning from 2019 to 2033, a base year of 2025, and a forecast period of 2025-2033, this report offers invaluable insights for industry professionals, investors, and strategic decision-makers. The report analyzes the market across various segments, including device types (discrete semiconductors, optoelectronics, sensors, integrated circuits, microprocessors (MPU), microcontrollers (MCU), digital signal processors) and end-user verticals (automotive, communication, consumer electronics, industrial, computing/data storage, and others). The market size is presented in million units.

Parent Market: Global Semiconductor Market Child Market: Japan Semiconductor Devices Market

Japan Semiconductor Device Market Dynamics & Structure

The Japan semiconductor device market is characterized by a complex interplay of factors influencing its structure and dynamics. Market concentration is relatively high, with a few dominant players holding significant market share. Technological innovation is a crucial driver, particularly in areas like AI, 5G, and automotive electronics. Stringent regulatory frameworks, including those related to data privacy and environmental sustainability, shape market practices. The emergence of competitive product substitutes, such as new materials and architectures, constantly challenges established technologies. End-user demographics, notably the aging population and shifting consumer preferences, influence demand patterns. Furthermore, mergers and acquisitions (M&A) activity plays a significant role in shaping the competitive landscape.

- Market Concentration: High, with top 5 players accounting for xx% of market share in 2024 (estimated).

- Technological Innovation: Rapid advancements in AI, 5G, and automotive electronics are key drivers.

- Regulatory Landscape: Stringent regulations related to data privacy and environmental sustainability influence market dynamics.

- Competitive Substitutes: Emerging materials and architectures challenge established technologies.

- M&A Activity: Significant M&A activity reshapes the market structure; xx deals recorded in the period 2019-2024.

- End-User Demographics: Aging population and evolving consumer preferences impact demand.

Japan Semiconductor Device Market Growth Trends & Insights

The Japan semiconductor device market exhibits robust growth, driven by increasing demand across various end-user verticals. The market size expanded from xx million units in 2019 to xx million units in 2024, showcasing a significant CAGR of xx%. This growth is fueled by technological disruptions, such as the proliferation of IoT devices and the rise of AI-powered applications. Consumer behavior shifts towards smart and connected devices further stimulate market expansion. Adoption rates for advanced semiconductor technologies are rapidly increasing, particularly in automotive and industrial applications. Further market penetration in niche segments, especially within the industrial automation sector, promises continued growth. Technological disruptions, such as the advent of advanced packaging technologies and new materials, constantly reshape market dynamics, creating opportunities for innovative players.

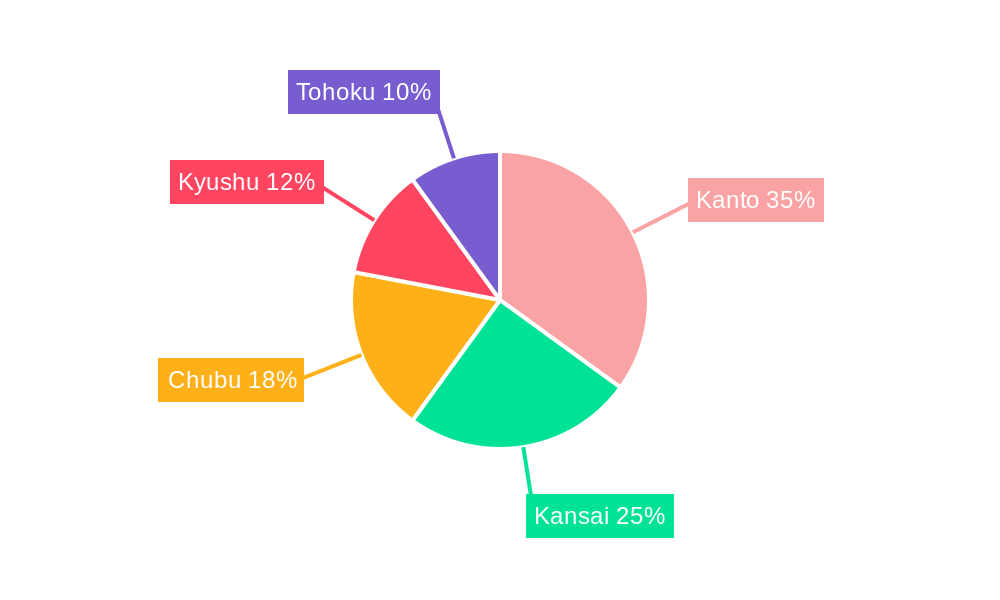

Dominant Regions, Countries, or Segments in Japan Semiconductor Device Market

Within the Japan semiconductor device market, the Kanto region, encompassing Tokyo and surrounding prefectures, holds the largest market share due to its concentration of manufacturing facilities, R&D centers, and a highly skilled workforce. Specific segments driving market growth include:

- By Device Type: Integrated circuits (ICs), particularly microcontrollers (MCUs) and microprocessors (MPUs), dominate the market, driven by high demand from automotive and consumer electronics sectors. The optoelectronics segment shows significant growth potential due to applications in displays and communication infrastructure.

- By End-user Vertical: The automotive sector is the largest end-user vertical, fueled by the increasing adoption of advanced driver-assistance systems (ADAS) and electric vehicles. Consumer electronics maintain a strong position, driven by demand for smartphones, smart home devices, and gaming consoles.

Key drivers contributing to regional dominance include robust government support for the semiconductor industry, well-established infrastructure, and access to a highly skilled workforce. Growth potential is particularly evident in the industrial sector, driven by automation and smart manufacturing initiatives.

Japan Semiconductor Device Market Product Landscape

The Japanese semiconductor device market is characterized by a diverse product landscape encompassing a wide array of devices with varying functionalities and performance metrics. Continuous product innovations focus on enhancing performance, reducing power consumption, and miniaturizing device sizes. Key trends include the integration of advanced features like AI capabilities into existing devices, and the development of new materials and architectures to improve device efficiency. The market is witnessing the emergence of unique selling propositions based on specialized functionalities and superior performance characteristics, enabling devices to cater to increasingly complex applications.

Key Drivers, Barriers & Challenges in Japan Semiconductor Device Market

Key Drivers:

- Increasing demand for high-performance electronics across various sectors (automotive, consumer electronics, industrial).

- Government initiatives and investments aimed at boosting domestic semiconductor production.

- Technological advancements in miniaturization, power efficiency, and performance.

Key Challenges:

- Global supply chain disruptions and geopolitical uncertainties significantly impact semiconductor availability and pricing.

- Intense competition from global players leads to price pressure and reduced profit margins.

- The high cost of research and development and manufacturing poses a significant barrier to entry for new players.

Emerging Opportunities in Japan Semiconductor Device Market

- Expansion into emerging applications, such as AI-powered devices and IoT solutions, presents significant growth opportunities.

- The development of specialized semiconductor devices tailored to specific industrial needs unlocks new market segments.

- Strategic partnerships and collaborations with foreign companies can help strengthen the Japanese semiconductor industry’s global competitiveness.

Growth Accelerators in the Japan Semiconductor Device Market Industry

Technological breakthroughs, especially in advanced packaging and new materials, are driving significant growth. Strategic partnerships and collaborations between Japanese companies and foreign technology firms are further enhancing innovation and market reach. Expansion into high-growth segments, such as electric vehicles and smart manufacturing, significantly accelerates market expansion.

Key Players Shaping the Japan Semiconductor Device Market Market

- STMicroelectronics NV

- Qualcomm Incorporated

- Infineon Technologies AG

- Renesas Electronics Corporation

- SK Hynix Inc

- Rohm Co Ltd

- Advanced Semiconductor Engineering Inc

- ON Semiconductor Corporation

- NXP Semiconductors NV

- Toshiba Corporation

- Micron Technology Inc

- Kyocera Corporation

- Xilinx Inc

- Texas Instruments Inc

- Nvidia Corporation

- Samsung Electronics Co Ltd

- Taiwan Semiconductor Manufacturing Company (TSMC) Limited

- Intel Corporation

- Fujitsu Semiconductor Ltd

- Broadcom Inc

Notable Milestones in Japan Semiconductor Device Market Sector

- May 2024: Toshiba completes a new 300-millimeter wafer fabrication facility for power semiconductors, signifying increased production capacity and bolstering its position in the power semiconductor market.

- May 2024: SK Hynix unveils ZUFS 4.0, a high-performance solution for on-device AI in mobile devices, strengthening its competitiveness in the AI memory segment and leveraging its DRAM expertise.

In-Depth Japan Semiconductor Device Market Market Outlook

The Japan semiconductor device market is poised for continued growth, driven by technological advancements, government support, and expanding demand across key sectors. Strategic partnerships and investment in R&D will further fuel innovation and expansion into high-growth applications. The market's future potential is significant, with opportunities for both established players and new entrants to capitalize on emerging trends and technological disruptions. The focus on advanced packaging, innovative materials, and AI integration will shape the market's trajectory in the coming years.

Japan Semiconductor Device Market Segmentation

-

1. Device Type

- 1.1. Discrete Semiconductors

- 1.2. Optoelectronics

- 1.3. Sensors

-

1.4. Integrated Circuits

- 1.4.1. Analog

- 1.4.2. Logic

- 1.4.3. Memory

-

1.4.4. Micro

- 1.4.4.1. Microprocessors (MPU)

- 1.4.4.2. Microcontrollers (MCU)

- 1.4.4.3. Digital Signal Processors

-

2. End-user Vertical

- 2.1. Automotive

- 2.2. Communication (Wired and Wireless)

- 2.3. Consumer Electronics

- 2.4. Industrial

- 2.5. Computing/Data Storage

- 2.6. Other End-user Verticals

Japan Semiconductor Device Market Segmentation By Geography

- 1. Japan

Japan Semiconductor Device Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.39% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Adoption of Technologies like IoT and AI; Increased Deployment of 5G and Rising Demand for 5G Smartphones

- 3.3. Market Restrains

- 3.3.1. Supply Chain Disruptions Resulting in Semiconductor Chip Shortage

- 3.4. Market Trends

- 3.4.1. Automotive is Expected to Hold Significant Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Japan Semiconductor Device Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 5.1.1. Discrete Semiconductors

- 5.1.2. Optoelectronics

- 5.1.3. Sensors

- 5.1.4. Integrated Circuits

- 5.1.4.1. Analog

- 5.1.4.2. Logic

- 5.1.4.3. Memory

- 5.1.4.4. Micro

- 5.1.4.4.1. Microprocessors (MPU)

- 5.1.4.4.2. Microcontrollers (MCU)

- 5.1.4.4.3. Digital Signal Processors

- 5.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.2.1. Automotive

- 5.2.2. Communication (Wired and Wireless)

- 5.2.3. Consumer Electronics

- 5.2.4. Industrial

- 5.2.5. Computing/Data Storage

- 5.2.6. Other End-user Verticals

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 6. Kanto Japan Semiconductor Device Market Analysis, Insights and Forecast, 2019-2031

- 7. Kansai Japan Semiconductor Device Market Analysis, Insights and Forecast, 2019-2031

- 8. Chubu Japan Semiconductor Device Market Analysis, Insights and Forecast, 2019-2031

- 9. Kyushu Japan Semiconductor Device Market Analysis, Insights and Forecast, 2019-2031

- 10. Tohoku Japan Semiconductor Device Market Analysis, Insights and Forecast, 2019-2031

- 11. Competitive Analysis

- 11.1. Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 STMicroelectronics NV

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Qualcomm Incorporated

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Infineon Technologies AG

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Renesas Electronics Corporation

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 SK Hynix Inc

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Rohm Co Ltd

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Advanced Semiconductor Engineering Inc

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 ON Semiconductor Corporation*List Not Exhaustive

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 NXP Semiconductors NV

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Toshiba Corporation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Micron Technology Inc

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Kyocera Corporation

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Xilinx Inc

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Texas Instruments Inc

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Nvidia Corporation

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Samsung Electronics Co Ltd

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Taiwan Semiconductor Manufacturing Company (TSMC) Limited

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Intel Corporation

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Fujitsu Semiconductor Ltd

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Broadcom Inc

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.1 STMicroelectronics NV

List of Figures

- Figure 1: Japan Semiconductor Device Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Japan Semiconductor Device Market Share (%) by Company 2024

List of Tables

- Table 1: Japan Semiconductor Device Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Japan Semiconductor Device Market Revenue Million Forecast, by Device Type 2019 & 2032

- Table 3: Japan Semiconductor Device Market Revenue Million Forecast, by End-user Vertical 2019 & 2032

- Table 4: Japan Semiconductor Device Market Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Japan Semiconductor Device Market Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Kanto Japan Semiconductor Device Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Kansai Japan Semiconductor Device Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Chubu Japan Semiconductor Device Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Kyushu Japan Semiconductor Device Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Tohoku Japan Semiconductor Device Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Japan Semiconductor Device Market Revenue Million Forecast, by Device Type 2019 & 2032

- Table 12: Japan Semiconductor Device Market Revenue Million Forecast, by End-user Vertical 2019 & 2032

- Table 13: Japan Semiconductor Device Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japan Semiconductor Device Market?

The projected CAGR is approximately 5.39%.

2. Which companies are prominent players in the Japan Semiconductor Device Market?

Key companies in the market include STMicroelectronics NV, Qualcomm Incorporated, Infineon Technologies AG, Renesas Electronics Corporation, SK Hynix Inc, Rohm Co Ltd, Advanced Semiconductor Engineering Inc, ON Semiconductor Corporation*List Not Exhaustive, NXP Semiconductors NV, Toshiba Corporation, Micron Technology Inc, Kyocera Corporation, Xilinx Inc, Texas Instruments Inc, Nvidia Corporation, Samsung Electronics Co Ltd, Taiwan Semiconductor Manufacturing Company (TSMC) Limited, Intel Corporation, Fujitsu Semiconductor Ltd, Broadcom Inc.

3. What are the main segments of the Japan Semiconductor Device Market?

The market segments include Device Type, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 50.29 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Adoption of Technologies like IoT and AI; Increased Deployment of 5G and Rising Demand for 5G Smartphones.

6. What are the notable trends driving market growth?

Automotive is Expected to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

Supply Chain Disruptions Resulting in Semiconductor Chip Shortage.

8. Can you provide examples of recent developments in the market?

May 2024: Toshiba marked the completion of a new 300-millimeter wafer fabrication facility for power semiconductors and an office building at KagaToshiba Electronics Corporation in Ishikawa Prefecture, Japan, one of Toshiba’s key group companies. Toshiba will now proceed with equipment installation, toward starting mass production in the second half of fiscal year 2024.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japan Semiconductor Device Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japan Semiconductor Device Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japan Semiconductor Device Market?

To stay informed about further developments, trends, and reports in the Japan Semiconductor Device Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence