Key Insights

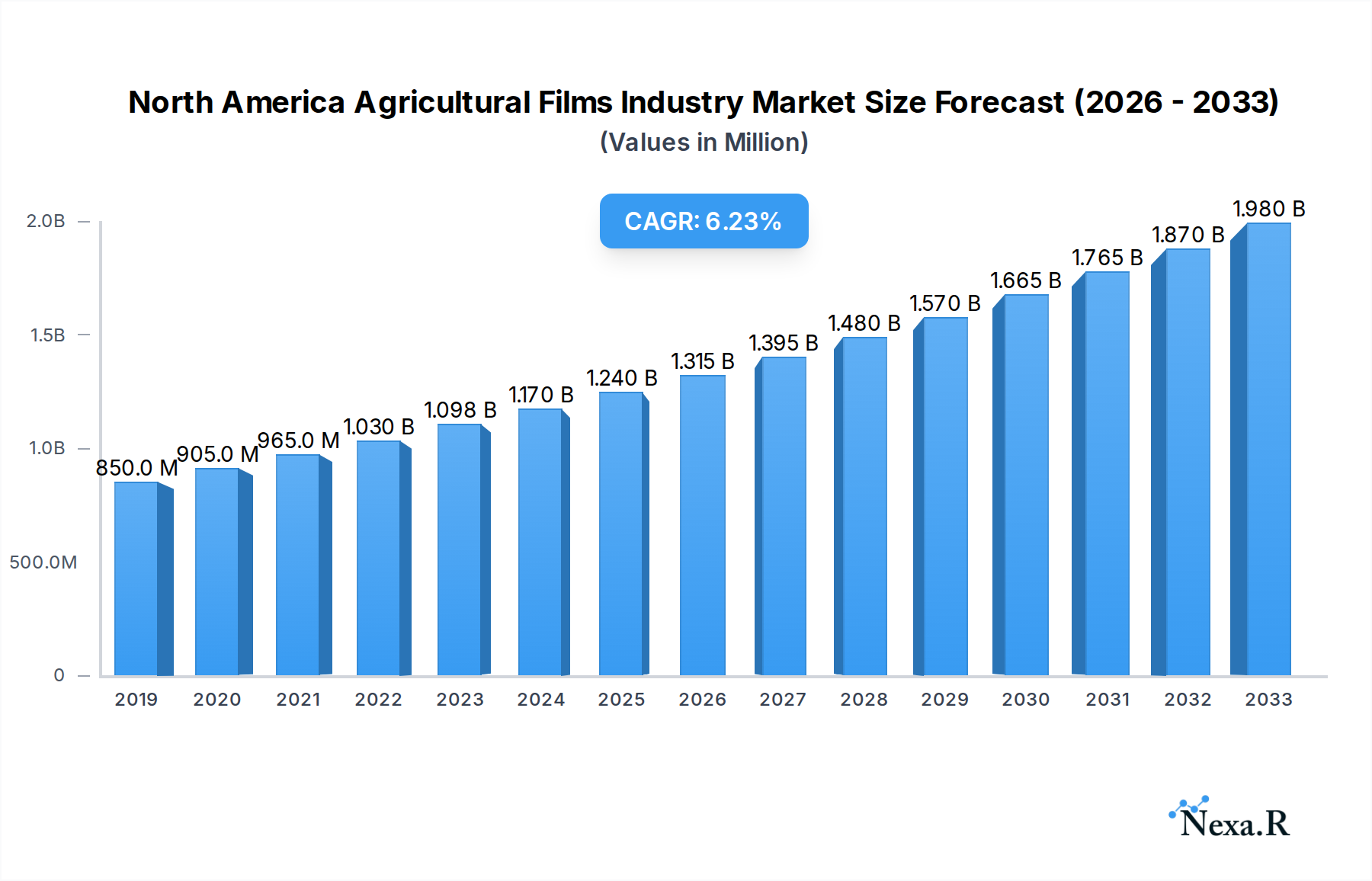

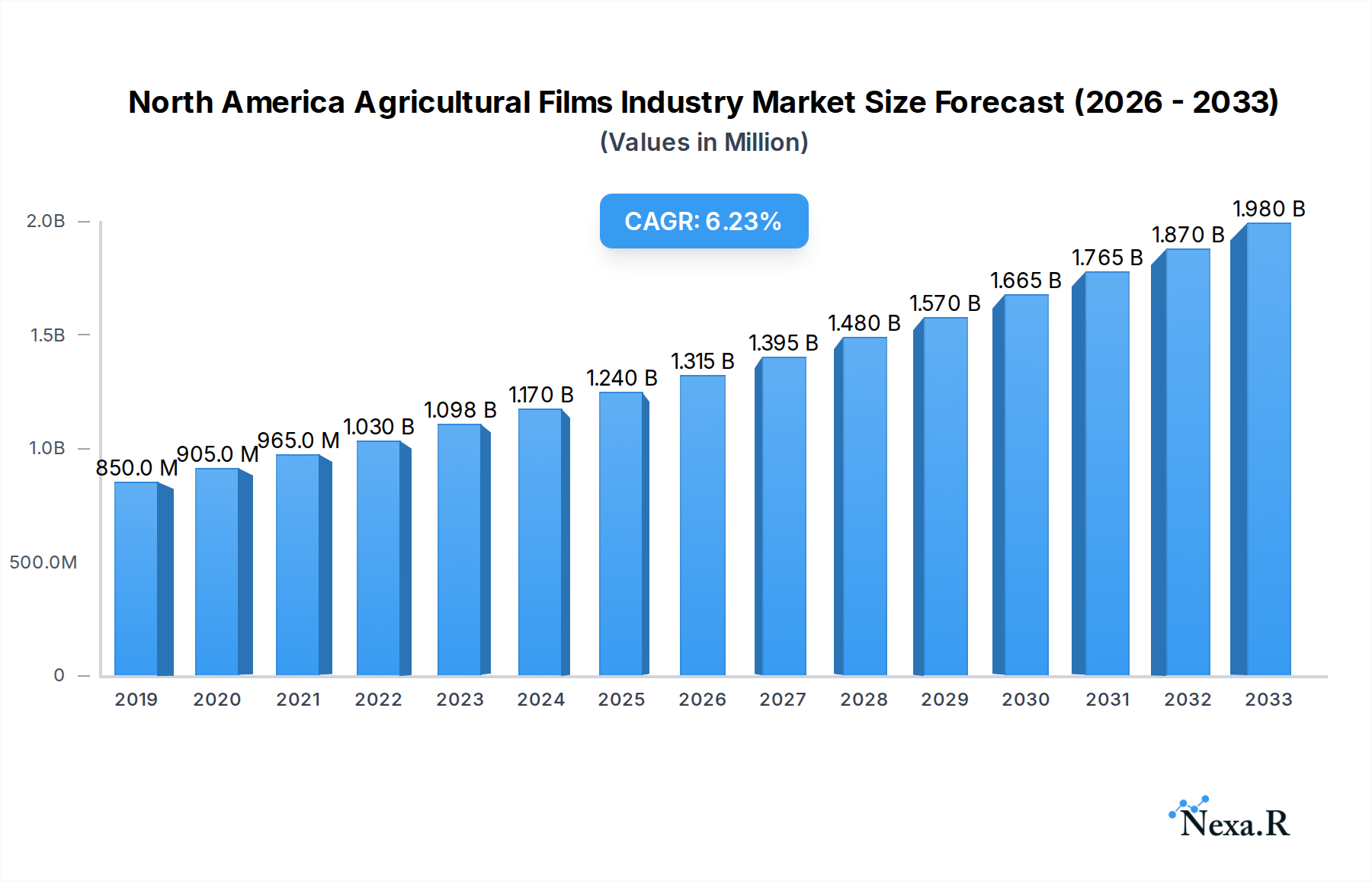

The North American agricultural films market is poised for significant expansion, projected to reach $1.24 billion by 2025. This growth is underpinned by a robust Compound Annual Growth Rate (CAGR) of 6.20%, indicating sustained momentum over the forecast period. Key drivers for this upward trajectory include the increasing demand for enhanced crop yields and protection, the adoption of advanced agricultural practices, and the rising need for efficient resource management in the face of climate change and growing food security concerns. The market is segmented across production, consumption, import/export value and volume, and price trends, offering a comprehensive view of its dynamics. Berry Plastics Corporation, ExxonMobil Chemical, and BASF are among the prominent players shaping this landscape, contributing to innovation and market competitiveness.

North America Agricultural Films Industry Market Size (In Million)

The agricultural films industry in North America is being propelled by several key trends. The development of specialized films, such as those offering UV resistance, improved light diffusion, and enhanced barrier properties, is meeting the evolving needs of modern agriculture. Furthermore, the increasing focus on sustainability is driving the adoption of biodegradable and recyclable agricultural films, aligning with environmental regulations and consumer preferences. However, the market also faces certain restraints, including the fluctuating prices of raw materials like polyethylene, which can impact production costs and profitability. Geopolitical factors and trade policies could also present challenges to the import and export segments. Despite these challenges, the overall outlook for the North American agricultural films market remains strong, driven by innovation, increasing adoption rates, and the fundamental importance of agriculture in the region.

North America Agricultural Films Industry Company Market Share

North America Agricultural Films Industry Market Dynamics & Structure

The North America agricultural films industry is characterized by a moderate to high market concentration, with a few major players holding significant market share. Technological innovation is a primary driver, fueled by the demand for enhanced crop yields, improved resource management, and sustainable farming practices. Key innovations include advanced barrier properties, UV stabilization, biodegradability, and smart film technologies for controlled environments. The regulatory landscape, encompassing environmental regulations and food safety standards, plays a crucial role in shaping product development and market access. Competitive product substitutes, such as traditional mulching materials and alternative cultivation methods, are present but often lack the comprehensive benefits offered by modern agricultural films. End-user demographics are shifting, with increasing adoption by both large-scale commercial farms and smaller, technologically-inclined operations. Mergers and acquisitions (M&A) are a notable trend, as established companies seek to expand their product portfolios, geographic reach, and technological capabilities.

- Market Concentration: Dominated by key players such as Berry Plastics Corporation, ExxonMobil Chemical, BASF, The Dow Chemical Company, and RK RKW SE, who collectively hold an estimated 50-60% market share.

- Technological Innovation: Driven by demand for increased crop yields, reduced water usage, and enhanced protection against pests and extreme weather.

- Regulatory Frameworks: Stringent environmental regulations in countries like the US and Canada are pushing for the development of sustainable and biodegradable agricultural films.

- Competitive Substitutes: While present, traditional methods often require more labor and offer less precise control over growing conditions.

- End-User Demographics: Growing interest from organic farming sectors and controlled environment agriculture (CEA) operations.

- M&A Trends: Recent years have seen a rise in strategic acquisitions aimed at consolidating market presence and acquiring specialized technologies, with an estimated 5-8 significant M&A deals annually over the historical period.

North America Agricultural Films Industry Growth Trends & Insights

The North America agricultural films industry is poised for robust growth, projected to expand significantly from an estimated market size of USD 2,500 Million in 2025 to USD 3,800 Million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 5.2% during the forecast period. This expansion is underpinned by several interconnected trends, including the escalating demand for food security, the imperative to optimize agricultural resource utilization, and the increasing adoption of advanced farming techniques. As the global population continues to grow, so does the pressure on agricultural output, making efficient crop production paramount. Agricultural films play a vital role in this by creating microclimates that enhance plant growth, protect crops from environmental stressors like frost and pests, and significantly reduce water evaporation, a critical concern in many North American agricultural regions.

The adoption rate of agricultural films is steadily increasing across diverse farming segments. This surge is driven by the clear return on investment that farmers experience through improved crop yields, reduced pesticide and fertilizer usage, and extended growing seasons. Furthermore, technological disruptions are continuously reshaping the market landscape. Innovations such as multi-layer films with enhanced UV resistance, improved light diffusion properties, and increased durability are becoming standard. The development of biodegradable and compostable agricultural films is also gaining significant traction, driven by growing environmental consciousness and stricter regulations concerning plastic waste. Consumers are increasingly demanding sustainably produced food, and this preference is filtering back through the supply chain, incentivizing farmers to adopt eco-friendly solutions like biodegradable mulches.

Consumer behavior shifts are also playing a crucial role. The growing popularity of precision agriculture and controlled environment agriculture (CEA) – including greenhouses and vertical farms – is creating a new wave of demand for specialized agricultural films. These applications often require films with specific light transmission properties, humidity control capabilities, and thermal insulation. Farmers are becoming more sophisticated in their approach to crop management, viewing agricultural films not just as protective coverings but as integral components of an integrated farming system designed for maximum efficiency and sustainability. The market penetration of advanced agricultural films is expected to deepen as more farmers recognize their value in addressing contemporary agricultural challenges, from climate change impacts to the need for more sustainable and resource-efficient food production systems.

Dominant Regions, Countries, or Segments in North America Agricultural Films Industry

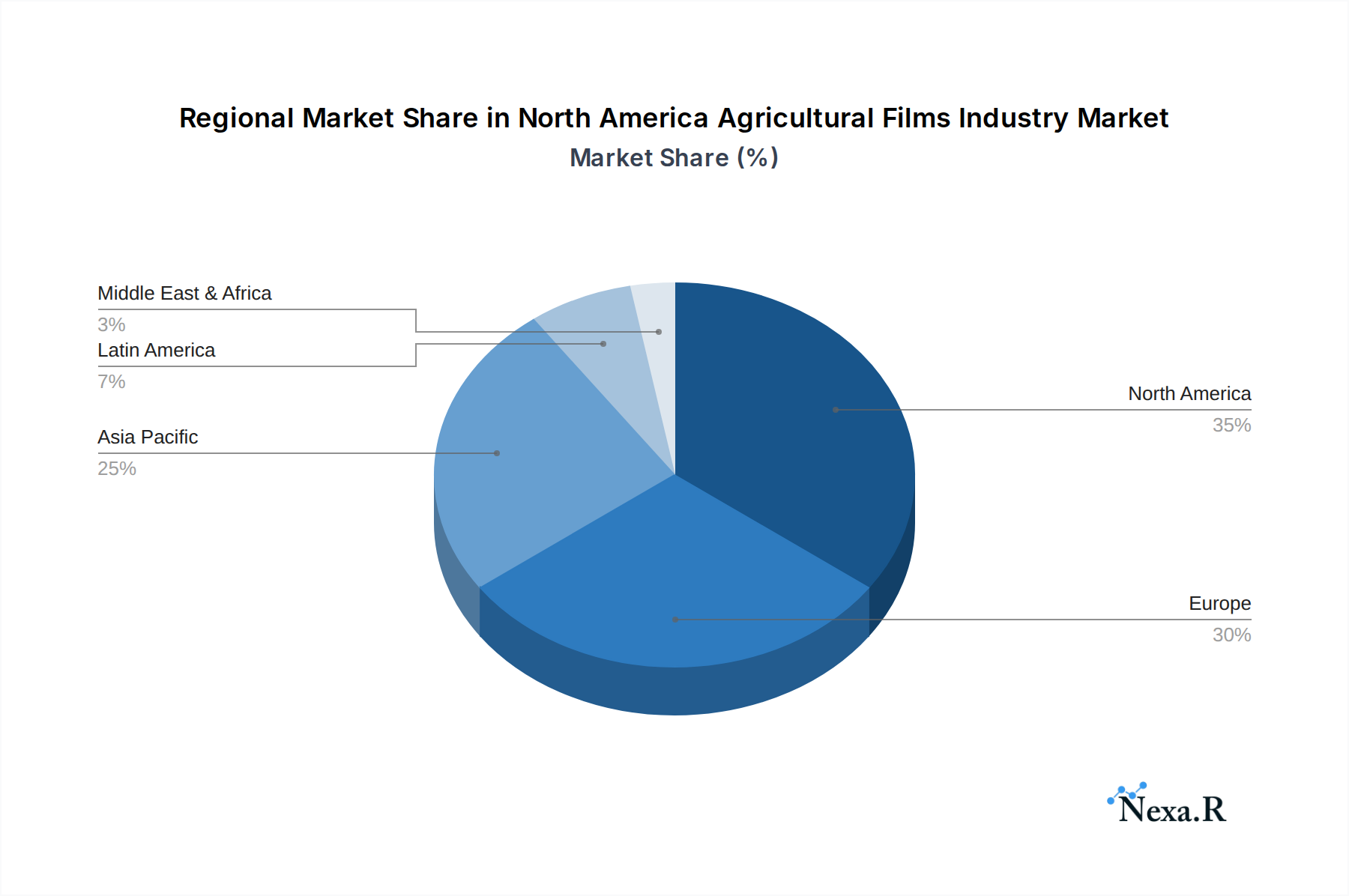

The North America agricultural films industry exhibits dominance across various segments and geographic regions, each driven by distinct factors. From a Production Analysis perspective, the United States, with its vast agricultural land and advanced manufacturing capabilities, stands as the primary production hub, contributing an estimated 75% of the region's total agricultural film output. Canada follows, leveraging its significant agricultural sector and growing interest in specialized farming.

In terms of Consumption Analysis, the U.S. agricultural sector also leads, consuming approximately 70% of the total agricultural films. This is attributed to its diverse range of crops, from large-scale corn and soybean cultivation to specialized fruit and vegetable farming, all of which benefit from various agricultural film applications like mulching, greenhouse coverings, and silage films. Mexico, while a smaller player in production, is a significant and growing consumer, particularly for greenhouse applications and crop protection in its burgeoning horticultural export industry.

The Import Market Analysis (Value & Volume) reveals a dynamic landscape. While intra-regional trade is substantial, the U.S. remains a net importer for certain specialized film types not produced domestically. Mexico, in particular, is a key importer of high-performance greenhouse films and UV-stabilized mulches. The value of imports is estimated at USD 450 Million in 2025, with a projected volume of 180 Million units.

Conversely, the Export Market Analysis (Value & Volume) highlights the U.S. as a significant exporter of agricultural films, particularly to Latin American countries and certain niche markets in Europe. The total export value is estimated at USD 380 Million in 2025, with a volume of 150 Million units. This export strength is driven by the technological sophistication and quality of American-manufactured films.

The Price Trend Analysis indicates a steady upward trend, influenced by raw material costs (primarily polyethylene), manufacturing overheads, and the increasing demand for specialized, higher-value films with advanced properties. The average price of agricultural films is estimated to be USD 2.50 per unit in 2025, with variations based on film type and application.

The dominant segment driving market growth is greenhouse films, accounting for an estimated 35% of the market share. This is fueled by the increasing adoption of controlled environment agriculture (CEA) to mitigate the impacts of climate change, improve crop quality, and ensure year-round production. Mulching films follow closely, driven by their proven ability to conserve water, suppress weeds, and improve soil temperature, contributing an estimated 30% to the market. Silage films, crucial for livestock feed preservation, represent another significant segment.

North America Agricultural Films Industry Product Landscape

The North America agricultural films industry is characterized by a diverse and innovative product landscape. Key innovations focus on enhancing crop performance, resource efficiency, and environmental sustainability. This includes advanced multi-layer polyethylene films with superior UV resistance and durability for extended field life, offering protection against harsh weather and solar degradation. Light-diffusing films improve canopy penetration and reduce overheating in greenhouses, promoting healthier plant growth. Biodegradable and compostable films, made from polylactic acid (PLA) or other bio-based polymers, are emerging as a critical solution to plastic waste, breaking down naturally after use. Smart films incorporating antimicrobial properties or controlled gas release are also being developed to further optimize growing conditions and reduce disease incidence. These product advancements are driven by the need for higher yields, reduced chemical inputs, and greater environmental responsibility in agriculture.

Key Drivers, Barriers & Challenges in North America Agricultural Films Industry

Key Drivers:

- Increasing demand for food security: The need to feed a growing population necessitates enhanced agricultural productivity, where films play a vital role in optimizing crop yields.

- Water scarcity and conservation efforts: Agricultural films, particularly mulches, significantly reduce water evaporation, making them crucial in arid and semi-arid regions.

- Advancements in agricultural technology: The rise of precision agriculture and controlled environment agriculture (CEA) drives demand for specialized, high-performance films.

- Growing adoption of sustainable farming practices: The market is increasingly leaning towards biodegradable and recyclable film options.

Key Barriers & Challenges:

- Raw material price volatility: Fluctuations in polyethylene and other polymer prices directly impact manufacturing costs and film pricing.

- Disposal and end-of-life management of conventional films: The environmental impact of non-biodegradable films presents a significant challenge, leading to regulatory pressures and disposal costs.

- High initial investment for some advanced films: While offering long-term benefits, the upfront cost of certain specialized or biodegradable films can be a deterrent for some farmers.

- Competition from alternative farming methods: Traditional open-field farming and other crop protection methods can sometimes present a less technologically integrated alternative.

- Supply chain disruptions: Global events can impact the availability and cost of raw materials and finished products.

Emerging Opportunities in North America Agricultural Films Industry

Emerging opportunities lie in the continued development and market penetration of biodegradable and compostable agricultural films, addressing growing environmental concerns and regulatory mandates. The expansion of controlled environment agriculture (CEA), including vertical farming and advanced greenhouse operations, presents a significant avenue for specialized films with tailored light transmission, thermal insulation, and humidity control properties. Furthermore, the development of smart films with integrated sensors for real-time environmental monitoring and disease detection offers a pathway to enhance crop management and predictive analytics. The increasing focus on organic farming also presents a niche for certified organic-compatible film solutions.

Growth Accelerators in the North America Agricultural Films Industry Industry

Growth in the North America agricultural films industry is being significantly accelerated by technological breakthroughs in polymer science, leading to the creation of more durable, efficient, and sustainable film options. Strategic partnerships between film manufacturers and agricultural technology companies are fostering innovation and creating integrated solutions for farmers. Market expansion strategies, including educating farmers on the benefits and ROI of advanced films, and increasing accessibility through wider distribution networks, are also key growth accelerators. The proactive adoption of films in response to climate change impacts, such as extreme weather events and water scarcity, further propels market growth.

Key Players Shaping the North America Agricultural Films Industry Market

- Berry Plastics Corporation

- ExxonMobil Chemical

- BASF

- The Dow Chemical Company

- RKW S

- AB Rani Plast Oy

- Hyplast NV

- Britton Group

- Trioplast Industries AB

- Armando Alvarez Group

Notable Milestones in North America Agricultural Films Industry Sector

- 2020: Increased research and development into biodegradable polyethylene film alternatives.

- 2021: Launch of new multi-layer greenhouse films with enhanced UV resistance and light diffusion properties.

- 2022: Growing regulatory focus on plastic waste management in agriculture, driving demand for sustainable solutions.

- 2023: Significant investment in expanding production capacity for high-performance agricultural films to meet rising demand.

- 2024: Introduction of advanced silage films with improved barrier properties to minimize spoilage.

In-Depth North America Agricultural Films Industry Market Outlook

The outlook for the North America agricultural films industry is exceptionally positive, driven by the persistent need for enhanced agricultural productivity and sustainability. Key growth accelerators include the ongoing innovation in biodegradable and smart film technologies, catering to both environmental regulations and the demand for data-driven farming. The expansion of controlled environment agriculture represents a substantial untapped market with specific film requirements. Strategic initiatives focusing on market education and wider distribution will ensure broader adoption. The industry is well-positioned to capitalize on its ability to address critical agricultural challenges, from climate change resilience to resource optimization, securing a robust growth trajectory in the coming years.

North America Agricultural Films Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

North America Agricultural Films Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Agricultural Films Industry Regional Market Share

Geographic Coverage of North America Agricultural Films Industry

North America Agricultural Films Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.20% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 6. North America Agricultural Films Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Berry Plastics Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 ExxonMobil Chemical

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 BASF

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 The Dow Chemical Company

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 RKW S

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 AB Rani Plast Oy

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Hyplast NV

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Britton Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Trioplast Industries AB

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Armando Alvarez Group

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Berry Plastics Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Agricultural Films Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Agricultural Films Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Agricultural Films Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 2: North America Agricultural Films Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 3: North America Agricultural Films Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: North America Agricultural Films Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: North America Agricultural Films Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: North America Agricultural Films Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: North America Agricultural Films Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 8: North America Agricultural Films Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 9: North America Agricultural Films Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: North America Agricultural Films Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: North America Agricultural Films Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: North America Agricultural Films Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: United States North America Agricultural Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Canada North America Agricultural Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Mexico North America Agricultural Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Agricultural Films Industry?

The projected CAGR is approximately 6.20%.

2. Which companies are prominent players in the North America Agricultural Films Industry?

Key companies in the market include Berry Plastics Corporation, ExxonMobil Chemical, BASF, The Dow Chemical Company, RKW S, AB Rani Plast Oy, Hyplast NV, Britton Group, Trioplast Industries AB, Armando Alvarez Group.

3. What are the main segments of the North America Agricultural Films Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.24 Million as of 2022.

5. What are some drivers contributing to market growth?

Adoption of Organic and Eco-friendly Farming Practices; Declining Area of Arable Land and Rising Food Security Concerns.

6. What are the notable trends driving market growth?

Shrinking Farm Lands Necessitating to Increase the Productivity.

7. Are there any restraints impacting market growth?

High Demand for Conventional and Synthetic Products; Lack of Awareness and Other Factors Limiting the Adoption of Agricultural Inoculants.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Agricultural Films Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Agricultural Films Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Agricultural Films Industry?

To stay informed about further developments, trends, and reports in the North America Agricultural Films Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence