Key Insights

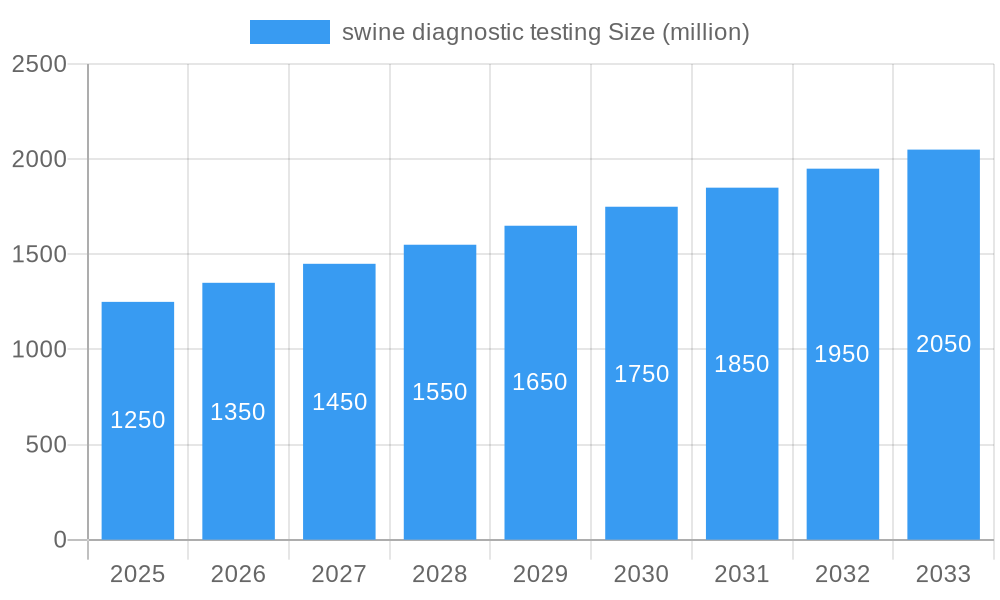

The swine diagnostic testing market is poised for significant expansion, projected to reach an estimated $XXX million by 2025 and grow at a Compound Annual Growth Rate (CAGR) of XX% through 2033. This robust growth is primarily fueled by an increasing global demand for pork, driven by a growing population and rising disposable incomes, particularly in emerging economies. The imperative to ensure herd health and food safety, coupled with the escalating threat of zoonotic diseases and evolving regulatory landscapes, necessitates advanced and rapid diagnostic solutions. Key market drivers include the continuous emergence of novel swine pathogens, the adoption of precision farming techniques, and the growing awareness among producers about the economic impact of disease outbreaks on productivity and profitability. Technological advancements in immunoassay (ELISA) kits and PCR kits are enhancing sensitivity, specificity, and turnaround times, making them indispensable tools for early disease detection and outbreak management in veterinary hospitals and clinics.

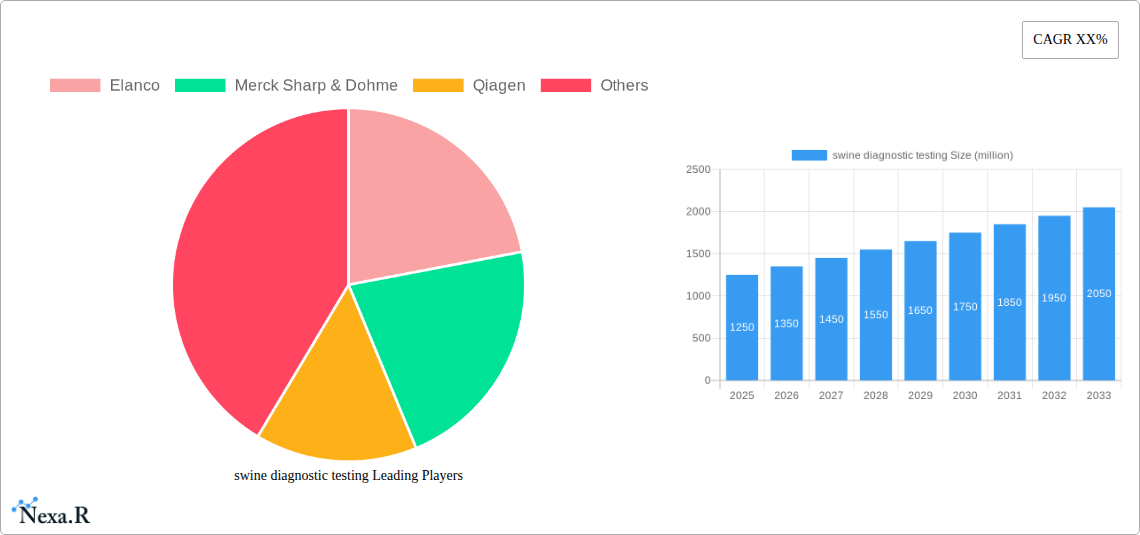

swine diagnostic testing Market Size (In Billion)

Further bolstering market expansion are the ongoing trends in herd consolidation, leading to larger production units that require sophisticated disease surveillance. The increasing emphasis on antibiotic stewardship also propels the demand for diagnostics, enabling targeted treatment and reducing the reliance on broad-spectrum antimicrobials. However, the market faces certain restraints, including the high cost of advanced diagnostic equipment and reagents in some regions, and the need for skilled personnel to operate and interpret test results. The evolving landscape of biosecurity protocols and the global efforts to control and eradicate diseases like African Swine Fever (ASF) will continue to shape the demand for a comprehensive suite of diagnostic tools. The market segmentation into veterinary hospitals, veterinary clinics, and distinct testing types like immunoassay (ELISA) kits, PCR kits, and others, highlights the diverse needs addressed by this dynamic sector. Leading companies such as Elanco, Merck Sharp & Dohme, and Qiagen are at the forefront, driving innovation and catering to the evolving demands of the swine industry.

swine diagnostic testing Company Market Share

Comprehensive Swine Diagnostic Testing Market Report: Forecast 2019-2033

This in-depth report offers a definitive analysis of the global swine diagnostic testing market, encompassing a detailed historical overview from 2019-2024 and a robust forecast through 2033, with a base year of 2025 and estimated year of 2025. We delve into critical market dynamics, growth trends, regional dominance, product landscapes, and the strategic imperatives shaping this vital sector. With a focus on high-traffic keywords and parent/child market segmentation, this report is optimized for search engine visibility and designed to equip industry professionals with actionable intelligence.

swine diagnostic testing Market Dynamics & Structure

The global swine diagnostic testing market exhibits a moderately concentrated structure, driven by continuous technological innovation and stringent regulatory frameworks aimed at ensuring animal health and food safety. Key players like Elanco, Merck Sharp & Dohme, and Qiagen are at the forefront of developing advanced diagnostic solutions. Technological innovation, particularly in molecular diagnostics like PCR kits, is a significant driver, enabling faster and more accurate disease detection. Regulatory bodies globally are continuously updating guidelines for disease surveillance and control, creating a steady demand for effective diagnostic tools.

- Market Concentration: Moderate, with a few key global players holding significant market share.

- Technological Innovation Drivers: Advancement in molecular diagnostics (PCR, NGS), automation in labs, and development of multiplex assays.

- Regulatory Frameworks: Strict governmental regulations for animal disease control, biosecurity, and international trade of swine products.

- Competitive Product Substitutes: While specialized, some general veterinary diagnostic platforms can offer basic swine disease screening.

- End-User Demographics: Primarily large-scale commercial swine farms, veterinary diagnostic laboratories, government animal health agencies, and research institutions.

- M&A Trends: Strategic acquisitions focused on expanding technological capabilities or market reach, with approximately 3-5 significant deals annually in the last two years. The volume of M&A activities is projected to increase by 15% in the forecast period.

swine diagnostic testing Growth Trends & Insights

The swine diagnostic testing market has witnessed robust growth, propelled by escalating concerns over infectious diseases, increasing global pork consumption, and a growing emphasis on herd health management. The market size, valued at an estimated $1,100 million in 2025, is projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 6.5% over the forecast period (2025–2033). This growth is fueled by the increasing adoption of advanced diagnostic techniques that offer higher sensitivity and specificity compared to traditional methods. Technological disruptions, such as the integration of artificial intelligence (AI) in data analysis of diagnostic results and the development of point-of-care testing (POCT) solutions, are further accelerating market penetration.

Consumer behavior shifts towards demanding higher standards of animal welfare and food safety are indirectly influencing the demand for comprehensive diagnostic testing. Producers are increasingly investing in proactive health monitoring systems to prevent outbreaks and minimize economic losses. The historical period (2019-2024) saw a steady rise in diagnostic test utilization, with an average market expansion of 5.8% year-on-year. The adoption rate of PCR-based diagnostics, for instance, has surged by over 20% during this period, reflecting a significant move away from older immunoassay-based methods for certain applications.

The parent market for veterinary diagnostics is a multi-billion dollar industry, and swine diagnostic testing constitutes a significant and growing segment within it. The child markets, such as specific disease testing kits for Porcine Reproductive and Respiratory Syndrome (PRRS) or African Swine Fever (ASF), are experiencing exponential growth due to emerging and re-emerging disease threats. These specialized segments, often driven by critical public health concerns, contribute substantially to the overall market value. The market penetration of routine diagnostic testing in developing countries is still in its nascent stages, presenting a substantial untapped potential for future growth.

Dominant Regions, Countries, or Segments in swine diagnostic testing

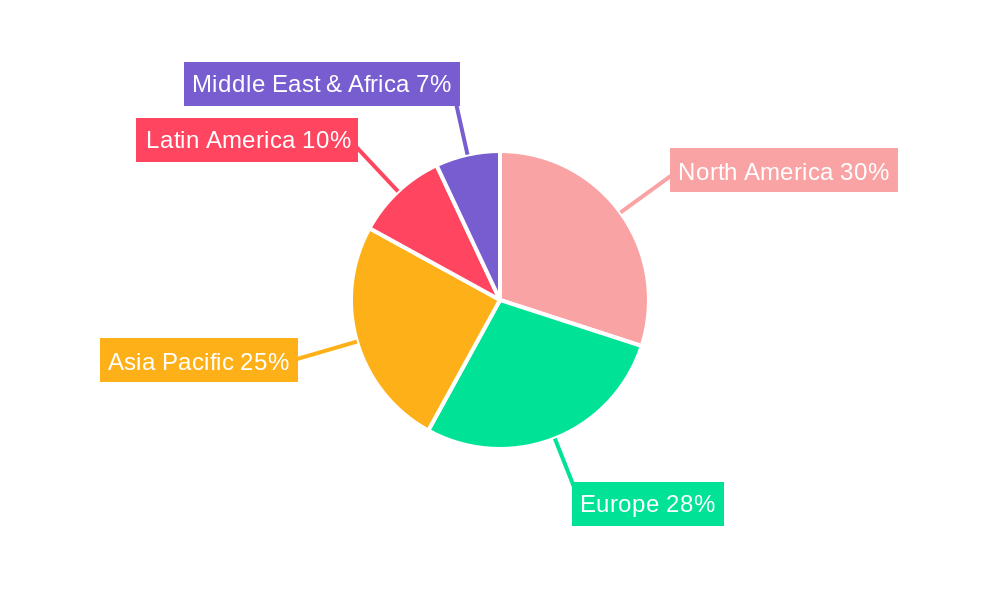

The Asia-Pacific region is emerging as a dominant force in the global swine diagnostic testing market, driven by its substantial swine population, increasing meat consumption, and a growing awareness of biosecurity measures. Countries like China and Vietnam, with their massive pig farming industries, are major consumers of diagnostic solutions. Economic policies promoting agricultural modernization and increased government investment in animal disease surveillance programs are key drivers in this region.

Within the Application segment, Veterinary Clinics are playing an increasingly pivotal role, offering accessible diagnostic services to a wider range of swine producers, from smallholders to medium-sized operations. While Veterinary Hospitals cater to more complex cases, the sheer volume of routine testing and early disease detection often occurs at the clinic level, contributing to a significant market share. The market share of Veterinary Clinics in diagnostic testing is estimated to be around 35% in 2025, with projected growth of 7% annually.

In terms of Types, PCR Kits have become the fastest-growing segment, accounting for an estimated 45% of the market value in 2025, with a CAGR of 7.2%. Their superior sensitivity, specificity, and ability to detect viral RNA or DNA directly make them indispensable for early and accurate diagnosis of a wide range of swine diseases, including highly contagious ones like ASF and PRRS. Immunoassays (ELISA) Kits, while still widely used for antigen and antibody detection, represent a mature segment with a slower but steady growth rate of approximately 4.5%. The "Others" segment, encompassing next-generation sequencing (NGS) and other novel technologies, is expected to witness significant growth as its cost decreases and accessibility increases.

Dominant Region Drivers (Asia-Pacific):

- Largest swine population globally, particularly in China and Southeast Asia.

- Increasing demand for pork as a primary protein source.

- Government initiatives to enhance biosecurity and disease control.

- Growing adoption of advanced technologies in livestock farming.

- Significant foreign direct investment in the agricultural sector.

Dominant Application Drivers (Veterinary Clinics):

- Accessibility and cost-effectiveness for a broad range of producers.

- Role in routine herd health monitoring and preventative care.

- Increasing number of veterinary professionals specializing in swine health.

Dominant Type Drivers (PCR Kits):

- High sensitivity and specificity for accurate disease identification.

- Rapid detection capabilities, crucial for outbreak containment.

- Versatility in detecting multiple pathogens simultaneously.

- Advancements in multiplex PCR assays.

swine diagnostic testing Product Landscape

The swine diagnostic testing product landscape is characterized by rapid innovation, focusing on enhanced sensitivity, specificity, and speed. Leading companies are introducing multiplex assays capable of detecting multiple pathogens simultaneously, thereby reducing testing time and costs. Innovations in sample preparation and real-time PCR technology are further improving diagnostic accuracy. The development of portable and user-friendly diagnostic kits for point-of-care use in on-farm settings is also gaining traction, enabling quicker decision-making and early intervention. Performance metrics like detection limits, turnaround time, and cost per test are key differentiators in this competitive market. Unique selling propositions often revolve around disease coverage, ease of use, and integration with digital health platforms for data management.

Key Drivers, Barriers & Challenges in swine diagnostic testing

Key Drivers:

- Increasing incidence of swine diseases: Outbreaks of diseases like African Swine Fever (ASF) and Porcine Reproductive and Respiratory Syndrome (PRRS) necessitate rapid and accurate diagnostics for control and prevention.

- Growing global demand for pork: A rising global population and changing dietary habits are driving the need for increased pork production, which in turn fuels the demand for robust animal health management and diagnostics.

- Technological advancements: Innovations in molecular diagnostics, including PCR and next-generation sequencing, offer higher sensitivity and specificity, leading to improved disease detection.

- Stringent regulations and food safety concerns: Government mandates and consumer demand for safe food products encourage the use of diagnostic testing to ensure herd health and prevent disease transmission.

Barriers & Challenges:

- High cost of advanced diagnostic technologies: While effective, some sophisticated diagnostic tools can be expensive, posing a barrier to adoption for smaller producers or in regions with limited financial resources.

- Lack of skilled personnel: The operation and interpretation of complex diagnostic tests require trained professionals, and a shortage of such expertise in certain regions can hinder market growth.

- Supply chain disruptions: The global nature of the industry means that disruptions in the supply of reagents, equipment, or raw materials can impact the availability and cost of diagnostic kits.

- Regulatory hurdles for new product approvals: Obtaining regulatory approval for new diagnostic tests can be a time-consuming and complex process, delaying market entry.

- Antimicrobial resistance concerns: While not a direct diagnostic challenge, the broader issue of antimicrobial resistance indirectly influences the need for accurate diagnostics to guide targeted treatment strategies.

Emerging Opportunities in swine diagnostic testing

Emerging opportunities in the swine diagnostic testing market lie in the development of ultra-rapid, on-farm diagnostic solutions that empower producers with real-time disease detection capabilities. The integration of AI and machine learning for predictive diagnostics, analyzing large datasets from diagnostic tests to forecast disease outbreaks, presents a significant untapped market. Furthermore, the growing global emphasis on animal welfare and sustainability is creating a demand for comprehensive health monitoring that goes beyond pathogen detection, including indicators of stress and immune status. Untapped markets in developing economies, where swine farming is on the rise but diagnostic infrastructure is nascent, offer substantial growth potential.

Growth Accelerators in the swine diagnostic testing Industry

The swine diagnostic testing industry is experiencing accelerated growth due to several key catalysts. Technological breakthroughs in areas like CRISPR-based diagnostics and microfluidics are promising even more sensitive, rapid, and cost-effective testing solutions. Strategic partnerships between diagnostic companies, pharmaceutical firms, and technology providers are fostering innovation and expanding market reach. Furthermore, aggressive market expansion strategies by key players, targeting emerging economies with tailored diagnostic solutions and educational initiatives, are significantly driving long-term growth. The increasing prevalence of zoonotic diseases and the heightened awareness among regulatory bodies and the public are creating sustained demand for advanced diagnostic tools.

Key Players Shaping the swine diagnostic testing Market

- Elanco

- Merck Sharp & Dohme

- Qiagen

Notable Milestones in swine diagnostic testing Sector

- 2019: Launch of novel PCR-based assays for multiple swine viruses by major diagnostic companies, enhancing multiplex testing capabilities.

- 2020: Increased investment in research and development for African Swine Fever (ASF) diagnostics due to its widespread impact.

- 2021: Emergence of AI-powered diagnostic platforms for faster data analysis and interpretation of swine disease outbreaks.

- 2022: Significant mergers and acquisitions aimed at consolidating market share and expanding technological portfolios in molecular diagnostics.

- 2023: Introduction of more user-friendly and portable diagnostic kits for on-farm application, improving accessibility for producers.

- 2024: Advancements in sample multiplexing and automation in laboratory workflows, aiming to reduce turnaround times for complex diagnostic panels.

In-Depth swine diagnostic testing Market Outlook

The outlook for the swine diagnostic testing market remains exceptionally positive, driven by ongoing advancements in diagnostic technologies and the persistent global need for effective disease management in swine populations. Growth accelerators such as the development of next-generation sequencing for genomic surveillance of swine pathogens, coupled with strategic alliances aimed at developing integrated farm health management systems, will further propel the market. The increasing adoption of digital health solutions and the potential for point-of-care diagnostics will democratize access to critical health insights for producers worldwide. Strategic opportunities abound in emerging markets and in the development of novel diagnostic markers for emerging diseases and production-related challenges. The market is poised for sustained expansion, underpinned by a commitment to animal welfare, food safety, and efficient pork production.

swine diagnostic testing Segmentation

-

1. Application

- 1.1. Veterinary Hospitals

- 1.2. Veterinary Clinics

-

2. Types

- 2.1. Immunoassays (ELISA) Kits

- 2.2. PCR Kits

- 2.3. Others

swine diagnostic testing Segmentation By Geography

- 1. CA

swine diagnostic testing Regional Market Share

Geographic Coverage of swine diagnostic testing

swine diagnostic testing REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.96% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Veterinary Hospitals

- 5.1.2. Veterinary Clinics

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Immunoassays (ELISA) Kits

- 5.2.2. PCR Kits

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. CA

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. swine diagnostic testing Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Veterinary Hospitals

- 6.1.2. Veterinary Clinics

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Immunoassays (ELISA) Kits

- 6.2.2. PCR Kits

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Elanco

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Merck Sharp & Dohme

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Qiagen

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.1 Elanco

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: swine diagnostic testing Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: swine diagnostic testing Share (%) by Company 2025

List of Tables

- Table 1: swine diagnostic testing Revenue billion Forecast, by Application 2020 & 2033

- Table 2: swine diagnostic testing Revenue billion Forecast, by Types 2020 & 2033

- Table 3: swine diagnostic testing Revenue billion Forecast, by Region 2020 & 2033

- Table 4: swine diagnostic testing Revenue billion Forecast, by Application 2020 & 2033

- Table 5: swine diagnostic testing Revenue billion Forecast, by Types 2020 & 2033

- Table 6: swine diagnostic testing Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the swine diagnostic testing?

The projected CAGR is approximately 9.96%.

2. Which companies are prominent players in the swine diagnostic testing?

Key companies in the market include Elanco, Merck Sharp & Dohme, Qiagen.

3. What are the main segments of the swine diagnostic testing?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.95 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3400.00, USD 5100.00, and USD 6800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "swine diagnostic testing," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the swine diagnostic testing report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the swine diagnostic testing?

To stay informed about further developments, trends, and reports in the swine diagnostic testing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence