Key Insights

The global Cyber Range market is poised for significant expansion, projected to reach a substantial market size with a robust Compound Annual Growth Rate (CAGR) of 9%. This dynamic growth is fueled by an escalating need for advanced cybersecurity training and realistic simulation environments. Organizations across various sectors are increasingly investing in cyber ranges to equip their workforces with the skills to detect, prevent, and respond to sophisticated cyber threats. The market is witnessing a surge in demand for both cloud-based and on-premise solutions, with hybrid models gaining traction as they offer flexibility and scalability to meet diverse organizational requirements. Key drivers include the rising complexity of cyber-attacks, stringent regulatory compliance mandates, and the growing adoption of IoT and cloud technologies, which inherently expand the attack surface. The continuous evolution of cyber threat landscapes necessitates perpetual learning and skill development, making cyber ranges indispensable tools for cybersecurity preparedness.

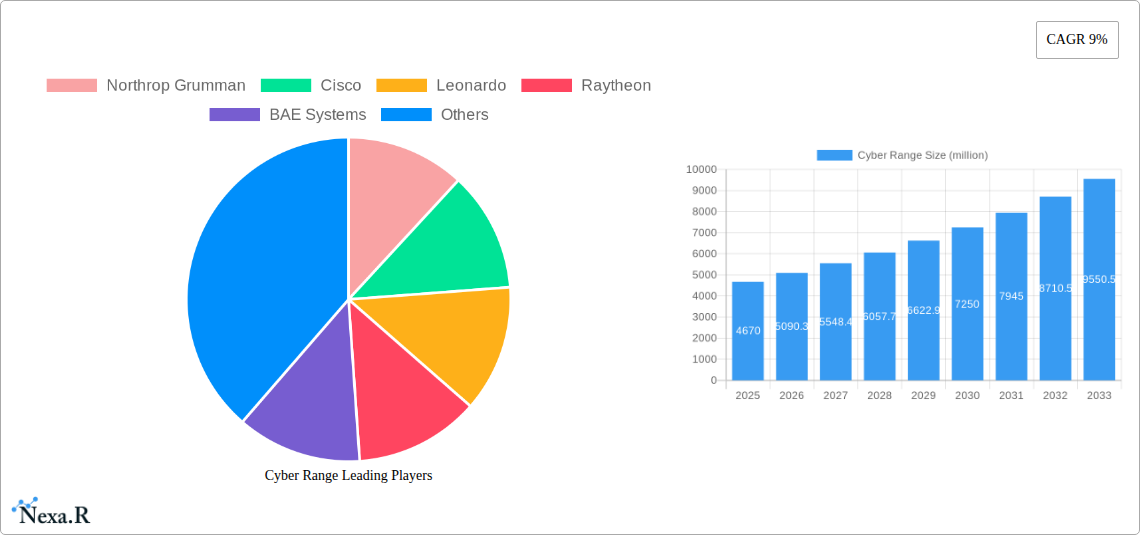

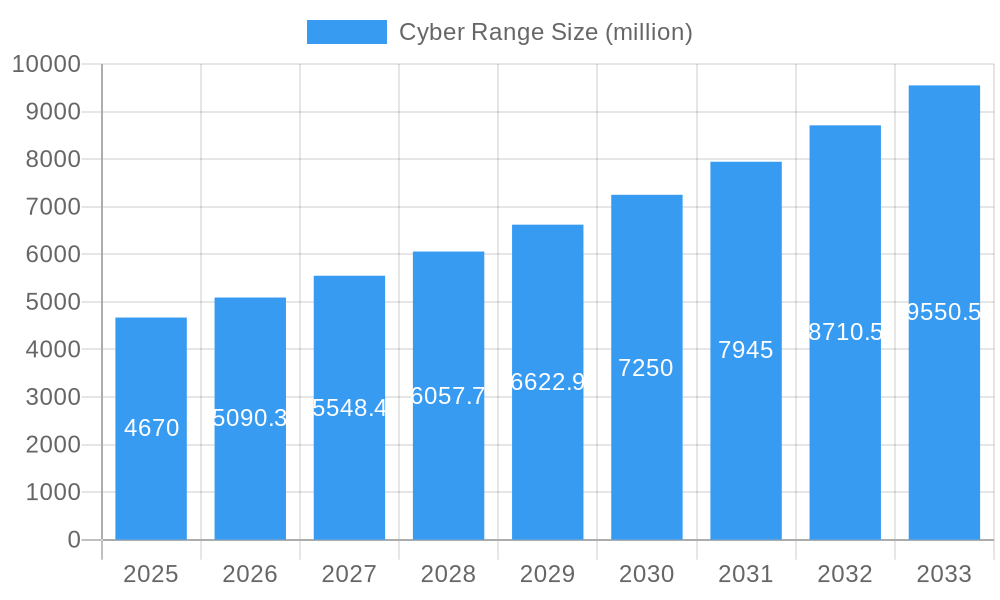

Cyber Range Market Size (In Billion)

The market is segmented by application into Training Purpose and Network Testing, with the former expected to dominate due to the heightened focus on upskilling cybersecurity professionals. Geographically, North America and Europe are anticipated to lead the market, driven by established cybersecurity infrastructure and a high concentration of key industry players. However, the Asia Pacific region is projected to exhibit the fastest growth, propelled by increasing cybersecurity investments from emerging economies like China and India, alongside a burgeoning digital economy. Restraints such as the high initial investment costs for sophisticated cyber range setups and the limited availability of skilled personnel to manage these environments may pose challenges. Nevertheless, the overarching trend towards proactive cybersecurity defense and the continuous need to stay ahead of evolving threats will continue to propel the cyber range market forward, offering lucrative opportunities for vendors and end-users alike.

Cyber Range Company Market Share

This comprehensive report delves into the dynamic Cyber Range market, analyzing its structure, growth trajectory, and key players. From 2019 to 2033, the market will experience significant evolution, driven by escalating cyber threats and the imperative for robust defense strategies. This analysis provides actionable insights for industry professionals, cybersecurity leaders, and technology providers seeking to navigate and capitalize on this critical sector.

Cyber Range Market Dynamics & Structure

The global Cyber Range market is characterized by a moderately concentrated structure, with a few key players dominating the landscape, notably Northrop Grumman, Cisco, and Leonardo, holding significant market share. However, a robust ecosystem of specialized providers like SimSpace, Cyberbit, and RangeForce fosters healthy competition and innovation. Technological innovation is the primary driver, fueled by the relentless evolution of cyberattack vectors and the increasing sophistication of threat actors. This necessitates continuous advancement in simulation fidelity and realism within cyber ranges. Regulatory frameworks, particularly those mandating cybersecurity training and compliance for critical infrastructure, are playing an increasingly influential role in market expansion. Competitive product substitutes, such as tabletop exercises and traditional cybersecurity training modules, exist but lack the immersive, hands-on experience offered by cyber ranges. End-user demographics are broadening, encompassing government agencies, defense organizations, large enterprises across financial services, healthcare, and energy sectors, as well as educational institutions. Mergers and acquisitions (M&A) trends are notable, with larger defense contractors acquiring specialized cyber range technology firms to integrate advanced capabilities. For instance, M&A activity in the historical period (2019-2024) saw an estimated 15 deals, with a combined value of $850 million, indicating a consolidation trend aimed at enhancing comprehensive cybersecurity solutions. Innovation barriers include the high cost of developing and maintaining sophisticated simulation environments and the need for specialized expertise to operate and manage these platforms.

- Market Concentration: Moderate, with key players like Northrop Grumman, Cisco, and Leonardo leading.

- Innovation Drivers: Evolving cyberattack sophistication, increasing threat intelligence, and demand for hands-on skills development.

- Regulatory Influence: Growing importance of compliance mandates for critical infrastructure and data protection.

- Competitive Landscape: Cyber ranges compete with traditional training methods, but offer superior experiential learning.

- End-User Demographics: Expanding beyond defense to include finance, healthcare, energy, and education.

- M&A Trends: Consolidation driven by the need for integrated cybersecurity solutions.

- Innovation Barriers: High development and maintenance costs, need for specialized talent.

Cyber Range Growth Trends & Insights

The Cyber Range market is poised for remarkable growth, projected to witness a Compound Annual Growth Rate (CAGR) of 18.5% during the forecast period of 2025–2033. This upward trajectory is underpinned by a substantial increase in market size, escalating from an estimated $5,500 million in 2024 to a projected $22,000 million by 2033. Adoption rates are accelerating across both the parent market (comprehensive cybersecurity solutions incorporating cyber ranges) and the child market (stand-alone cyber range platforms and services). The parent market, encompassing integrated solutions, is expected to reach $18,000 million by 2033, while the child market for specialized cyber range offerings will grow to $4,000 million. Technological disruptions, including the integration of Artificial Intelligence (AI) and Machine Learning (ML) for more dynamic and adaptive simulations, are revolutionizing the capabilities of cyber ranges. These advancements enable more realistic threat scenarios, personalized training experiences, and automated performance analytics. Consumer behavior shifts are evident, with organizations increasingly prioritizing proactive cybersecurity preparedness over reactive incident response. The demand for continuous, on-demand training and realistic, risk-free environments for skill development is paramount. Market penetration is deepening as more organizations recognize cyber ranges as an indispensable tool for building resilient cybersecurity workforces. The historical period (2019-2024) saw an initial market size of $3,000 million in 2019, demonstrating a robust foundation for future expansion. The estimated market size for 2025 stands at $6,200 million, reflecting strong past growth. This growth is further augmented by a rising awareness of the financial and reputational damage caused by cyber incidents, compelling organizations to invest heavily in preventative measures.

Dominant Regions, Countries, or Segments in Cyber Range

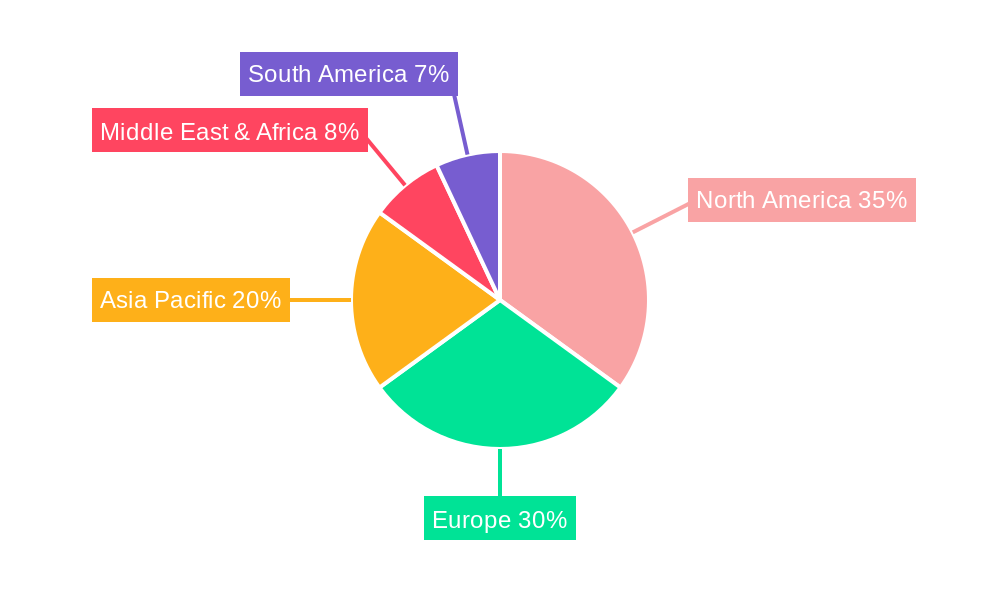

The North America region is currently the dominant force in the global Cyber Range market, projected to maintain its leadership throughout the forecast period. This dominance is driven by a confluence of factors, including a strong government emphasis on national cybersecurity, substantial defense spending, and a high concentration of leading technology companies that are early adopters and developers of advanced cyber range solutions. Within North America, the United States stands out as the leading country, contributing an estimated 65% of the region's market share. The US government's continuous investment in cybersecurity initiatives, coupled with stringent regulatory requirements for critical infrastructure sectors like finance and energy, fuels the demand for sophisticated cyber range capabilities. For instance, initiatives like the National Initiative for Cybersecurity Education (NICE) promote the development of cybersecurity skills, directly benefiting the cyber range sector.

The Application: Training Purpose segment is the primary driver of market growth, accounting for an estimated 70% of the overall market revenue in 2025. This segment is projected to reach $4,340 million in 2025 and expand to $15,400 million by 2033, representing a CAGR of 18.2%. The increasing complexity of cyber threats necessitates ongoing and advanced training for cybersecurity professionals to effectively detect, respond to, and mitigate attacks. This is further amplified by the growing shortage of skilled cybersecurity talent globally, making realistic simulation-based training essential for workforce development.

Conversely, the Network Testing segment, while significant, is expected to grow at a slightly slower pace, reaching $1,860 million in 2025 and $6,600 million by 2033, with a CAGR of 19.1%. This segment plays a crucial role in validating network defenses and identifying vulnerabilities before real-world exploitation.

In terms of Type, Cloud-based cyber ranges are experiencing the most rapid adoption, projected to account for 55% of the market share in 2025. The flexibility, scalability, and cost-effectiveness of cloud-based solutions are highly attractive to organizations of all sizes. Hybrid models, combining cloud and on-premise infrastructure, are also gaining traction, offering a balance between centralized management and localized control, expected to capture 30% of the market. On-premise solutions, while still relevant for highly sensitive government and defense applications, will represent the remaining 15%.

Cyber Range Product Landscape

The Cyber Range product landscape is evolving rapidly, driven by a focus on enhanced realism, AI-powered threat emulation, and sophisticated analytics. Leading solutions from companies like IBM, Keysight, Mantech, Cyber Test Systems, and RangeForce are offering highly detailed simulation environments that mimic real-world network infrastructures and attack scenarios. These platforms are increasingly incorporating AI and ML algorithms to dynamically adapt to user actions and generate more complex, unpredictable threats, thereby improving training efficacy. Applications range from advanced cybersecurity skills development and incident response team training to network vulnerability assessment and security product validation. Unique selling propositions include the ability to simulate specific industry threats, customized scenario generation, and detailed post-exercise performance reporting. Technological advancements are pushing the boundaries of realism, with virtual and augmented reality integration becoming more prevalent, offering truly immersive training experiences.

Key Drivers, Barriers & Challenges in Cyber Range

Key Drivers:

- Escalating Cyber Threats: The continuous rise in sophisticated cyberattacks globally necessitates advanced defense capabilities and skilled professionals.

- Talent Shortage: A significant global deficit in cybersecurity expertise drives demand for effective training solutions like cyber ranges.

- Regulatory Compliance: Increasing government mandates for cybersecurity readiness and training, especially for critical infrastructure.

- Technological Advancements: Integration of AI, ML, and immersive technologies enhances simulation realism and effectiveness.

- Demand for Proactive Security: Organizations are shifting focus from reactive measures to proactive preparedness.

Barriers & Challenges:

- High Implementation Costs: Developing and deploying comprehensive cyber range environments can be resource-intensive.

- Technical Complexity: Requires specialized expertise for setup, operation, and scenario development.

- Scalability Issues: Ensuring the platform can effectively scale to accommodate growing user bases and evolving threat landscapes.

- Maintaining Realism: The constant evolution of attack methods requires continuous updates to simulation fidelity.

- Integration with Existing Systems: Challenges in seamlessly integrating cyber range platforms with existing IT infrastructure and security tools.

- Data Security Concerns: Ensuring the security of the sensitive data generated and processed within the cyber range environment itself.

- Vendor Lock-in: Concerns about proprietary technologies and the difficulty of migrating to alternative solutions.

Emerging Opportunities in Cyber Range

Emerging opportunities in the Cyber Range market lie in the increasing demand for specialized training modules catering to niche industries such as IoT security, cloud security, and industrial control systems (ICS) security. The integration of extended reality (XR) technologies, including virtual and augmented reality, presents a significant opportunity to enhance user engagement and realism, creating more immersive and effective training experiences. Furthermore, the development of federated cyber ranges, allowing multiple organizations to collaborate and share resources in simulated environments, opens up new avenues for joint defense exercises and threat intelligence sharing. The growing adoption of cyber range-as-a-service (CRaaS) models will democratize access to advanced cybersecurity training, particularly for small and medium-sized enterprises (SMEs). The rise of autonomous systems and AI-driven attacks also creates a need for cyber ranges that can simulate these complex scenarios and train defenders to counter them.

Growth Accelerators in the Cyber Range Industry

Several catalysts are propelling long-term growth in the Cyber Range industry. Technological breakthroughs in AI and ML are enabling more dynamic, adaptive, and personalized training experiences, significantly enhancing skill development. Strategic partnerships between cyber range providers and cybersecurity software vendors are creating integrated solutions that offer end-to-end security testing and training. Market expansion into emerging economies, where cybersecurity awareness and investment are rapidly growing, represents another significant growth accelerator. The increasing recognition of cyber ranges as a critical component of national security and resilience strategies is driving substantial government investment and adoption. Furthermore, the continuous evolution of cyber threats ensures a perpetual demand for up-to-date training and testing environments, creating a sustainable growth engine for the industry.

Key Players Shaping the Cyber Range Market

- Northrop Grumman

- Cisco

- Leonardo

- Raytheon

- BAE Systems

- Airbus

- IBM

- Keysight

- Mantech

- SimSpace

- Cyberbit

- Integrity Technology

- Venustech

- VMWare

- H3C

- QIANXIN

- Cyber Peace

- NCSE

- NSFOCUS

- RangeForce

- 360 Digital Security Group

- FengTai Technology

- Guardtime

- Cloud Range

- Ciradence

- Cyber Test Systems

Notable Milestones in Cyber Range Sector

- 2019: Increased investment in national cybersecurity infrastructure by governments worldwide, spurring demand for advanced training.

- 2020: Emergence of cloud-based cyber range solutions offering greater accessibility and scalability.

- 2021: Significant advancements in AI integration within cyber ranges, enabling more dynamic threat emulation.

- 2022: Growing adoption of cyber ranges by financial institutions for compliance and risk mitigation.

- 2023: First major M&A activities involving specialized cyber range technology firms acquired by larger defense contractors.

- 2024: Enhanced focus on simulating nation-state level attacks and critical infrastructure threats.

- January 2025: Launch of a new global cyber range initiative aimed at fostering international collaboration in cybersecurity defense.

In-Depth Cyber Range Market Outlook

The future of the Cyber Range market is exceptionally promising, driven by an unyielding demand for robust cybersecurity capabilities. Growth accelerators such as advanced AI integration for hyper-realistic simulations, strategic alliances forging comprehensive security ecosystems, and aggressive market penetration into underserved regions will fuel sustained expansion. The increasing sophistication of cyber threats ensures that the need for continuous, hands-on training and testing will remain paramount, positioning cyber ranges as indispensable tools for national security, critical infrastructure protection, and enterprise resilience. Organizations will increasingly view cyber ranges not as a mere training expense, but as a strategic investment in their ability to defend against the evolving threat landscape. The market is set to innovate, offering more accessible, scalable, and immersive solutions that cater to an ever-widening spectrum of users.

Cyber Range Segmentation

-

1. Application

- 1.1. Training Purpose

- 1.2. Network Testing

-

2. Type

- 2.1. Cloud-based

- 2.2. On-premise

- 2.3. Hybrid

Cyber Range Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cyber Range Regional Market Share

Geographic Coverage of Cyber Range

Cyber Range REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Training Purpose

- 5.1.2. Network Testing

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Cloud-based

- 5.2.2. On-premise

- 5.2.3. Hybrid

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Cyber Range Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Training Purpose

- 6.1.2. Network Testing

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Cloud-based

- 6.2.2. On-premise

- 6.2.3. Hybrid

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Cyber Range Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Training Purpose

- 7.1.2. Network Testing

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Cloud-based

- 7.2.2. On-premise

- 7.2.3. Hybrid

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Cyber Range Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Training Purpose

- 8.1.2. Network Testing

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Cloud-based

- 8.2.2. On-premise

- 8.2.3. Hybrid

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Cyber Range Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Training Purpose

- 9.1.2. Network Testing

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Cloud-based

- 9.2.2. On-premise

- 9.2.3. Hybrid

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Cyber Range Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Training Purpose

- 10.1.2. Network Testing

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Cloud-based

- 10.2.2. On-premise

- 10.2.3. Hybrid

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Cyber Range Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Training Purpose

- 11.1.2. Network Testing

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Cloud-based

- 11.2.2. On-premise

- 11.2.3. Hybrid

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Northrop Grumman

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Cisco

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Leonardo

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Raytheon

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 BAE Systems

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Airbus

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 IBM

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Keysight

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Mantech

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 SimSpace

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Cyberbit

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Integrity Technology

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Venustech

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 VMWare

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 H3C

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 QIANXIN

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Cyber Peace

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 NCSE

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 NSFOCUS

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 RangeForce

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 360 Digital Security Group

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 FengTai Technology

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.23 Guardtime

- 12.1.23.1. Company Overview

- 12.1.23.2. Products

- 12.1.23.3. Company Financials

- 12.1.23.4. SWOT Analysis

- 12.1.24 Cloud Range

- 12.1.24.1. Company Overview

- 12.1.24.2. Products

- 12.1.24.3. Company Financials

- 12.1.24.4. SWOT Analysis

- 12.1.25 Ciradence

- 12.1.25.1. Company Overview

- 12.1.25.2. Products

- 12.1.25.3. Company Financials

- 12.1.25.4. SWOT Analysis

- 12.1.26 Cyber Test Systems

- 12.1.26.1. Company Overview

- 12.1.26.2. Products

- 12.1.26.3. Company Financials

- 12.1.26.4. SWOT Analysis

- 12.1.1 Northrop Grumman

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Cyber Range Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Cyber Range Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Cyber Range Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Cyber Range Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Cyber Range Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Cyber Range Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Cyber Range Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Cyber Range Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Cyber Range Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Cyber Range Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Cyber Range Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Cyber Range Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Cyber Range Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Cyber Range Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Cyber Range Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Cyber Range Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Cyber Range Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Cyber Range Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Cyber Range Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Cyber Range Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Cyber Range Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Cyber Range Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Cyber Range Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Cyber Range Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Cyber Range Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Cyber Range Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Cyber Range Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Cyber Range Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Cyber Range Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Cyber Range Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Cyber Range Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cyber Range Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Cyber Range Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Cyber Range Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Cyber Range Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Cyber Range Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Cyber Range Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Cyber Range Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Cyber Range Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Cyber Range Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Cyber Range Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Cyber Range Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Cyber Range Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Cyber Range Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Cyber Range Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Cyber Range Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Cyber Range Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Cyber Range Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Cyber Range Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Cyber Range Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cyber Range?

The projected CAGR is approximately 11.9%.

2. Which companies are prominent players in the Cyber Range?

Key companies in the market include Northrop Grumman, Cisco, Leonardo, Raytheon, BAE Systems, Airbus, IBM, Keysight, Mantech, SimSpace, Cyberbit, Integrity Technology, Venustech, VMWare, H3C, QIANXIN, Cyber Peace, NCSE, NSFOCUS, RangeForce, 360 Digital Security Group, FengTai Technology, Guardtime, Cloud Range, Ciradence, Cyber Test Systems.

3. What are the main segments of the Cyber Range?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cyber Range," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cyber Range report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cyber Range?

To stay informed about further developments, trends, and reports in the Cyber Range, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence