Key Insights for Telehealth Market

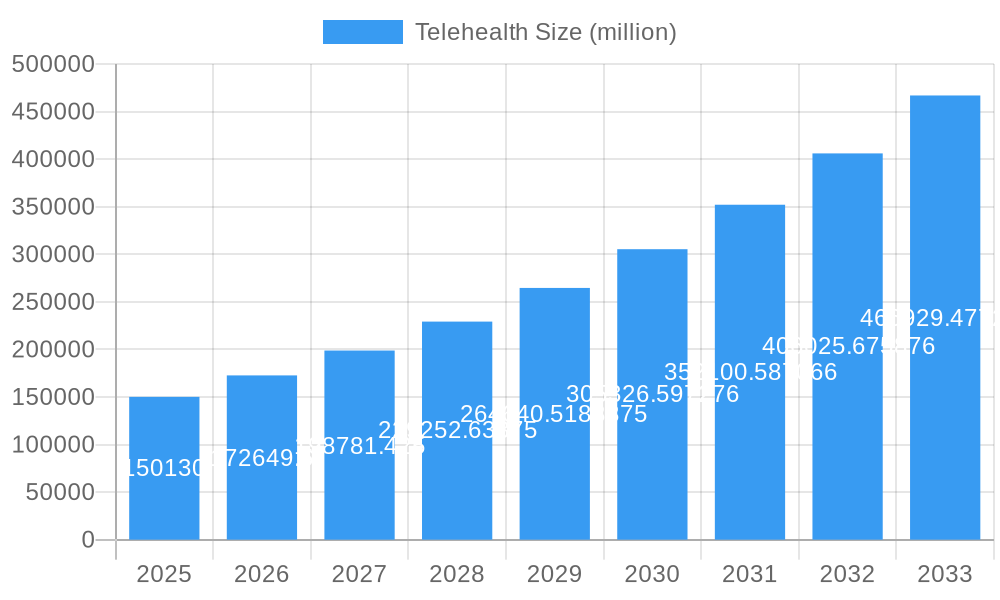

The global Telehealth Market is poised for substantial expansion, driven by accelerating digital transformation in healthcare and a burgeoning demand for accessible, cost-effective medical services. Valued at an estimated $78.25 billion in 2025, the market is projected to reach approximately $513.12 billion by 2034, exhibiting a robust Compound Annual Growth Rate (CAGR) of 24.11% over the forecast period. This remarkable growth trajectory is underpinned by several macro tailwinds, including the increasing prevalence of chronic diseases, the global aging population, and a shifting paradigm towards patient-centric care models. Furthermore, advancements in communication technology, such as high-speed internet and sophisticated mobile platforms, have significantly lowered barriers to entry and adoption for both providers and patients.

Telehealth Market Size (In Billion)

The demand drivers for the Telehealth Market are multifaceted. A critical factor is the imperative to manage healthcare costs effectively, as telehealth solutions often reduce hospital readmissions and unnecessary in-person visits. The growing need for continuous and personalized patient care, particularly for individuals with long-term conditions, fuels the adoption of telemonitoring and virtual consultation platforms. Regulatory support and evolving reimbursement policies, particularly post-pandemic, have also played a pivotal role in legitimizing and mainstreaming telehealth services. The integration of artificial intelligence and machine learning further enhances diagnostic capabilities and predictive analytics within telehealth platforms, contributing to better patient outcomes and operational efficiencies for healthcare providers. This technological convergence is attracting significant investment, fostering innovation across the ecosystem from specialized software to advanced Wearable Devices Market offerings. The outlook for the Telehealth Market remains exceptionally positive, characterized by continuous technological evolution, expanding service portfolios, and a deepening integration into mainstream healthcare delivery, cementing its role as a fundamental pillar of future medical practice.

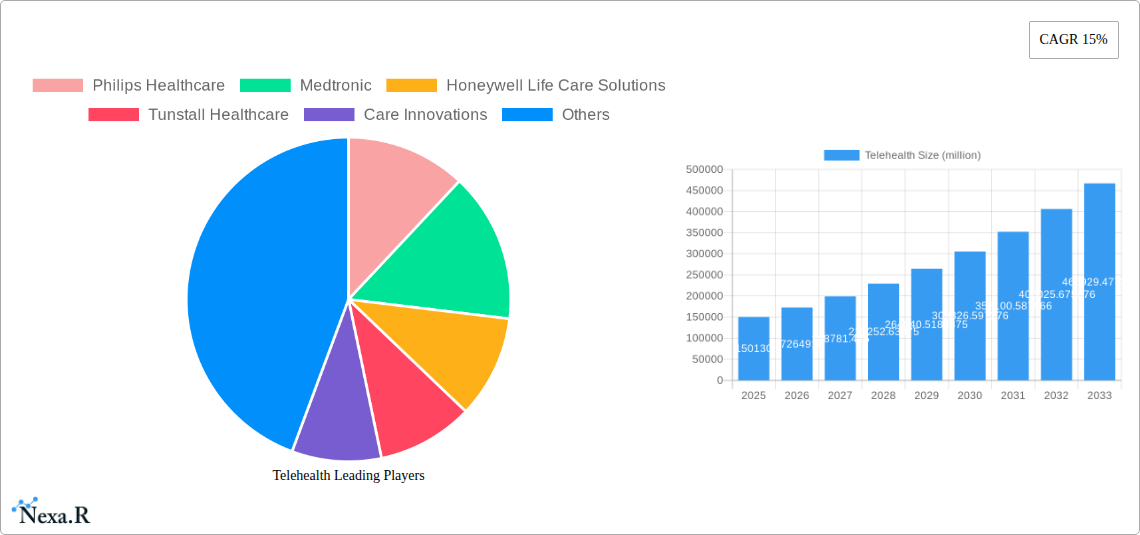

Telehealth Company Market Share

Dominant Offering Segment in Telehealth Market

Within the multifaceted Telehealth Market, the Services segment, encompassing teleconsultation, telemonitoring, telemedicine, and teletherapy, emerges as the dominant component by revenue share. This dominance is primarily attributable to the direct patient-provider interactions and the immediate value proposition offered by these virtual care modalities. Services form the core utility of telehealth, addressing critical needs such as remote diagnostics, treatment planning, chronic disease management, and mental health support. The widespread adoption of virtual visits, propelled by increased convenience, reduced travel times, and enhanced accessibility, especially in rural or underserved areas, continues to drive this segment's robust growth. Healthcare providers, recognizing the operational efficiencies and expanded patient reach, are increasingly investing in sophisticated service delivery platforms.

Teleconsultation, for instance, allows patients to connect with general practitioners and specialists via video or audio calls, reducing the need for physical appointments. This not only improves patient satisfaction but also optimizes resource allocation for healthcare facilities. Telemonitoring services, often coupled with Medical Devices Market innovations, enable continuous tracking of vital signs and other health parameters for patients with chronic conditions, facilitating proactive interventions and preventing acute episodes. The integration of these services into comprehensive care pathways has solidified their position. Key players in the broader Telehealth Market often differentiate themselves by the breadth and depth of their service offerings, leveraging proprietary platforms and specialized medical expertise to cater to diverse patient populations and clinical needs.

While hardware components, such as monitoring devices and specialized peripherals, and Healthcare Software Market solutions, including Electronic Health Records (EHR) integration and patient management systems, are foundational enablers, the direct revenue generation and recurring subscription models associated with actual service delivery place the Services segment at the forefront. The share of services is anticipated to continue its growth trajectory as more healthcare systems globally institutionalize telehealth as a standard mode of care delivery. Furthermore, ongoing innovation in service delivery models, such as asynchronous consultations and AI-powered triage systems, will further enhance efficiency and expand the applicability of telehealth services, ensuring this segment maintains its leading position within the Telehealth Market landscape.

Key Market Drivers for Telehealth Market Expansion

Expansion within the Telehealth Market is fundamentally propelled by a confluence of demographic, technological, and systemic factors, each demonstrating a quantifiable impact. One primary driver is the escalating global burden of chronic diseases and the rapid aging of populations. As per World Health Organization (WHO) projections, chronic diseases account for over 70% of all deaths globally, necessitating long-term care and frequent monitoring. This trend directly fuels the demand for services like telemonitoring, a core component of the Remote Patient Monitoring Market, enabling continuous oversight of conditions such as diabetes, heart disease, and hypertension, particularly for the Geriatric patient type segment. Telehealth facilitates proactive management, reducing hospitalizations and improving quality of life for an increasingly elderly demographic requiring consistent medical attention.

Secondly, the relentless pace of technological advancements, particularly in digital communication and data processing, serves as a significant catalyst. The proliferation of high-speed internet, 5G networks, and increasingly powerful mobile devices has made virtual consultations, delivered via platforms incorporating sophisticated Video Conferencing Market technologies, widely accessible. Concurrently, the maturation of Cloud Computing Market infrastructure has enabled scalable, secure, and on-demand telehealth software solutions, supporting everything from patient management systems to complex diagnostic tools. This digital transformation allows healthcare providers to implement telehealth systems without substantial upfront IT investments, improving scalability and reducing operational friction.

Lastly, the persistent demand for greater healthcare accessibility and cost-efficiency is a critical driver. Geographic disparities in healthcare access remain a global challenge, with rural and remote communities often lacking immediate access to specialists. Telehealth bridges these gaps, offering virtual access to care regardless of location, directly impacting the End User segments of Patients and Healthcare Providers. The economic advantages are also clear: virtual visits can significantly reduce patient travel costs, lost workdays, and facility overheads for providers. This shift towards efficiency is increasingly valued by entities within the Managed Healthcare Market, which seek to optimize care delivery while containing expenditures, making telehealth an attractive and essential component of modern healthcare strategy.

Competitive Ecosystem of Telehealth Market

The competitive landscape of the Telehealth Market is characterized by a mix of established medical technology giants, specialized telehealth solution providers, and IT and communication firms. Key players are strategically expanding their portfolios through innovation, partnerships, and acquisitions to capture a larger share of this rapidly growing market.

- Philips Healthcare: A global leader in health technology, Philips offers comprehensive telehealth solutions, integrating remote patient monitoring, acute care, and virtual care platforms to enhance connected care delivery across various settings.

- Medtronic: Known for its medical device innovations, Medtronic extends its presence in the telehealth space by integrating remote monitoring capabilities into its device ecosystems, particularly for chronic disease management.

- Honeywell Life Care Solutions: This division focuses on providing remote patient monitoring solutions and emergency response systems, leveraging connectivity to empower patients and support healthcare providers.

- Tunstall Healthcare: Specializing in technology-enabled care, Tunstall offers a range of telehealth and telecare solutions aimed at supporting independent living and managing long-term conditions for vulnerable individuals.

- Care Innovations: A joint venture focused on connecting patients, caregivers, and providers through innovative remote care management programs and telehealth platforms.

- Cerner: A leading provider of health information technology, Cerner integrates telehealth functionalities into its broader electronic health record (EHR) systems, streamlining virtual care workflows for hospitals and health systems.

- Cisco: A networking and communications technology giant, Cisco provides the underlying infrastructure and Video Conferencing Market technologies critical for secure and reliable telehealth communications, often partnering with healthcare providers.

- Medvivo: Offers integrated urgent and routine care services, leveraging telehealth technology to provide remote consultations, clinical triage, and monitoring across different care pathways.

- Globalmedia: Specializes in high-definition video conferencing solutions designed for healthcare, facilitating secure and effective virtual consultations and medical education.

- Aerotel Medical Systems: A pioneer in providing remote patient monitoring solutions, including mobile medical devices and communication systems for various medical applications.

- AMD Global Telemedicine: A dedicated telehealth company offering a wide array of telemedicine hardware and software solutions, from clinical workstations to cloud-based platforms.

- American Well: A prominent pure-play telehealth provider, offering a comprehensive platform for on-demand and scheduled virtual care across a multitude of specialties.

- Intouch Health: Acquired by Teladoc Health, Intouch Health was a leader in enterprise telehealth solutions for hospitals and health systems, focusing on acute and specialty care.

- Vidyo: A company providing high-quality, scalable Video Conferencing Market technology, which is critical for real-time, face-to-face virtual consultations in telehealth applications.

Recent Developments & Milestones in Telehealth Market

Recent years have seen a surge in innovations and strategic partnerships bolstering the Telehealth Market:

- May 2023: A major healthcare system announced the expansion of its virtual urgent care services, integrating AI-powered symptom checkers to improve patient triage and reduce wait times, reflecting growing digital health maturity.

- September 2023: Leading Healthcare Software Market vendors unveiled new interoperability standards for telehealth platforms, aiming to facilitate seamless data exchange with electronic health records (EHRs) and other clinical systems.

- November 2023: A prominent Wearable Devices Market player launched a new generation of smart health watches with advanced health monitoring capabilities, including ECG and continuous glucose monitoring, directly integrating with telehealth platforms for data sharing with providers.

- January 2024: Several national governments, notably in Europe and North America, passed legislation standardizing telehealth reimbursement rates, providing greater financial stability and incentivizing wider adoption among providers.

- April 2024: A consortium of technology companies and medical institutions collaborated to develop a secure, blockchain-based framework for telehealth data management, enhancing privacy and data integrity for patient records.

- June 2024: A large payer group announced a strategic partnership with a Remote Patient Monitoring Market leader to offer comprehensive virtual care programs for chronic disease management to its entire member base, demonstrating a shift towards proactive, preventative care.

- August 2024: The launch of a new telehealth platform specifically designed for pediatric patients gained significant traction, offering child-friendly interfaces and specialized virtual care teams to address the unique needs of younger populations.

- October 2024: Several major hospitals initiated pilot programs for integrating virtual reality (VR) and augmented reality (AR) into telehealth, particularly for remote surgical guidance and immersive therapy sessions, marking an exciting frontier for the Digital Health Market.

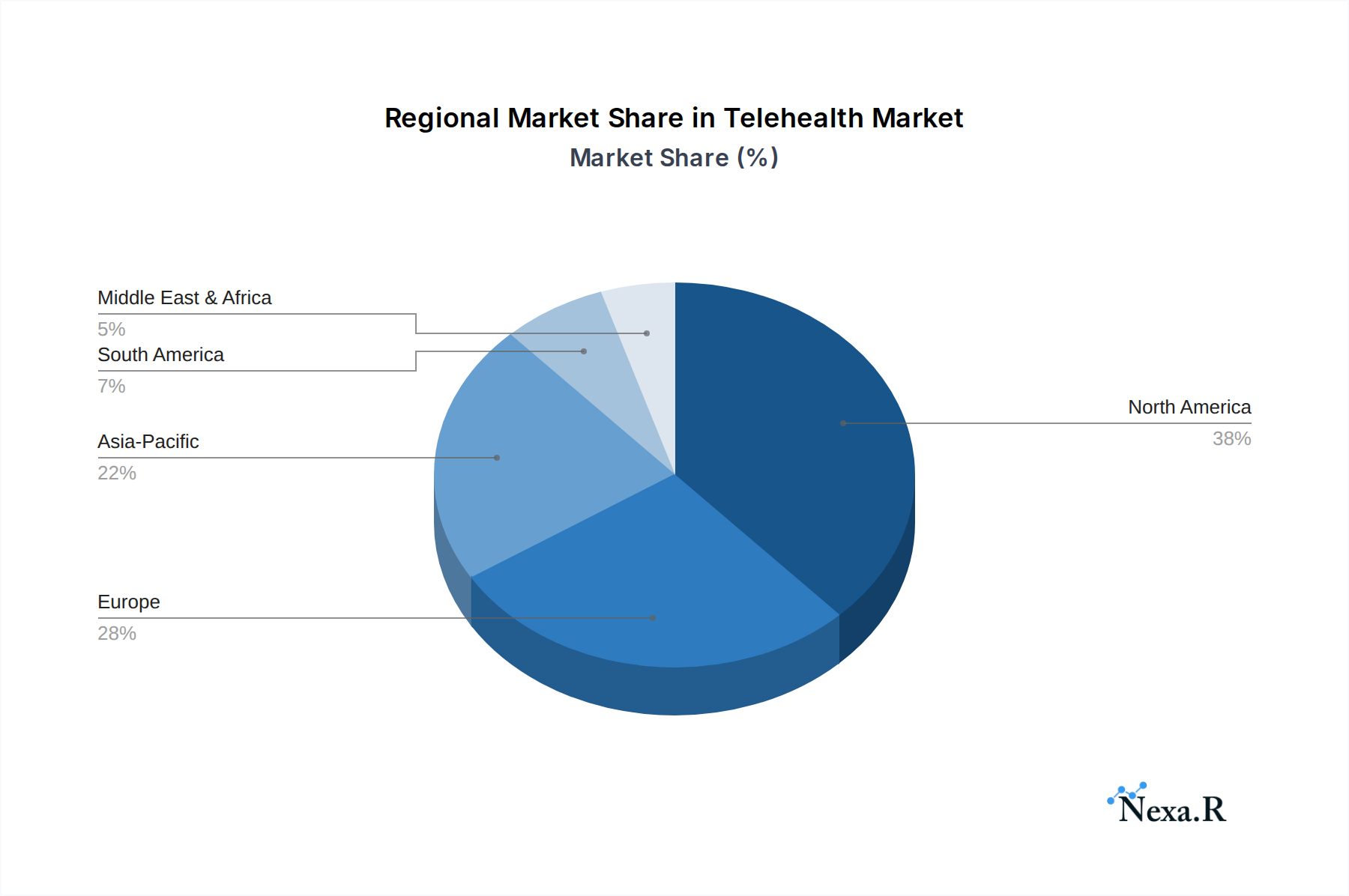

Regional Market Breakdown for Telehealth Market

The global Telehealth Market exhibits significant regional variations in adoption, growth drivers, and market maturity. North America currently dominates the market, largely due to its advanced healthcare infrastructure, high technological adoption rates, and favorable reimbursement policies. The United States, in particular, has seen rapid expansion, driven by significant investments in Digital Health Market solutions and widespread acceptance of virtual care by both consumers and providers. The region benefits from a robust competitive landscape and a strong emphasis on reducing healthcare costs, resulting in a mature yet continually expanding telehealth ecosystem.

Europe represents another substantial market, characterized by strong government initiatives and national health services actively promoting telehealth to manage healthcare demands, particularly from its aging population. Countries like the UK, Germany, and France are prominent adopters, focusing on integrating telehealth into primary care and chronic disease management. While growth rates are steady, the fragmented regulatory landscape across different European nations can pose a challenge compared to the more unified approach seen in North America.

Asia Pacific is projected to be the fastest-growing region in the Telehealth Market, driven by its vast population, increasing internet penetration, rising disposable incomes, and a strong governmental push for digital healthcare initiatives. Countries such as China, India, and Japan are at the forefront, investing heavily in smart hospitals, telemedicine platforms, and Remote Patient Monitoring Market solutions to address healthcare disparities and improve access in both urban and rural areas. The immense potential for new patient acquisition and the rapid adoption of mobile technology contribute to its exceptionally high regional CAGR.

In the Middle East & Africa and South America, the Telehealth Market is still in nascent stages but demonstrates considerable growth potential. These regions are characterized by evolving healthcare infrastructures, increasing chronic disease prevalence, and a growing recognition of telehealth as a viable solution for improving healthcare access and efficiency. While challenges such as regulatory frameworks and digital literacy persist, strategic investments in Medical Devices Market and telecom infrastructure are paving the way for future growth, making these emerging markets critical for long-term expansion strategies.

Telehealth Regional Market Share

Customer Segmentation & Buying Behavior in Telehealth Market

The Telehealth Market caters to a diverse range of end-users, each with distinct purchasing criteria and behavioral patterns. The primary segments include Healthcare Providers, Payers, Patients, and Employers, alongside other specialized entities. Healthcare Providers, encompassing hospitals, clinics, and individual practitioners, prioritize solutions that integrate seamlessly with existing Electronic Health Record (EHR) systems, enhance operational efficiency, and improve patient outcomes. Their purchasing decisions are heavily influenced by clinical efficacy, data security, regulatory compliance (e.g., HIPAA), and the potential for revenue generation or cost savings. They often procure through direct sales channels, seeking enterprise-level solutions with comprehensive training and support.

Payers, including private health insurance companies and government agencies, focus on telehealth solutions that demonstrate clear cost-effectiveness, reduce claims payouts, and improve member health and satisfaction. They assess solutions based on their ability to facilitate preventative care, manage chronic conditions, and reduce emergency room visits. Their procurement strategies often involve partnerships with telehealth vendors to offer integrated virtual care benefits to their members, directly influencing the Managed Healthcare Market. Price sensitivity is high, and they typically seek long-term contractual agreements with performance metrics.

Patients, as end-consumers, are primarily driven by convenience, accessibility, and ease of use. They seek immediate access to care, reduced waiting times, and the ability to consult with healthcare professionals from the comfort of their homes. Price sensitivity varies depending on insurance coverage and the urgency of their medical needs. Many patients access telehealth services through provider recommendations, direct-to-consumer platforms, or employer-sponsored programs. There's a notable shift towards demanding user-friendly mobile applications and platforms that offer a broad range of services, including mental health support and chronic disease management, often enabled by advancements in the Healthcare Software Market.

Employers utilize telehealth services as a benefit for their employees, aiming to reduce absenteeism, improve employee well-being, and lower overall healthcare costs. Their buying behavior is shaped by the comprehensiveness of services offered, privacy assurances, and demonstrable return on investment (ROI) through improved employee health metrics. Procurement often occurs through benefits consultants or directly with telehealth providers, seeking customized packages. Recent cycles have seen a heightened preference across all segments for solutions that offer robust data analytics, personalized care pathways, and seamless integration with existing health and wellness programs, reflecting a broader movement towards value-based care within the Digital Health Market.

Sustainability & ESG Pressures on Telehealth Market

The Telehealth Market, while inherently beneficial from an environmental and social perspective due to reduced patient travel and infrastructure demands, is increasingly subject to rigorous sustainability and ESG (Environmental, Social, and Governance) pressures. From an environmental standpoint, telehealth significantly reduces carbon footprints associated with healthcare delivery. Virtual consultations minimize patient and provider travel, cutting down on vehicle emissions and fuel consumption. This aligns directly with global carbon reduction targets and contributes positively to environmental regulations aimed at reducing transportation-related pollution. Manufacturers of Wearable Devices Market and other hardware components within telehealth are facing scrutiny to adopt more circular economy principles, focusing on sustainable sourcing of raw materials, energy-efficient production, and end-of-life recycling programs for electronic waste. The shift towards cloud-based software solutions, a key part of the Cloud Computing Market, also introduces ESG considerations regarding data center energy consumption, although these are often offset by the larger scale efficiencies offered by cloud providers.

Socially, telehealth inherently addresses critical ESG criteria by improving access to healthcare, especially for underserved populations, thereby enhancing health equity. It reduces barriers related to geography, mobility, and socioeconomic status, directly contributing to UN Sustainable Development Goal 3 (Good Health and Well-being). Companies are under pressure to ensure their platforms are accessible to individuals with disabilities, offer culturally competent care, and protect patient data with the highest standards of privacy and security. The "S" in ESG also extends to workforce practices, with increasing emphasis on fair labor, diversity, equity, and inclusion within telehealth companies.

Governance aspects are paramount, especially given the sensitive nature of health data. Robust data governance frameworks, cybersecurity protocols, and ethical AI deployment are crucial for maintaining patient trust and regulatory compliance. ESG investors are increasingly evaluating telehealth companies not just on their financial performance but also on their commitment to transparent governance, responsible data handling, and proactive measures to combat digital health disparities. The sustained growth of the Digital Health Market will be increasingly tied to how effectively companies integrate these environmental and social responsibilities into their core strategies, proving that telehealth not only delivers economic value but also contributes positively to planetary and societal well-being.

Telehealth Segmentation

-

1. Offering

-

1.1. Hardware

- 1.1.1. Monitoring Devices

- 1.1.2. Wearable Devices

- 1.2. Software

- 1.3. Services

-

1.1. Hardware

-

2. Delivery Mode

- 2.1. On-Premise

- 2.2. Cloud-Based

-

3. Patient Type

- 3.1. Adult

- 3.2. Pediatric

- 3.3. Geriatric

-

4. Communication Technology

- 4.1. Video Conferencing

- 4.2. Audio/Voice Calls

- 4.3. Messaging & Chat-Based Services

-

5. Application

- 5.1. Teleconsultation

- 5.2. Telemonitoring

- 5.3. Telemedicine

- 5.4. Teletherapy

- 5.5. Tele-Education

- 5.6. Others

-

6. End User

- 6.1. Healthcare Providers

- 6.2. Payers

- 6.3. Patients

- 6.4. Employers

- 6.5. Others

Telehealth Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Telehealth Regional Market Share

Geographic Coverage of Telehealth

Telehealth REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 24.11% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 5.1.1. Hardware

- 5.1.1.1. Monitoring Devices

- 5.1.1.2. Wearable Devices

- 5.1.2. Software

- 5.1.3. Services

- 5.1.1. Hardware

- 5.2. Market Analysis, Insights and Forecast - by Delivery Mode

- 5.2.1. On-Premise

- 5.2.2. Cloud-Based

- 5.3. Market Analysis, Insights and Forecast - by Patient Type

- 5.3.1. Adult

- 5.3.2. Pediatric

- 5.3.3. Geriatric

- 5.4. Market Analysis, Insights and Forecast - by Communication Technology

- 5.4.1. Video Conferencing

- 5.4.2. Audio/Voice Calls

- 5.4.3. Messaging & Chat-Based Services

- 5.5. Market Analysis, Insights and Forecast - by Application

- 5.5.1. Teleconsultation

- 5.5.2. Telemonitoring

- 5.5.3. Telemedicine

- 5.5.4. Teletherapy

- 5.5.5. Tele-Education

- 5.5.6. Others

- 5.6. Market Analysis, Insights and Forecast - by End User

- 5.6.1. Healthcare Providers

- 5.6.2. Payers

- 5.6.3. Patients

- 5.6.4. Employers

- 5.6.5. Others

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. North America

- 5.7.2. South America

- 5.7.3. Europe

- 5.7.4. Middle East & Africa

- 5.7.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 6. Global Telehealth Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Offering

- 6.1.1. Hardware

- 6.1.1.1. Monitoring Devices

- 6.1.1.2. Wearable Devices

- 6.1.2. Software

- 6.1.3. Services

- 6.1.1. Hardware

- 6.2. Market Analysis, Insights and Forecast - by Delivery Mode

- 6.2.1. On-Premise

- 6.2.2. Cloud-Based

- 6.3. Market Analysis, Insights and Forecast - by Patient Type

- 6.3.1. Adult

- 6.3.2. Pediatric

- 6.3.3. Geriatric

- 6.4. Market Analysis, Insights and Forecast - by Communication Technology

- 6.4.1. Video Conferencing

- 6.4.2. Audio/Voice Calls

- 6.4.3. Messaging & Chat-Based Services

- 6.5. Market Analysis, Insights and Forecast - by Application

- 6.5.1. Teleconsultation

- 6.5.2. Telemonitoring

- 6.5.3. Telemedicine

- 6.5.4. Teletherapy

- 6.5.5. Tele-Education

- 6.5.6. Others

- 6.6. Market Analysis, Insights and Forecast - by End User

- 6.6.1. Healthcare Providers

- 6.6.2. Payers

- 6.6.3. Patients

- 6.6.4. Employers

- 6.6.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Offering

- 7. North America Telehealth Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Offering

- 7.1.1. Hardware

- 7.1.1.1. Monitoring Devices

- 7.1.1.2. Wearable Devices

- 7.1.2. Software

- 7.1.3. Services

- 7.1.1. Hardware

- 7.2. Market Analysis, Insights and Forecast - by Delivery Mode

- 7.2.1. On-Premise

- 7.2.2. Cloud-Based

- 7.3. Market Analysis, Insights and Forecast - by Patient Type

- 7.3.1. Adult

- 7.3.2. Pediatric

- 7.3.3. Geriatric

- 7.4. Market Analysis, Insights and Forecast - by Communication Technology

- 7.4.1. Video Conferencing

- 7.4.2. Audio/Voice Calls

- 7.4.3. Messaging & Chat-Based Services

- 7.5. Market Analysis, Insights and Forecast - by Application

- 7.5.1. Teleconsultation

- 7.5.2. Telemonitoring

- 7.5.3. Telemedicine

- 7.5.4. Teletherapy

- 7.5.5. Tele-Education

- 7.5.6. Others

- 7.6. Market Analysis, Insights and Forecast - by End User

- 7.6.1. Healthcare Providers

- 7.6.2. Payers

- 7.6.3. Patients

- 7.6.4. Employers

- 7.6.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Offering

- 8. South America Telehealth Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Offering

- 8.1.1. Hardware

- 8.1.1.1. Monitoring Devices

- 8.1.1.2. Wearable Devices

- 8.1.2. Software

- 8.1.3. Services

- 8.1.1. Hardware

- 8.2. Market Analysis, Insights and Forecast - by Delivery Mode

- 8.2.1. On-Premise

- 8.2.2. Cloud-Based

- 8.3. Market Analysis, Insights and Forecast - by Patient Type

- 8.3.1. Adult

- 8.3.2. Pediatric

- 8.3.3. Geriatric

- 8.4. Market Analysis, Insights and Forecast - by Communication Technology

- 8.4.1. Video Conferencing

- 8.4.2. Audio/Voice Calls

- 8.4.3. Messaging & Chat-Based Services

- 8.5. Market Analysis, Insights and Forecast - by Application

- 8.5.1. Teleconsultation

- 8.5.2. Telemonitoring

- 8.5.3. Telemedicine

- 8.5.4. Teletherapy

- 8.5.5. Tele-Education

- 8.5.6. Others

- 8.6. Market Analysis, Insights and Forecast - by End User

- 8.6.1. Healthcare Providers

- 8.6.2. Payers

- 8.6.3. Patients

- 8.6.4. Employers

- 8.6.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Offering

- 9. Europe Telehealth Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Offering

- 9.1.1. Hardware

- 9.1.1.1. Monitoring Devices

- 9.1.1.2. Wearable Devices

- 9.1.2. Software

- 9.1.3. Services

- 9.1.1. Hardware

- 9.2. Market Analysis, Insights and Forecast - by Delivery Mode

- 9.2.1. On-Premise

- 9.2.2. Cloud-Based

- 9.3. Market Analysis, Insights and Forecast - by Patient Type

- 9.3.1. Adult

- 9.3.2. Pediatric

- 9.3.3. Geriatric

- 9.4. Market Analysis, Insights and Forecast - by Communication Technology

- 9.4.1. Video Conferencing

- 9.4.2. Audio/Voice Calls

- 9.4.3. Messaging & Chat-Based Services

- 9.5. Market Analysis, Insights and Forecast - by Application

- 9.5.1. Teleconsultation

- 9.5.2. Telemonitoring

- 9.5.3. Telemedicine

- 9.5.4. Teletherapy

- 9.5.5. Tele-Education

- 9.5.6. Others

- 9.6. Market Analysis, Insights and Forecast - by End User

- 9.6.1. Healthcare Providers

- 9.6.2. Payers

- 9.6.3. Patients

- 9.6.4. Employers

- 9.6.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Offering

- 10. Middle East & Africa Telehealth Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Offering

- 10.1.1. Hardware

- 10.1.1.1. Monitoring Devices

- 10.1.1.2. Wearable Devices

- 10.1.2. Software

- 10.1.3. Services

- 10.1.1. Hardware

- 10.2. Market Analysis, Insights and Forecast - by Delivery Mode

- 10.2.1. On-Premise

- 10.2.2. Cloud-Based

- 10.3. Market Analysis, Insights and Forecast - by Patient Type

- 10.3.1. Adult

- 10.3.2. Pediatric

- 10.3.3. Geriatric

- 10.4. Market Analysis, Insights and Forecast - by Communication Technology

- 10.4.1. Video Conferencing

- 10.4.2. Audio/Voice Calls

- 10.4.3. Messaging & Chat-Based Services

- 10.5. Market Analysis, Insights and Forecast - by Application

- 10.5.1. Teleconsultation

- 10.5.2. Telemonitoring

- 10.5.3. Telemedicine

- 10.5.4. Teletherapy

- 10.5.5. Tele-Education

- 10.5.6. Others

- 10.6. Market Analysis, Insights and Forecast - by End User

- 10.6.1. Healthcare Providers

- 10.6.2. Payers

- 10.6.3. Patients

- 10.6.4. Employers

- 10.6.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Offering

- 11. Asia Pacific Telehealth Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Offering

- 11.1.1. Hardware

- 11.1.1.1. Monitoring Devices

- 11.1.1.2. Wearable Devices

- 11.1.2. Software

- 11.1.3. Services

- 11.1.1. Hardware

- 11.2. Market Analysis, Insights and Forecast - by Delivery Mode

- 11.2.1. On-Premise

- 11.2.2. Cloud-Based

- 11.3. Market Analysis, Insights and Forecast - by Patient Type

- 11.3.1. Adult

- 11.3.2. Pediatric

- 11.3.3. Geriatric

- 11.4. Market Analysis, Insights and Forecast - by Communication Technology

- 11.4.1. Video Conferencing

- 11.4.2. Audio/Voice Calls

- 11.4.3. Messaging & Chat-Based Services

- 11.5. Market Analysis, Insights and Forecast - by Application

- 11.5.1. Teleconsultation

- 11.5.2. Telemonitoring

- 11.5.3. Telemedicine

- 11.5.4. Teletherapy

- 11.5.5. Tele-Education

- 11.5.6. Others

- 11.6. Market Analysis, Insights and Forecast - by End User

- 11.6.1. Healthcare Providers

- 11.6.2. Payers

- 11.6.3. Patients

- 11.6.4. Employers

- 11.6.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Offering

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Philips Healthcare

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Medtronic

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Honeywell Life Care Solutions

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Tunstall Healthcare

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Care Innovations

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Cerner

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Cisco

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Medvivo

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Globalmedia

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Aerotel Medical Systems

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 AMD Global Telemedicine

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 American Well

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Intouch Health

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Vidyo

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Philips Healthcare

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Telehealth Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Telehealth Revenue (billion), by Offering 2025 & 2033

- Figure 3: North America Telehealth Revenue Share (%), by Offering 2025 & 2033

- Figure 4: North America Telehealth Revenue (billion), by Delivery Mode 2025 & 2033

- Figure 5: North America Telehealth Revenue Share (%), by Delivery Mode 2025 & 2033

- Figure 6: North America Telehealth Revenue (billion), by Patient Type 2025 & 2033

- Figure 7: North America Telehealth Revenue Share (%), by Patient Type 2025 & 2033

- Figure 8: North America Telehealth Revenue (billion), by Communication Technology 2025 & 2033

- Figure 9: North America Telehealth Revenue Share (%), by Communication Technology 2025 & 2033

- Figure 10: North America Telehealth Revenue (billion), by Application 2025 & 2033

- Figure 11: North America Telehealth Revenue Share (%), by Application 2025 & 2033

- Figure 12: North America Telehealth Revenue (billion), by End User 2025 & 2033

- Figure 13: North America Telehealth Revenue Share (%), by End User 2025 & 2033

- Figure 14: North America Telehealth Revenue (billion), by Country 2025 & 2033

- Figure 15: North America Telehealth Revenue Share (%), by Country 2025 & 2033

- Figure 16: South America Telehealth Revenue (billion), by Offering 2025 & 2033

- Figure 17: South America Telehealth Revenue Share (%), by Offering 2025 & 2033

- Figure 18: South America Telehealth Revenue (billion), by Delivery Mode 2025 & 2033

- Figure 19: South America Telehealth Revenue Share (%), by Delivery Mode 2025 & 2033

- Figure 20: South America Telehealth Revenue (billion), by Patient Type 2025 & 2033

- Figure 21: South America Telehealth Revenue Share (%), by Patient Type 2025 & 2033

- Figure 22: South America Telehealth Revenue (billion), by Communication Technology 2025 & 2033

- Figure 23: South America Telehealth Revenue Share (%), by Communication Technology 2025 & 2033

- Figure 24: South America Telehealth Revenue (billion), by Application 2025 & 2033

- Figure 25: South America Telehealth Revenue Share (%), by Application 2025 & 2033

- Figure 26: South America Telehealth Revenue (billion), by End User 2025 & 2033

- Figure 27: South America Telehealth Revenue Share (%), by End User 2025 & 2033

- Figure 28: South America Telehealth Revenue (billion), by Country 2025 & 2033

- Figure 29: South America Telehealth Revenue Share (%), by Country 2025 & 2033

- Figure 30: Europe Telehealth Revenue (billion), by Offering 2025 & 2033

- Figure 31: Europe Telehealth Revenue Share (%), by Offering 2025 & 2033

- Figure 32: Europe Telehealth Revenue (billion), by Delivery Mode 2025 & 2033

- Figure 33: Europe Telehealth Revenue Share (%), by Delivery Mode 2025 & 2033

- Figure 34: Europe Telehealth Revenue (billion), by Patient Type 2025 & 2033

- Figure 35: Europe Telehealth Revenue Share (%), by Patient Type 2025 & 2033

- Figure 36: Europe Telehealth Revenue (billion), by Communication Technology 2025 & 2033

- Figure 37: Europe Telehealth Revenue Share (%), by Communication Technology 2025 & 2033

- Figure 38: Europe Telehealth Revenue (billion), by Application 2025 & 2033

- Figure 39: Europe Telehealth Revenue Share (%), by Application 2025 & 2033

- Figure 40: Europe Telehealth Revenue (billion), by End User 2025 & 2033

- Figure 41: Europe Telehealth Revenue Share (%), by End User 2025 & 2033

- Figure 42: Europe Telehealth Revenue (billion), by Country 2025 & 2033

- Figure 43: Europe Telehealth Revenue Share (%), by Country 2025 & 2033

- Figure 44: Middle East & Africa Telehealth Revenue (billion), by Offering 2025 & 2033

- Figure 45: Middle East & Africa Telehealth Revenue Share (%), by Offering 2025 & 2033

- Figure 46: Middle East & Africa Telehealth Revenue (billion), by Delivery Mode 2025 & 2033

- Figure 47: Middle East & Africa Telehealth Revenue Share (%), by Delivery Mode 2025 & 2033

- Figure 48: Middle East & Africa Telehealth Revenue (billion), by Patient Type 2025 & 2033

- Figure 49: Middle East & Africa Telehealth Revenue Share (%), by Patient Type 2025 & 2033

- Figure 50: Middle East & Africa Telehealth Revenue (billion), by Communication Technology 2025 & 2033

- Figure 51: Middle East & Africa Telehealth Revenue Share (%), by Communication Technology 2025 & 2033

- Figure 52: Middle East & Africa Telehealth Revenue (billion), by Application 2025 & 2033

- Figure 53: Middle East & Africa Telehealth Revenue Share (%), by Application 2025 & 2033

- Figure 54: Middle East & Africa Telehealth Revenue (billion), by End User 2025 & 2033

- Figure 55: Middle East & Africa Telehealth Revenue Share (%), by End User 2025 & 2033

- Figure 56: Middle East & Africa Telehealth Revenue (billion), by Country 2025 & 2033

- Figure 57: Middle East & Africa Telehealth Revenue Share (%), by Country 2025 & 2033

- Figure 58: Asia Pacific Telehealth Revenue (billion), by Offering 2025 & 2033

- Figure 59: Asia Pacific Telehealth Revenue Share (%), by Offering 2025 & 2033

- Figure 60: Asia Pacific Telehealth Revenue (billion), by Delivery Mode 2025 & 2033

- Figure 61: Asia Pacific Telehealth Revenue Share (%), by Delivery Mode 2025 & 2033

- Figure 62: Asia Pacific Telehealth Revenue (billion), by Patient Type 2025 & 2033

- Figure 63: Asia Pacific Telehealth Revenue Share (%), by Patient Type 2025 & 2033

- Figure 64: Asia Pacific Telehealth Revenue (billion), by Communication Technology 2025 & 2033

- Figure 65: Asia Pacific Telehealth Revenue Share (%), by Communication Technology 2025 & 2033

- Figure 66: Asia Pacific Telehealth Revenue (billion), by Application 2025 & 2033

- Figure 67: Asia Pacific Telehealth Revenue Share (%), by Application 2025 & 2033

- Figure 68: Asia Pacific Telehealth Revenue (billion), by End User 2025 & 2033

- Figure 69: Asia Pacific Telehealth Revenue Share (%), by End User 2025 & 2033

- Figure 70: Asia Pacific Telehealth Revenue (billion), by Country 2025 & 2033

- Figure 71: Asia Pacific Telehealth Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Telehealth Revenue billion Forecast, by Offering 2020 & 2033

- Table 2: Global Telehealth Revenue billion Forecast, by Delivery Mode 2020 & 2033

- Table 3: Global Telehealth Revenue billion Forecast, by Patient Type 2020 & 2033

- Table 4: Global Telehealth Revenue billion Forecast, by Communication Technology 2020 & 2033

- Table 5: Global Telehealth Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global Telehealth Revenue billion Forecast, by End User 2020 & 2033

- Table 7: Global Telehealth Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Global Telehealth Revenue billion Forecast, by Offering 2020 & 2033

- Table 9: Global Telehealth Revenue billion Forecast, by Delivery Mode 2020 & 2033

- Table 10: Global Telehealth Revenue billion Forecast, by Patient Type 2020 & 2033

- Table 11: Global Telehealth Revenue billion Forecast, by Communication Technology 2020 & 2033

- Table 12: Global Telehealth Revenue billion Forecast, by Application 2020 & 2033

- Table 13: Global Telehealth Revenue billion Forecast, by End User 2020 & 2033

- Table 14: Global Telehealth Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United States Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Mexico Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Global Telehealth Revenue billion Forecast, by Offering 2020 & 2033

- Table 19: Global Telehealth Revenue billion Forecast, by Delivery Mode 2020 & 2033

- Table 20: Global Telehealth Revenue billion Forecast, by Patient Type 2020 & 2033

- Table 21: Global Telehealth Revenue billion Forecast, by Communication Technology 2020 & 2033

- Table 22: Global Telehealth Revenue billion Forecast, by Application 2020 & 2033

- Table 23: Global Telehealth Revenue billion Forecast, by End User 2020 & 2033

- Table 24: Global Telehealth Revenue billion Forecast, by Country 2020 & 2033

- Table 25: Brazil Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Argentina Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of South America Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Telehealth Revenue billion Forecast, by Offering 2020 & 2033

- Table 29: Global Telehealth Revenue billion Forecast, by Delivery Mode 2020 & 2033

- Table 30: Global Telehealth Revenue billion Forecast, by Patient Type 2020 & 2033

- Table 31: Global Telehealth Revenue billion Forecast, by Communication Technology 2020 & 2033

- Table 32: Global Telehealth Revenue billion Forecast, by Application 2020 & 2033

- Table 33: Global Telehealth Revenue billion Forecast, by End User 2020 & 2033

- Table 34: Global Telehealth Revenue billion Forecast, by Country 2020 & 2033

- Table 35: United Kingdom Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Germany Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: France Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Italy Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Spain Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Russia Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: Benelux Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Nordics Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: Rest of Europe Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Global Telehealth Revenue billion Forecast, by Offering 2020 & 2033

- Table 45: Global Telehealth Revenue billion Forecast, by Delivery Mode 2020 & 2033

- Table 46: Global Telehealth Revenue billion Forecast, by Patient Type 2020 & 2033

- Table 47: Global Telehealth Revenue billion Forecast, by Communication Technology 2020 & 2033

- Table 48: Global Telehealth Revenue billion Forecast, by Application 2020 & 2033

- Table 49: Global Telehealth Revenue billion Forecast, by End User 2020 & 2033

- Table 50: Global Telehealth Revenue billion Forecast, by Country 2020 & 2033

- Table 51: Turkey Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Israel Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 53: GCC Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: North Africa Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 55: South Africa Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: Rest of Middle East & Africa Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 57: Global Telehealth Revenue billion Forecast, by Offering 2020 & 2033

- Table 58: Global Telehealth Revenue billion Forecast, by Delivery Mode 2020 & 2033

- Table 59: Global Telehealth Revenue billion Forecast, by Patient Type 2020 & 2033

- Table 60: Global Telehealth Revenue billion Forecast, by Communication Technology 2020 & 2033

- Table 61: Global Telehealth Revenue billion Forecast, by Application 2020 & 2033

- Table 62: Global Telehealth Revenue billion Forecast, by End User 2020 & 2033

- Table 63: Global Telehealth Revenue billion Forecast, by Country 2020 & 2033

- Table 64: China Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 65: India Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: Japan Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 67: South Korea Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: ASEAN Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 69: Oceania Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: Rest of Asia Pacific Telehealth Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Telehealth?

The projected CAGR is approximately 24.11%.

2. Which companies are prominent players in the Telehealth?

Key companies in the market include Philips Healthcare, Medtronic, Honeywell Life Care Solutions, Tunstall Healthcare, Care Innovations, Cerner, Cisco, Medvivo, Globalmedia, Aerotel Medical Systems, AMD Global Telemedicine, American Well, Intouch Health, Vidyo.

3. What are the main segments of the Telehealth?

The market segments include Offering, Delivery Mode, Patient Type, Communication Technology, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 78.25 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Telehealth," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Telehealth report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Telehealth?

To stay informed about further developments, trends, and reports in the Telehealth, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence