Key Insights

The global digital wallet market is poised for substantial growth, projected to reach an estimated $1,800 billion by 2025, with a robust Compound Annual Growth Rate (CAGR) of 28% during the forecast period of 2025-2033. This remarkable expansion is primarily driven by the increasing adoption of smartphones, the surging demand for contactless payment solutions, and the growing e-commerce landscape. The convenience and security offered by digital wallets are revolutionizing how consumers and businesses transact, making them an indispensable part of modern financial ecosystems. Key applications span across Mobile Network Operators (MNOs), financial institutions, payment networks, intermediaries, merchants, and end-customers, all contributing to a dynamic and interconnected market. The market is further segmented by type into hardware, software, and services, with software and services expected to dominate due to their flexibility and scalability. Leading companies such as MasterCard, Apple, Amazon, and Google are actively shaping this market through continuous innovation and strategic partnerships.

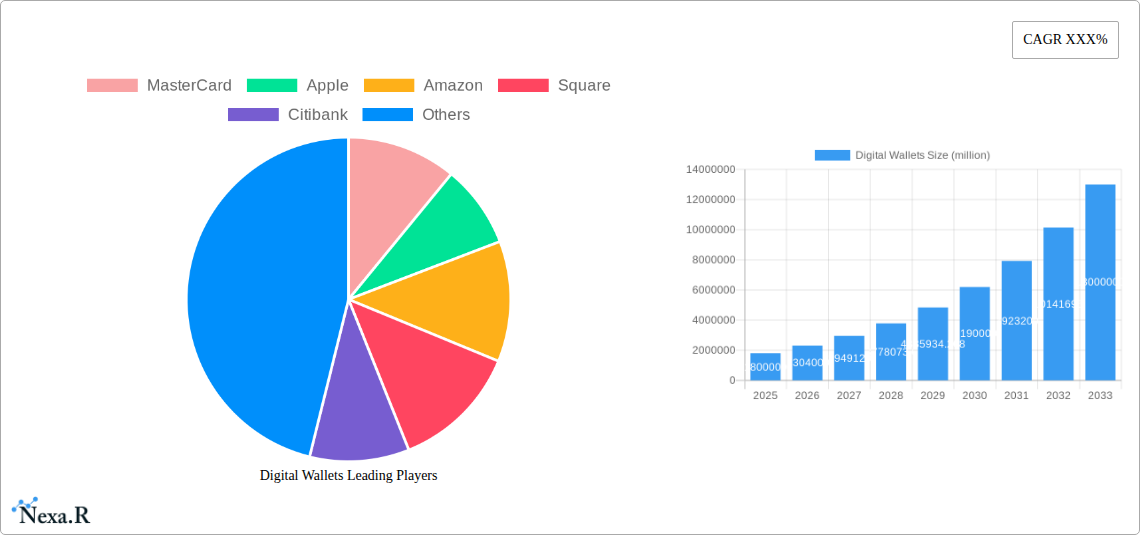

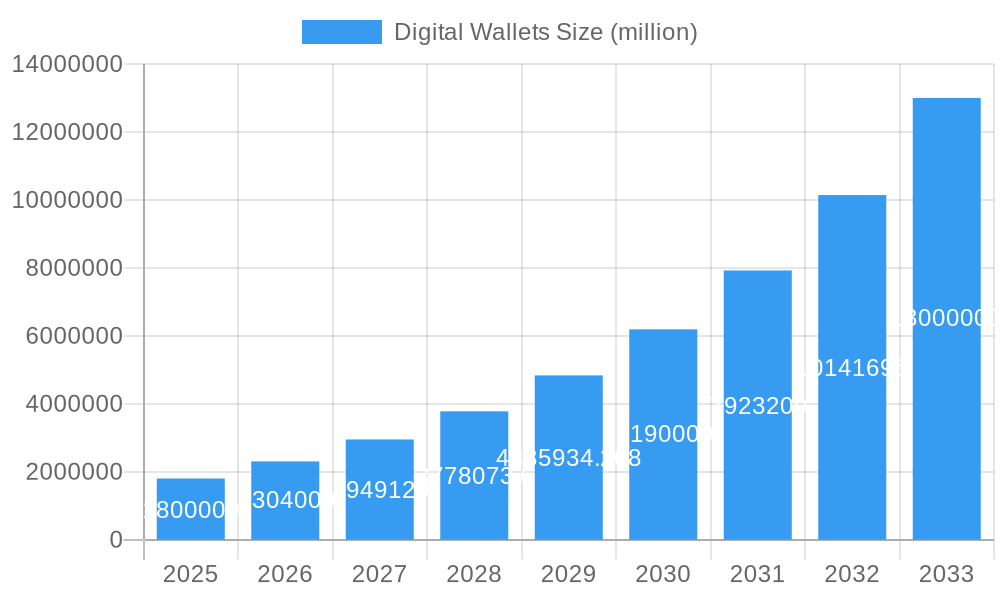

Digital Wallets Market Size (In Million)

The market's growth trajectory is supported by evolving consumer preferences for faster and more integrated payment experiences. The COVID-19 pandemic significantly accelerated the shift towards digital transactions, solidifying the importance of digital wallets for both everyday purchases and online commerce. While the market benefits from these strong drivers, it also faces certain restraints, including data security concerns and stringent regulatory frameworks in various regions, which may temper the pace of adoption in some segments. Geographically, Asia Pacific, led by China and India, is anticipated to be a key growth engine, owing to a large unbanked population and rapid digital infrastructure development. North America and Europe also represent significant markets, driven by advanced technological adoption and a mature e-commerce ecosystem. The ongoing integration of digital wallets with loyalty programs, identity verification, and other financial services will further enhance their value proposition and fuel sustained market expansion.

Digital Wallets Company Market Share

Digital Wallets Market Analysis: Comprehensive Report & Global Outlook (2019-2033)

This in-depth report offers a complete analysis of the global digital wallets market, exploring its dynamics, growth trajectories, regional dominance, product landscape, and key players. Covering the historical period from 2019-2024, the base year of 2025, and a forecast period extending to 2033, this study provides actionable insights for stakeholders seeking to capitalize on this rapidly evolving industry. We meticulously analyze market size, adoption rates, technological advancements, and consumer behavior shifts, leveraging extensive data and expert analysis. This report is designed to be the definitive resource for industry professionals, investors, and strategists navigating the future of digital payments.

Digital Wallets Market Dynamics & Structure

The global digital wallets market is characterized by a dynamic and evolving structure, driven by rapid technological innovation and increasing consumer adoption of contactless and mobile payment solutions. Market concentration is moderately high, with key players like Google, Apple, Samsung, and MasterCard holding significant market share through their integrated payment ecosystems. However, the emergence of FinTech disruptors and the expansion of payment network providers such as Visa and Square are fostering a more competitive landscape.

- Technological Innovation Drivers: The primary drivers of innovation include the advancement of NFC (Near Field Communication), QR code technology, biometrics for enhanced security, and the integration of loyalty programs and personalized offers within digital wallet applications. Cloud-based solutions and open banking initiatives further fuel innovation by enabling seamless integration with various financial services.

- Regulatory Frameworks: Evolving regulatory environments, particularly concerning data privacy (e.g., GDPR, CCPA) and anti-money laundering (AML) regulations, significantly influence market development. Compliance with these frameworks often requires substantial investment in security infrastructure and transparent data handling practices.

- Competitive Product Substitutes: While digital wallets offer convenience, they face competition from traditional payment methods like credit and debit cards, as well as emerging alternatives like cryptocurrencies and buy-now-pay-later (BNPL) services. The seamless integration with point-of-sale systems and online checkout processes remains crucial for digital wallets to maintain their competitive edge.

- End-User Demographics: The market caters to a broad spectrum of end-users, from tech-savvy millennials and Gen Z who are early adopters of mobile technologies, to older demographics increasingly embracing digital solutions for convenience and accessibility. Understanding diverse demographic needs is key to tailoring product offerings.

- M&A Trends: Mergers and acquisitions are prevalent, as larger companies acquire innovative startups to gain access to new technologies, customer bases, or specialized expertise. For instance, acquisitions of payment processors and FinTech companies by established financial institutions and tech giants underscore this trend. The volume of M&A deals is expected to remain robust as players seek to consolidate market positions and expand service portfolios.

Digital Wallets Growth Trends & Insights

The global digital wallets market is poised for substantial growth, driven by an accelerating shift towards digital transactions, increasing smartphone penetration worldwide, and a growing acceptance of contactless payments. This growth is further amplified by the expansion of e-commerce and the rising demand for secure, convenient, and integrated payment solutions. Over the study period from 2019 to 2033, the market will witness significant expansion, with the base year of 2025 serving as a pivotal point for current market valuation and the forecast period from 2025 to 2033 projecting sustained upward momentum. The historical period of 2019-2024 has laid the groundwork for this expansion, marked by increasing consumer trust and merchant adoption.

The market size evolution is a key indicator of this growth. In 2025, the estimated market size is projected to reach $1,850 million units, a significant increase from historical figures, demonstrating the maturation of the digital wallet ecosystem. This growth trajectory is expected to continue at a Compound Annual Growth Rate (CAGR) of approximately 18.5% between 2025 and 2033. This robust CAGR reflects not only the increasing number of transactions processed through digital wallets but also the expansion of the types of services offered, including peer-to-peer payments, loyalty programs, transit passes, and even digital identities.

Adoption rates are on a steep upward curve globally. As of 2025, an estimated 65% of smartphone users are expected to utilize digital wallets for at least one type of transaction. This penetration rate is significantly higher in developed economies but is rapidly catching up in emerging markets due to increased smartphone affordability and the proliferation of mobile network operator (MNO) services that bundle digital payment solutions.

Technological disruptions are continuously reshaping the landscape. Innovations in biometric authentication (fingerprint, facial recognition), tokenization for enhanced security, and the integration of artificial intelligence (AI) for personalized user experiences and fraud detection are becoming standard features. The increasing prevalence of contactless payment terminals at retail outlets, coupled with the convenience of mobile payments, is a major catalyst for adoption. Furthermore, the development of cross-border payment solutions within digital wallets is opening up new avenues for growth and convenience for global consumers and businesses alike.

Consumer behavior shifts are equally influential. There is a discernible move away from carrying physical wallets towards a preference for digital equivalents that consolidate payment methods, loyalty cards, and even event tickets. Consumers are prioritizing speed, security, and the ability to manage their finances on the go. The rise of the gig economy and the increasing reliance on online platforms for commerce and services further reinforce the demand for agile and accessible digital payment options. This fundamental change in consumer preference is a powerful engine driving the sustained growth of the digital wallets market.

Dominant Regions, Countries, or Segments in Digital Wallets

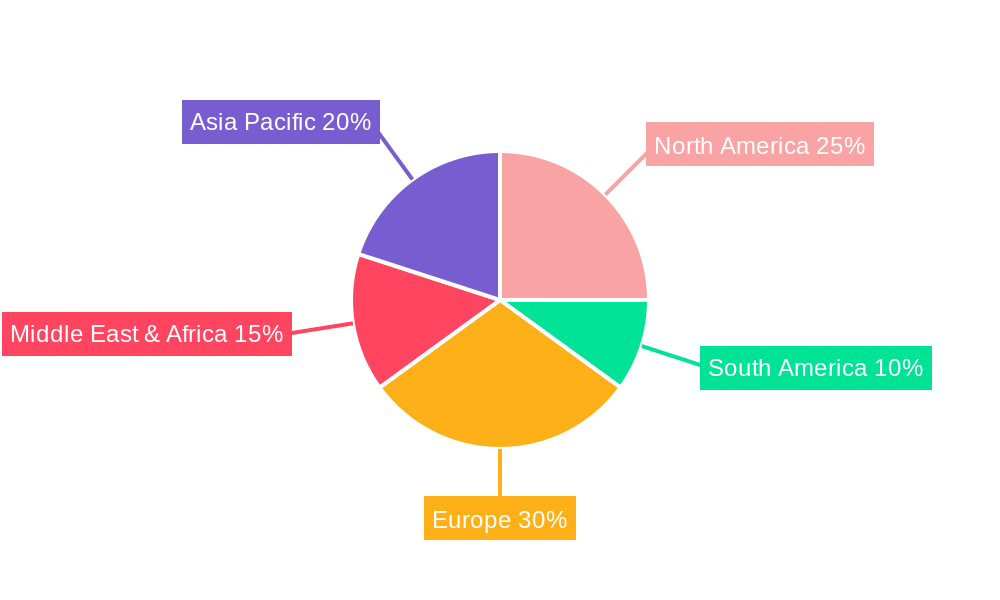

The digital wallets market exhibits significant dominance across various regions and segments, with North America and Asia-Pacific leading the charge in terms of market size and growth potential. Within the Application segment, Customers represent the largest and most influential group, driving demand for convenient and secure payment solutions. Their adoption rates are directly correlated with the overall market expansion.

- Dominant Region: Asia-Pacific: This region is the powerhouse of the digital wallets market, driven by rapid digitalization, a vast population embracing mobile technology, and the widespread adoption of QR code-based payments in countries like China and India. The presence of major local players like Paytm has significantly boosted market penetration. The supportive government initiatives promoting digital economies and the increasing penetration of smartphones further solidify Asia-Pacific's dominance. Market share in this region is estimated to be over 40% of the global digital wallets market.

- Dominant Country: China: As a global leader in mobile payments, China's digital wallet ecosystem is exceptionally mature. Platforms like Alipay and WeChat Pay have integrated seamlessly into daily life, encompassing everything from retail purchases to utility bill payments and social transactions. This deep integration, supported by strong infrastructure and widespread merchant acceptance, makes China the most dominant single country.

- Dominant Application Segment: Customers: The end-users, or Customers, are the primary drivers of the digital wallets market. Their increasing reliance on mobile devices for daily transactions, combined with a growing preference for contactless and streamlined payment experiences, fuels demand. As more consumers adopt digital wallets for online shopping, in-store purchases, and peer-to-peer transfers, the market naturally expands. The growth potential within this segment is immense, as a significant portion of the global population is still in the early stages of digital wallet adoption.

- Dominant Type Segment: Software: While Hardware wallets (like secure elements in smartphones) and Services (like transaction processing) are crucial components, the Software segment, encompassing the digital wallet applications themselves, currently holds the largest market share. The ease of deployment, continuous updates, and the ability to integrate a wide array of features within software make it the most dynamic and scalable segment. This includes mobile apps, web-based wallets, and integrated payment solutions within other applications.

Key drivers contributing to this dominance include robust economic policies encouraging digital transformation, widespread availability of high-speed internet infrastructure, and favorable regulatory environments that support the growth of FinTech. The competitive landscape within these dominant segments, while intense, also spurs innovation, leading to a continuous cycle of improvement and user-centric development, further cementing their leading positions.

Digital Wallets Product Landscape

The digital wallets product landscape is characterized by rapid innovation, focusing on enhanced security, user convenience, and expanded functionality. Key product innovations include the seamless integration of biometric authentication methods such as fingerprint and facial recognition, significantly bolstering security protocols. Tokenization technology is also a cornerstone, replacing sensitive card details with unique tokens for secure transactions, minimizing the risk of data breaches. Furthermore, digital wallets are increasingly incorporating loyalty programs, discount coupons, and digital tickets, transforming them into comprehensive personal finance management tools. Performance metrics are measured by transaction speed, success rates, and the breadth of accepted payment methods. Unique selling propositions often lie in the user-friendly interface, the ability to support multiple currencies for international transactions, and robust customer support. Technological advancements continue to push the boundaries, with a growing emphasis on leveraging AI for personalized offers and predictive spending insights.

Key Drivers, Barriers & Challenges in Digital Wallets

The digital wallets market is propelled by several key drivers that are accelerating its growth and adoption.

- Technological Advancements: The ongoing development of NFC, QR codes, and biometric security significantly enhances user experience and security, making digital wallets more attractive.

- Increasing Smartphone Penetration: A growing global base of smartphone users provides a fertile ground for mobile-first payment solutions.

- E-commerce Growth: The surge in online shopping necessitates secure and convenient digital payment options, directly benefiting digital wallets.

- Government Initiatives: Many governments worldwide are promoting digital economies, encouraging the adoption of digital payment systems.

- Demand for Contactless Payments: Public health concerns and a desire for convenience have accelerated the adoption of contactless payment solutions.

However, the market also faces significant barriers and challenges.

- Security Concerns and Data Privacy: Despite advancements, consumer concerns about data breaches and financial fraud remain a major hurdle, requiring continuous investment in robust cybersecurity measures.

- Regulatory Hurdles: Navigating diverse and evolving regulatory landscapes across different regions can be complex and costly for service providers.

- Fragmented Market and Interoperability Issues: A lack of universal standards and interoperability between different digital wallet platforms can create friction for users and merchants.

- Low Financial Literacy in Emerging Markets: In certain regions, a lack of understanding about digital financial services can hinder adoption rates.

- Merchant Adoption and Infrastructure: While growing, ensuring widespread merchant acceptance and adequate payment infrastructure remains a challenge, particularly for smaller businesses.

- Supply Chain Issues: While less direct, disruptions in the global supply chain for essential hardware components required for some wallet functionalities could indirectly impact the market.

Emerging Opportunities in Digital Wallets

Emerging opportunities in the digital wallets industry are abundant, driven by evolving consumer needs and technological advancements. The integration of digital wallets with the Internet of Things (IoT) presents a significant avenue, enabling seamless payments from smart devices like appliances and vehicles. Furthermore, the expansion of open banking initiatives provides fertile ground for digital wallets to offer a wider array of financial services, including personalized budgeting tools, investment management, and seamless loan applications, moving beyond mere payment processing. The burgeoning market for digital identity management is another key opportunity, with digital wallets poised to securely store and manage digital IDs, credentials, and certifications, facilitating secure access to services. Lastly, the untapped potential in emerging economies, where mobile-first solutions are paramount, offers substantial growth prospects for localized and accessible digital wallet services tailored to specific cultural and economic contexts.

Growth Accelerators in the Digital Wallets Industry

Several catalysts are driving long-term growth in the digital wallets industry. Technological breakthroughs, particularly in areas like advanced AI for fraud detection and predictive analytics, are enhancing security and personalization, thereby boosting user trust and engagement. Strategic partnerships between FinTech companies, financial institutions like Citibank, and major tech players like Microsoft are crucial for expanding reach, integrating services, and building comprehensive payment ecosystems. For example, partnerships with MNOs like Sprint have historically been important for bringing mobile payments to a wider audience. Market expansion strategies, including the development of cross-border payment solutions and localized offerings for underserved markets, are further fueling growth. The increasing focus on integrating loyalty programs and offering rewards within digital wallets also acts as a significant growth accelerator, encouraging repeat usage and customer retention.

Key Players Shaping the Digital Wallets Market

- MasterCard

- Apple

- Amazon

- Square

- Citibank

- Citrus Payment

- Dwolla

- Merchant Customer Exchange

- Visa

- Microsoft

- Sprint

- First Data

- Paytm

- Samsung

Notable Milestones in Digital Wallets Sector

- 2019: Introduction of enhanced security features like advanced tokenization by major payment networks, increasing consumer confidence.

- 2020: Significant surge in contactless payment adoption due to global health concerns, accelerating the shift to digital wallets.

- 2021: Increased integration of Buy Now, Pay Later (BNPL) options within digital wallet platforms, offering greater purchasing flexibility.

- 2022: Expansion of digital wallet capabilities to include digital identity verification and document storage, enhancing utility beyond payments.

- 2023: Growing investment in AI and machine learning for personalized user experiences and more sophisticated fraud detection mechanisms.

- 2024: Continued push for interoperability and standardization among digital wallet providers to improve user experience and merchant integration.

In-Depth Digital Wallets Market Outlook

The digital wallets market outlook remains exceptionally strong, driven by the confluence of technological innovation, shifting consumer behaviors, and supportive economic policies. Growth accelerators such as the widespread adoption of 5G networks, the continued expansion of e-commerce, and the increasing demand for seamless, omnichannel payment experiences will continue to propel the market forward. Strategic opportunities lie in further enhancing the security and privacy features of digital wallets, developing more sophisticated AI-driven personalization, and expanding into new service verticals like micro-investing and digital insurance. The growing focus on sustainability and ethical finance may also present opportunities for digital wallets to integrate eco-friendly payment options and transparent financial tracking. The ability of market players to innovate, adapt to evolving regulations, and foster robust partnerships will be critical in capitalizing on the immense future potential of the digital wallets industry.

Digital Wallets Segmentation

-

1. Application

- 1.1. MNOs

- 1.2. Financial Institutions (Banks)

- 1.3. Payment Network

- 1.4. Intermediaries

- 1.5. Merchants

- 1.6. Customers

-

2. Type

- 2.1. Hardware

- 2.2. Software

- 2.3. Services

Digital Wallets Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Digital Wallets Regional Market Share

Geographic Coverage of Digital Wallets

Digital Wallets REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 21.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. MNOs

- 5.1.2. Financial Institutions (Banks)

- 5.1.3. Payment Network

- 5.1.4. Intermediaries

- 5.1.5. Merchants

- 5.1.6. Customers

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Hardware

- 5.2.2. Software

- 5.2.3. Services

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Digital Wallets Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. MNOs

- 6.1.2. Financial Institutions (Banks)

- 6.1.3. Payment Network

- 6.1.4. Intermediaries

- 6.1.5. Merchants

- 6.1.6. Customers

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Hardware

- 6.2.2. Software

- 6.2.3. Services

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Digital Wallets Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. MNOs

- 7.1.2. Financial Institutions (Banks)

- 7.1.3. Payment Network

- 7.1.4. Intermediaries

- 7.1.5. Merchants

- 7.1.6. Customers

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Hardware

- 7.2.2. Software

- 7.2.3. Services

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Digital Wallets Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. MNOs

- 8.1.2. Financial Institutions (Banks)

- 8.1.3. Payment Network

- 8.1.4. Intermediaries

- 8.1.5. Merchants

- 8.1.6. Customers

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Hardware

- 8.2.2. Software

- 8.2.3. Services

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Digital Wallets Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. MNOs

- 9.1.2. Financial Institutions (Banks)

- 9.1.3. Payment Network

- 9.1.4. Intermediaries

- 9.1.5. Merchants

- 9.1.6. Customers

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Hardware

- 9.2.2. Software

- 9.2.3. Services

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Digital Wallets Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. MNOs

- 10.1.2. Financial Institutions (Banks)

- 10.1.3. Payment Network

- 10.1.4. Intermediaries

- 10.1.5. Merchants

- 10.1.6. Customers

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Hardware

- 10.2.2. Software

- 10.2.3. Services

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Digital Wallets Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. MNOs

- 11.1.2. Financial Institutions (Banks)

- 11.1.3. Payment Network

- 11.1.4. Intermediaries

- 11.1.5. Merchants

- 11.1.6. Customers

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Hardware

- 11.2.2. Software

- 11.2.3. Services

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 MasterCard

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Apple

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Amazon

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Square

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Citibank

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Citrus Payment

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Dwolla

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Merchant Customer Exchange

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Visa

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Microsoft

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Sprint

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 First Data

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Paytm

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Samsung

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Google

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 MasterCard

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Digital Wallets Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Digital Wallets Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Digital Wallets Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Digital Wallets Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Digital Wallets Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Digital Wallets Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Digital Wallets Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Digital Wallets Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Digital Wallets Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Digital Wallets Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Digital Wallets Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Digital Wallets Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Digital Wallets Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Digital Wallets Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Digital Wallets Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Digital Wallets Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Digital Wallets Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Digital Wallets Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Digital Wallets Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Digital Wallets Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Digital Wallets Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Digital Wallets Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Digital Wallets Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Digital Wallets Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Digital Wallets Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Digital Wallets Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Digital Wallets Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Digital Wallets Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Digital Wallets Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Digital Wallets Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Digital Wallets Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Digital Wallets Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Digital Wallets Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Digital Wallets Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Digital Wallets Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Digital Wallets Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Digital Wallets Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Digital Wallets Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Digital Wallets Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Digital Wallets Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Digital Wallets Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Digital Wallets Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Digital Wallets Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Digital Wallets Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Digital Wallets Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Digital Wallets Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Digital Wallets Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Digital Wallets Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Digital Wallets Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Digital Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Digital Wallets?

The projected CAGR is approximately 21.9%.

2. Which companies are prominent players in the Digital Wallets?

Key companies in the market include MasterCard, Apple, Amazon, Square, Citibank, Citrus Payment, Dwolla, Merchant Customer Exchange, Visa, Microsoft, Sprint, First Data, Paytm, Samsung, Google.

3. What are the main segments of the Digital Wallets?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Digital Wallets," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Digital Wallets report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Digital Wallets?

To stay informed about further developments, trends, and reports in the Digital Wallets, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence