Key Insights

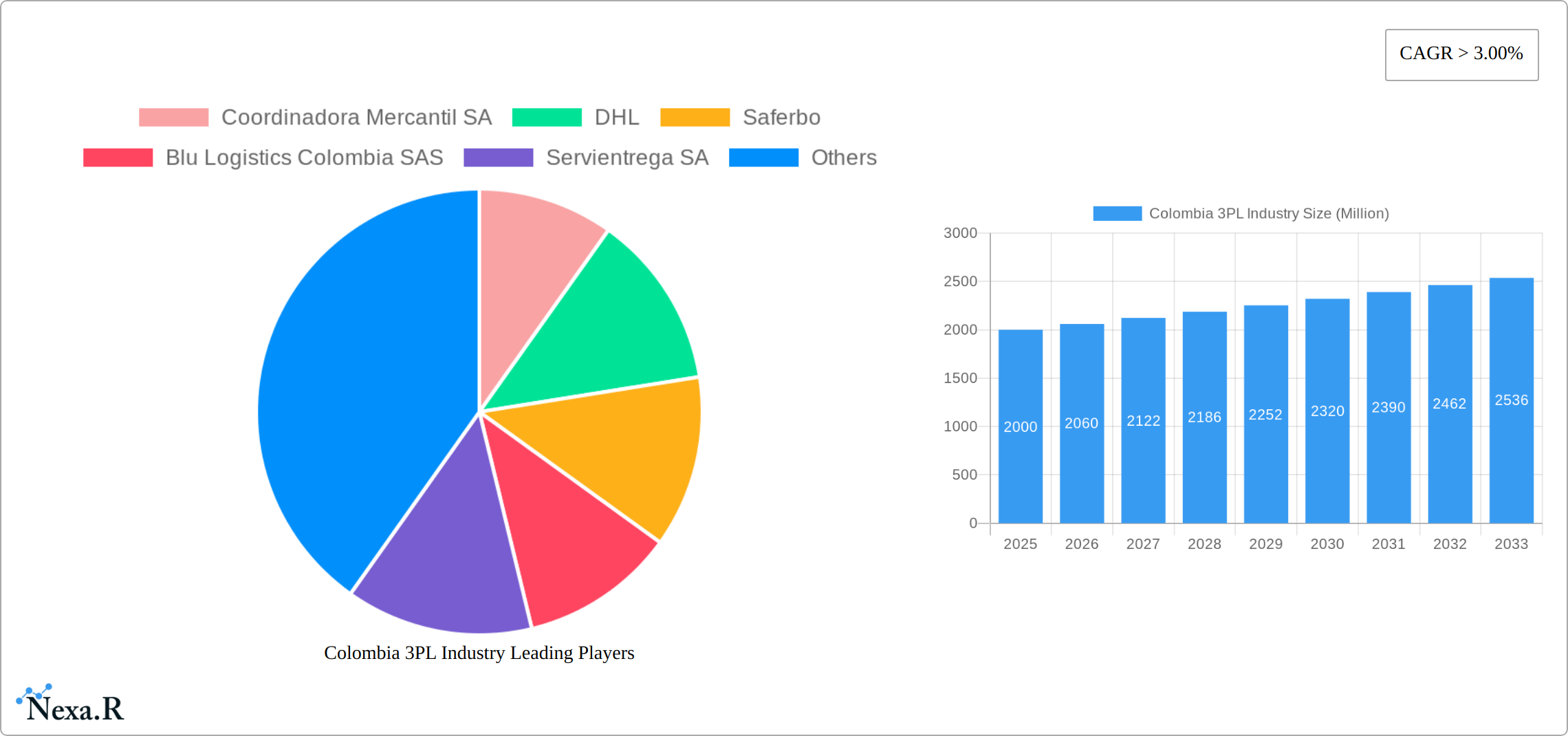

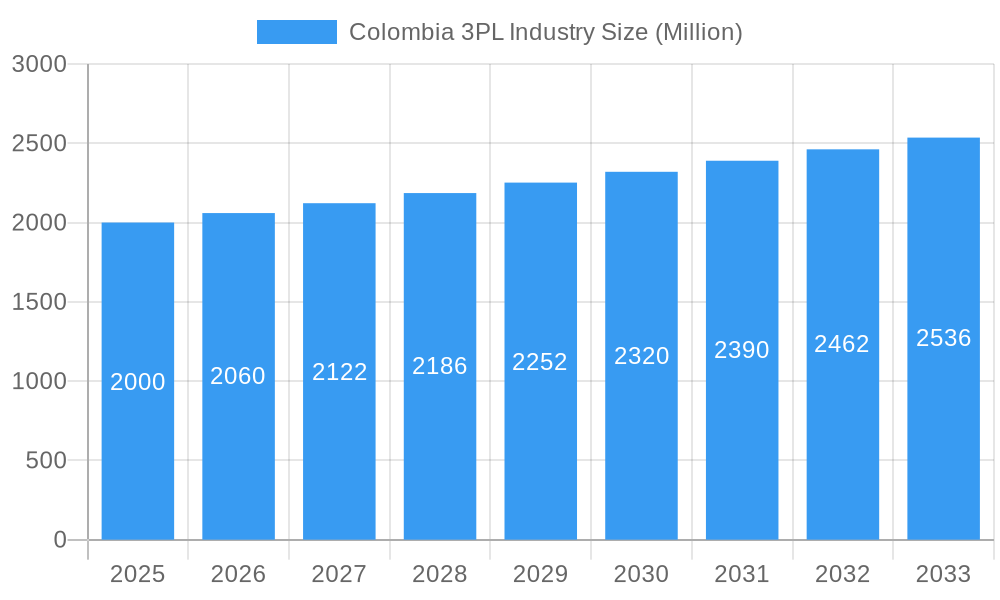

The Colombian Third-Party Logistics (3PL) market is experiencing significant expansion, driven by e-commerce growth, intricate supply chains, and the escalating demand for efficient logistics across industries. The market, estimated at $1.27 billion in 2025, is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.1% through 2033. Key drivers include the robust FMCG sector, particularly in beauty, personal care, beverages, and home care, alongside the thriving retail and e-commerce sectors. The automotive industry's complex logistics requirements also contribute substantially to market demand. Furthermore, the growing need for refrigerated transportation for perishable goods such as fruits, vegetables, pharmaceuticals, meat, and seafood represents a significant emerging segment.

Colombia 3PL Industry Market Size (In Billion)

Established global and local 3PL providers are actively competing within this dynamic Colombian market. While infrastructure limitations and regulatory complexities present challenges, the overall growth trajectory remains highly positive.

Colombia 3PL Industry Company Market Share

Segmentation analysis reveals that domestic transportation management dominates, with international transportation management showing rapid growth due to increasing global trade. Value-added warehousing and distribution services are becoming indispensable, especially for e-commerce and FMCG businesses. While automotive, FMCG, and retail are major end-users, the technology sector (consumer electronics, home appliances) is an emerging segment with rising logistics demands. The specialized refrigerated ("reefer") segment is anticipated for strong growth, reflecting increased demand for efficient cold chain solutions. Future market expansion hinges on addressing infrastructure gaps, refining regulatory frameworks, and fostering logistics technology innovation. Continued e-commerce expansion and evolving consumer demand will be pivotal factors driving growth throughout the forecast period.

Colombia 3PL Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Colombia 3PL (Third-Party Logistics) industry, offering invaluable insights for industry professionals, investors, and strategic planners. Covering the period 2019-2033, with a focus on 2025, this report meticulously examines market dynamics, growth trends, key players, and emerging opportunities within this rapidly evolving sector. The report utilizes a robust methodology incorporating both qualitative and quantitative data to deliver actionable intelligence.

Colombia 3PL Industry Market Dynamics & Structure

The Colombian Third-Party Logistics (3PL) market is characterized by a moderately consolidated structure, projecting a valuation of approximately [Insert specific value here] Million in 2025. Prominent players such as Coordinadora Mercantil SA, DHL, and Servientrega SA command substantial market share. However, the landscape is also enriched by the presence of numerous smaller, highly specialized firms that contribute significantly to the industry's overall dynamism. A pivotal force driving market evolution is technological innovation, with advancements in warehouse automation and sophisticated supply chain visibility software leading the charge. Conversely, the significant capital investment required for implementation and the ongoing need for a skilled workforce represent notable hurdles to widespread adoption. The regulatory environment in Colombia is in a state of continuous development, presenting both advantageous opportunities and strategic challenges that influence compliance expenses and the overall efficiency of operations. The industry navigates considerable competitive pressure from both established giants and agile new entrants, primarily fueled by aggressive price competition and the strategic differentiation of services. Merger and acquisition (M&A) activity remains a measured component of the market, with approximately [Insert number of deals here] transactions recorded between 2019 and 2024, predominantly geared towards expanding service portfolios and extending geographical reach.

- Market Concentration: The market exhibits moderate consolidation, with the top 5 players anticipated to hold around [Insert percentage here]% of the market share in 2025.

- Technological Innovation: A potent driver of growth, though high implementation costs present a significant barrier to entry and widespread adoption.

- Regulatory Framework: An evolving landscape that directly influences compliance costs and operational efficiency for all stakeholders.

- Competitive Substitutes: Increasing pressure is being exerted by nimble, smaller, and specialized 3PL providers offering niche solutions.

- M&A Activity: A moderate trend, with approximately [Insert number of deals here] deals observed between 2019 and 2024, largely motivated by strategic expansion objectives.

- End-User Demographics: Robust growth is being fueled by a diverse array of end-user sectors, prominently including Fast-Moving Consumer Goods (FMCG), retail, and the automotive industries.

Colombia 3PL Industry Growth Trends & Insights

The Colombian 3PL market has witnessed impressive growth during the historical period spanning 2019-2024, achieving a Compound Annual Growth Rate (CAGR) of [Insert CAGR percentage here]%. This impressive expansion is largely attributable to the burgeoning e-commerce sector, a strategic trend of businesses increasingly outsourcing their logistics functions, and tangible improvements in national infrastructure. Looking ahead to the forecast period of 2025-2033, continued robust expansion is anticipated. This upward trajectory will be propelled by factors such as escalating consumer spending, supportive government initiatives focused on enhancing logistics infrastructure, and the accelerating adoption of advanced technologies. Market penetration of 3PL services is projected to reach a significant [Insert penetration percentage here]% by 2033, underscoring considerable future growth potential. Technological disruptions, particularly the integration of Artificial Intelligence (AI) and blockchain technology, are poised to dramatically enhance operational efficiency and bolster supply chain transparency. Evolving consumer behaviors, exemplified by the surge in e-commerce and the demand for expedited delivery services, are further propelling the market's momentum. Moreover, the growing emphasis on environmental consciousness is driving increased adoption of sustainable logistics practices throughout the industry.

Dominant Regions, Countries, or Segments in Colombia 3PL Industry

The Bogota metropolitan area represents the dominant region within the Colombian 3PL market, driven by its concentration of businesses, advanced infrastructure, and proximity to major ports. Among service segments, value-added warehousing and distribution currently holds the largest market share (xx%), followed by domestic transportation management (xx%) and international transportation management (xx%). In terms of end-users, the FMCG sector, with its high volume and diverse logistical needs, emerges as the most significant driver, followed by retail and automotive. The Reefer segment is experiencing strong growth fueled by the export of perishable goods.

- Key Growth Drivers: Economic growth, increasing e-commerce penetration, infrastructure development, government support for logistics sector.

- Dominant Segments: Value-added warehousing and distribution, FMCG, and Bogota metropolitan area.

- Growth Potential: Significant potential in the Reefer segment and expansion into secondary cities.

Colombia 3PL Industry Product Landscape

The Colombian 3PL industry offers a comprehensive and diverse suite of products and services designed to meet the multifaceted needs of businesses. This portfolio includes robust domestic and international transportation management solutions, advanced warehousing capabilities encompassing specialized facilities for temperature-sensitive goods, and value-added services such as precise labeling and strategic packaging. Furthermore, the industry provides integrated supply chain solutions for end-to-end management. Recent technological advancements have catalyzed the introduction of cutting-edge Warehouse Management Systems (WMS), Transportation Management Systems (TMS), and real-time tracking functionalities. These innovations are instrumental in elevating operational efficiency, refining inventory management practices, and delivering unparalleled visibility across the entire supply chain. The key value propositions offered to clients include significant cost optimization, demonstrable improvements in efficiency, enhanced supply chain visibility, and guaranteed compliance with all relevant regulatory standards.

Key Drivers, Barriers & Challenges in Colombia 3PL Industry

Key Drivers: The sustained surge in the e-commerce sector, a growing demand for highly efficient and dependable logistics solutions, and proactive government initiatives aimed at modernizing the nation's infrastructure are the principal forces propelling market growth. The continuous evolution of technology, particularly in areas like automation and advanced data analytics, further accelerates industry progress.

Key Challenges: Persistent infrastructure limitations in specific regions, ongoing security concerns, and the inherent volatility of fuel prices present considerable operational challenges. Furthermore, the complexity of regulatory frameworks and a discernible shortage of skilled labor can impede operational efficiency and hinder growth. The intensely competitive landscape, populated by both established market leaders and dynamic emerging players, imposes significant pricing pressures and necessitates continuous innovation to maintain a competitive edge. The industry also remains susceptible to supply chain disruptions stemming from geopolitical events, adding an element of market volatility.

Emerging Opportunities in Colombia 3PL Industry

The growing e-commerce market presents substantial growth opportunities, with increasing demand for last-mile delivery solutions and fulfillment services. The expansion of the cold chain logistics sector, catering to the perishable goods industry, is another significant area of opportunity. Furthermore, the adoption of sustainable and environmentally friendly logistics practices offers a competitive advantage and aligns with growing consumer preferences.

Growth Accelerators in the Colombia 3PL Industry

Strategic alliances between 3PL providers and innovative technology companies are paramount for the seamless integration of cutting-edge solutions and the enhancement of operational efficiency. Substantial investments in advanced technologies, including Artificial Intelligence (AI) and blockchain, are critical for improving supply chain visibility and optimizing intricate logistical processes. Expanding service offerings into underserved geographical regions and diversifying the range of services provided are essential strategies for ensuring sustained long-term growth and market leadership.

Key Players Shaping the Colombia 3PL Industry Market

- Coordinadora Mercantil SA

- DHL

- Saferbo

- Blu Logistics Colombia SAS

- Servientrega SA

- EGA - KAT

- Kuehne + Nagel

- Icoltrans

- TCC SAS

- Almaviva

Notable Milestones in Colombia 3PL Industry Sector

- December 2022: CEVA Logistics opened a new carbon-neutral warehouse in Bogota, expanding its capacity and serving new automotive clients.

- December 2022: Leschaco acquired Coltrans S.A.S., strengthening its presence in the Colombian market.

In-Depth Colombia 3PL Industry Market Outlook

The Colombian 3PL market is poised for sustained growth, driven by a confluence of factors. Continued expansion of e-commerce, ongoing investments in infrastructure, and the increasing adoption of advanced technologies all contribute to a positive outlook. Strategic partnerships and a focus on sustainability will further enhance market competitiveness. The potential for market consolidation through M&A activity remains, offering both opportunities and challenges for existing and new players.

Colombia 3PL Industry Segmentation

-

1. Service

- 1.1. Domestic Transportation Management

- 1.2. International Transportation Management

- 1.3. Value-added Warehousing and Distribution

-

2. End User

- 2.1. Automotive

- 2.2. FMCG (Fa

- 2.3. Retail (

- 2.4. Fashion and Lifestyle (Apparel and Footwear)

- 2.5. Technolo

- 2.6. Reefer (

- 2.7. Other End Users

Colombia 3PL Industry Segmentation By Geography

- 1. Colombia

Colombia 3PL Industry Regional Market Share

Geographic Coverage of Colombia 3PL Industry

Colombia 3PL Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service

- 5.1.1. Domestic Transportation Management

- 5.1.2. International Transportation Management

- 5.1.3. Value-added Warehousing and Distribution

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Automotive

- 5.2.2. FMCG (Fa

- 5.2.3. Retail (

- 5.2.4. Fashion and Lifestyle (Apparel and Footwear)

- 5.2.5. Technolo

- 5.2.6. Reefer (

- 5.2.7. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Colombia

- 5.1. Market Analysis, Insights and Forecast - by Service

- 6. Colombia 3PL Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service

- 6.1.1. Domestic Transportation Management

- 6.1.2. International Transportation Management

- 6.1.3. Value-added Warehousing and Distribution

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Automotive

- 6.2.2. FMCG (Fa

- 6.2.3. Retail (

- 6.2.4. Fashion and Lifestyle (Apparel and Footwear)

- 6.2.5. Technolo

- 6.2.6. Reefer (

- 6.2.7. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Service

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Coordinadora Mercantil SA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 DHL

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Saferbo

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Blu Logistics Colombia SAS

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Servientrega SA

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 EGA - KAT**List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Kuehne + Nagel

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Icoltrans

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 TCC SAS

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Almaviva

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Coordinadora Mercantil SA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Colombia 3PL Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Colombia 3PL Industry Share (%) by Company 2025

List of Tables

- Table 1: Colombia 3PL Industry Revenue billion Forecast, by Service 2020 & 2033

- Table 2: Colombia 3PL Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 3: Colombia 3PL Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Colombia 3PL Industry Revenue billion Forecast, by Service 2020 & 2033

- Table 5: Colombia 3PL Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Colombia 3PL Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Colombia 3PL Industry?

The projected CAGR is approximately 8.1%.

2. Which companies are prominent players in the Colombia 3PL Industry?

Key companies in the market include Coordinadora Mercantil SA, DHL, Saferbo, Blu Logistics Colombia SAS, Servientrega SA, EGA - KAT**List Not Exhaustive, Kuehne + Nagel, Icoltrans, TCC SAS, Almaviva.

3. What are the main segments of the Colombia 3PL Industry?

The market segments include Service, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.27 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Events in E-commerce Sector; Increasing Demand for Qualified Event Logistics Services.

6. What are the notable trends driving market growth?

Colombia Third-party Logistics (3PL) Market Trends.

7. Are there any restraints impacting market growth?

High Labour Cost; High Pricing.

8. Can you provide examples of recent developments in the market?

December 2022: CEVA Logistics opened a new multi-client, 15,000-square-meter warehouse in Bogota, Colombia, allowing the company to better serve the strategic growth needs of its customers in South and Latin America. The new facility is the first carbon-neutral CEVA warehouse in the country and consolidates the operations of three other former sites in Colombia, while also adding space for new customers. The Bogota facility will serve existing technology, industrial and automotive clients, who have shifted from other CEVA operations in Colombia. The new warehouse also serves several new customers, including a new automaker, whose spare parts operation will occupy roughly one-third of the total space. In addition to its sustainability measures, the Bogota warehouse will employ advanced security measures, as well as leading-edge software, workflow, and picking and sorting technologies. The facility also positions CEVA for future growth in a thriving region.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Colombia 3PL Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Colombia 3PL Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Colombia 3PL Industry?

To stay informed about further developments, trends, and reports in the Colombia 3PL Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence