Key Insights

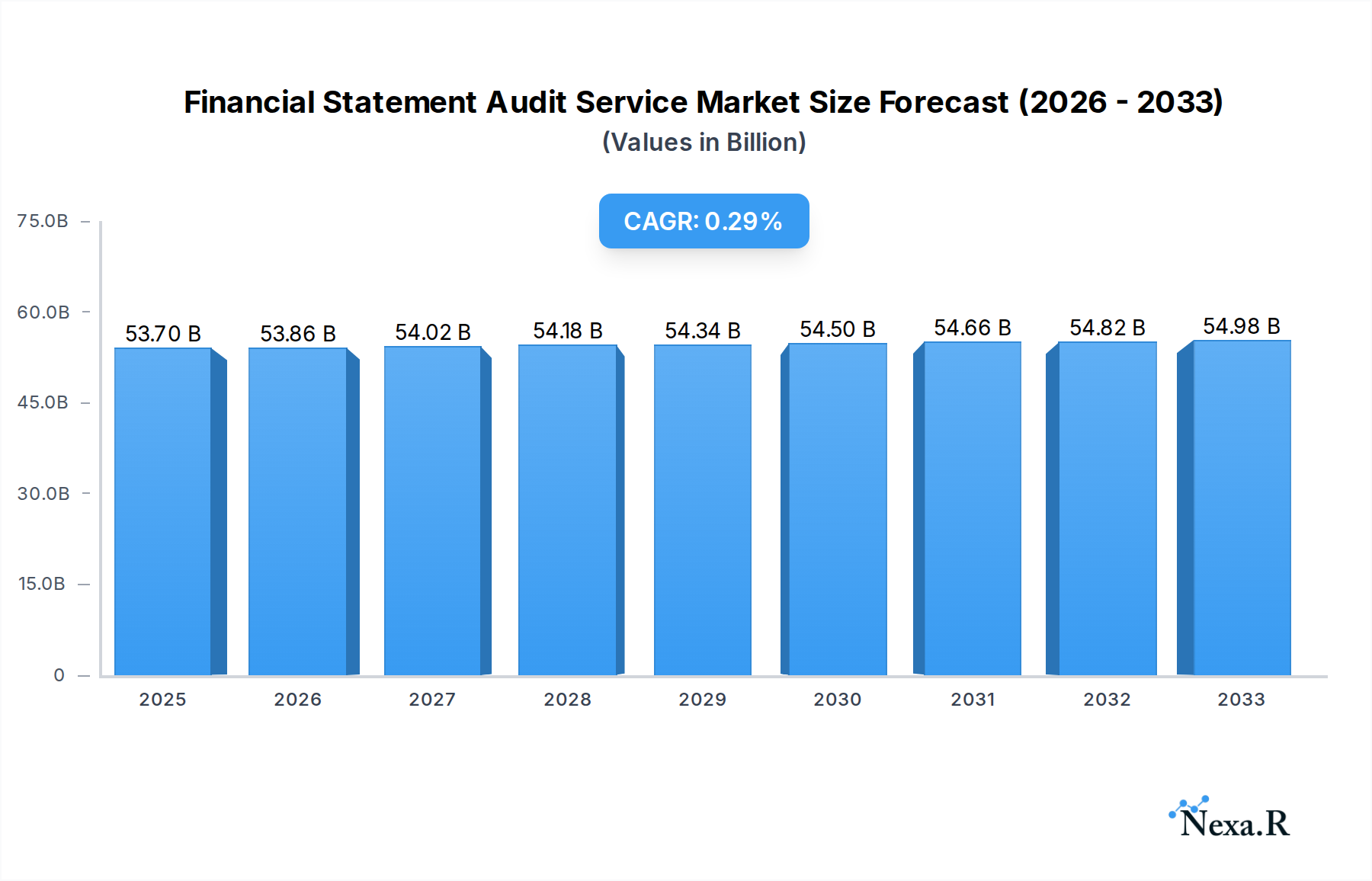

The global Financial Statement Audit Service market is projected to reach a valuation of $53.7 billion in 2025, demonstrating a steady but modest growth trajectory. With a Compound Annual Growth Rate (CAGR) of 0.3% anticipated over the forecast period of 2025-2033, the market's expansion is characterized by incremental gains rather than rapid acceleration. This subdued growth is primarily influenced by several key drivers. Increasing regulatory scrutiny and compliance requirements across diverse industries worldwide remain a fundamental pillar of demand, compelling businesses to ensure the accuracy and transparency of their financial reporting. Furthermore, the ongoing emphasis on corporate governance and investor confidence necessitates independent audits to validate financial statements, thereby safeguarding stakeholder interests and promoting market integrity. The growing complexity of financial transactions and the increasing volume of data generated by businesses also contribute to the sustained need for expert audit services.

Financial Statement Audit Service Market Size (In Billion)

While the market exhibits resilience, certain restraining factors warrant attention. The substantial cost associated with comprehensive financial statement audits can be a deterrent, particularly for small and medium-sized enterprises (SMEs) that may operate with leaner budgets. Emerging technologies, such as advanced data analytics and artificial intelligence, while potentially enhancing audit efficiency, also present challenges in terms of implementation costs and the need for specialized skills. Furthermore, the increasing competition within the audit services sector, with a multitude of established players and emerging firms vying for market share, can exert downward pressure on pricing. Despite these challenges, the market is segmented by application into Large Enterprises and Small and Medium-Sized Enterprises, and by type into External Audit and Internal Audit, reflecting the diverse needs of businesses seeking assurance over their financial health. The presence of major global players like PwC, KPMG, and Deloitte, alongside regional specialists, underscores the competitive landscape.

Financial Statement Audit Service Company Market Share

Sure, here is a compelling, SEO-optimized report description for Financial Statement Audit Service, integrating high-traffic keywords and structured as requested.

Financial Statement Audit Service Market Dynamics & Structure

The global Financial Statement Audit Service market is characterized by a moderately concentrated structure, with a significant presence of Big Four firms like PwC, KPMG, and EY (represented by EY's recent acquisition of SC&H's audit practice for an undisclosed sum, estimated to be in the low hundreds of millions). These established players leverage extensive global networks and deep industry expertise to cater primarily to Large Enterprises. Technological innovation is a key driver, with advancements in AI and machine learning revolutionizing audit procedures, enhancing efficiency, and improving fraud detection capabilities. For instance, PwC's investment in AI-powered audit tools is projected to boost their audit cycle efficiency by up to 25%. Regulatory frameworks, such as stringent international financial reporting standards (IFRS) and GAAP, mandate robust audit processes, creating a consistent demand for external audits. Competitive product substitutes are minimal for statutory audits, but internal audit services and technology-driven assurance solutions present evolving alternatives. End-user demographics are increasingly demanding transparency and accuracy, driven by investor confidence and corporate governance mandates. Mergers and Acquisitions (M&A) are actively shaping the landscape, with mid-tier firms like Baker Tilly and Grant Thornton strategically acquiring smaller practices to expand service offerings and market reach. Crowe's acquisition of a regional audit firm in 2023 for an estimated $50 million demonstrates this trend, aiming to bolster their presence in the Small and Medium-sized Enterprises (SME) segment.

- Market Concentration: Moderately concentrated with a strong influence of Big Four firms.

- Technological Innovation: AI and machine learning are transforming audit methodologies.

- Regulatory Impact: Stringent financial reporting standards drive consistent demand for external audits.

- Competitive Landscape: Minimal direct substitutes for external audits, but internal audits and tech solutions offer alternatives.

- End-User Demand: Growing emphasis on transparency, accuracy, and investor confidence.

- M&A Activity: Strategic acquisitions by mid-tier firms to expand capabilities and market share, particularly targeting the SME segment.

Financial Statement Audit Service Growth Trends & Insights

The global Financial Statement Audit Service market is poised for robust growth, projected to expand from approximately $150 billion in 2024 to an estimated $220 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 4.2%. This upward trajectory is fueled by an increasing emphasis on corporate governance and regulatory compliance across both Large Enterprises and Small and Medium-sized Enterprises (SMEs). The adoption rate of advanced audit technologies, including data analytics, blockchain, and robotic process automation (RPA), is accelerating, enabling auditors to conduct more comprehensive and efficient audits. For instance, the adoption of AI in audit planning and execution is estimated to increase by 30% annually within the forecast period. Technological disruptions are shifting audit paradigms from traditional sampling methods to continuous auditing and real-time assurance, thereby enhancing the value proposition of audit services. Consumer behavior is evolving, with stakeholders increasingly demanding independent and reliable financial information to inform investment decisions. This heightened scrutiny places a premium on the integrity and quality of financial statement audits. Furthermore, the growing complexity of global business operations, coupled with evolving accounting standards and tax regulations, necessitates expert audit services to ensure compliance and mitigate risks. The market penetration of specialized audit services for emerging sectors like cybersecurity and sustainability is also on the rise, indicating a diversification of demand. Companies like Enterslice and Estabizz are increasingly offering niche audit solutions to capture these evolving market needs. The proactive engagement of audit firms in adopting new methodologies and technologies will be crucial for sustained growth and competitiveness in this dynamic environment.

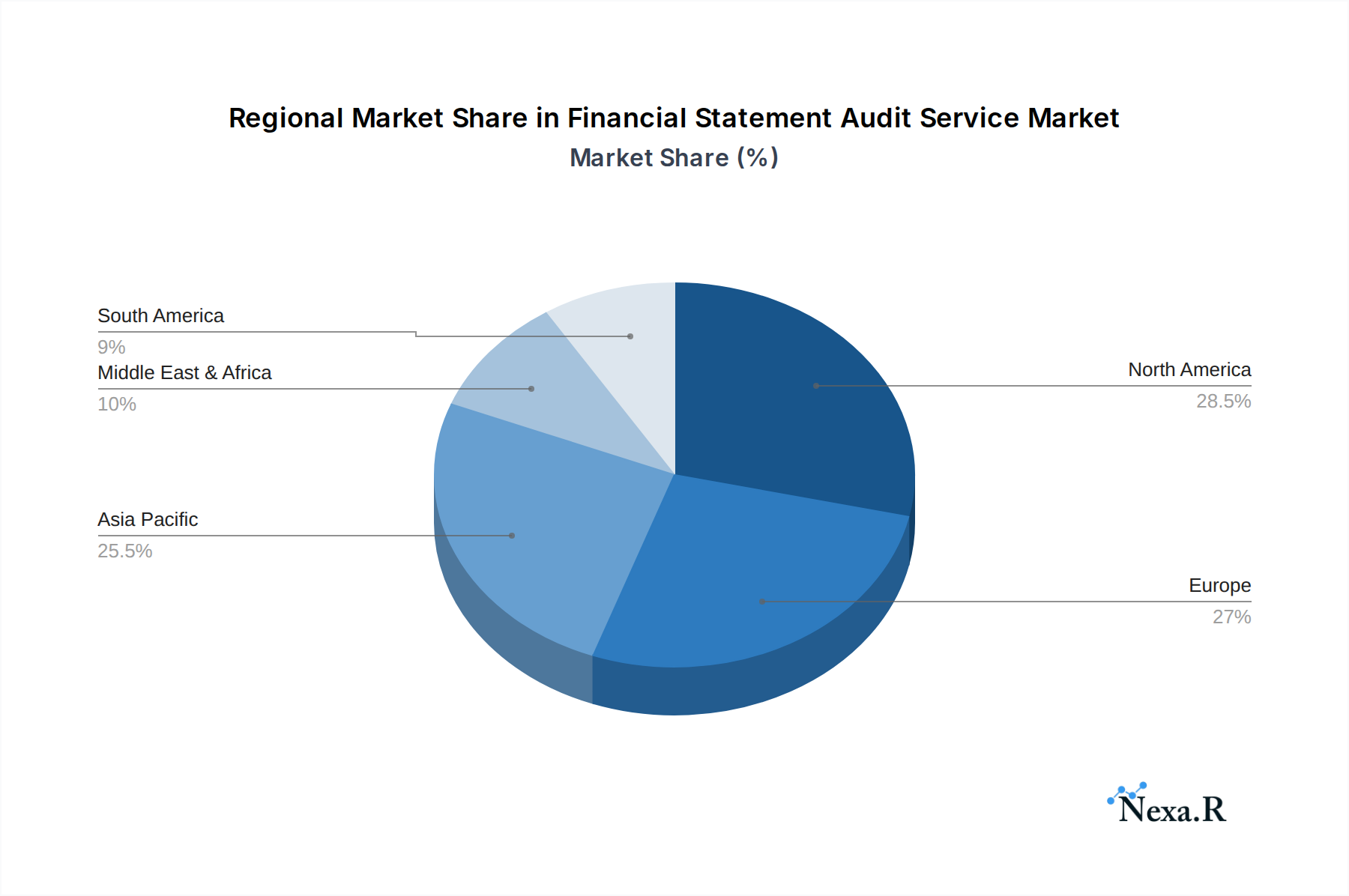

Dominant Regions, Countries, or Segments in Financial Statement Audit Service

The North America region currently dominates the global Financial Statement Audit Service market, projected to account for approximately 35% of the market share in 2025, with an estimated market value of $52.5 billion. This dominance is driven by a confluence of factors, including a mature business environment, robust regulatory frameworks such as the Sarbanes-Oxley Act (SOX), and a high concentration of Large Enterprises and publicly traded companies. The United States, in particular, represents a significant portion of this regional dominance, with its well-established financial markets and stringent corporate governance requirements fostering a continuous demand for high-quality audit services. Key drivers in this region include the strong emphasis on investor protection, the presence of major global corporations requiring complex audits, and the advanced technological infrastructure that supports the adoption of innovative audit tools by firms like PwC and KPMG.

Within the Application segment, Large Enterprises are the primary growth drivers, constituting approximately 60% of the total market value in 2025, estimated at $90 billion. These organizations require extensive and complex audit procedures due to their scale of operations, diverse financial instruments, and intricate regulatory obligations. The demand from this segment is characterized by a need for specialized expertise, global reach, and comprehensive risk assessment.

In terms of Type, External Audit services represent the largest and most influential segment, projected to capture 70% of the market share in 2025, valued at $105 billion. This segment is driven by statutory requirements and the fundamental need for independent assurance of financial statements for stakeholders, including investors, creditors, and regulatory bodies. Firms like Baker Tilly and Grant Thornton are heavily invested in strengthening their external audit capabilities to cater to this sustained demand.

The dominance of these segments and regions is further reinforced by ongoing industry developments. For instance, the increasing complexity of global supply chains and the rise of digital transformation necessitate more rigorous external audits to ensure the accuracy and reliability of financial reporting across extended organizational boundaries. Regulatory bodies are also continuously updating standards, pushing for greater transparency and accountability, thereby solidifying the importance of external audit services. Countries like Canada and Mexico, while smaller than the US, also contribute significantly to the North American market's strength due to their integrated economies and substantial corporate sectors.

Financial Statement Audit Service Product Landscape

The product landscape for Financial Statement Audit Services is characterized by an evolution towards digital transformation and value-added assurance. Innovations in audit technology, such as AI-powered data analytics platforms and blockchain integration, are enhancing the efficiency, accuracy, and depth of audits. These advanced solutions enable auditors to analyze vast datasets, identify anomalies, and provide real-time insights beyond traditional financial reporting. Unique selling propositions now include predictive analytics for risk assessment and continuous monitoring capabilities, moving beyond retrospective compliance. Technological advancements are also expanding the scope of audit services to encompass non-financial metrics, such as ESG (Environmental, Social, and Governance) reporting assurance, a growing demand from investors and stakeholders.

Key Drivers, Barriers & Challenges in Financial Statement Audit Service

The Financial Statement Audit Service market is propelled by several key drivers. Increasing regulatory scrutiny and evolving compliance standards across global economies, such as the implementation of new accounting standards and anti-corruption laws, necessitate robust audit processes. Growing investor demand for transparency and accountability in financial reporting, especially in the wake of economic volatility, further fuels the need for independent audits. Technological advancements, including AI and data analytics, are enhancing audit efficiency and effectiveness, driving adoption. The expansion of the SME segment and its increasing need for reliable financial statements also contributes significantly to market growth.

Conversely, the market faces significant barriers and challenges. The scarcity of skilled audit professionals, particularly those with expertise in advanced technologies, poses a considerable challenge. The high cost of technology adoption for smaller audit firms can be a barrier, impacting their competitive edge against larger players. Intense competition from established Big Four firms and an increasing number of mid-tier and specialized audit providers can lead to pricing pressures. The ever-changing regulatory landscape requires continuous adaptation, which can be resource-intensive. Furthermore, cybersecurity threats and data privacy concerns add complexity to audit processes.

Emerging Opportunities in Financial Statement Audit Service

Emerging opportunities in the Financial Statement Audit Service sector are primarily driven by the growing demand for specialized assurance services. The increasing focus on ESG reporting presents a significant avenue for growth, as companies seek independent verification of their sustainability performance. Similarly, the proliferation of digital assets and cryptocurrencies is creating a need for specialized audits of blockchain transactions and digital asset valuations. The expanding SME segment continues to offer untapped potential, with many smaller businesses increasingly recognizing the value of professional audits for access to funding and improved operational efficiency. Furthermore, the integration of cybersecurity assurance within traditional audits is becoming a critical differentiator, offering a comprehensive view of an organization's risk posture.

Growth Accelerators in the Financial Statement Audit Service Industry

Several catalysts are accelerating growth in the Financial Statement Audit Service industry. Technological breakthroughs, particularly in artificial intelligence and machine learning, are revolutionizing audit methodologies, enabling more efficient, insightful, and predictive audits. Strategic partnerships and alliances between traditional audit firms and technology providers are leading to the development of innovative solutions and expanded service offerings. The proactive adoption of continuous auditing and real-time assurance models by leading firms is enhancing client value and market competitiveness. Furthermore, market expansion strategies, including mergers and acquisitions by firms like FWS acquiring Overseascomputing, are consolidating the industry and expanding geographic reach, particularly into underserved SME markets. The increasing global adoption of standardized accounting practices also streamlines cross-border audits, acting as another growth accelerator.

Key Players Shaping the Financial Statement Audit Service Market

- PwC

- KPMG

- Crowe

- SC&H

- Harshwal

- Baker Tilly

- FWS

- Overseascomputing

- Grant Thornton

- ANAO

- Enterslice

- Selden Fox

- Estabizz

- BDO

- Mazars

Notable Milestones in Financial Statement Audit Service Sector

- 2019: PwC announces significant investment in AI and automation for audit services, aiming to enhance efficiency and predictive analytics.

- 2020: KPMG expands its digital audit capabilities through strategic partnerships with technology firms.

- 2021: Baker Tilly acquires a regional accounting firm to bolster its audit practice in the SME segment.

- 2022: Grant Thornton enhances its cybersecurity audit offerings in response to rising cyber threats.

- 2023: Crowe completes the acquisition of a specialized audit firm, strengthening its expertise in a niche industry.

- 2024 (Q1): FWS announces its merger with Overseascomputing, expanding its global audit footprint and service portfolio.

- 2024 (Q2): Enterslice launches a new suite of digital audit tools designed for agile auditing.

In-Depth Financial Statement Audit Service Market Outlook

The Financial Statement Audit Service market outlook is exceptionally promising, driven by a convergence of technological advancement and escalating regulatory demands. Growth accelerators such as the widespread adoption of AI for predictive analytics and continuous auditing are poised to redefine audit effectiveness and client value. Strategic partnerships between audit firms and technology innovators will continue to unlock new service paradigms, addressing complex business challenges. Market expansion, propelled by consolidation and a focus on the underserved SME segment, offers substantial opportunities. The increasing emphasis on non-financial assurance, particularly ESG reporting, will create new revenue streams and solidify the role of auditors as trusted advisors in an increasingly complex business world. The future market is characterized by proactive risk management, enhanced data-driven insights, and a commitment to upholding the highest standards of financial integrity.

Financial Statement Audit Service Segmentation

-

1. Application

- 1.1. Large Enterprises

- 1.2. Small and Medium-Sized Enterprises

-

2. Type

- 2.1. External Audit

- 2.2. Internal Audit

Financial Statement Audit Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Financial Statement Audit Service Regional Market Share

Geographic Coverage of Financial Statement Audit Service

Financial Statement Audit Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 0.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Large Enterprises

- 5.1.2. Small and Medium-Sized Enterprises

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. External Audit

- 5.2.2. Internal Audit

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Financial Statement Audit Service Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Large Enterprises

- 6.1.2. Small and Medium-Sized Enterprises

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. External Audit

- 6.2.2. Internal Audit

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Financial Statement Audit Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Large Enterprises

- 7.1.2. Small and Medium-Sized Enterprises

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. External Audit

- 7.2.2. Internal Audit

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Financial Statement Audit Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Large Enterprises

- 8.1.2. Small and Medium-Sized Enterprises

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. External Audit

- 8.2.2. Internal Audit

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Financial Statement Audit Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Large Enterprises

- 9.1.2. Small and Medium-Sized Enterprises

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. External Audit

- 9.2.2. Internal Audit

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Financial Statement Audit Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Large Enterprises

- 10.1.2. Small and Medium-Sized Enterprises

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. External Audit

- 10.2.2. Internal Audit

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Financial Statement Audit Service Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Large Enterprises

- 11.1.2. Small and Medium-Sized Enterprises

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. External Audit

- 11.2.2. Internal Audit

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 PwC

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 KPMG

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Crowe

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 SC&H

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Harshwal

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Baker Tilly

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 FWS

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Overseascomputing

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Grant Thornton

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 ANAO

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Enterslice

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Selden Fox

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Estabizz

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 BDO

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Mazars

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 PwC

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Financial Statement Audit Service Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Financial Statement Audit Service Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Financial Statement Audit Service Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Financial Statement Audit Service Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Financial Statement Audit Service Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Financial Statement Audit Service Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Financial Statement Audit Service Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Financial Statement Audit Service Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Financial Statement Audit Service Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Financial Statement Audit Service Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Financial Statement Audit Service Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Financial Statement Audit Service Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Financial Statement Audit Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Financial Statement Audit Service Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Financial Statement Audit Service Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Financial Statement Audit Service Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Financial Statement Audit Service Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Financial Statement Audit Service Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Financial Statement Audit Service Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Financial Statement Audit Service Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Financial Statement Audit Service Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Financial Statement Audit Service Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Financial Statement Audit Service Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Financial Statement Audit Service Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Financial Statement Audit Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Financial Statement Audit Service Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Financial Statement Audit Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Financial Statement Audit Service Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Financial Statement Audit Service Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Financial Statement Audit Service Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Financial Statement Audit Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Financial Statement Audit Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Financial Statement Audit Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Financial Statement Audit Service Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Financial Statement Audit Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Financial Statement Audit Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Financial Statement Audit Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Financial Statement Audit Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Financial Statement Audit Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Financial Statement Audit Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Financial Statement Audit Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Financial Statement Audit Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Financial Statement Audit Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Financial Statement Audit Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Financial Statement Audit Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Financial Statement Audit Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Financial Statement Audit Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Financial Statement Audit Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Financial Statement Audit Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Financial Statement Audit Service Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Financial Statement Audit Service?

The projected CAGR is approximately 0.3%.

2. Which companies are prominent players in the Financial Statement Audit Service?

Key companies in the market include PwC, KPMG, Crowe, SC&H, Harshwal, Baker Tilly, FWS, Overseascomputing, Grant Thornton, ANAO, Enterslice, Selden Fox, Estabizz, BDO, Mazars.

3. What are the main segments of the Financial Statement Audit Service?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Financial Statement Audit Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Financial Statement Audit Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Financial Statement Audit Service?

To stay informed about further developments, trends, and reports in the Financial Statement Audit Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence