Key Insights

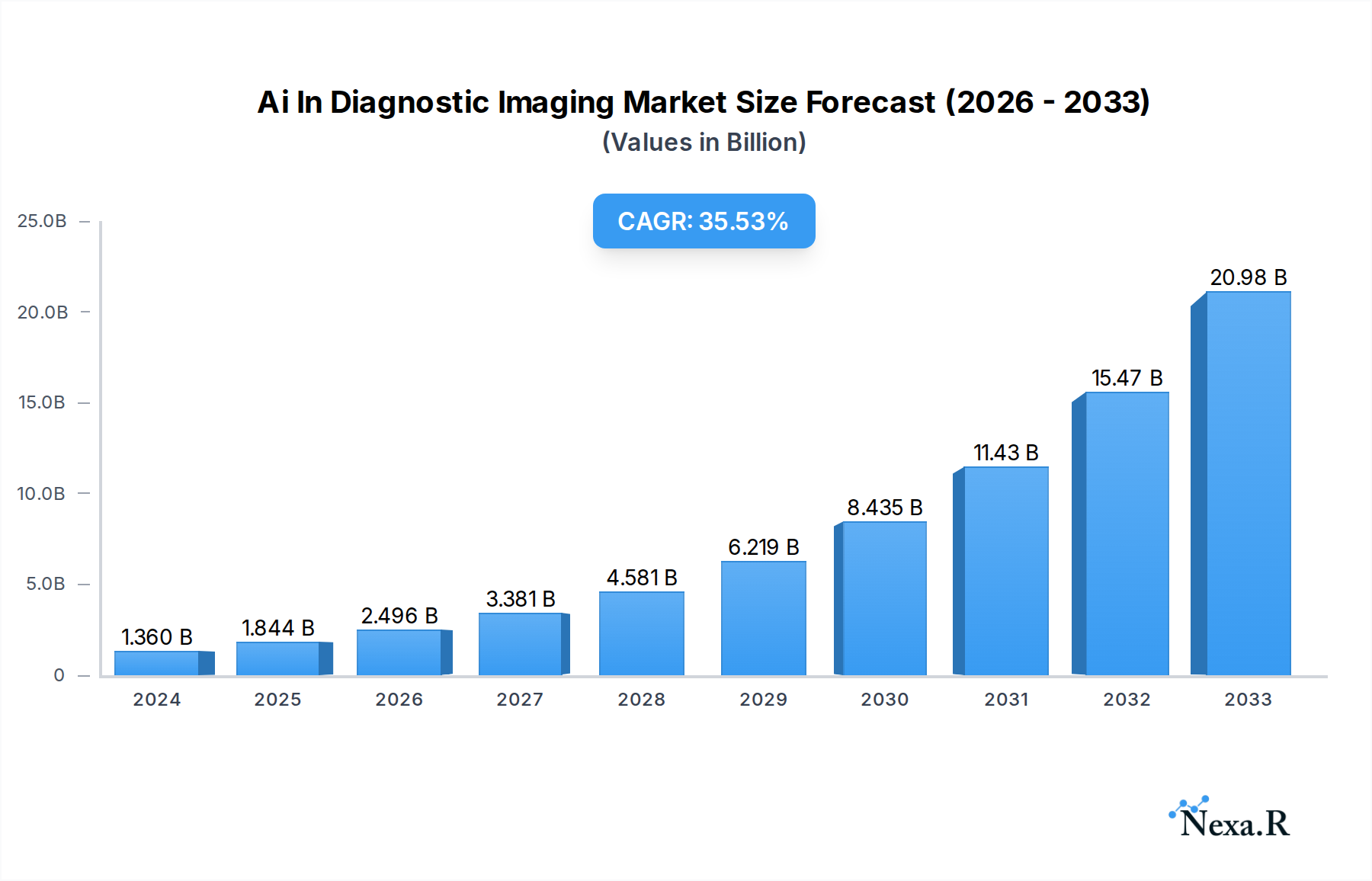

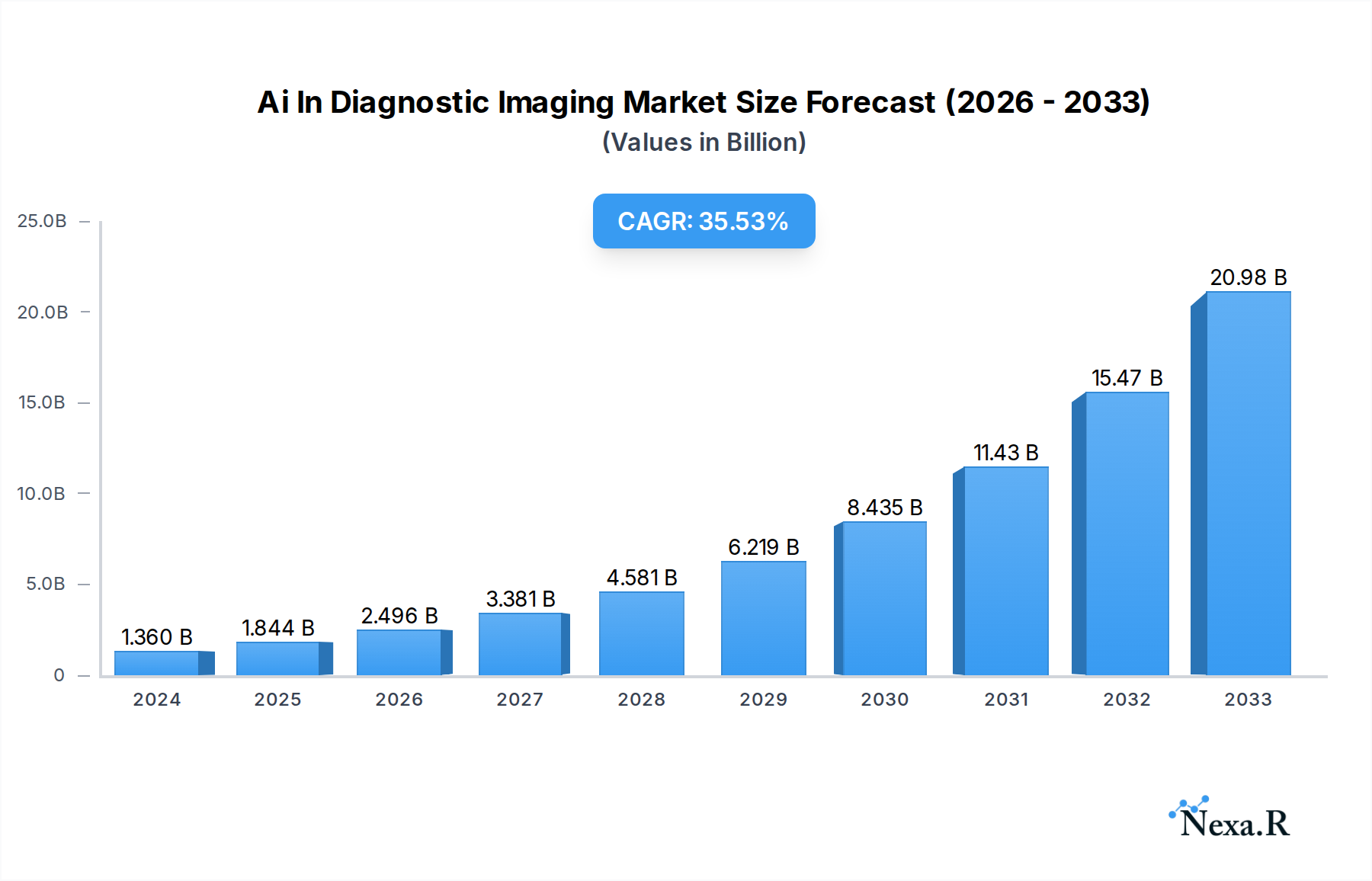

The AI in Diagnostic Imaging market is poised for exceptional growth, with an estimated market size of $1.36 billion in 2024. This rapid expansion is driven by several critical factors, including the increasing demand for faster and more accurate diagnostic interpretations, the burgeoning volume of medical imaging data, and the continuous advancements in artificial intelligence and machine learning algorithms. The integration of AI is revolutionizing how medical images are analyzed, leading to earlier disease detection, improved treatment planning, and enhanced patient outcomes. Key applications are emerging across hospitals, ambulatory surgical centers, and diagnostic centers, highlighting the pervasive impact of this technology. The market is also seeing significant innovation in its core components, with substantial growth expected in software and services alongside the hardware advancements. This dynamic landscape is attracting major players like GE Healthcare, Siemens Healthineers, and Koninklijke Philips N.V., alongside pioneering AI-focused companies, all vying to shape the future of medical imaging.

Ai In Diagnostic Imaging Market Size (In Billion)

Projected to experience a robust CAGR of 34.67%, the AI in Diagnostic Imaging market is anticipated to reach significant valuations by 2033. This remarkable growth trajectory is fueled by the urgent need to address radiologist shortages, optimize workflow efficiency, and reduce diagnostic errors. The growing adoption of AI-powered solutions for tasks such as image segmentation, anomaly detection, and quantitative analysis is a testament to their value proposition. Despite challenges like regulatory hurdles and the need for extensive data validation, the compelling benefits of AI in improving diagnostic speed, accuracy, and accessibility are outweighing these restraints. Geographically, North America and Europe are leading the adoption, but the Asia Pacific region, with its large patient populations and increasing healthcare investments, is emerging as a significant growth frontier. The ongoing research and development, coupled with strategic collaborations between technology firms and healthcare providers, are expected to further accelerate market penetration and unlock new application areas for AI in diagnostic imaging.

Ai In Diagnostic Imaging Company Market Share

This comprehensive report delves into the dynamic AI in Diagnostic Imaging market, providing a deep dive into market dynamics, growth trends, regional dominance, product innovations, key drivers, emerging opportunities, and the landscape of leading players. Designed to equip industry professionals, investors, and researchers with actionable insights, this analysis leverages high-traffic keywords and a structured format to maximize visibility and deliver critical information. We examine the market's trajectory from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, offering a detailed understanding of its evolution and future potential. This report also incorporates parent and child market analyses to provide a holistic view of market interconnectedness.

AI In Diagnostic Imaging Market Dynamics & Structure

The AI in Diagnostic Imaging market is characterized by a moderate to high concentration, driven by significant investments from established players like GE Healthcare, Siemens Healthineers, and Koninklijke Philips N.V., who are increasingly integrating AI capabilities into their imaging hardware and software. Technological innovation is a primary driver, with advancements in deep learning algorithms and machine learning continuously improving image analysis, detection accuracy, and workflow efficiency. Regulatory frameworks, though evolving, are a critical consideration, with bodies like the FDA actively developing guidelines for AI-driven medical devices to ensure safety and efficacy. Competitive product substitutes are emerging, particularly in software solutions that offer AI-powered analysis for existing imaging equipment, posing a challenge to purely hardware-centric strategies. End-user demographics are shifting towards a greater demand for faster, more accurate diagnoses and personalized treatment plans, pushing the adoption of AI. Mergers and acquisitions (M&A) are a significant trend, with larger companies acquiring innovative AI startups to bolster their portfolios and expand their market reach. For instance, numerous smaller AI imaging analytics firms have been acquired by major medical technology giants in the past five years, with an estimated 40 M&A deals in the AI in healthcare diagnostics space between 2019-2024, valued at over $5 billion.

- Market Concentration: Dominated by a few key players, with a growing number of specialized AI firms.

- Technological Innovation: Driven by deep learning, natural language processing, and advanced algorithms for image interpretation.

- Regulatory Frameworks: Increasing scrutiny and evolving guidelines from health authorities globally.

- Competitive Landscape: Intense competition between integrated solutions and standalone AI software.

- End-User Demand: Growing preference for AI-enhanced diagnostic speed and precision.

- M&A Activity: Strategic acquisitions are shaping the market landscape and consolidating technological capabilities.

AI In Diagnostic Imaging Growth Trends & Insights

The AI in Diagnostic Imaging market is experiencing exponential growth, projected to reach an estimated $65.5 billion by 2025, with a significant CAGR of 32.7% during the forecast period of 2025–2033. This robust expansion is fueled by a paradigm shift in healthcare towards proactive, efficient, and precise diagnostics. The increasing volume of medical imaging data, coupled with the growing need for early disease detection and personalized medicine, is creating immense demand for AI-powered solutions. Adoption rates are accelerating across hospitals, diagnostic centers, and ambulatory surgical centers, as healthcare providers recognize the potential of AI to improve diagnostic accuracy, reduce radiologist workload, and optimize patient outcomes. Technological disruptions, including the development of more sophisticated deep learning models capable of analyzing complex imaging modalities like MRI, CT, and X-rays with unprecedented speed and detail, are transforming the field. Consumer behavior is also evolving, with patients and physicians alike seeking the most advanced diagnostic tools available. The market's growth is not just about incremental improvements; it's about a fundamental reimagining of the diagnostic process. The integration of AI into imaging workflows is moving beyond simple image enhancement to sophisticated anomaly detection, predictive analytics for disease progression, and even aiding in treatment planning. The child market for AI in radiology AI software alone is expected to grow by a CAGR of 35.2% during the study period. This pervasive integration is supported by advancements in cloud computing and edge AI, making these powerful tools more accessible and scalable. The growing emphasis on value-based healthcare is also a key factor, as AI solutions can demonstrably improve efficiency and reduce costs associated with misdiagnosis and delayed treatment, contributing to a healthier global population and a more sustainable healthcare system.

Dominant Regions, Countries, or Segments in AI In Diagnostic Imaging

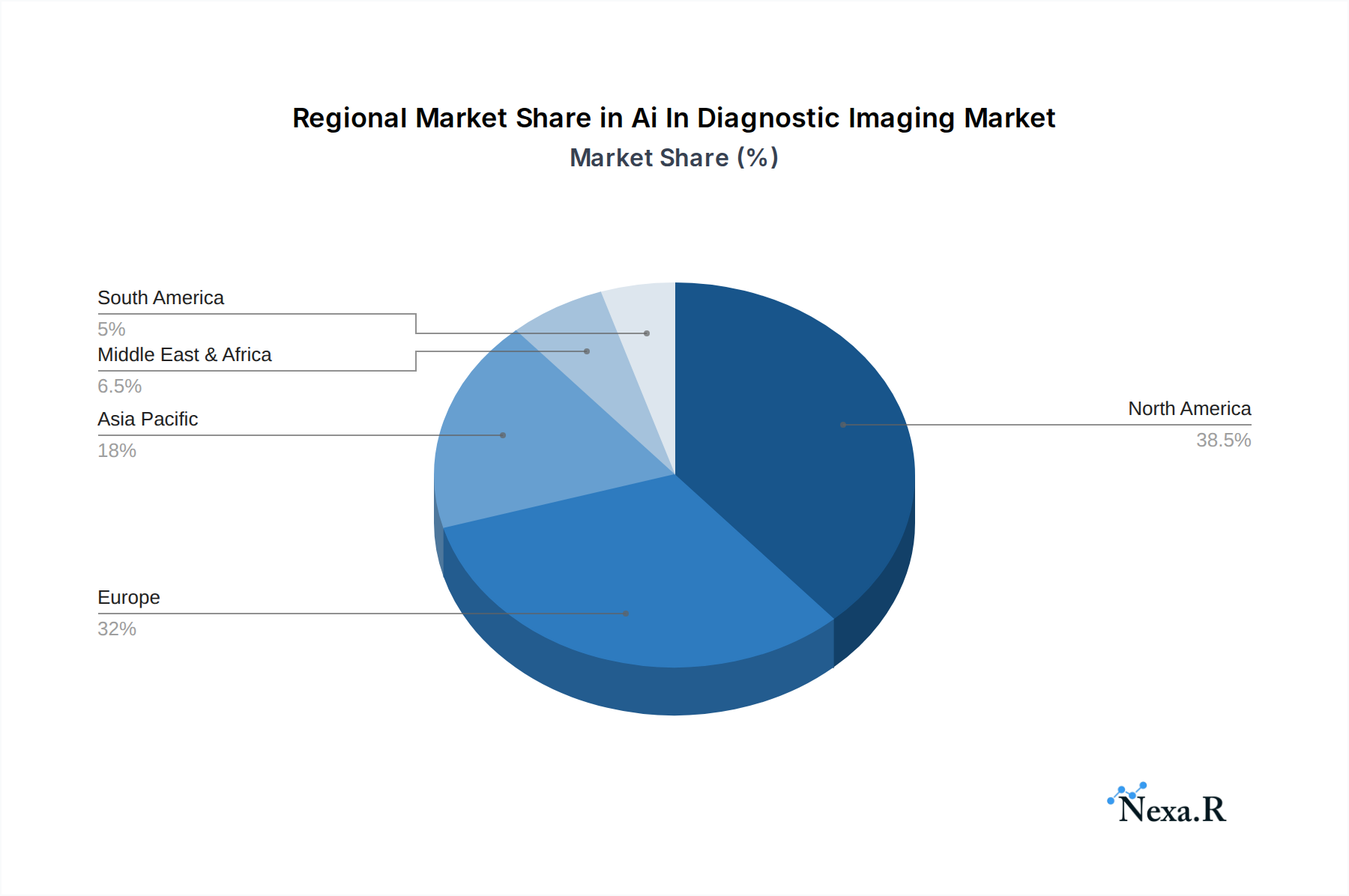

North America currently stands as the dominant region in the AI in Diagnostic Imaging market, driven by significant investment in healthcare IT, a well-established regulatory framework that fosters innovation, and a high adoption rate of advanced medical technologies. The United States, in particular, accounts for a substantial portion of the market share, estimated at 45% of the global market in 2025, due to its robust research and development ecosystem and the presence of leading AI and healthcare companies. This dominance is further bolstered by strong government initiatives promoting digital health and precision medicine.

Within the Application segment, Hospitals represent the largest market, accounting for an estimated 58% of the total market value in 2025. This is attributable to the high volume of diagnostic imaging procedures performed in hospital settings and the availability of infrastructure to support AI integration. The child market of AI in Hospital imaging alone is projected to reach $38.3 billion by 2025.

In terms of Type, Software holds the leading position, projected to capture 55% of the market share in 2025. This is driven by the growing demand for AI-powered algorithms for image analysis, workflow optimization, and data management, which can be retrofitted into existing imaging hardware. The software segment's growth is outpacing hardware and services due to its flexibility and cost-effectiveness.

- North America: Leading region due to strong R&D, regulatory support, and high technology adoption.

- United States: Largest market share, driven by advanced healthcare infrastructure and innovation.

- Canada: Growing adoption, supported by government initiatives in digital health.

- Application Segment Dominance:

- Hospitals: Primary adopters due to high procedure volumes and infrastructure.

- Drivers: Need for enhanced diagnostic accuracy, workflow efficiency, and early disease detection.

- Hospitals: Primary adopters due to high procedure volumes and infrastructure.

- Type Segment Dominance:

- Software: Leading segment due to versatility, scalability, and integration capabilities.

- Drivers: Cost-effectiveness, ability to enhance existing hardware, and rapid algorithm development.

- Software: Leading segment due to versatility, scalability, and integration capabilities.

AI In Diagnostic Imaging Product Landscape

The AI in Diagnostic Imaging product landscape is rapidly evolving, characterized by sophisticated algorithms that enhance image quality, automate analysis, and improve diagnostic speed. Innovations range from AI-powered tools that detect subtle anomalies in X-rays and CT scans, such as early signs of lung nodules or fractures, to deep learning models that aid in the segmentation of tumors and organs in MRI images for more precise treatment planning. Performance metrics are continually improving, with AI systems demonstrating comparable or even superior accuracy to human radiologists in specific tasks, while significantly reducing interpretation time. Unique selling propositions often lie in the seamless integration of these AI solutions into existing PACS and EMR systems, offering a user-friendly experience for healthcare professionals. Technological advancements are also focusing on explainable AI (XAI) to build trust and transparency in clinical decision-making.

Key Drivers, Barriers & Challenges in AI In Diagnostic Imaging

Key Drivers: The AI in Diagnostic Imaging market is propelled by several critical factors. The increasing volume of medical imaging data generated globally necessitates efficient analytical tools. Advancements in AI algorithms, particularly deep learning, are enabling more accurate and faster diagnoses. The growing demand for early disease detection and personalized medicine is a significant catalyst, as AI can identify subtle patterns indicative of disease at its nascent stages. Furthermore, the need to improve workflow efficiency and reduce radiologist burnout by automating repetitive tasks is a major driver.

Barriers & Challenges: Despite its promise, the market faces significant challenges. High implementation costs for AI systems and the necessary IT infrastructure can be a barrier, especially for smaller healthcare facilities. Data privacy and security concerns surrounding sensitive patient information are paramount and require robust solutions. Regulatory hurdles and the lengthy approval processes for AI-based medical devices can slow down market entry. The lack of standardization in AI algorithms and data formats can hinder interoperability. Additionally, clinician adoption and trust in AI-powered diagnostic tools require ongoing education and validation to overcome resistance to change and ensure confidence in AI-driven recommendations, which can sometimes impact supply chain stability due to component sourcing complexities.

Emerging Opportunities in AI In Diagnostic Imaging

Emerging opportunities in AI in Diagnostic Imaging lie in the expansion into underserved markets and the development of predictive AI models for population health management. The increasing demand for AI-powered tools for remote diagnostics and telemedicine presents a significant growth avenue, particularly in rural or resource-limited regions. Furthermore, the integration of AI with other emerging technologies like augmented reality (AR) and virtual reality (VR) for surgical planning and medical training offers novel applications. The development of AI solutions for novel imaging modalities and rare disease detection also represents a significant untapped potential.

Growth Accelerators in the AI In Diagnostic Imaging Industry

The long-term growth of the AI in Diagnostic Imaging industry is significantly accelerated by breakthroughs in deep learning architectures and neural networks, leading to more sophisticated and accurate diagnostic capabilities. Strategic partnerships and collaborations between AI technology providers, medical device manufacturers, and healthcare institutions are crucial for co-developing and deploying innovative solutions that meet clinical needs. Government initiatives and funding for digital health and AI research are also playing a vital role in fostering innovation and market expansion. The growing body of evidence from successful clinical trials and real-world implementations demonstrating improved patient outcomes and cost-effectiveness is further building confidence and driving wider adoption.

Key Players Shaping the AI In Diagnostic Imaging Market

- GE Healthcare

- Canon

- Siemens Healthineers

- Subtle Medical

- DeepMind

- Samsung Healthcare

- Koninklijke Philips N.V.

- Butterfly Network

Notable Milestones in AI In Diagnostic Imaging Sector

- 2019: FDA approves the first AI-powered software for stroke detection in CT scans.

- 2020: DeepMind's AI demonstrates human-level performance in detecting breast cancer from mammograms.

- 2021: GE Healthcare launches its AI-powered radiomics solution for oncology.

- 2022: Subtle Medical receives FDA clearance for its AI-powered image enhancement technology.

- 2023: Siemens Healthineers announces expansion of its AI-Rad Companion portfolio for various imaging applications.

- 2024: Butterfly Network expands its AI capabilities for point-of-care ultrasound diagnostics.

In-Depth AI In Diagnostic Imaging Market Outlook

The AI in Diagnostic Imaging market outlook is exceptionally positive, with sustained high growth anticipated. Key growth accelerators include continuous advancements in AI algorithms, increasing healthcare digitization, and a global push towards value-based care. Strategic partnerships between AI innovators and established medical technology giants will further fuel market expansion and product development. The increasing adoption of AI for predictive diagnostics and population health management presents a significant long-term opportunity, promising to revolutionize preventative healthcare. The market is poised for transformative growth, driven by its potential to enhance diagnostic accuracy, improve patient outcomes, and optimize healthcare resource allocation, solidifying its indispensable role in the future of medicine.

Ai In Diagnostic Imaging Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Ambulatory Surgical Centers

- 1.3. Diagnostic Centers

- 1.4. Others

-

2. Type

- 2.1. Hardware

- 2.2. Software

- 2.3. Services

Ai In Diagnostic Imaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ai In Diagnostic Imaging Regional Market Share

Geographic Coverage of Ai In Diagnostic Imaging

Ai In Diagnostic Imaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 34.67% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Ambulatory Surgical Centers

- 5.1.3. Diagnostic Centers

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Hardware

- 5.2.2. Software

- 5.2.3. Services

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Ai In Diagnostic Imaging Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. Ambulatory Surgical Centers

- 6.1.3. Diagnostic Centers

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Hardware

- 6.2.2. Software

- 6.2.3. Services

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Ai In Diagnostic Imaging Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. Ambulatory Surgical Centers

- 7.1.3. Diagnostic Centers

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Hardware

- 7.2.2. Software

- 7.2.3. Services

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Ai In Diagnostic Imaging Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. Ambulatory Surgical Centers

- 8.1.3. Diagnostic Centers

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Hardware

- 8.2.2. Software

- 8.2.3. Services

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Ai In Diagnostic Imaging Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. Ambulatory Surgical Centers

- 9.1.3. Diagnostic Centers

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Hardware

- 9.2.2. Software

- 9.2.3. Services

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Ai In Diagnostic Imaging Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. Ambulatory Surgical Centers

- 10.1.3. Diagnostic Centers

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Hardware

- 10.2.2. Software

- 10.2.3. Services

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Ai In Diagnostic Imaging Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospitals

- 11.1.2. Ambulatory Surgical Centers

- 11.1.3. Diagnostic Centers

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Hardware

- 11.2.2. Software

- 11.2.3. Services

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 GE Healthcare

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Canon

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Siemens Healthineers

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Subtle Medical

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 DeepMind

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Samsung Healthcare

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Koninklijke Philips N.V.

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Butterfly Network

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.1 GE Healthcare

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Ai In Diagnostic Imaging Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Ai In Diagnostic Imaging Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Ai In Diagnostic Imaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Ai In Diagnostic Imaging Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Ai In Diagnostic Imaging Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Ai In Diagnostic Imaging Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Ai In Diagnostic Imaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Ai In Diagnostic Imaging Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Ai In Diagnostic Imaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Ai In Diagnostic Imaging Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Ai In Diagnostic Imaging Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Ai In Diagnostic Imaging Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Ai In Diagnostic Imaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Ai In Diagnostic Imaging Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Ai In Diagnostic Imaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Ai In Diagnostic Imaging Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Ai In Diagnostic Imaging Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Ai In Diagnostic Imaging Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Ai In Diagnostic Imaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Ai In Diagnostic Imaging Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Ai In Diagnostic Imaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Ai In Diagnostic Imaging Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Ai In Diagnostic Imaging Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Ai In Diagnostic Imaging Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Ai In Diagnostic Imaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Ai In Diagnostic Imaging Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Ai In Diagnostic Imaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Ai In Diagnostic Imaging Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Ai In Diagnostic Imaging Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Ai In Diagnostic Imaging Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Ai In Diagnostic Imaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Ai In Diagnostic Imaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Ai In Diagnostic Imaging Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ai In Diagnostic Imaging?

The projected CAGR is approximately 34.67%.

2. Which companies are prominent players in the Ai In Diagnostic Imaging?

Key companies in the market include GE Healthcare, Canon, Siemens Healthineers, Subtle Medical, DeepMind, Samsung Healthcare, Koninklijke Philips N.V., Butterfly Network.

3. What are the main segments of the Ai In Diagnostic Imaging?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ai In Diagnostic Imaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ai In Diagnostic Imaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ai In Diagnostic Imaging?

To stay informed about further developments, trends, and reports in the Ai In Diagnostic Imaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence