Key Insights

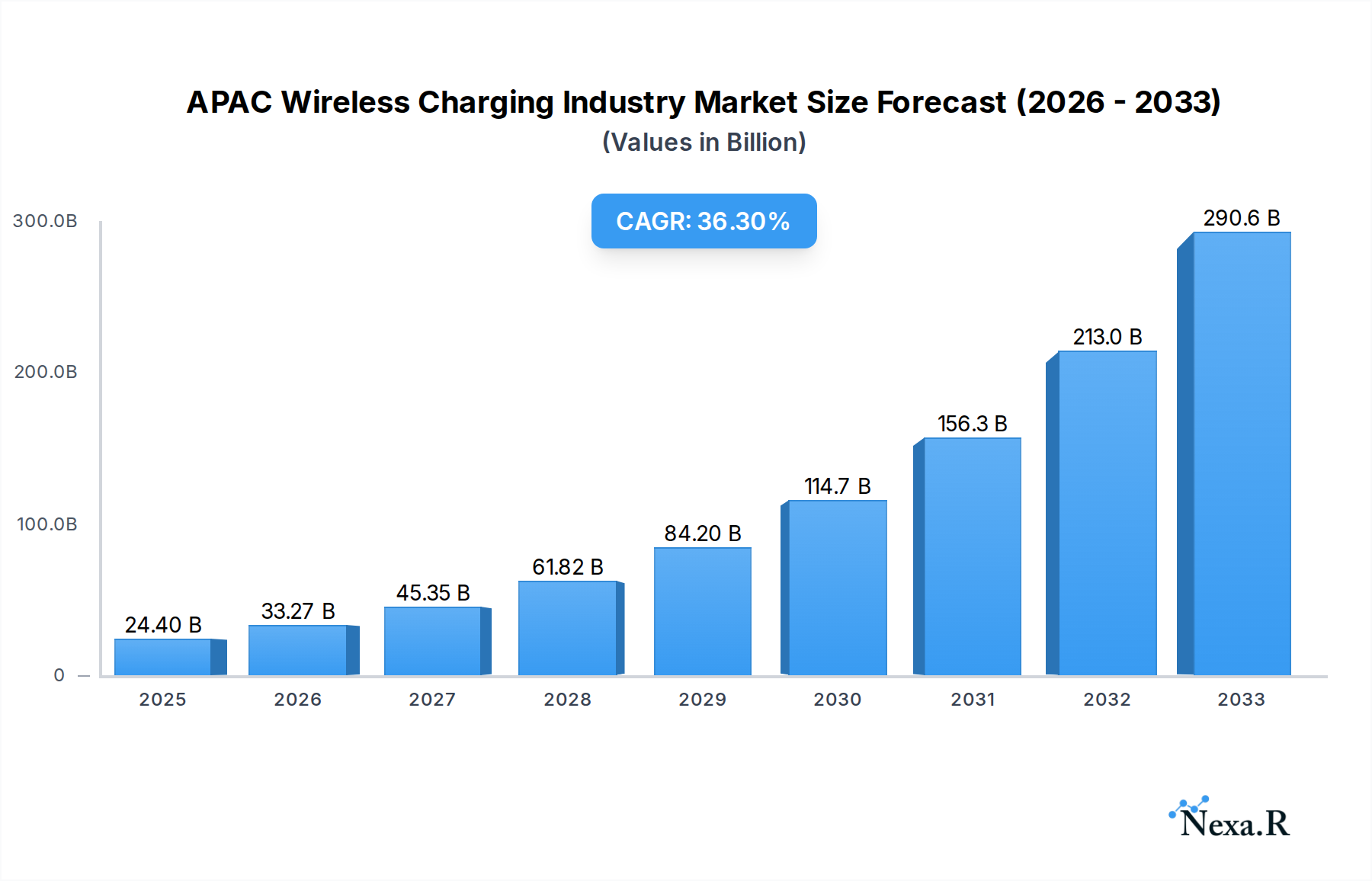

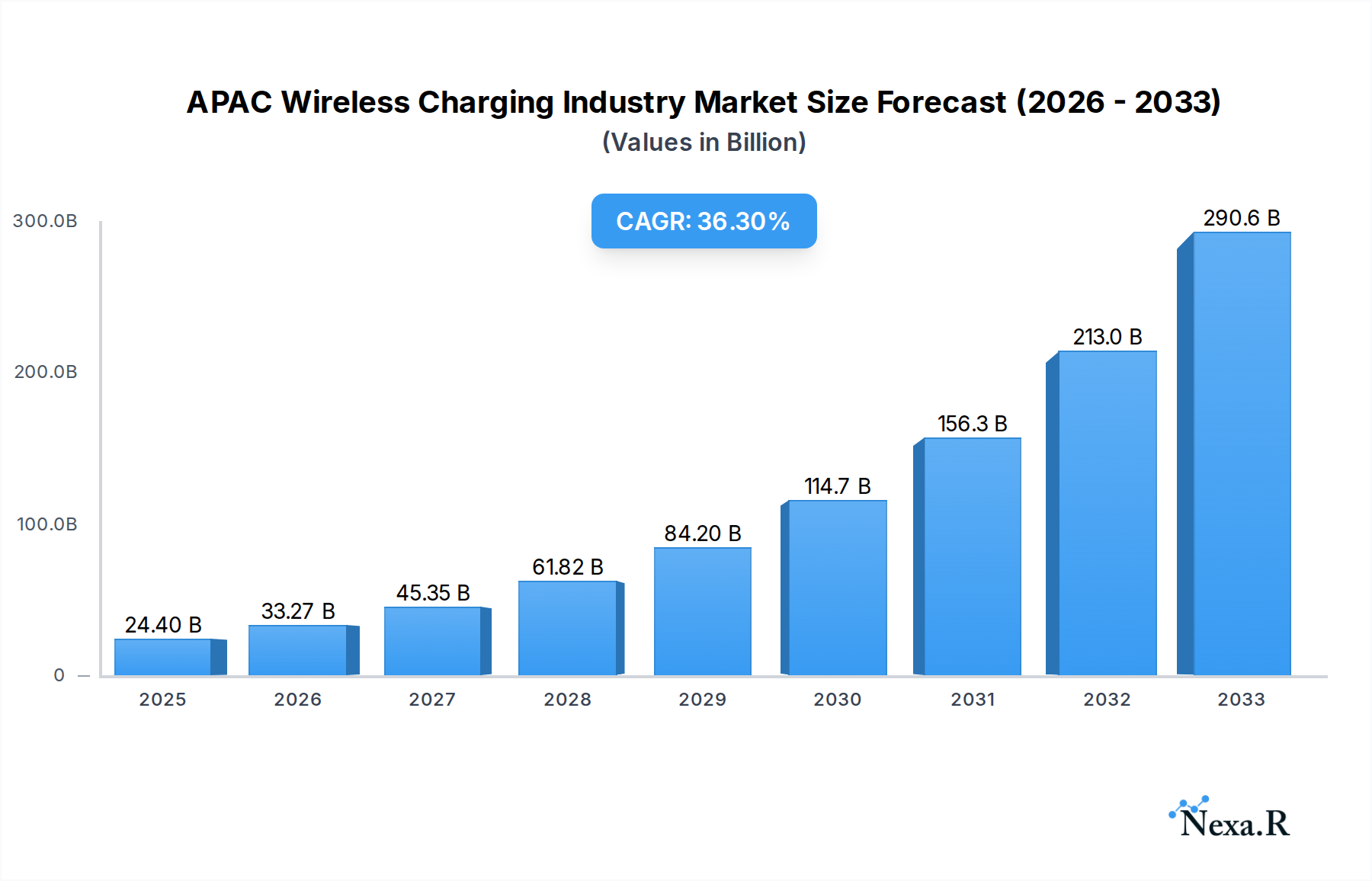

The APAC Wireless Charging Industry is poised for exceptional growth, projected to reach USD 24.4 billion in 2025, driven by a remarkable CAGR of 36.2% over the forecast period. This explosive expansion is underpinned by several powerful catalysts, most notably the escalating adoption of electric vehicles (EVs) across the region. As governments in countries like China, Japan, and South Korea champion EV incentives and expand charging infrastructure, the demand for seamless and convenient charging solutions, such as wireless charging, is set to skyrocket. Furthermore, advancements in charging technology, leading to faster speeds, increased efficiency, and greater interoperability, are directly contributing to market acceleration. The burgeoning consumer preference for sophisticated and integrated automotive features, coupled with a growing awareness of the benefits of wireless charging in terms of reduced cable clutter and enhanced user experience, further fuels this upward trajectory. The integration of wireless charging in public spaces and commercial fleets is also emerging as a significant driver, expanding the market's reach beyond individual vehicle owners.

APAC Wireless Charging Industry Market Size (In Billion)

Despite this robust growth, certain challenges could temper the pace of adoption. High initial installation costs for wireless charging infrastructure and vehicles, coupled with the need for standardization across different charging protocols and vehicle manufacturers, remain key concerns for widespread market penetration. However, these restraints are progressively being addressed through technological innovation and collaborative efforts within the industry. The market is segmenting significantly, with Battery Electric Vehicles (BEVs) leading the charge, followed closely by Plug-in Hybrid Vehicles (PHEVs). Major players such as Tesla Motors, Toyota Motor Corporation, and Nissan are actively investing in and developing wireless charging solutions, signaling a competitive landscape and a strong commitment to this transformative technology. The Asia Pacific region, particularly China, is expected to dominate the market due to its leading position in EV manufacturing and adoption.

APAC Wireless Charging Industry Company Market Share

APAC Wireless Charging Industry Report: Market Analysis, Trends, and Future Outlook (2019-2033)

Unlock the future of electric vehicle (EV) charging in the Asia-Pacific region with our comprehensive report on the APAC Wireless Charging Industry. This in-depth analysis provides critical insights into market dynamics, growth trajectories, technological innovations, and competitive landscapes, essential for stakeholders navigating this rapidly evolving sector. Focusing on the seamless integration of convenience and sustainability, this report delves into the parent market of electric vehicle charging infrastructure and its vital child market, wireless charging solutions.

This report examines the APAC Wireless Charging Industry, covering the Battery Electric Vehicle (BEV) and Plug-in Hybrid Vehicle (PHEV) segments. Utilizing data from the Historical Period (2019–2024), Base Year (2025), and extending to the Forecast Period (2025–2033), this study offers a robust outlook on market evolution.

APAC Wireless Charging Industry Market Dynamics & Structure

The APAC Wireless Charging Industry is characterized by a dynamic and evolving market structure. While still in its nascent stages compared to the broader electric vehicle charging market, the wireless charging segment is witnessing increasing consolidation driven by technological advancements and strategic partnerships. Key drivers of innovation include the growing demand for autonomous driving, enhanced consumer convenience, and the need for more efficient EV charging infrastructure. Regulatory frameworks are gradually adapting to accommodate this nascent technology, with several countries in the APAC region actively developing standards and guidelines. Competitive product substitutes, primarily traditional plug-in charging solutions, remain a significant factor, but the unique advantages of wireless charging, such as ease of use and enhanced safety, are steadily gaining traction. End-user demographics are shifting towards tech-savvy early adopters and premium vehicle owners, who are more inclined to embrace innovative charging solutions. Mergers and acquisitions (M&A) trends are expected to accelerate as established automotive players and technology companies seek to secure intellectual property and market share in this high-growth area. The market concentration is currently moderate, with a few key players leading in technological development, but this is likely to diversify as the market matures.

- Market Concentration: Moderate, with increasing M&A activity expected.

- Technological Innovation Drivers: Autonomous driving, enhanced consumer convenience, and infrastructure efficiency.

- Regulatory Frameworks: Emerging and evolving, with a focus on standardization and safety.

- Competitive Product Substitutes: Primarily plug-in charging solutions, with wireless charging offering distinct advantages.

- End-User Demographics: Early adopters, premium vehicle owners, and smart city initiatives.

- M&A Trends: Expected to increase as companies secure IP and market positions.

APAC Wireless Charging Industry Growth Trends & Insights

The APAC Wireless Charging Industry is poised for substantial growth, driven by a confluence of factors that are reshaping the electric vehicle landscape. The market size evolution is anticipated to witness a significant upward trajectory throughout the forecast period, fueled by increasing EV adoption rates across the region. Technological disruptions, such as advancements in charging efficiency, power transfer capabilities, and standardization efforts, are playing a pivotal role in accelerating this growth. Consumer behavior shifts are also a critical element, with a growing preference for hassle-free and integrated charging experiences, which wireless technology perfectly embodies. The sheer volume of electric vehicles being deployed in key APAC markets presents a vast addressable market for wireless charging solutions. We project a Compound Annual Growth Rate (CAGR) that will significantly outpace that of traditional charging methods, reflecting the disruptive potential of this technology. Market penetration is expected to climb steadily, initially driven by premium vehicle segments and later expanding to mass-market EVs as costs decrease and infrastructure becomes more widespread. The integration of wireless charging into public spaces, parking facilities, and even roadways signifies a paradigm shift in how EVs will be powered, moving towards a more seamless and ubiquitous charging ecosystem. The increasing investment in EV infrastructure, coupled with supportive government policies, further solidifies the optimistic outlook for wireless charging adoption in APAC.

Dominant Regions, Countries, or Segments in APAC Wireless Charging Industry

The Battery Electric Vehicle (BEV) segment is unequivocally the dominant force driving the APAC Wireless Charging Industry's growth. This dominance stems from several interconnected factors, including government mandates, rapid technological advancements in battery technology, and a heightened consumer awareness regarding environmental sustainability. Countries like China, a global leader in EV production and adoption, are at the forefront, with supportive policies and substantial investments in charging infrastructure, including wireless solutions. The sheer volume of BEVs hitting the roads in China creates an immediate and substantial market for wireless charging integration.

- Key Drivers in China:

- Government subsidies and incentives for EV adoption.

- Ambitious targets for EV sales and charging infrastructure development.

- Strong domestic automotive manufacturers investing heavily in EV technology, including wireless charging.

- Development of smart city initiatives integrating advanced charging solutions.

- Market Share and Growth Potential: China alone represents a significant portion of the global BEV market and is expected to continue leading in the adoption of wireless charging technologies within this segment.

Beyond China, other key APAC nations are increasingly focusing on BEV adoption, further bolstering the wireless charging market. Japan and South Korea, with their advanced automotive industries and technological prowess, are also significant contributors. Their commitment to innovation and the development of next-generation vehicle technologies positions them as crucial markets for wireless charging.

- Factors contributing to BEV segment dominance:

- Technological Advancement: Continuous improvements in battery capacity and charging speeds make BEVs more practical and appealing.

- Environmental Consciousness: Growing public concern over climate change is driving demand for zero-emission vehicles.

- Infrastructure Development: Strategic investments in charging networks, with a growing emphasis on wireless solutions for convenience.

- Fleet Electrification: Commercial fleets are increasingly transitioning to BEVs, creating large-scale demand for efficient charging.

While Plug-in Hybrid Vehicles (PHEVs) also contribute to the market, the long-term trend and strategic focus are overwhelmingly on fully electric vehicles, making the BEV segment the primary engine of growth for APAC wireless charging solutions. The scalability and inherent advantages of wireless charging are best realized in a predominantly BEV ecosystem.

APAC Wireless Charging Industry Product Landscape

The product landscape of the APAC Wireless Charging Industry is defined by an accelerating pace of innovation, focusing on higher power transfer, improved efficiency, and enhanced safety features. Companies are developing advanced wireless charging pads and receivers designed for seamless integration into vehicles, from passenger cars to public transportation. Applications are expanding beyond simple at-home charging to include dynamic wireless charging capabilities for in-road charging systems, enabling continuous power replenishment during transit. Performance metrics are steadily improving, with higher kilowatt (kW) charging capabilities becoming more prevalent, rivaling the speeds of some plug-in chargers. Unique selling propositions include the elimination of cable entanglement, increased user convenience, and enhanced safety by reducing exposure to electrical components. Technological advancements are centered around efficient energy transfer coils, sophisticated foreign object detection systems, and robust communication protocols for seamless authentication and billing.

Key Drivers, Barriers & Challenges in APAC Wireless Charging Industry

Key Drivers:

The APAC Wireless Charging Industry is propelled by several powerful forces. Technological innovation in power electronics and inductive charging coil design is a primary driver, enabling higher efficiency and faster charging speeds. Government initiatives and supportive policies across numerous APAC nations, promoting EV adoption and infrastructure development, are crucial. The growing consumer demand for convenience and a seamless user experience, particularly in urban environments, is a significant catalyst. Furthermore, the increasing deployment of electric vehicles, especially Battery Electric Vehicles (BEVs), creates a substantial addressable market. Strategic investments by automotive manufacturers and technology companies in R&D and infrastructure development are accelerating market growth.

- Technological Advancements: Higher power transfer, increased efficiency.

- Government Support: Pro-EV policies and infrastructure mandates.

- Consumer Demand: Convenience and ease of use.

- EV Adoption: Growing fleet sizes.

- Industry Investment: R&D and infrastructure funding.

Barriers & Challenges:

Despite its promise, the industry faces significant barriers and challenges. High initial infrastructure deployment costs for wireless charging stations and the need for standardization across different manufacturers pose considerable hurdles. The current power transfer limitations of some wireless systems compared to fast-plug-in chargers can be a deterrent for consumers requiring rapid charging. Public awareness and education about the benefits and functionalities of wireless charging are still developing. Supply chain complexities and the availability of raw materials for advanced charging components can also present challenges. Regulatory frameworks, while evolving, may still lack comprehensive guidelines for safety and interoperability, leading to uncertainty for market players.

- High Infrastructure Costs: Significant upfront investment required.

- Standardization Issues: Lack of universal protocols.

- Power Transfer Limitations: Slower charging speeds compared to some plug-in options.

- Public Awareness: Need for greater consumer understanding.

- Supply Chain Constraints: Availability of specialized components.

- Regulatory Hurdles: Evolving and sometimes inconsistent guidelines.

Emerging Opportunities in APAC Wireless Charging Industry

Emerging opportunities in the APAC Wireless Charging Industry are abundant and diverse. The expansion of wireless charging into public parking lots, commercial fleet depots, and even street parking presents a vast untapped market. The development of higher-power wireless charging solutions capable of rapidly charging heavy-duty commercial vehicles and buses represents a significant growth avenue. Integration with smart city infrastructure, enabling vehicle-to-grid (V2G) capabilities through wireless interfaces, offers innovative applications. Furthermore, the evolving consumer preference for integrated and aesthetically pleasing charging solutions will drive demand for in-home wireless charging systems that blend seamlessly with residential environments. The potential for dynamic wireless charging, where vehicles can charge while in motion on dedicated road sections, opens up revolutionary possibilities for continuous mobility.

Growth Accelerators in the APAC Wireless Charging Industry Industry

Several catalysts are poised to accelerate long-term growth in the APAC Wireless Charging Industry. Breakthroughs in materials science and power electronics are expected to enhance charging efficiency, reduce costs, and enable higher power transfer rates, making wireless charging more competitive with plug-in solutions. Strategic partnerships between automotive manufacturers, technology providers, and infrastructure developers are crucial for scaling deployment and ensuring interoperability. Market expansion strategies targeting developing economies within APAC, where the adoption of EVs is rapidly gaining momentum, will unlock new customer bases. The increasing focus on autonomous vehicles will further drive demand for seamless, hands-free charging solutions. Continued government support through incentives and clear regulatory roadmaps will foster investment and adoption.

Key Players Shaping the APAC Wireless Charging Industry Market

- Tesla Motors

- Daimler AG

- OLEV Technologies

- BMW AG

- Plugless

- Bombardier

- Toyota Motor Corporation

- Nissan

- Hella Aglaia

- HEVO Power

- WiTricity

- Qualcomm

Notable Milestones in APAC Wireless Charging Industry Sector

- June 2023: ST Microelectronics NV unveiled cutting-edge products for the smart mobility sector at MWC Shanghai, including the ST P-BOX Solution for autonomous driving and a 100W Wireless Charging Solution based on STWBC2-HP and STWLC99 platforms.

- June 2023: SAIC-GM commenced deliveries of the Buick Electra E5, a 5-seater intelligent electric SUV featuring the industry's first battery management system with wireless connectivity and a BEV HEAT thermal management system.

- May 2023: Malaysia's MITI announced a USD 422.3 million investment by China-based EVE Energy Co., Ltd. in Kulim, with ongoing policy exploration supporting charging systems, battery disposal, battery swapping, and wireless charging.

In-Depth APAC Wireless Charging Industry Market Outlook

The future outlook for the APAC Wireless Charging Industry is exceptionally promising, driven by a confluence of technological advancements and evolving consumer preferences. As EV adoption continues its exponential rise, the demand for convenient, safe, and integrated charging solutions will intensify. Growth accelerators such as breakthroughs in charging efficiency and power transfer capabilities will make wireless technology increasingly competitive. Strategic alliances between key industry players will streamline deployment and foster interoperability, creating a more robust ecosystem. Untapped markets in emerging economies within APAC offer significant potential for expansion. The evolving consumer preference for seamless and automated experiences further solidifies the long-term market potential for wireless charging. Strategic opportunities lie in developing solutions for dynamic charging, fleet electrification, and integration with smart grid technologies, positioning the APAC region as a global leader in the wireless charging revolution for electric vehicles.

APAC Wireless Charging Industry Segmentation

-

1. Vehicle Type

- 1.1. Battery Electric Vehicle

- 1.2. Plug-in Hybrid Vehicle

APAC Wireless Charging Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

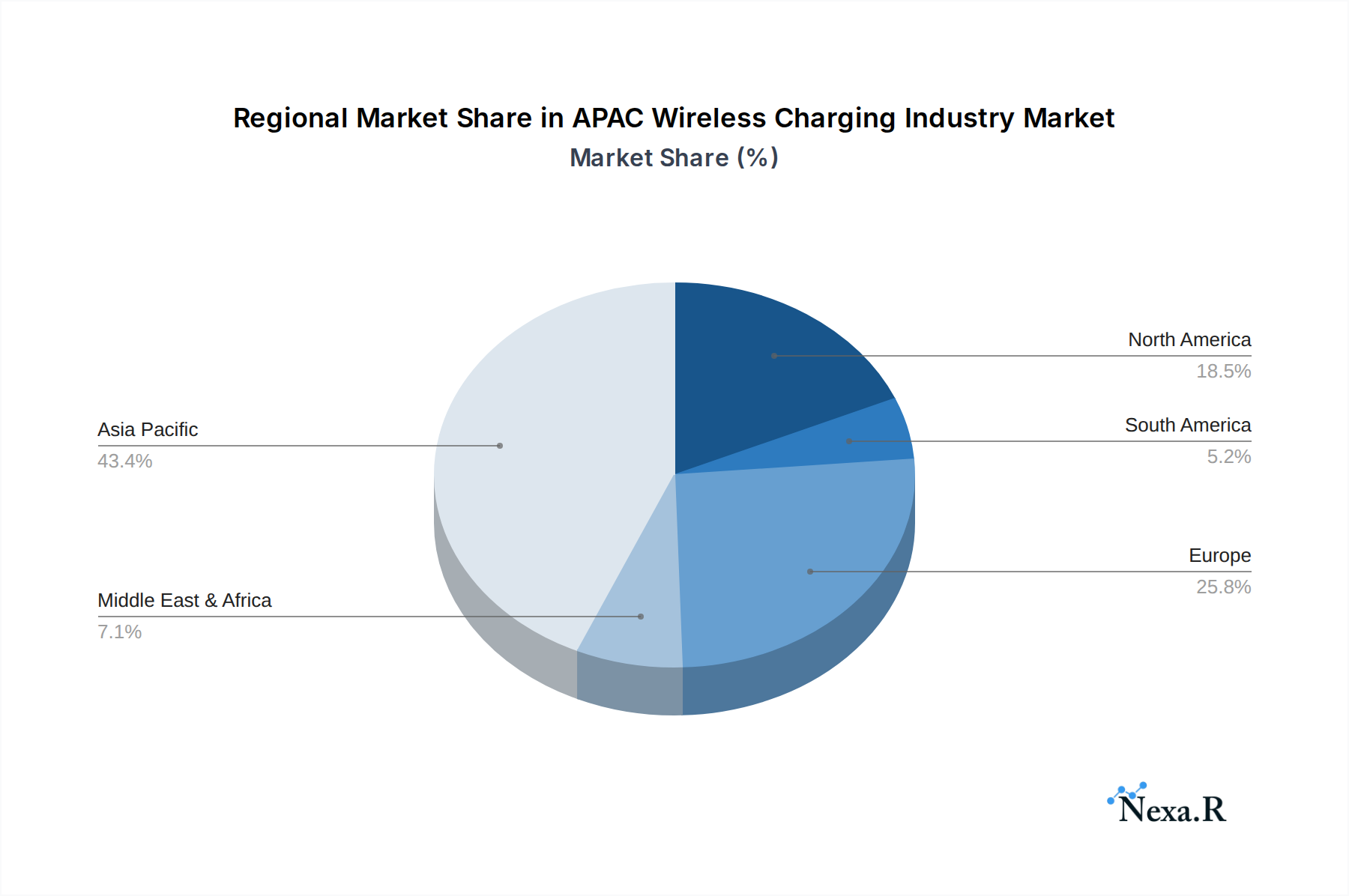

APAC Wireless Charging Industry Regional Market Share

Geographic Coverage of APAC Wireless Charging Industry

APAC Wireless Charging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 36.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Battery Electric Vehicle

- 5.1.2. Plug-in Hybrid Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Global APAC Wireless Charging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Battery Electric Vehicle

- 6.1.2. Plug-in Hybrid Vehicle

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. North America APAC Wireless Charging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.1.1. Battery Electric Vehicle

- 7.1.2. Plug-in Hybrid Vehicle

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8. South America APAC Wireless Charging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.1.1. Battery Electric Vehicle

- 8.1.2. Plug-in Hybrid Vehicle

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9. Europe APAC Wireless Charging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.1.1. Battery Electric Vehicle

- 9.1.2. Plug-in Hybrid Vehicle

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10. Middle East & Africa APAC Wireless Charging Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.1.1. Battery Electric Vehicle

- 10.1.2. Plug-in Hybrid Vehicle

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 11. Asia Pacific APAC Wireless Charging Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 11.1.1. Battery Electric Vehicle

- 11.1.2. Plug-in Hybrid Vehicle

- 11.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Tesla Motors

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Daimler AG

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 OLEV Technologies

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 BMW AG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Plugless

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Bombardier

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Toyota Motor Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Nissan

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Hella Aglaia

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 HEVO Powe

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 WiTricity

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Qualcomm

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Tesla Motors

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global APAC Wireless Charging Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America APAC Wireless Charging Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 3: North America APAC Wireless Charging Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 4: North America APAC Wireless Charging Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: North America APAC Wireless Charging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: South America APAC Wireless Charging Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 7: South America APAC Wireless Charging Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 8: South America APAC Wireless Charging Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: South America APAC Wireless Charging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe APAC Wireless Charging Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 11: Europe APAC Wireless Charging Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 12: Europe APAC Wireless Charging Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe APAC Wireless Charging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Middle East & Africa APAC Wireless Charging Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 15: Middle East & Africa APAC Wireless Charging Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 16: Middle East & Africa APAC Wireless Charging Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Middle East & Africa APAC Wireless Charging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific APAC Wireless Charging Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 19: Asia Pacific APAC Wireless Charging Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 20: Asia Pacific APAC Wireless Charging Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Asia Pacific APAC Wireless Charging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global APAC Wireless Charging Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 2: Global APAC Wireless Charging Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global APAC Wireless Charging Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 4: Global APAC Wireless Charging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United States APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Canada APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Mexico APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Global APAC Wireless Charging Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 9: Global APAC Wireless Charging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Brazil APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Argentina APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Rest of South America APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Global APAC Wireless Charging Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 14: Global APAC Wireless Charging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United Kingdom APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Germany APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: France APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Italy APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Spain APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Russia APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Benelux APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Nordics APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Rest of Europe APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Global APAC Wireless Charging Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 25: Global APAC Wireless Charging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Turkey APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Israel APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: GCC APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: North Africa APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: South Africa APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Middle East & Africa APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global APAC Wireless Charging Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 33: Global APAC Wireless Charging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 34: China APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: India APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Japan APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: South Korea APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: ASEAN APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Oceania APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Rest of Asia Pacific APAC Wireless Charging Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the APAC Wireless Charging Industry?

The projected CAGR is approximately 36.2%.

2. Which companies are prominent players in the APAC Wireless Charging Industry?

Key companies in the market include Tesla Motors, Daimler AG, OLEV Technologies, BMW AG, Plugless, Bombardier, Toyota Motor Corporation, Nissan, Hella Aglaia, HEVO Powe, WiTricity, Qualcomm.

3. What are the main segments of the APAC Wireless Charging Industry?

The market segments include Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 24.4 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Sales of Electric Vehicles Aiding Market Growth.

6. What are the notable trends driving market growth?

Increasing Sales of Electric Vehicles Driving the Wireless Charging Demand.

7. Are there any restraints impacting market growth?

High Cost of Installing Wireless Chargers.

8. Can you provide examples of recent developments in the market?

June 2023: ST Microelectronics NV unveiled an array of cutting-edge products and solutions for the smart mobility sector during the MWC Shanghai event. Among the highlights was the debut of the ST P-BOX Solution, a groundbreaking technology set to revolutionize autonomous driving. Additionally, the company showcased its 100W Wireless Charging Solution, built upon the STWBC2-HP and STWLC99 platforms.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "APAC Wireless Charging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the APAC Wireless Charging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the APAC Wireless Charging Industry?

To stay informed about further developments, trends, and reports in the APAC Wireless Charging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence