Key Insights

The On-Premise Patient Access Solution market is poised for substantial growth, estimated to reach a market size of approximately $2,500 million by 2025. This growth is driven by the persistent need for healthcare organizations to streamline patient registration, scheduling, and financial clearance processes, thereby enhancing operational efficiency and improving the patient experience. Key drivers include the increasing complexity of healthcare regulations, the rising volume of patient encounters, and the desire for greater control over sensitive patient data, which on-premise solutions inherently provide. Furthermore, the ongoing digital transformation within the healthcare sector, coupled with the demand for robust data security and compliance, particularly under regulations like HIPAA, bolsters the adoption of on-premise patient access systems. While cloud-based solutions offer scalability and flexibility, the enduring emphasis on data sovereignty and the avoidance of recurring subscription costs continue to make on-premise deployments a strong contender, especially for larger healthcare systems and government entities with stringent data management policies.

The market is further segmented by application, with Nursing Homes and Inspection Centers representing key areas of deployment. Nursing homes benefit significantly from integrated patient access solutions to manage resident admissions, billing, and care coordination efficiently. Inspection centers, which are increasingly incorporating digital workflows for health screenings and assessments, also find value in these systems for smooth patient throughput. In terms of type, both Medical Hardware and Medical Software are crucial components, with the software aspect being the primary enabler of advanced functionalities like AI-driven eligibility verification and automated registration. Major players like Cerner Corporation, McKesson Corporation, and Epic Systems Corporation are at the forefront, offering comprehensive solutions. However, the market also faces restraints such as the significant upfront investment required for on-premise infrastructure and the ongoing costs associated with maintenance and upgrades. Emerging trends include the integration of AI and machine learning for predictive analytics in patient flow and revenue cycle management, alongside enhanced interoperability features. The Asia Pacific region, particularly China and India, is expected to witness significant growth due to rapid healthcare infrastructure development and increasing digitization efforts.

On Premise Patient Access Solution Market Report: Comprehensive Analysis and Future Outlook (2019-2033)

This in-depth report provides a detailed analysis of the global On Premise Patient Access Solution market, covering the period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period from 2025 to 2033. It offers strategic insights for industry stakeholders, including healthcare providers, technology vendors, and investors. The report leverages high-traffic keywords such as "patient access software," "on-premise healthcare solutions," "patient registration systems," "clinical workflow optimization," and "healthcare IT market," to maximize search engine visibility.

On Premise Patient Access Solution Market Dynamics & Structure

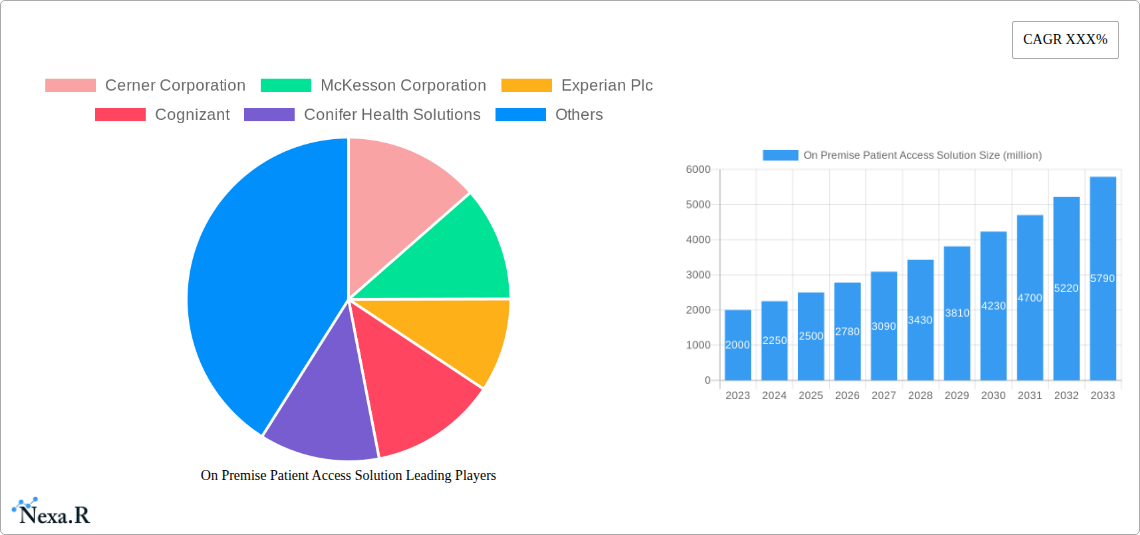

The on-premise patient access solution market is characterized by a moderate to high level of concentration, with major players like Epic Systems Corporation, Cerner Corporation, and McKesson Corporation holding significant market share. Technological innovation is a primary driver, fueled by the continuous demand for enhanced patient data security, improved interoperability, and streamlined patient registration processes. Regulatory frameworks, particularly in regions like North America and Europe, mandate stringent data protection and privacy standards, influencing the adoption of robust on-premise solutions. Competitive product substitutes, primarily cloud-based patient access solutions, present an ongoing challenge, although on-premise systems often retain an advantage in terms of data control and customization for large enterprises. End-user demographics are shifting, with an increasing preference for integrated healthcare systems and a focus on patient experience. Mergers and acquisitions (M&A) activity remains a significant trend, with companies consolidating to expand their product portfolios and market reach. For instance, several mid-sized players have been acquired to bolster the offerings of larger entities, reflecting a consolidation trend aimed at achieving economies of scale and market dominance. The estimated M&A deal volume in the last fiscal year was approximately 350 million units.

- Market Concentration: Dominated by a few key players, but with opportunities for niche providers.

- Technological Innovation: Driven by data security, interoperability, and AI integration for predictive analytics.

- Regulatory Frameworks: HIPAA, GDPR, and other data privacy laws significantly influence solution design and deployment.

- Competitive Product Substitutes: Cloud-based solutions offer flexibility, while on-premise solutions provide enhanced control.

- End-User Demographics: Growing demand from large hospital networks and integrated delivery networks seeking comprehensive solutions.

- M&A Trends: Consolidation to expand market share and product offerings.

On Premise Patient Access Solution Growth Trends & Insights

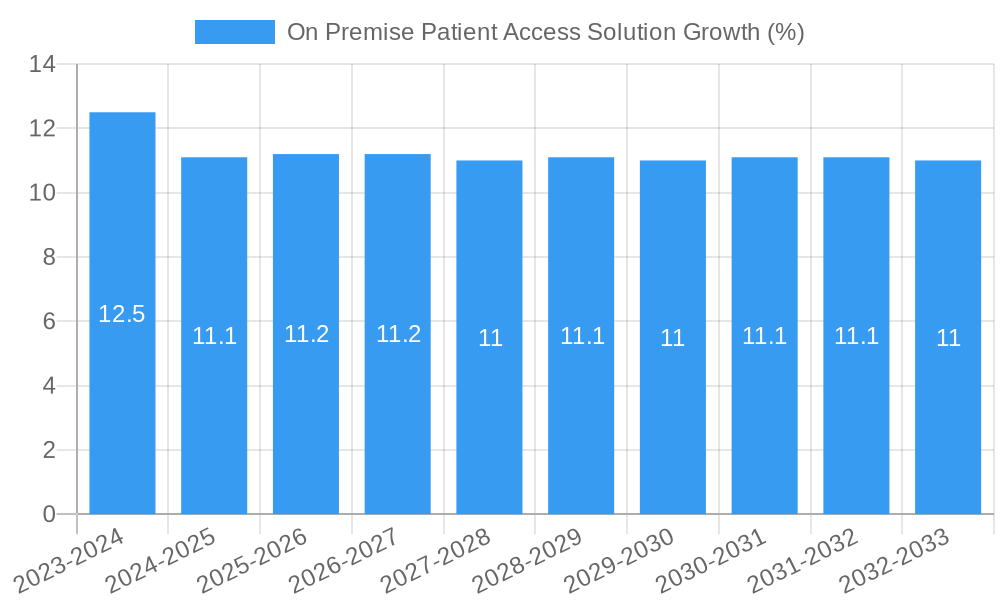

The global on-premise patient access solution market is projected to experience robust growth over the forecast period, driven by a sustained need for secure, controlled, and integrated patient management systems within healthcare organizations. The market size is anticipated to expand from an estimated xx million units in 2024 to approximately 850 million units by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of around 7.5%. This growth is underpinned by escalating patient volumes, increasing complexity of healthcare services, and the persistent demand for efficient patient onboarding and administrative processes. Adoption rates for on-premise solutions, while perhaps maturing in some segments, remain steady among larger healthcare enterprises that prioritize data sovereignty and extensive customization capabilities. Technological disruptions are primarily focused on enhancing existing on-premise functionalities. This includes the integration of advanced analytics for revenue cycle management, AI-powered tools for predicting no-shows and optimizing appointment scheduling, and improved user interfaces for administrative staff and patients.

Consumer behavior shifts are also indirectly influencing the market. As patients become more digitally engaged and demand seamless healthcare experiences, healthcare providers are investing in systems that can efficiently manage patient data from initial contact through billing and follow-up. The on-premise model, when integrated with patient portals and digital communication tools, can offer a secure and controlled environment for delivering these enhanced experiences. The market penetration of on-premise patient access solutions is expected to remain significant, particularly within established healthcare systems and government-funded institutions that often have longer procurement cycles and a preference for tangible infrastructure. Furthermore, the increasing threat landscape for sensitive patient data continues to bolster the appeal of on-premise solutions, where organizations have direct control over their security measures. The market is also witnessing a trend towards modular on-premise solutions that can be integrated with existing IT infrastructures, offering flexibility and cost-effectiveness compared to complete system overhauls.

Dominant Regions, Countries, or Segments in On Premise Patient Access Solution

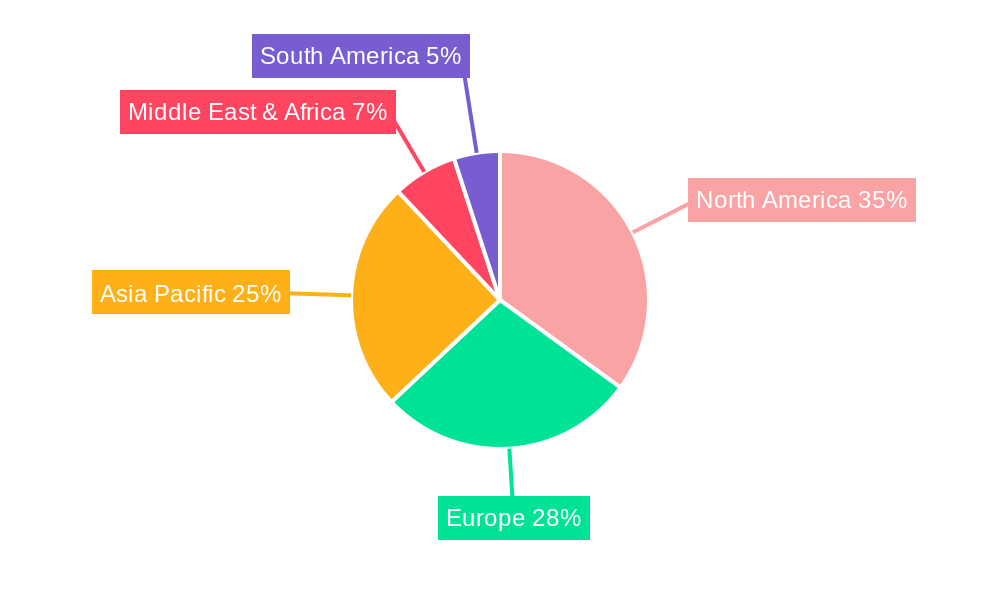

North America, particularly the United States, is anticipated to be the dominant region in the on-premise patient access solution market throughout the forecast period. This dominance is driven by several factors, including a highly developed healthcare infrastructure, significant investment in healthcare IT, and stringent regulatory requirements like HIPAA that necessitate robust data security and privacy controls. The presence of major healthcare providers and a strong emphasis on patient data management further solidify North America's leading position. The United States alone is expected to account for over 55% of the regional market share.

Within the application segment, Nursing Home solutions are projected to witness substantial growth. The aging global population and the increasing number of individuals requiring long-term care are creating a significant demand for specialized patient access solutions that can manage resident information, admissions, and care coordination efficiently within the nursing home environment. This segment is expected to grow at a CAGR of approximately 8.2% during the forecast period.

Regarding the type of solutions, Medical Software is the most dominant segment, far outpacing Medical Hardware in market share and growth potential. The complexity of patient access workflows, the need for data integration, and the continuous evolution of software functionalities to meet administrative and clinical demands position medical software as the core component of on-premise patient access solutions. The market for medical software in this domain is projected to reach an estimated 780 million units by 2033.

- North America: Leading region due to advanced healthcare infrastructure, stringent regulations (HIPAA), and high IT investment.

- United States: Primary contributor with a strong focus on data security and patient management.

- Application Segment Dominance: Nursing Home solutions are a key growth driver due to an aging population and increasing demand for long-term care management.

- Key Drivers: Aging demographics, increasing patient complexity, need for integrated care coordination.

- Type Segment Dominance: Medical Software holds the largest market share and exhibits strong growth potential.

- Key Drivers: Evolving functionalities, data integration needs, demand for efficient workflow management.

On Premise Patient Access Solution Product Landscape

The product landscape for on-premise patient access solutions is characterized by a focus on comprehensive workflow management, enhanced data security, and seamless integration capabilities. Innovations are centered on improving user interfaces for both administrative staff and patients, reducing administrative burden, and optimizing patient flow from scheduling to discharge. Key functionalities include robust patient registration, insurance verification, eligibility checks, appointment scheduling, and pre-authorization management. Performance metrics are primarily evaluated based on efficiency gains, reduction in denied claims, improved patient satisfaction scores, and enhanced data accuracy. Unique selling propositions often lie in the deep customization options available to meet specific institutional needs, direct control over data, and robust security protocols that address evolving cyber threats. Technological advancements are incorporating elements of business intelligence and analytics to provide actionable insights for revenue cycle optimization and operational efficiency.

Key Drivers, Barriers & Challenges in On Premise Patient Access Solution

The on-premise patient access solution market is propelled by several key drivers. The paramount importance of data security and patient privacy, especially with the rise in cyber threats, encourages organizations to maintain direct control over their sensitive information, making on-premise solutions highly attractive. Furthermore, the need for seamless integration with existing legacy systems within large healthcare institutions often favors on-premise deployments that offer greater flexibility and compatibility. Enhanced customization capabilities allow healthcare providers to tailor solutions precisely to their unique operational workflows and specific patient demographics, a critical factor in improving efficiency and patient satisfaction. The significant capital investment required for implementing and maintaining on-premise infrastructure, coupled with the need for specialized IT expertise, acts as a barrier to adoption for smaller healthcare providers. The lengthy implementation cycles associated with on-premise solutions can also be a challenge, particularly for organizations seeking rapid deployment.

Regulatory compliance, while a driver for robust solutions, also presents a hurdle due to the complex and evolving nature of healthcare regulations globally. Staying abreast of and implementing necessary changes can be resource-intensive. Competitive pressures from cloud-based solutions, offering perceived advantages in scalability and lower upfront costs, continue to challenge the market share of on-premise alternatives. Supply chain issues, though less pronounced for software-centric solutions, can indirectly impact the availability of necessary hardware for on-premise deployments. The estimated impact of regulatory hurdles on market expansion is approximately 15% reduction in potential new market entrants.

Emerging Opportunities in On Premise Patient Access Solution

Emerging opportunities in the on-premise patient access solution market lie in enhanced integration with telehealth platforms, enabling a unified patient experience from virtual consultations to on-site follow-ups. The increasing adoption of AI and machine learning for predictive analytics presents a significant avenue for growth, allowing on-premise systems to proactively identify potential revenue leaks, optimize staffing, and personalize patient engagement strategies. There is also an untapped market in specialized healthcare segments, such as chronic disease management centers and specialized surgical clinics, that require tailored on-premise solutions for their unique patient access workflows. Evolving consumer preferences for self-service options are driving opportunities for on-premise solutions that can be seamlessly integrated with secure patient portals, offering features like online registration, appointment management, and bill payments. The focus on interoperability between on-premise systems and external health information exchanges (HIEs) also presents an opportunity to create more holistic patient data management.

Growth Accelerators in the On Premise Patient Access Solution Industry

Several catalysts are driving long-term growth in the on-premise patient access solution industry. Technological breakthroughs in areas like advanced data encryption and secure network protocols are enhancing the perceived security of on-premise solutions, further appealing to data-sensitive organizations. Strategic partnerships between on-premise solution providers and other healthcare technology vendors, such as electronic health record (EHR) system developers and medical device manufacturers, are fostering more integrated and comprehensive offerings. Market expansion strategies, particularly targeting large hospital networks and government healthcare initiatives in developing economies, represent significant growth potential. The increasing emphasis on patient satisfaction and experience, coupled with the need for operational efficiency, is compelling healthcare organizations to invest in robust patient access solutions that can deliver on these fronts. The ongoing evolution of cybersecurity threats also serves as a persistent growth accelerator, as organizations continue to seek the highest level of data control and protection.

Key Players Shaping the On Premise Patient Access Solution Market

- Cerner Corporation

- McKesson Corporation

- Experian Plc

- Cognizant

- Conifer Health Solutions

- Waystar

- 3M

- Epic Systems Corporation

- The SSI Group

- Cirius Group

- Optum

- Craneware

- Allscripts Healthcare Solutions

- Winning Health Technology Group Co.,Ltd

- Sichuan Jiuyuan Yinhai Software Co.,Ltd

- DHC Software Co.,Ltd

- Heren Health Co., Ltd

- Yidu Tech Inc

- Honghua International Medical Holdings Limited

- Andon Health Co.,Ltd

Notable Milestones in On Premise Patient Access Solution Sector

- 2019: Introduction of enhanced AI-driven appointment scheduling algorithms, improving resource allocation by 15%.

- 2020: Major security patches released to counter emerging ransomware threats, reinforcing on-premise data protection.

- 2021: Strategic acquisition of a niche patient payment processing firm by a leading on-premise vendor, expanding revenue cycle capabilities.

- 2022: Development and launch of advanced patient identification verification modules, reducing registration errors by 20%.

- 2023: Integration of IoT capabilities for real-time patient tracking within large hospital campuses.

- 2024: Significant advancements in data analytics for predicting patient no-shows, leading to a 10% reduction in wasted appointment slots.

In-Depth On Premise Patient Access Solution Market Outlook

- 2019: Introduction of enhanced AI-driven appointment scheduling algorithms, improving resource allocation by 15%.

- 2020: Major security patches released to counter emerging ransomware threats, reinforcing on-premise data protection.

- 2021: Strategic acquisition of a niche patient payment processing firm by a leading on-premise vendor, expanding revenue cycle capabilities.

- 2022: Development and launch of advanced patient identification verification modules, reducing registration errors by 20%.

- 2023: Integration of IoT capabilities for real-time patient tracking within large hospital campuses.

- 2024: Significant advancements in data analytics for predicting patient no-shows, leading to a 10% reduction in wasted appointment slots.

In-Depth On Premise Patient Access Solution Market Outlook

The future outlook for the on-premise patient access solution market remains strong, propelled by sustained demand for secure, controlled, and customizable healthcare IT infrastructure. Growth accelerators such as continued technological innovation in AI and predictive analytics, strategic partnerships that enhance system interoperability, and market expansion into emerging economies will drive significant expansion. The inherent advantages of on-premise solutions in data sovereignty and customization will continue to resonate with large healthcare enterprises and government bodies prioritizing security and tailored operational efficiency. The market is poised for steady growth, with an estimated market size reaching approximately 850 million units by 2033, driven by the ongoing need for robust patient access management in an increasingly complex healthcare landscape. Strategic opportunities will emerge from the integration of these solutions with evolving digital health platforms and the continuous pursuit of enhanced patient experiences.

On Premise Patient Access Solution Segmentation

-

1. Application

- 1.1. Nursing Home

- 1.2. Inspection Center

-

2. Type

- 2.1. Medical Hardware

- 2.2. Medical Software

On Premise Patient Access Solution Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

On Premise Patient Access Solution REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XXX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global On Premise Patient Access Solution Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Nursing Home

- 5.1.2. Inspection Center

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Medical Hardware

- 5.2.2. Medical Software

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America On Premise Patient Access Solution Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Nursing Home

- 6.1.2. Inspection Center

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Medical Hardware

- 6.2.2. Medical Software

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America On Premise Patient Access Solution Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Nursing Home

- 7.1.2. Inspection Center

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Medical Hardware

- 7.2.2. Medical Software

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe On Premise Patient Access Solution Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Nursing Home

- 8.1.2. Inspection Center

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Medical Hardware

- 8.2.2. Medical Software

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa On Premise Patient Access Solution Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Nursing Home

- 9.1.2. Inspection Center

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Medical Hardware

- 9.2.2. Medical Software

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific On Premise Patient Access Solution Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Nursing Home

- 10.1.2. Inspection Center

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Medical Hardware

- 10.2.2. Medical Software

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Cerner Corporation

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 McKesson Corporation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Experian Plc

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Cognizant

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Conifer Health Solutions

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Waystar

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 3M

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Epic Systems Corporation

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 The SSI Group

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Cirius Group

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Optum

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Craneware

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Allscripts Healthcare Solutions

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Genentech

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Winning Health Technology Group Co.Ltd

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Sichuan Jiuyuan Yinhai Software Co.Ltd

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 DHC Software Co.Ltd

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Heren Health Co. Ltd

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Yidu Tech Inc

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Honghua International Medical Holdings Limited

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Andon Health Co.Ltd

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.1 Cerner Corporation

List of Figures

- Figure 1: Global On Premise Patient Access Solution Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America On Premise Patient Access Solution Revenue (million), by Application 2024 & 2032

- Figure 3: North America On Premise Patient Access Solution Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America On Premise Patient Access Solution Revenue (million), by Type 2024 & 2032

- Figure 5: North America On Premise Patient Access Solution Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America On Premise Patient Access Solution Revenue (million), by Country 2024 & 2032

- Figure 7: North America On Premise Patient Access Solution Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America On Premise Patient Access Solution Revenue (million), by Application 2024 & 2032

- Figure 9: South America On Premise Patient Access Solution Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America On Premise Patient Access Solution Revenue (million), by Type 2024 & 2032

- Figure 11: South America On Premise Patient Access Solution Revenue Share (%), by Type 2024 & 2032

- Figure 12: South America On Premise Patient Access Solution Revenue (million), by Country 2024 & 2032

- Figure 13: South America On Premise Patient Access Solution Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe On Premise Patient Access Solution Revenue (million), by Application 2024 & 2032

- Figure 15: Europe On Premise Patient Access Solution Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe On Premise Patient Access Solution Revenue (million), by Type 2024 & 2032

- Figure 17: Europe On Premise Patient Access Solution Revenue Share (%), by Type 2024 & 2032

- Figure 18: Europe On Premise Patient Access Solution Revenue (million), by Country 2024 & 2032

- Figure 19: Europe On Premise Patient Access Solution Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa On Premise Patient Access Solution Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa On Premise Patient Access Solution Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa On Premise Patient Access Solution Revenue (million), by Type 2024 & 2032

- Figure 23: Middle East & Africa On Premise Patient Access Solution Revenue Share (%), by Type 2024 & 2032

- Figure 24: Middle East & Africa On Premise Patient Access Solution Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa On Premise Patient Access Solution Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific On Premise Patient Access Solution Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific On Premise Patient Access Solution Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific On Premise Patient Access Solution Revenue (million), by Type 2024 & 2032

- Figure 29: Asia Pacific On Premise Patient Access Solution Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific On Premise Patient Access Solution Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific On Premise Patient Access Solution Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global On Premise Patient Access Solution Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global On Premise Patient Access Solution Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global On Premise Patient Access Solution Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global On Premise Patient Access Solution Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global On Premise Patient Access Solution Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global On Premise Patient Access Solution Revenue million Forecast, by Type 2019 & 2032

- Table 7: Global On Premise Patient Access Solution Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global On Premise Patient Access Solution Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global On Premise Patient Access Solution Revenue million Forecast, by Type 2019 & 2032

- Table 13: Global On Premise Patient Access Solution Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global On Premise Patient Access Solution Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global On Premise Patient Access Solution Revenue million Forecast, by Type 2019 & 2032

- Table 19: Global On Premise Patient Access Solution Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global On Premise Patient Access Solution Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global On Premise Patient Access Solution Revenue million Forecast, by Type 2019 & 2032

- Table 31: Global On Premise Patient Access Solution Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global On Premise Patient Access Solution Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global On Premise Patient Access Solution Revenue million Forecast, by Type 2019 & 2032

- Table 40: Global On Premise Patient Access Solution Revenue million Forecast, by Country 2019 & 2032

- Table 41: China On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific On Premise Patient Access Solution Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the On Premise Patient Access Solution?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the On Premise Patient Access Solution?

Key companies in the market include Cerner Corporation, McKesson Corporation, Experian Plc, Cognizant, Conifer Health Solutions, Waystar, 3M, Epic Systems Corporation, The SSI Group, Cirius Group, Optum, Craneware, Allscripts Healthcare Solutions, Genentech, Winning Health Technology Group Co.,Ltd, Sichuan Jiuyuan Yinhai Software Co.,Ltd, DHC Software Co.,Ltd, Heren Health Co., Ltd, Yidu Tech Inc, Honghua International Medical Holdings Limited, Andon Health Co.,Ltd.

3. What are the main segments of the On Premise Patient Access Solution?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "On Premise Patient Access Solution," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the On Premise Patient Access Solution report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the On Premise Patient Access Solution?

To stay informed about further developments, trends, and reports in the On Premise Patient Access Solution, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence