Key Insights

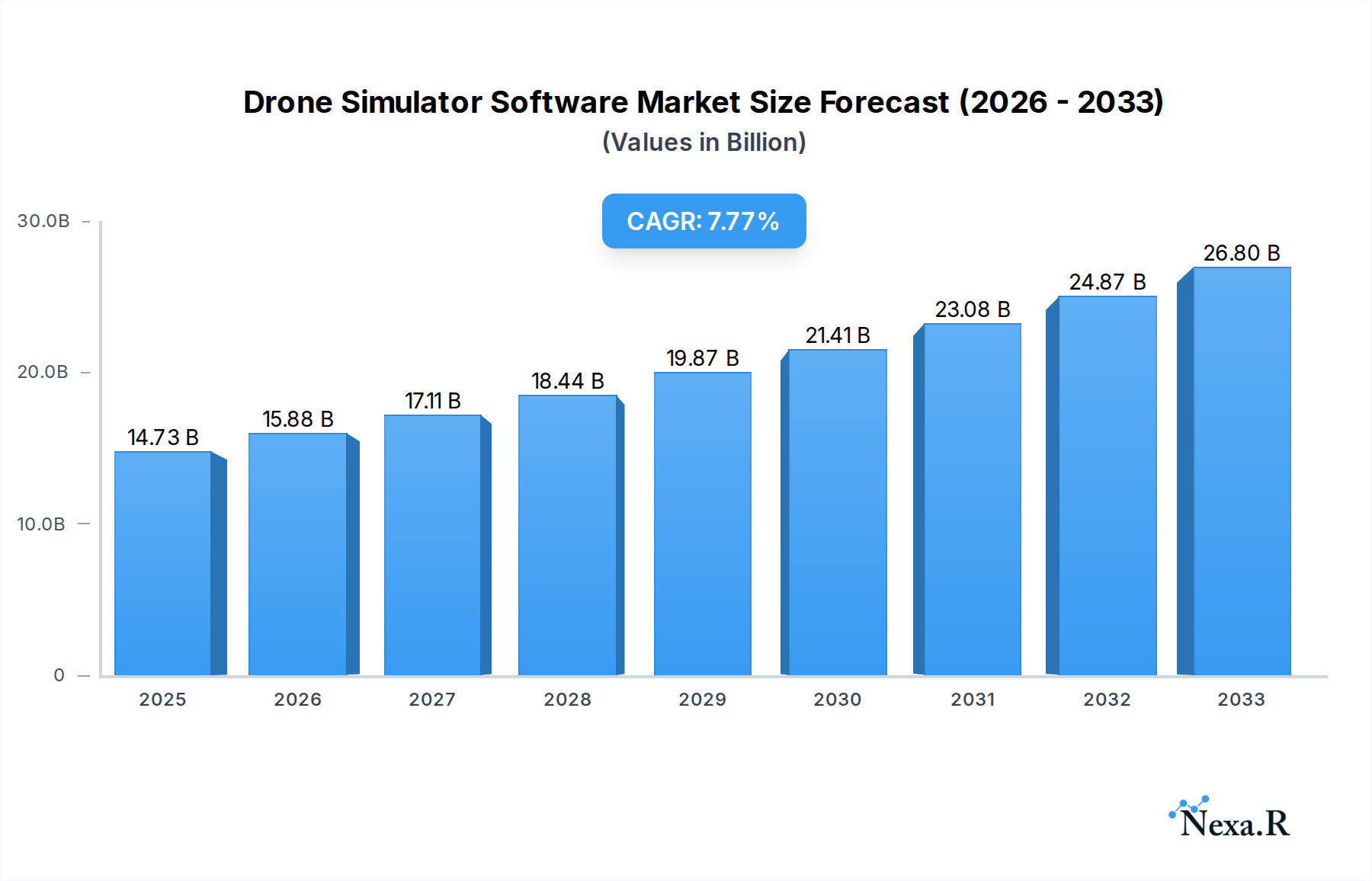

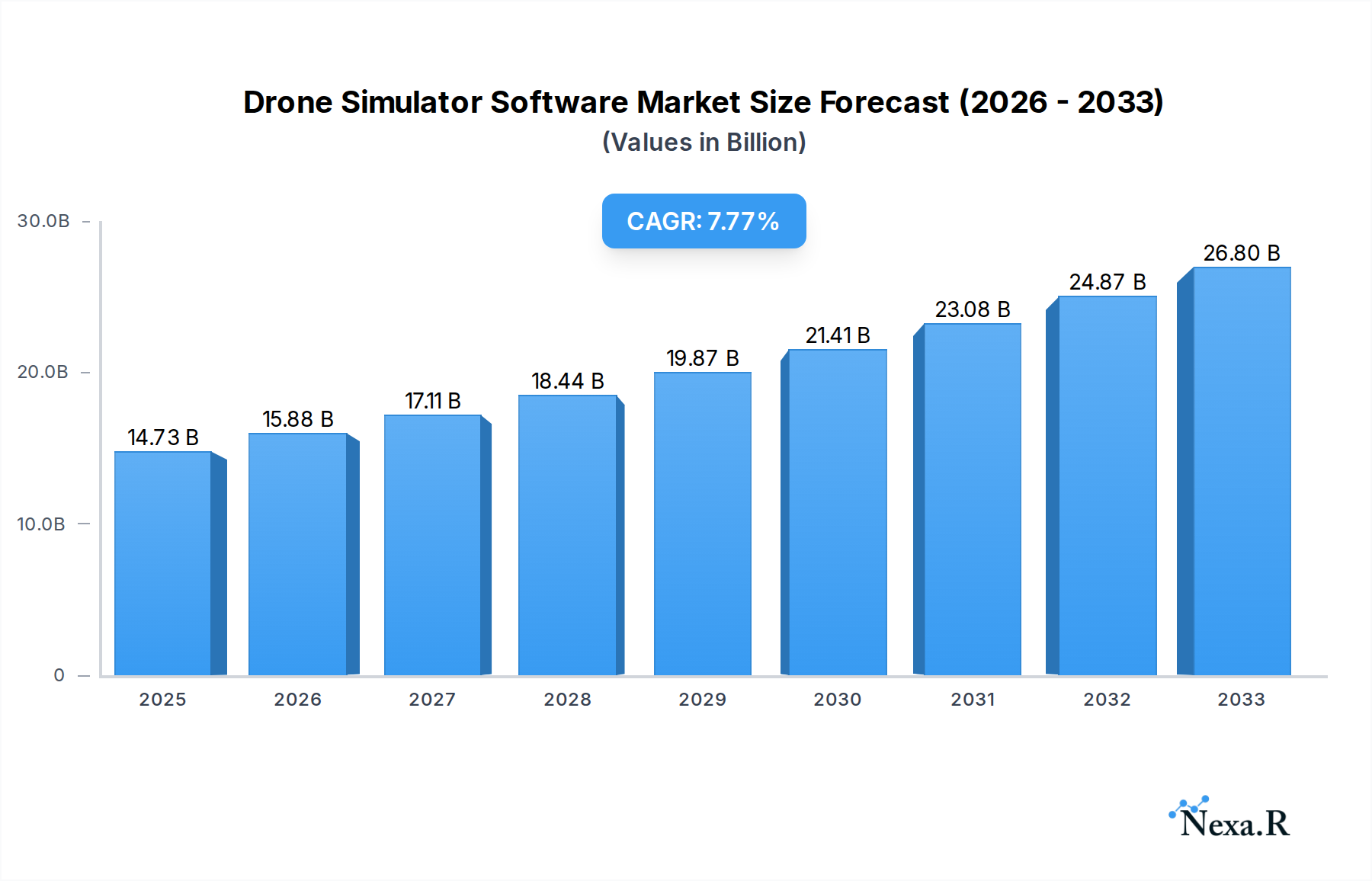

The global drone simulator software market is projected to reach $14.73 billion by 2025, exhibiting a robust compound annual growth rate (CAGR) of 7.88% during the forecast period of 2025-2033. This significant expansion is driven by the escalating adoption of drones across diverse sectors, including defense and law enforcement for enhanced training and mission readiness, and the burgeoning commercial applications in areas like aerial surveying, inspection, agriculture, and delivery services. The increasing need for cost-effective, safe, and repeatable training environments is a primary catalyst, enabling pilots and operators to refine their skills and test various flight scenarios without the risks and expenses associated with real-world operations. Furthermore, advancements in virtual reality (VR) and augmented reality (AR) technologies are integrating with drone simulators, offering more immersive and realistic training experiences, thereby fueling market growth.

Drone Simulator Software Market Size (In Billion)

The market is witnessing a surge in demand for sophisticated simulation platforms that can accurately replicate flight dynamics, environmental conditions, and sensor payloads. Key trends shaping the landscape include the development of AI-powered adaptive training modules that personalize learning experiences, the integration of multi-drone simulation capabilities for swarm training, and the increasing focus on cybersecurity features within simulator software to protect sensitive training data. While the market demonstrates strong growth potential, certain restraints exist, such as the high initial investment required for advanced simulation hardware and software, and the need for continuous software updates to keep pace with rapidly evolving drone technologies and regulations. However, the continuous innovation in simulation technology and the expanding use cases for drones across industries are expected to outweigh these challenges, propelling the drone simulator software market to new heights.

Drone Simulator Software Company Market Share

Drone Simulator Software Market Dynamics & Structure

The global drone simulator software market is characterized by a moderately consolidated structure, with key players like CAE, Leonardo, and Zen Technologies holding significant shares. Technological innovation is a primary driver, fueled by advancements in AI, machine learning, and virtual reality, enabling more realistic and sophisticated training environments. Regulatory frameworks, particularly concerning drone operation and pilot certification, are increasingly influencing the adoption of simulator software, creating a demand for compliance-driven training solutions. Competitive product substitutes, such as actual flight training and basic online courses, exist but lack the cost-effectiveness, safety, and repeatability offered by advanced simulators. End-user demographics are diverse, ranging from defense forces and law enforcement agencies to commercial drone operators and hobbyists. Mergers and acquisitions (M&A) activity is a notable trend, with companies consolidating to expand their technological capabilities and market reach. For instance, the M&A volume in the broader aerospace and defense simulation sector reached approximately $2.5 billion in 2023, indicating a strategic consolidation aimed at capturing emerging technologies and markets. Innovation barriers include high development costs for complex simulation environments and the need for continuous updates to mirror rapidly evolving drone technology.

- Market Concentration: Moderately consolidated with key players investing heavily in R&D.

- Technological Innovation Drivers: AI, ML, VR, AR integration for enhanced realism.

- Regulatory Frameworks: Driving demand for certified and compliant training solutions.

- Competitive Product Substitutes: Physical training and basic online modules offer alternatives but lack advanced features.

- End-User Demographics: Defense, law enforcement, commercial operators, and hobbyists.

- M&A Trends: Strategic acquisitions to bolster technological portfolios and market presence.

- Innovation Barriers: High development costs and the need for continuous software updates.

Drone Simulator Software Growth Trends & Insights

The drone simulator software market is poised for substantial growth, driven by an escalating demand for efficient and safe drone pilot training across various sectors. The market size is projected to expand from an estimated $1.2 billion in 2025 to an impressive $3.8 billion by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of approximately 15.8%. This surge is underpinned by increasing adoption rates, particularly within the defense and commercial segments, where complex operational scenarios require extensive and risk-free practice. Technological disruptions, such as the integration of realistic weather simulation, advanced sensor modeling, and multi-user network capabilities, are enhancing the fidelity and effectiveness of these simulators, making them indispensable training tools. Consumer behavior shifts are also playing a crucial role; as the complexity and capabilities of drones continue to grow, so does the need for skilled operators who can navigate diverse environments and challenging conditions. This has led to a greater appreciation for simulator-based training, which offers a cost-effective and repeatable method to build proficiency without the inherent risks and expenses associated with actual flight. Market penetration is deepening as more organizations recognize the return on investment through reduced accident rates, optimized mission planning, and faster skill acquisition. For example, the increasing use of drones for delivery services, infrastructure inspection, and agricultural monitoring necessitates a larger pool of certified and competent pilots, directly fueling the demand for sophisticated simulation software. The global market penetration of drone simulator software, currently estimated at 25% of all drone operators requiring formal training, is expected to rise to over 60% by 2033. This trend highlights the transformative impact of these digital training platforms on the overall drone ecosystem. Furthermore, the evolution of training paradigms, moving towards blended learning approaches that combine virtual simulation with minimal real-world flight hours, is accelerating market adoption. The software’s ability to replicate a wide array of scenarios, from urban flight in congested airspace to operating in extreme weather conditions, ensures that pilots are adequately prepared for virtually any situation, thereby enhancing operational safety and mission success rates. The continuous development of more immersive experiences through VR/AR integration further solidifies the role of simulators as the cornerstone of modern drone pilot education.

Dominant Regions, Countries, or Segments in Drone Simulator Software

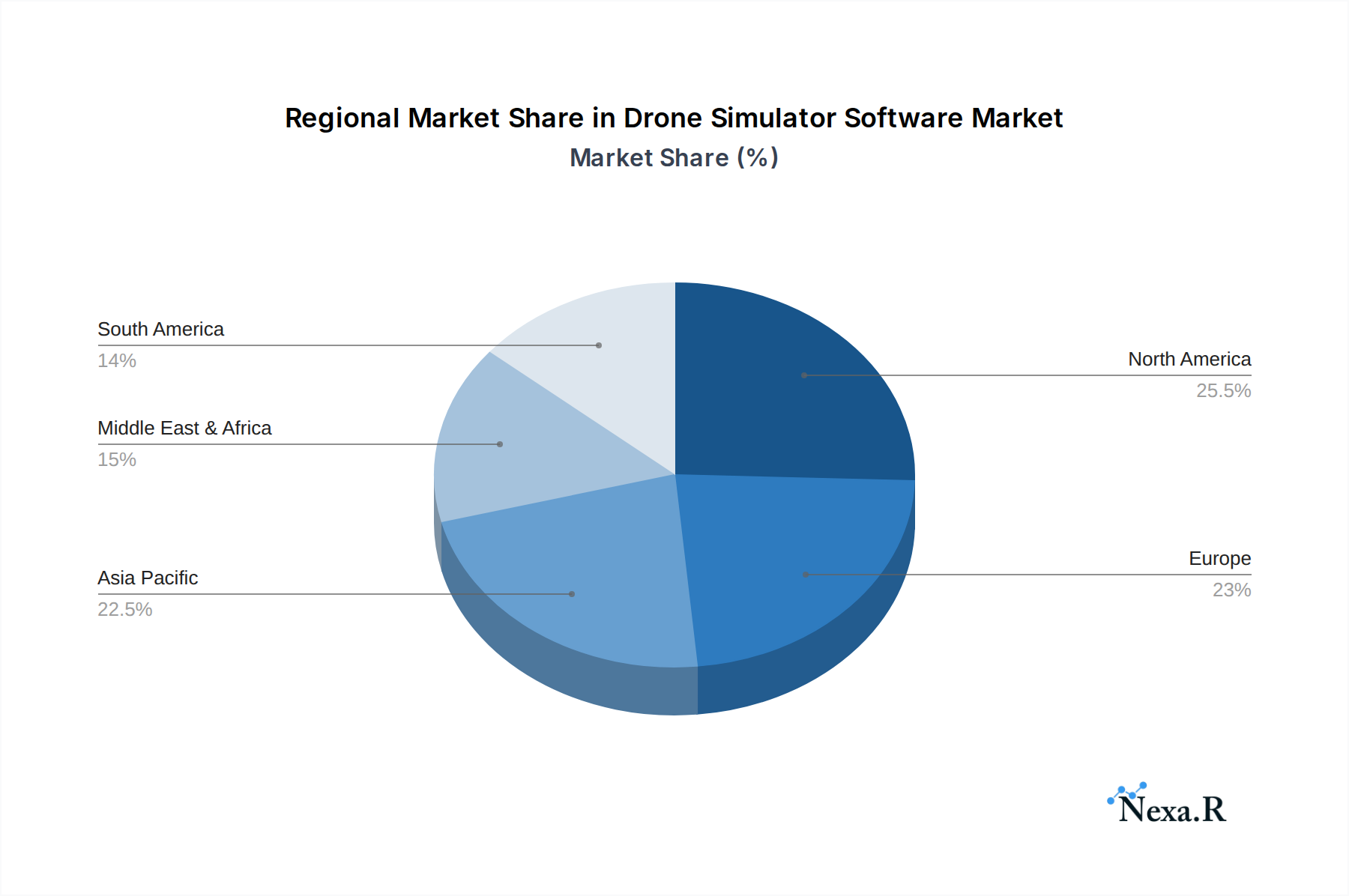

The Defense & Law Enforcement application segment is the most dominant force driving growth in the global drone simulator software market. This segment is projected to account for over 55% of the total market revenue by 2033, significantly outperforming commercial and other applications. This dominance stems from the critical need for advanced and realistic training for military and para-military operations, where drone warfare and surveillance capabilities are paramount. Countries with significant defense budgets and active military engagements, such as the United States, China, and European nations, are leading this demand. The United States, in particular, is expected to represent approximately 30% of the global market share within this segment by 2033, driven by continuous investment in next-generation defense technologies and extensive training programs for its drone operators.

Dominant Application Segment: Defense & Law Enforcement.

- Market Share Projection: Expected to exceed 55% of the total market by 2033.

- Key Drivers: Critical need for realistic training for complex military and security operations, including reconnaissance, surveillance, target acquisition, and combat.

- Technological Advancements: Demand for simulation of advanced drone capabilities, including swarm tactics, electronic warfare countermeasures, and multi-sensor fusion.

- Regulatory Influence: Strict governmental regulations and military procurement policies favor validated and robust simulation solutions.

Leading Regions & Countries:

- North America (especially the United States):

- Market Share: Estimated at 30% of the global market by 2033, with a strong focus on defense.

- Key Drivers: High defense spending, advanced technological infrastructure, and a significant presence of major defense contractors. Continuous modernization of military fleets and training protocols.

- Europe:

- Market Share: Anticipated to capture around 25% of the global market by 2033.

- Key Drivers: Harmonization of defense procurement policies, increasing collaboration on advanced drone technologies, and a growing emphasis on border security and law enforcement. Countries like Germany, France, and the UK are key contributors.

- Asia-Pacific (especially China and India):

- Market Share: Projected to grow at the fastest CAGR, reaching approximately 20% of the global market by 2033.

- Key Drivers: Rapid modernization of military forces, significant investments in domestic drone manufacturing, and increasing adoption for law enforcement and internal security.

- North America (especially the United States):

Dominant Operating System Types:

- Windows: Remains the dominant operating system for drone simulator software, accounting for over 70% of the market share due to its widespread adoption in defense and commercial sectors, robust hardware compatibility, and extensive software development ecosystem.

- Linux: Shows a growing niche, particularly in specialized defense applications and research environments, with an anticipated market share of around 15%.

- Mac: Holds a smaller but growing segment, estimated at 10%, catering to educational institutions and some commercial entities.

Drone Simulator Software Product Landscape

The drone simulator software product landscape is characterized by continuous innovation aimed at enhancing realism and training effectiveness. Leading solutions now offer advanced physics engines that accurately replicate flight dynamics under various environmental conditions, including wind, turbulence, and precipitation. Integration of high-fidelity 3D environments, custom mission builders, and real-time data visualization are becoming standard. Performance metrics are evaluated based on the accuracy of flight modeling, the breadth of drone models supported (e.g., fixed-wing, multi-rotor, VTOL), the realism of sensor simulation (e.g., EO/IR cameras, LiDAR), and the flexibility of network-enabled multi-user training. Unique selling propositions often lie in the software's ability to simulate advanced scenarios like electronic warfare, swarm operations, and specific payload integrations. Technological advancements are focused on leveraging AI for intelligent scenario generation and adaptive training paths, ensuring personalized learning experiences for pilots.

Key Drivers, Barriers & Challenges in Drone Simulator Software

Key Drivers: The primary forces propelling the drone simulator software market include the escalating demand for skilled drone pilots across defense, commercial, and public safety sectors, driven by the rapid proliferation of drone technology. Technological advancements in AI, VR, and AR are enabling increasingly realistic and immersive training experiences, which are crucial for preparing operators for complex missions. Furthermore, stringent aviation regulations and the desire to minimize the risks and costs associated with actual flight training are significant accelerators. For instance, the defense sector’s continuous need for advanced training solutions to maintain a technological edge is a substantial market driver, contributing to an estimated 40% of the market’s growth.

Barriers & Challenges: Despite the positive outlook, the market faces several challenges. High development costs for sophisticated simulation software, including detailed environmental modeling and accurate physics engines, can be a significant barrier for smaller companies. The rapid pace of drone technology evolution necessitates continuous software updates and adaptation, which can be resource-intensive. Supply chain issues, while less direct for software, can impact the availability of high-performance hardware required for optimal simulation experiences. Regulatory hurdles, such as the certification process for simulator training programs, can also slow down adoption. Competitive pressures from established players and new entrants, alongside the persistent threat of basic, less sophisticated training alternatives, present ongoing challenges. The estimated impact of regulatory delays on market penetration is around 10-15%.

Emerging Opportunities in Drone Simulator Software

Emerging opportunities in the drone simulator software market are abundant, particularly in the expansion of applications beyond traditional defense and commercial use. The growing demand for drone operation in urban air mobility (UAM) and advanced agricultural technology presents lucrative avenues. The development of simulators capable of training pilots for autonomous drone operations, including AI-driven decision-making and complex swarm coordination, represents a significant untapped market. Furthermore, the integration of haptic feedback systems and advanced motion platforms into simulators offers opportunities to create even more immersive and realistic training environments, catering to evolving consumer preferences for highly engaging experiences. The use of simulators for emergency response training, such as disaster management and search and rescue operations, is also a rapidly growing segment.

Growth Accelerators in the Drone Simulator Software Industry

Several catalysts are accelerating long-term growth in the drone simulator software industry. Technological breakthroughs, such as the further integration of AI for predictive analytics in pilot performance and the development of cloud-based simulation platforms, are enhancing scalability and accessibility. Strategic partnerships between simulator software developers, drone manufacturers, and aviation training organizations are crucial for creating comprehensive training ecosystems and expanding market reach. For instance, collaborations that bundle simulator software with drone hardware and certified training programs streamline the adoption process for end-users. Market expansion strategies targeting emerging economies with rapidly growing drone adoption rates, particularly in logistics and infrastructure development, will also play a significant role. The increasing adoption of mixed reality (MR) in simulation is another key accelerator, offering a blend of virtual and real-world elements for enhanced training realism.

Key Players Shaping the Drone Simulator Software Market

- Aegis Technologies

- CAE

- Zen Technologies

- Leonardo

- HELI-X

- Selex ES

- RealFlight Software

- ImmersionRC Ltd.

- L-3 Link Simulation & Training

- Hotprops

Notable Milestones in Drone Simulator Software Sector

- 2019: CAE's acquisition of L3 Technologies' military training business, enhancing its portfolio in advanced simulation solutions.

- 2020: The introduction of advanced VR integration by HELI-X, significantly boosting immersion in drone simulation.

- 2021: Zen Technologies' successful development and deployment of drone simulators for multiple defense forces, highlighting its growing market influence.

- 2022: Leonardo's unveiling of a next-generation simulator platform incorporating AI-driven adaptive learning for drone pilots.

- 2023: RealFlight Software's release of expanded drone models and environmental scenarios, catering to a wider range of hobbyist and professional users.

- 2024: Increased investment in cloud-based simulation infrastructure by various players to enable remote and scalable training.

In-Depth Drone Simulator Software Market Outlook

The drone simulator software market is set for sustained and robust growth, driven by an unwavering demand for proficient drone operators across critical sectors. Future growth accelerators will be centered on continuous technological innovation, including advanced AI integration for realistic autonomous flight simulations and the expansion of mixed reality capabilities for hyper-realistic training. Strategic collaborations between software developers, hardware manufacturers, and educational institutions will further consolidate the market and enhance the accessibility of comprehensive training solutions. The increasing adoption of these sophisticated simulators in emerging markets and for specialized applications like advanced logistics and urban air mobility will unlock new revenue streams. The market's outlook is optimistic, with significant potential for further expansion and innovation as drone technology continues its rapid evolution.

Drone Simulator Software Segmentation

-

1. Application

- 1.1. Defense & Law Enforcement

- 1.2. Commercial

-

2. Type

- 2.1. Windows

- 2.2. Mac

- 2.3. Linux

Drone Simulator Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Drone Simulator Software Regional Market Share

Geographic Coverage of Drone Simulator Software

Drone Simulator Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.88% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Defense & Law Enforcement

- 5.1.2. Commercial

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Windows

- 5.2.2. Mac

- 5.2.3. Linux

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Drone Simulator Software Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Defense & Law Enforcement

- 6.1.2. Commercial

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Windows

- 6.2.2. Mac

- 6.2.3. Linux

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Drone Simulator Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Defense & Law Enforcement

- 7.1.2. Commercial

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Windows

- 7.2.2. Mac

- 7.2.3. Linux

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Drone Simulator Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Defense & Law Enforcement

- 8.1.2. Commercial

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Windows

- 8.2.2. Mac

- 8.2.3. Linux

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Drone Simulator Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Defense & Law Enforcement

- 9.1.2. Commercial

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Windows

- 9.2.2. Mac

- 9.2.3. Linux

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Drone Simulator Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Defense & Law Enforcement

- 10.1.2. Commercial

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Windows

- 10.2.2. Mac

- 10.2.3. Linux

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Drone Simulator Software Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Defense & Law Enforcement

- 11.1.2. Commercial

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Windows

- 11.2.2. Mac

- 11.2.3. Linux

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Aegis Technologies

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 CAE

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Zen Technologies

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Leonardo

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 HELI-X

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Selex ES

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 RealFlight Software

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 ImmersionRC Ltd.

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 L-3 Link Simulation & Training

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Hotprops

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Aegis Technologies

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Drone Simulator Software Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Drone Simulator Software Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Drone Simulator Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Drone Simulator Software Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Drone Simulator Software Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Drone Simulator Software Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Drone Simulator Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Drone Simulator Software Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Drone Simulator Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Drone Simulator Software Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Drone Simulator Software Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Drone Simulator Software Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Drone Simulator Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Drone Simulator Software Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Drone Simulator Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Drone Simulator Software Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Drone Simulator Software Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Drone Simulator Software Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Drone Simulator Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Drone Simulator Software Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Drone Simulator Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Drone Simulator Software Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Drone Simulator Software Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Drone Simulator Software Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Drone Simulator Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Drone Simulator Software Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Drone Simulator Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Drone Simulator Software Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Drone Simulator Software Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Drone Simulator Software Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Drone Simulator Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Drone Simulator Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Drone Simulator Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Drone Simulator Software Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Drone Simulator Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Drone Simulator Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Drone Simulator Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Drone Simulator Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Drone Simulator Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Drone Simulator Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Drone Simulator Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Drone Simulator Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Drone Simulator Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Drone Simulator Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Drone Simulator Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Drone Simulator Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Drone Simulator Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Drone Simulator Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Drone Simulator Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Drone Simulator Software Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Drone Simulator Software?

The projected CAGR is approximately 7.88%.

2. Which companies are prominent players in the Drone Simulator Software?

Key companies in the market include Aegis Technologies, CAE, Zen Technologies, Leonardo, HELI-X, Selex ES, RealFlight Software, ImmersionRC Ltd., L-3 Link Simulation & Training, Hotprops.

3. What are the main segments of the Drone Simulator Software?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Drone Simulator Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Drone Simulator Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Drone Simulator Software?

To stay informed about further developments, trends, and reports in the Drone Simulator Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence