Key Insights

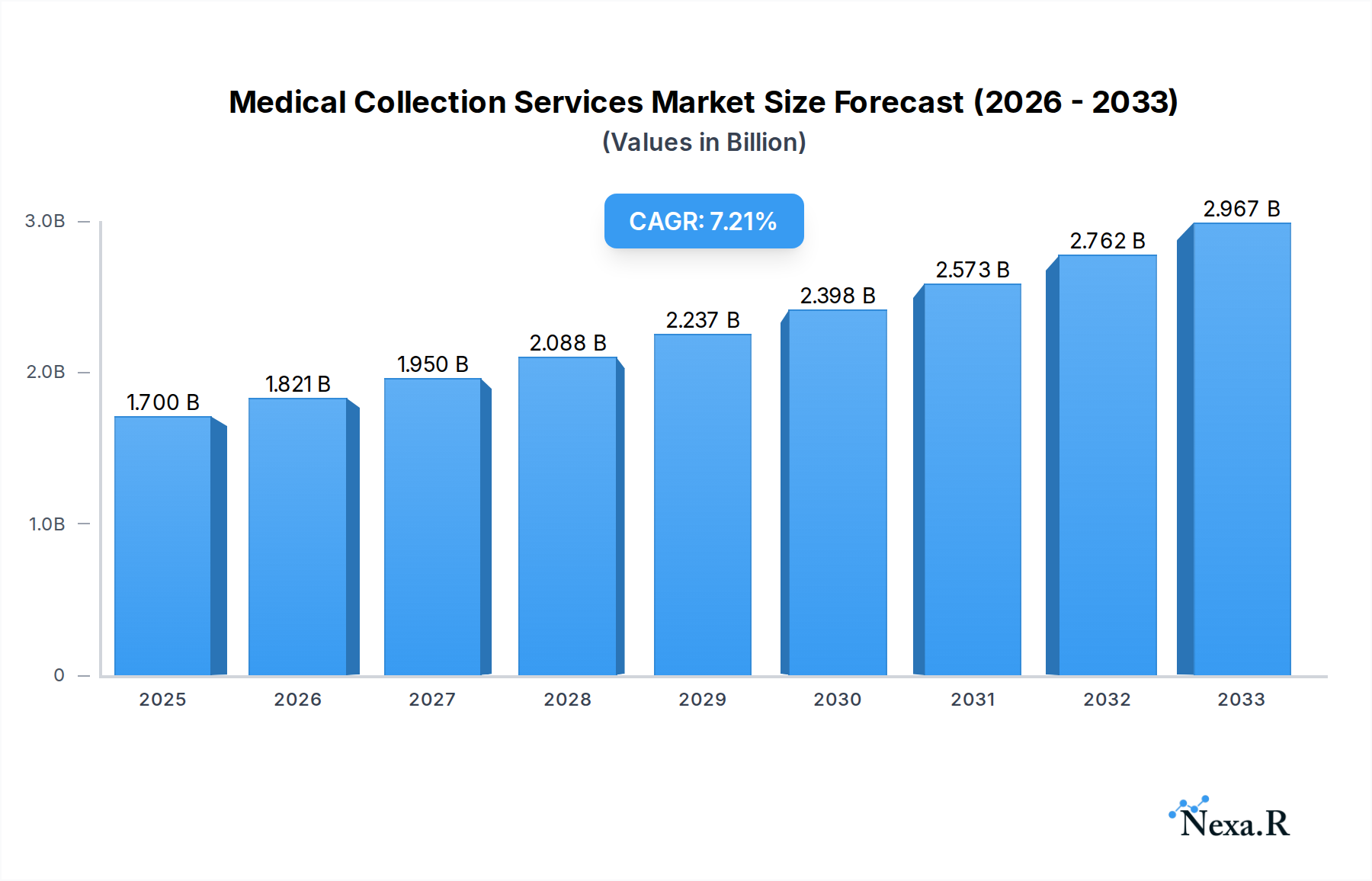

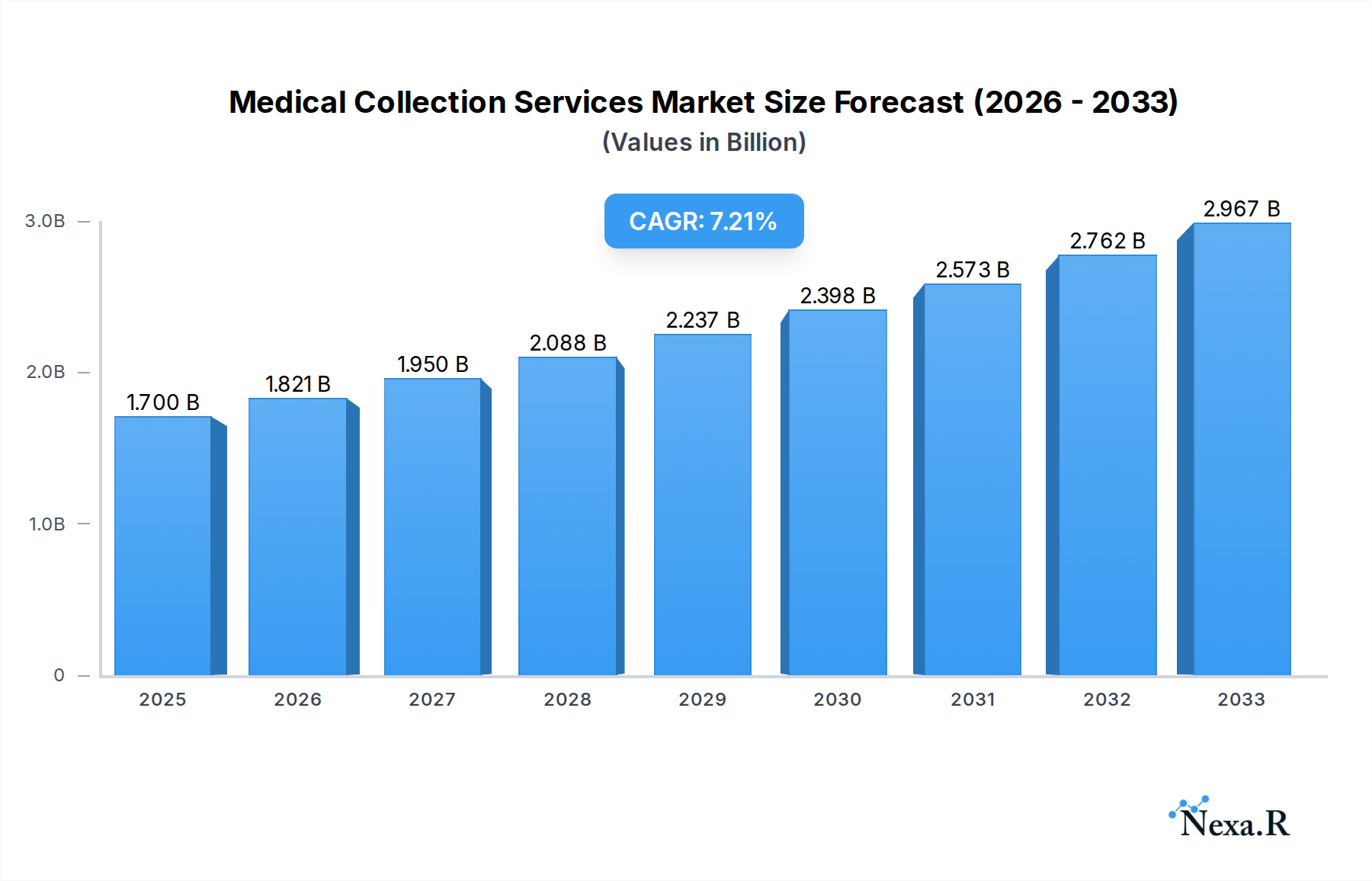

The Medical Collection Services market is poised for robust expansion, driven by an increasing volume of healthcare services and evolving reimbursement landscapes. With a current market size estimated at 1589 million USD and a projected Compound Annual Growth Rate (CAGR) of 7.1%, the market is expected to reach significant valuations by 2033. This growth is primarily fueled by the increasing complexity of medical billing and the rising need for specialized services to manage delinquent accounts. Healthcare providers, particularly independent medical practices and those with a high volume of overdue payments, are increasingly outsourcing their collection efforts to dedicated service providers to optimize revenue cycles and improve financial health. The growing emphasis on patient financial responsibility, coupled with intricate insurance claim processes, creates persistent challenges for in-house billing departments, thereby augmenting the demand for efficient and compliant collection solutions.

Medical Collection Services Market Size (In Billion)

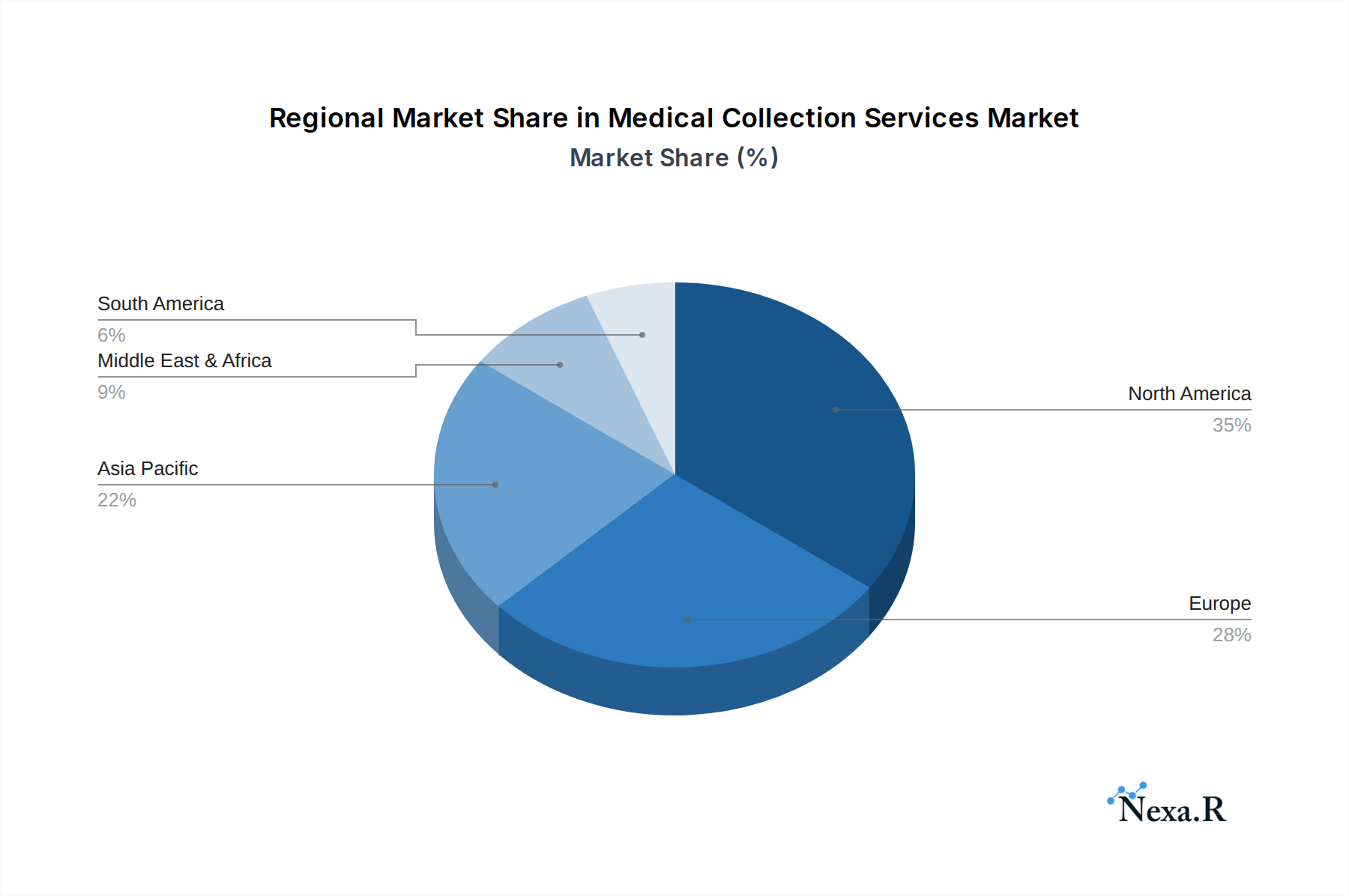

The market is characterized by distinct segmentation, with cloud-based solutions gaining considerable traction due to their scalability, accessibility, and cost-effectiveness, appealing to a wide range of medical practices. On-premises solutions continue to serve organizations with stringent data security requirements or existing infrastructure investments. Key drivers for market growth include the rising healthcare expenditure, the aging global population, and the increasing prevalence of chronic diseases, all contributing to a higher volume of medical services and, consequently, a greater volume of accounts requiring collection. The competitive landscape features a mix of established players and emerging companies, each vying to offer advanced technological solutions, sophisticated analytics, and a strong focus on compliance with healthcare regulations. North America, with its highly developed healthcare infrastructure and established collection practices, currently dominates the market, but significant growth is anticipated in the Asia Pacific region due to its rapidly expanding healthcare sector and increasing adoption of digital solutions.

Medical Collection Services Company Market Share

This comprehensive report provides an in-depth analysis of the global Medical Collection Services market, exploring its dynamic landscape, growth trajectories, and future potential. Designed for industry professionals, investors, and stakeholders, this report offers actionable insights to navigate this evolving sector. The study covers the historical period from 2019 to 2024, with a base year of 2025 and a forecast period extending to 2033.

Medical Collection Services Market Dynamics & Structure

The Medical Collection Services market is characterized by a moderately concentrated structure, with key players like Clearwave, NextStep, Aura, Collectly, MD Charts, Mendable, CWX, MediYeti, Graphium Health, precyse, HCI, Pioneer Collections, CCI Collections, AvadyneHealth, TSI, and IV Medical vying for market dominance. Technological innovation is a significant driver, with cloud-based solutions and AI-powered automation increasingly adopted to enhance efficiency and reduce operational costs. Regulatory frameworks, including HIPAA compliance and evolving debt collection regulations, shape market operations and necessitate robust data security and ethical practices. Competitive product substitutes, such as in-house billing departments and simpler payment gateway solutions, pose a challenge, but specialized medical collection services offer tailored expertise and higher recovery rates. End-user demographics span from large hospital networks to independent medical practices, each with unique collection needs and volumes. Merger and acquisition (M&A) activity is present, with strategic consolidations aiming to expand service offerings and market reach. For instance, there were approximately 12 M&A deals recorded between 2021 and 2023, with an average deal value of $XX million, reflecting the industry's consolidation trend. Innovation barriers include the high cost of advanced technology integration and the need for skilled personnel.

- Market Concentration: Moderately concentrated with a few dominant players and a growing number of niche providers.

- Technological Innovation Drivers: AI, machine learning, automation, cloud computing, and data analytics for improved recovery rates and compliance.

- Regulatory Frameworks: HIPAA, Fair Debt Collection Practices Act (FDCPA), and state-specific regulations influencing operational strategies.

- Competitive Product Substitutes: In-house billing, basic payment processors, and general debt collection agencies.

- End-User Demographics: Hospitals, clinics, physician groups, dental practices, and other healthcare providers.

- M&A Trends: Strategic acquisitions to broaden service portfolios, gain market share, and achieve economies of scale.

Medical Collection Services Growth Trends & Insights

The Medical Collection Services market is poised for robust growth, driven by an increasing volume of medical debt and the growing complexity of healthcare billing. Market size is projected to expand significantly, with an estimated Compound Annual Growth Rate (CAGR) of approximately 7.8% from 2025 to 2033. This growth is fueled by the escalating healthcare expenditures and the subsequent rise in delinquent patient accounts across the United States and globally. The adoption rate of specialized collection services is accelerating as healthcare providers recognize the inefficiencies and lower recovery rates associated with in-house management. Technological disruptions are a key factor; cloud-based platforms, offering enhanced scalability, accessibility, and integration capabilities with Electronic Health Records (EHRs), are gaining widespread acceptance. AI and machine learning algorithms are revolutionizing debt collection by enabling predictive analytics for identifying high-risk accounts, automating communication workflows, and personalizing collection strategies. This leads to improved collection rates and a better patient experience. Consumer behavior shifts are also influencing the market. Patients are increasingly expecting transparent billing processes and flexible payment options, putting pressure on providers to adopt more patient-centric collection approaches. This necessitates collection agencies to move beyond traditional methods towards empathetic and data-driven engagement. For example, the implementation of AI-driven communication tools has shown to increase patient engagement rates by up to 25%. The market penetration of dedicated medical collection services is expected to reach XX% by 2030. The estimated market size in the base year 2025 is valued at $XX billion and is projected to reach $XX billion by 2033.

Dominant Regions, Countries, or Segments in Medical Collection Services

The United States stands as the dominant region in the Medical Collection Services market, driven by its expansive healthcare system, high healthcare costs, and a significant volume of patient debt. Within the US, segments such as "Medical Practices with Many Delinquent Accounts" represent a substantial portion of the market, demanding specialized solutions for effective debt recovery. The "Cloud-based" service type is experiencing the most rapid growth, outpacing "On-premises" solutions due to its scalability, cost-effectiveness, and ease of integration. Key drivers for US dominance include robust economic policies supporting healthcare access, a well-developed technological infrastructure, and a large patient population generating considerable medical receivables. The regulatory landscape, while complex, also fosters specialized collection services that ensure compliance. For instance, the sheer volume of medical billing and collection challenges in the US healthcare system, estimated at over $XXX billion in outstanding patient balances annually, creates a persistent demand for these services. The market share for cloud-based medical collection services in the US is projected to reach XX% by 2028.

- Dominant Country: United States, due to its large healthcare market and high medical debt levels.

- Leading Application Segment: Medical Practices with Many Delinquent Accounts, driven by the need for specialized recovery strategies.

- Fastest-Growing Service Type: Cloud-based solutions, offering scalability, accessibility, and cost efficiencies.

- Key Growth Drivers in the US:

- High healthcare expenditures and increasing patient deductibles.

- Complex medical billing and coding processes.

- Technological advancements in billing and collection software.

- Regulatory compliance requirements.

- Growing adoption of RCM (Revenue Cycle Management) solutions.

Medical Collection Services Product Landscape

The product landscape in Medical Collection Services is rapidly evolving, with a strong emphasis on intelligent automation and patient-centric solutions. Innovations include AI-powered predictive analytics for prioritizing collection efforts, automated patient communication platforms employing natural language processing (NLP) for personalized outreach, and secure cloud-based systems that seamlessly integrate with Electronic Health Records (EHRs) and practice management software. Performance metrics are typically measured by collection rates, recovery percentages, cost-per-dollar collected, and patient satisfaction scores. Unique selling propositions often revolve around advanced data analytics for fraud detection, compliance assurance features, and a patient-friendly approach that aims to resolve outstanding balances without damaging patient relationships. For example, new platforms are leveraging machine learning to predict patient payment behavior with over 85% accuracy.

Key Drivers, Barriers & Challenges in Medical Collection Services

Key Drivers:

The Medical Collection Services market is propelled by several key drivers. Increasing healthcare costs and rising patient responsibility for medical bills directly translate to a larger pool of delinquent accounts. Technological advancements, particularly in AI, automation, and cloud computing, enable more efficient, data-driven, and compliant collection processes. Growing regulatory scrutiny mandates specialized expertise to ensure adherence to laws like HIPAA and FDCPA, driving demand for professional collection services. The desire of healthcare providers to focus on patient care rather than administrative tasks also fuels the outsourcing of collection functions.

Barriers & Challenges:

Despite strong growth potential, the market faces significant barriers and challenges. Regulatory complexity and evolving compliance requirements pose a constant challenge, demanding continuous adaptation and investment in legal expertise. Public perception and ethical concerns surrounding debt collection practices can lead to reputational risks for providers. The need for substantial upfront investment in technology and skilled personnel can be a barrier for smaller players. Furthermore, increasing competition from both specialized agencies and in-house solutions, coupled with potential data security breaches, presents ongoing challenges to market participants. Supply chain issues are less of a direct concern for services, but the reliance on technological infrastructure can be affected by broader tech supply chain disruptions.

Emerging Opportunities in Medical Collection Services

Emerging opportunities in the Medical Collection Services market are centered around leveraging advanced technologies and catering to evolving patient expectations. The increasing adoption of telehealth and remote patient monitoring creates new avenues for billing and collection, requiring specialized approaches. There is a significant opportunity in developing and deploying patient-centric collection strategies that focus on education, flexible payment plans, and empathetic communication, enhancing patient satisfaction and improving recovery rates. Furthermore, the untapped potential in specialized healthcare niches, such as long-term care facilities and mental health services, offers fertile ground for tailored collection solutions. The integration of blockchain technology for secure and transparent patient payment records is another nascent but promising area.

Growth Accelerators in the Medical Collection Services Industry

Several catalysts are accelerating long-term growth in the Medical Collection Services industry. The continuous innovation in AI and machine learning algorithms is a primary growth accelerator, enabling predictive analytics, intelligent automation, and personalized patient engagement strategies that significantly boost collection efficiency. Strategic partnerships between collection agencies and healthcare technology providers, particularly EHR vendors and RCM solution developers, are creating integrated ecosystems that streamline the entire revenue cycle. Market expansion strategies, including entering new geographical markets and acquiring smaller, specialized collection firms, are also driving growth. Furthermore, the increasing focus on patient experience as a differentiator is pushing providers to adopt more ethical and transparent collection practices, which in turn fuels demand for agencies that can deliver both results and positive patient interactions.

Key Players Shaping the Medical Collection Services Market

- Clearwave

- NextStep

- Aura

- Collectly

- MD Charts

- Mendable

- CWX

- MediYeti

- Graphium Health

- precyse

- HCI

- Pioneer Collections

- CCI Collections

- AvadyneHealth

- TSI

- IV Medical

- The Pre-Op Tool

Notable Milestones in Medical Collection Services Sector

- 2019: Increased adoption of AI-driven predictive analytics in collection agencies to forecast patient payment likelihood.

- 2020: Significant shift towards cloud-based solutions driven by remote work trends and the need for scalable infrastructure.

- 2021: Emergence of patient-centric collection platforms focusing on empathy and flexible payment options.

- 2022: Intensified focus on data security and compliance with evolving privacy regulations.

- 2023: Strategic partnerships between collection agencies and EHR providers to enhance data integration and workflow efficiency.

- 2024: Growing implementation of automated communication tools, including chatbots and personalized email campaigns.

In-Depth Medical Collection Services Market Outlook

The Medical Collection Services market is set for sustained and accelerated growth, driven by the persistent need for efficient revenue cycle management in healthcare. Future market potential is significant, fueled by ongoing technological advancements, particularly in AI and automation, which will continue to enhance collection effectiveness and compliance. Strategic opportunities lie in further specializing services for niche healthcare sectors and developing innovative, patient-friendly collection models. The increasing complexity of healthcare billing and the growing patient responsibility for costs will ensure a consistent demand for expert collection services. Healthcare providers will continue to outsource these functions to focus on core competencies, creating a favorable environment for market expansion and increased revenue realization.

Medical Collection Services Segmentation

-

1. Application

- 1.1. Medical Practices with Many Delinquent Accounts

- 1.2. Independent Medical Practices

-

2. Type

- 2.1. Cloud-based

- 2.2. On-premises

Medical Collection Services Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Medical Collection Services Regional Market Share

Geographic Coverage of Medical Collection Services

Medical Collection Services REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Medical Collection Services Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Medical Practices with Many Delinquent Accounts

- 5.1.2. Independent Medical Practices

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Cloud-based

- 5.2.2. On-premises

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Medical Collection Services Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Medical Practices with Many Delinquent Accounts

- 6.1.2. Independent Medical Practices

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Cloud-based

- 6.2.2. On-premises

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Medical Collection Services Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Medical Practices with Many Delinquent Accounts

- 7.1.2. Independent Medical Practices

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Cloud-based

- 7.2.2. On-premises

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Medical Collection Services Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Medical Practices with Many Delinquent Accounts

- 8.1.2. Independent Medical Practices

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Cloud-based

- 8.2.2. On-premises

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Medical Collection Services Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Medical Practices with Many Delinquent Accounts

- 9.1.2. Independent Medical Practices

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Cloud-based

- 9.2.2. On-premises

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Medical Collection Services Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Medical Practices with Many Delinquent Accounts

- 10.1.2. Independent Medical Practices

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Cloud-based

- 10.2.2. On-premises

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Clearwave

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 NextStep

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Aura

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Collectly

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 MD Charts

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Mendable

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 CWX

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 MediYeti

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Graphium Health

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 precyse

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 HCI

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Pioneer Collections

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 CCI Collections

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 AvadyneHealth

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 TSI

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 IV Medical

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 The Pre-Op Tool

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Clearwave

List of Figures

- Figure 1: Global Medical Collection Services Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Medical Collection Services Revenue (million), by Application 2025 & 2033

- Figure 3: North America Medical Collection Services Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Medical Collection Services Revenue (million), by Type 2025 & 2033

- Figure 5: North America Medical Collection Services Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Medical Collection Services Revenue (million), by Country 2025 & 2033

- Figure 7: North America Medical Collection Services Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Medical Collection Services Revenue (million), by Application 2025 & 2033

- Figure 9: South America Medical Collection Services Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Medical Collection Services Revenue (million), by Type 2025 & 2033

- Figure 11: South America Medical Collection Services Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Medical Collection Services Revenue (million), by Country 2025 & 2033

- Figure 13: South America Medical Collection Services Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Medical Collection Services Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Medical Collection Services Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Medical Collection Services Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Medical Collection Services Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Medical Collection Services Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Medical Collection Services Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Medical Collection Services Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Medical Collection Services Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Medical Collection Services Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Medical Collection Services Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Medical Collection Services Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Medical Collection Services Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Medical Collection Services Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Medical Collection Services Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Medical Collection Services Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Medical Collection Services Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Medical Collection Services Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Medical Collection Services Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Collection Services Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Medical Collection Services Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Medical Collection Services Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Medical Collection Services Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Medical Collection Services Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Medical Collection Services Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Medical Collection Services Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Medical Collection Services Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Medical Collection Services Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Medical Collection Services Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Medical Collection Services Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Medical Collection Services Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Medical Collection Services Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Medical Collection Services Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Medical Collection Services Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Medical Collection Services Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Medical Collection Services Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Medical Collection Services Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Medical Collection Services Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Collection Services?

The projected CAGR is approximately 7.1%.

2. Which companies are prominent players in the Medical Collection Services?

Key companies in the market include Clearwave, NextStep, Aura, Collectly, MD Charts, Mendable, CWX, MediYeti, Graphium Health, precyse, HCI, Pioneer Collections, CCI Collections, AvadyneHealth, TSI, IV Medical, The Pre-Op Tool.

3. What are the main segments of the Medical Collection Services?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1589 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Collection Services," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Collection Services report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Collection Services?

To stay informed about further developments, trends, and reports in the Medical Collection Services, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence