Key Insights

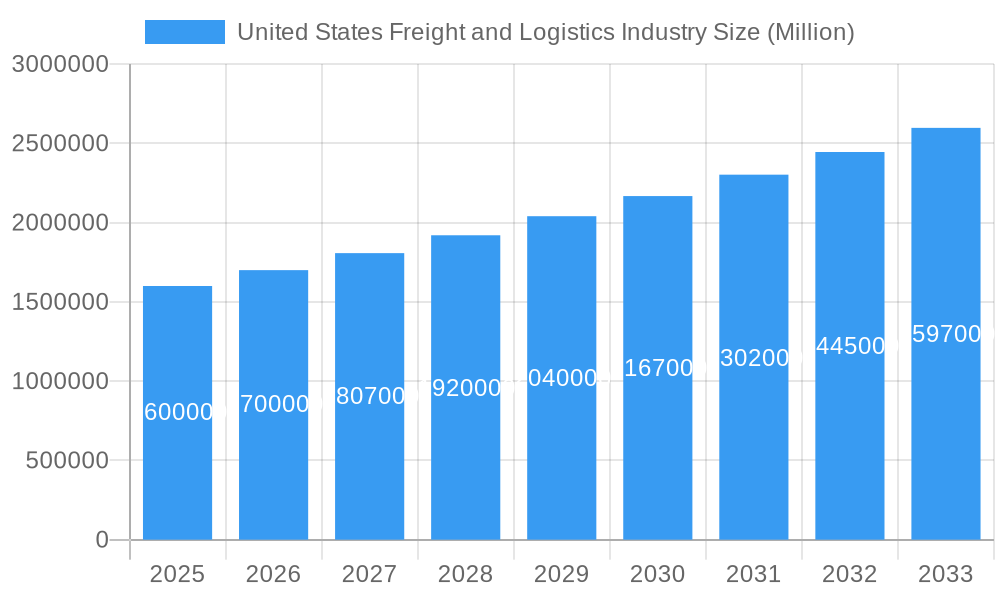

The United States freight and logistics market is a significant and evolving sector, propelled by the surge in e-commerce, strategic supply chain diversification, and expanding industrial output. The market, valued at $1.6 billion in 2025, is projected to grow at a Compound Annual Growth Rate (CAGR) of 0.6% from 2025 to 2033. Key growth catalysts include the increasing demand for efficient last-mile delivery driven by e-commerce, the necessity for temperature-controlled logistics for sensitive goods, and the growing intricacy of global supply chains necessitating specialized logistics partners. Technological innovations such as automation, AI-driven route optimization, and real-time tracking are enhancing supply chain efficiency and visibility. The industry is segmented by end-user sectors including Agriculture, Fishing, and Forestry; Construction; Manufacturing; Oil and Gas; Mining and Quarrying; Wholesale and Retail Trade; and Others. Logistics functions are categorized into Courier, Express, and Parcel (CEP); Temperature Controlled; and Other Services, presenting varied opportunities for businesses.

United States Freight and Logistics Industry Market Size (In Billion)

Dominant industry trends feature the widespread adoption of omnichannel fulfillment, the integration of sustainable logistics practices like fuel-efficient vehicles and emission reduction, and a rising demand for specialized logistics for unique cargo, such as oversized or hazardous materials. Growth impediments include persistent labor shortages in trucking and warehousing, fluctuations in fuel prices, and the imperative for substantial infrastructure investment to manage escalating freight volumes. Leading industry participants, including UPS, FedEx, DHL, and DB Schenker, are competing through innovation, strategic acquisitions, and service portfolio expansion to meet dynamic customer requirements. Sustained market expansion hinges on effectively addressing labor concerns, optimizing technology investments, and ensuring regulatory consistency in the transportation sector.

United States Freight and Logistics Industry Company Market Share

United States Freight & Logistics Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the United States freight and logistics industry, covering market dynamics, growth trends, key players, and future outlook. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report offers invaluable insights for industry professionals, investors, and strategists. The report analyzes key segments including End User Industries (Agriculture, Fishing & Forestry, Construction, Manufacturing, Oil & Gas, Mining & Quarrying, Wholesale & Retail Trade, Others) and Logistics Functions (Courier, Express, & Parcel (CEP), Temperature Controlled, Other Services). The report quantifies market size in million units.

United States Freight and Logistics Industry Market Dynamics & Structure

The US freight and logistics market is characterized by a dynamic interplay of factors shaping its structure and growth trajectory. Market concentration is moderate, with several large players holding significant market share, but also numerous smaller niche operators. Technological innovation, particularly in areas like AI-powered route optimization and autonomous vehicles, is a major driver. Stringent regulatory frameworks, including safety and environmental regulations, significantly impact operational costs and strategies. The industry faces competition from substitute modes of transportation (e.g., rail versus trucking) and is subject to macroeconomic fluctuations influencing demand. Mergers and acquisitions (M&A) activity is significant, reflecting industry consolidation and the pursuit of scale and efficiency.

- Market Concentration: The top 10 players account for approximately xx% of the market (2024 estimate).

- Technological Innovation: Investment in AI, IoT, and automation is driving efficiency gains and cost reductions. However, significant barriers include the high initial investment cost and integration challenges.

- Regulatory Framework: Compliance with federal and state regulations on safety, emissions, and labor is a major concern, impacting operational costs.

- M&A Activity: The historical period (2019-2024) witnessed approximately xx M&A deals annually (estimated). Consolidation is expected to continue.

- End-User Demographics: The manufacturing and retail sectors remain major drivers of freight demand, but growth in e-commerce is reshaping logistics needs.

United States Freight and Logistics Industry Growth Trends & Insights

The US freight and logistics market experienced robust growth during the historical period (2019-2024), driven by factors such as economic expansion, increasing e-commerce penetration, and the ongoing shift towards supply chain optimization. The market size grew from xx million units in 2019 to xx million units in 2024, exhibiting a compound annual growth rate (CAGR) of xx%. Technological disruptions, such as the adoption of automation and AI, are accelerating efficiency and impacting consumer behavior, with a shift towards faster and more transparent delivery options. Continued investment in infrastructure and emerging technologies will shape the future trajectory of market growth. Market penetration of advanced technologies like autonomous trucks is still relatively low but is projected to significantly increase over the forecast period. Consumer behavior increasingly favors on-demand delivery and real-time tracking, pushing logistics providers to enhance their technology capabilities.

Dominant Regions, Countries, or Segments in United States Freight and Logistics Industry

The dominant segment within the US freight and logistics industry is determined by a combination of factors including infrastructure development, economic activity, and regulatory environment. While precise market share figures for each segment require detailed analysis from the comprehensive report, some trends are clear. The Manufacturing sector remains a significant driver, representing xx% of market share in 2024 (estimated). The growth of e-commerce is boosting the Courier, Express, and Parcel (CEP) segment, though data for exact market share requires in-depth analysis. Geographically, regions with high population density and robust industrial activity (e.g., the East Coast and major metropolitan areas) tend to dominate.

- Key Drivers:

- Robust manufacturing output in key states.

- High population density in major cities fostering higher demand for CEP services.

- Development of efficient transportation networks, particularly rail and highway.

- Dominance Factors:

- Strong manufacturing base.

- Well-developed infrastructure (road, rail, air).

- High population density in key regions driving demand.

United States Freight and Logistics Industry Product Landscape

The US freight and logistics industry is witnessing significant product innovation, with a focus on enhanced visibility, real-time tracking, and predictive analytics. New technologies, such as AI-powered route optimization software and blockchain-based supply chain transparency platforms are transforming operational efficiency. Companies are increasingly offering customized solutions tailored to specific industry needs, such as temperature-controlled transport for pharmaceuticals and specialized handling for oversized cargo. These advancements enhance the reliability, speed, and cost-effectiveness of freight transportation.

Key Drivers, Barriers & Challenges in United States Freight and Logistics Industry

Key Drivers:

- E-commerce growth increasing demand for faster and more reliable delivery.

- Technological advancements improving efficiency and reducing costs.

- Infrastructure investments (e.g., port modernization).

Challenges & Restraints:

- Driver shortages impacting capacity and reliability.

- Fluctuating fuel prices impacting transportation costs.

- Increasing regulatory compliance burdens.

- Supply chain disruptions (e.g., port congestion, geopolitical factors). These challenges resulted in an estimated xx% increase in transportation costs in 2024 (estimated).

Emerging Opportunities in United States Freight and Logistics Industry

- Last-mile delivery solutions: Optimization of final delivery segment for e-commerce.

- Sustainable logistics: Growing demand for environmentally friendly transportation methods (e.g., electric vehicles).

- Data analytics: Leveraging data to optimize routes, improve efficiency, and predict disruptions.

- Autonomous vehicles: Potential to automate trucking and other transportation modes.

Growth Accelerators in the United States Freight and Logistics Industry

Technological innovation will be a key growth driver, particularly the adoption of AI, automation, and the Internet of Things (IoT). Strategic partnerships between logistics providers and technology companies will fuel further development. Expansion into new markets, such as specialized transportation segments (e.g., healthcare logistics), and investments in infrastructure improvements will contribute to market growth. A focus on sustainability, by adopting eco-friendly practices, will appeal to environmentally conscious businesses and consumers, driving market demand.

Key Players Shaping the United States Freight and Logistics Industry Market

Notable Milestones in United States Freight and Logistics Industry Sector

- November 2023: DB Schenker partnered with American Airlines Cargo to launch an API connection for airfreight booking, streamlining processes.

- January 2024: Kuehne + Nagel introduced its Book & Claim insetting solution for electric vehicles to enhance decarbonization efforts.

- February 2024: C.H. Robinson developed new AI-powered technology to optimize freight appointment scheduling, improving efficiency.

In-Depth United States Freight and Logistics Industry Market Outlook

The future of the US freight and logistics industry is bright, driven by continued technological advancements, increased e-commerce penetration, and growing demand for efficient and sustainable solutions. Strategic partnerships and investments in infrastructure will unlock further growth potential. Market expansion into niche segments and a focus on sustainability will create lucrative opportunities for players. The forecast period (2025-2033) is expected to witness significant market expansion, with a projected CAGR of xx% (estimated). Companies that embrace innovation, adapt to evolving consumer demands, and invest in sustainable practices will be best positioned to thrive in this dynamic market.

United States Freight and Logistics Industry Segmentation

-

1. End User Industry

- 1.1. Agriculture, Fishing, and Forestry

- 1.2. Construction

- 1.3. Manufacturing

- 1.4. Oil and Gas, Mining and Quarrying

- 1.5. Wholesale and Retail Trade

- 1.6. Others

-

2. Logistics Function

-

2.1. Courier, Express, and Parcel (CEP)

-

2.1.1. By Destination Type

- 2.1.1.1. Domestic

- 2.1.1.2. International

-

2.1.1. By Destination Type

-

2.2. Freight Forwarding

-

2.2.1. By Mode Of Transport

- 2.2.1.1. Air

- 2.2.1.2. Sea and Inland Waterways

- 2.2.1.3. Others

-

2.2.1. By Mode Of Transport

-

2.3. Freight Transport

- 2.3.1. Pipelines

- 2.3.2. Rail

- 2.3.3. Road

-

2.4. Warehousing and Storage

-

2.4.1. By Temperature Control

- 2.4.1.1. Non-Temperature Controlled

-

2.4.1. By Temperature Control

- 2.5. Other Services

-

2.1. Courier, Express, and Parcel (CEP)

United States Freight and Logistics Industry Segmentation By Geography

- 1. United States

United States Freight and Logistics Industry Regional Market Share

Geographic Coverage of United States Freight and Logistics Industry

United States Freight and Logistics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 0.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing trade relations; Increased demand for perishable goods

- 3.3. Market Restrains

- 3.3.1. Cargo theft; High cost of maintainig

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. United States Freight and Logistics Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Agriculture, Fishing, and Forestry

- 5.1.2. Construction

- 5.1.3. Manufacturing

- 5.1.4. Oil and Gas, Mining and Quarrying

- 5.1.5. Wholesale and Retail Trade

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Logistics Function

- 5.2.1. Courier, Express, and Parcel (CEP)

- 5.2.1.1. By Destination Type

- 5.2.1.1.1. Domestic

- 5.2.1.1.2. International

- 5.2.1.1. By Destination Type

- 5.2.2. Freight Forwarding

- 5.2.2.1. By Mode Of Transport

- 5.2.2.1.1. Air

- 5.2.2.1.2. Sea and Inland Waterways

- 5.2.2.1.3. Others

- 5.2.2.1. By Mode Of Transport

- 5.2.3. Freight Transport

- 5.2.3.1. Pipelines

- 5.2.3.2. Rail

- 5.2.3.3. Road

- 5.2.4. Warehousing and Storage

- 5.2.4.1. By Temperature Control

- 5.2.4.1.1. Non-Temperature Controlled

- 5.2.4.1. By Temperature Control

- 5.2.5. Other Services

- 5.2.1. Courier, Express, and Parcel (CEP)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 DB Schenker

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 United Parcel Service of America Inc (UPS

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 DHL Group

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 DSV A/S (De Sammensluttede Vognmænd af Air and Sea)

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Penske Logistics

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 FedEx

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 GXO Logistics

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Kuehne + Nagel

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 C H Robinson

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 NFI Industries

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 J B Hunt Transport Inc

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Expeditors International of Washington Inc

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.1 DB Schenker

List of Figures

- Figure 1: United States Freight and Logistics Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: United States Freight and Logistics Industry Share (%) by Company 2025

List of Tables

- Table 1: United States Freight and Logistics Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 2: United States Freight and Logistics Industry Revenue billion Forecast, by Logistics Function 2020 & 2033

- Table 3: United States Freight and Logistics Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: United States Freight and Logistics Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 5: United States Freight and Logistics Industry Revenue billion Forecast, by Logistics Function 2020 & 2033

- Table 6: United States Freight and Logistics Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Freight and Logistics Industry?

The projected CAGR is approximately 0.6%.

2. Which companies are prominent players in the United States Freight and Logistics Industry?

Key companies in the market include DB Schenker, United Parcel Service of America Inc (UPS, DHL Group, DSV A/S (De Sammensluttede Vognmænd af Air and Sea), Penske Logistics, FedEx, GXO Logistics, Kuehne + Nagel, C H Robinson, NFI Industries, J B Hunt Transport Inc, Expeditors International of Washington Inc.

3. What are the main segments of the United States Freight and Logistics Industry?

The market segments include End User Industry, Logistics Function.

4. Can you provide details about the market size?

The market size is estimated to be USD 4 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing trade relations; Increased demand for perishable goods.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Cargo theft; High cost of maintainig.

8. Can you provide examples of recent developments in the market?

February 2024: C.H. Robinson has developed a new technology that creates a major efficiency in freight shipping: removing the work of scheduling an appointment at the place where a load needs to be picked up and scheduling another appointment where the load needs to be delivered. The technology also uses artificial intelligence to determine the optimal appointment, based on transit-time data from C.H. Robinson’s millions of shipments across 300,000 shipping lanes.January 2024: Kuehne + Nagel has announced its Book & Claim insetting solution for electric vehicles, to improve its decarbonization solutions. Developing Book & Claim insetting solutions for road freight was a strategic priority for Kuehne + Nagel. Customers who use Kuehne + Nagel's road transport services can now claim the carbon reductions of electric trucks when it is not possible to physically move their goods on these vehicles.November 2023: DB Schenker, in partnership with American Airlines Cargo, announces an advancement in airfreight operations. The introduction of an API (Application Programming Interface) connection, introduced on November 14th, 2023, marks the next step in digitalizing and streamlining airfreight booking processes.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Freight and Logistics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Freight and Logistics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Freight and Logistics Industry?

To stay informed about further developments, trends, and reports in the United States Freight and Logistics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence