Key Insights

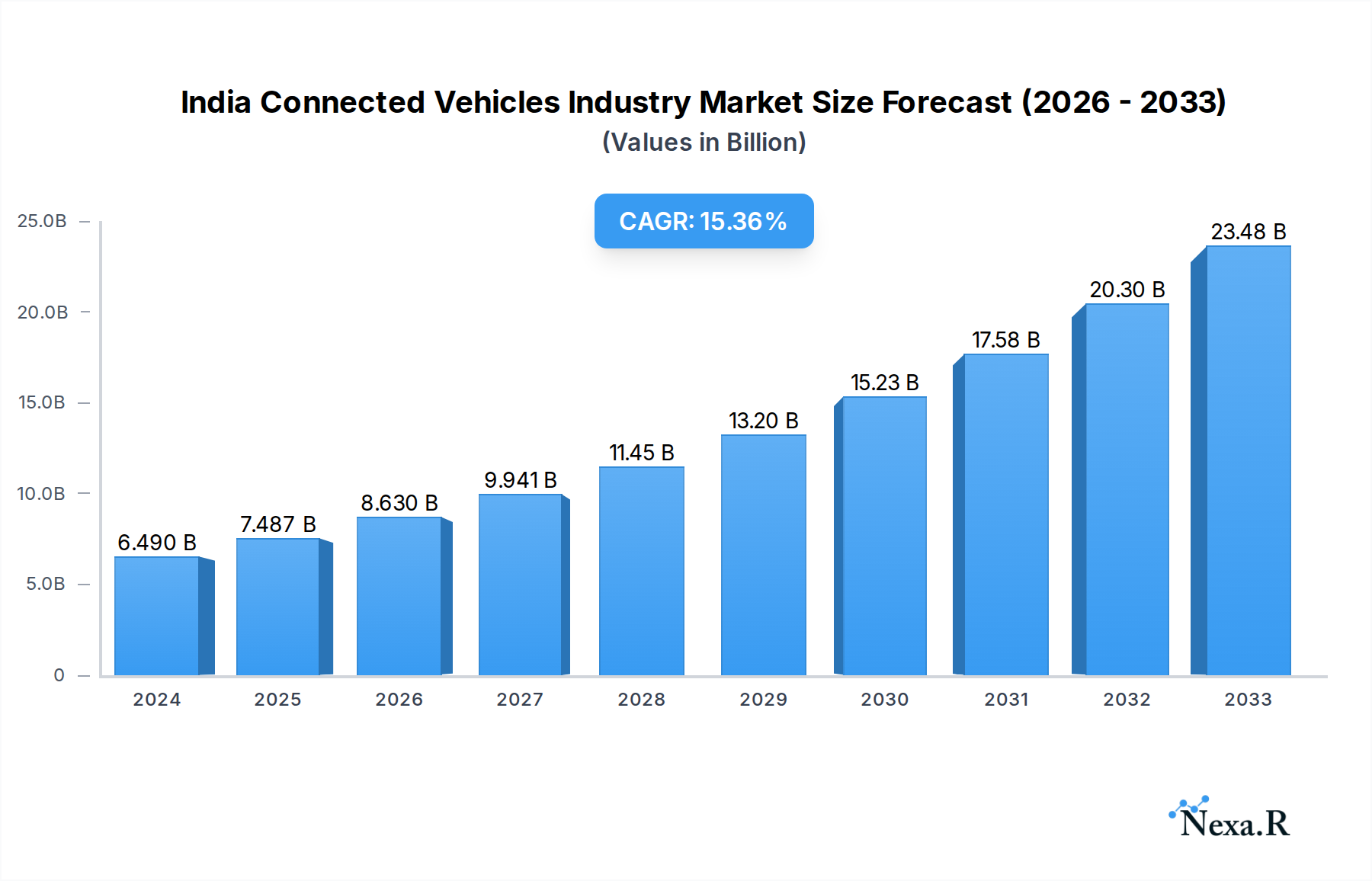

The Indian Connected Vehicles Industry is poised for remarkable expansion, with an estimated market size of USD 6.49 billion in 2024. This growth is fueled by a robust CAGR of 15.4%, indicating a dynamic and rapidly evolving market. The surge in demand for advanced safety features, enhanced driver experiences, and efficient fleet management is propelling the adoption of connected technologies across passenger cars and commercial vehicles. Key drivers include government initiatives promoting smart mobility, increasing consumer awareness and demand for in-car infotainment and telematics services, and the decreasing cost of advanced automotive electronics. The integration of features like real-time navigation, predictive maintenance, and remote diagnostics is becoming a standard expectation for Indian consumers, further accelerating market penetration.

India Connected Vehicles Industry Market Size (In Billion)

The market's trajectory is further shaped by emerging trends such as the increasing prevalence of Vehicle-to-Vehicle (V2V), Vehicle-to-Infrastructure (V2I), and Vehicle-to-Pedestrian (V2P) communication technologies, promising a more integrated and safer transportation ecosystem. While significant opportunities exist, potential restraints like cybersecurity concerns, the need for robust data infrastructure, and the affordability of premium connected features for a wider consumer base need to be strategically addressed by industry players. The diverse application types, spanning driver assistance, telematics, and infotainment, alongside various connectivity types like integrated, embedded, and tethered solutions, highlight the multifaceted nature of the Indian connected vehicle landscape. Leading automotive manufacturers such as Maruti Suzuki India Limited, Hyundai Motor Company, and Toyota Motor Corporation are actively investing in developing and deploying these advanced solutions, solidifying India's position as a key growth market in the global connected automotive sector.

India Connected Vehicles Industry Company Market Share

This comprehensive report provides an in-depth analysis of the burgeoning India Connected Vehicles Industry, a dynamic sector poised for significant expansion. Spanning from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, this study delves into market dynamics, growth trends, regional dominance, product landscape, key drivers, barriers, challenges, emerging opportunities, and growth accelerators. Our analysis meticulously examines parent and child markets, offering unparalleled insights for industry stakeholders, including manufacturers, technology providers, policymakers, and investors. The report leverages critical data from the historical period of 2019–2024 to project future trajectories, with the estimated year 2025 serving as a pivotal benchmark.

Keywords: India Connected Vehicles, Connected Car Market India, Automotive Connectivity India, V2X India, Telematics India, Infotainment India, Driver Assistance Systems India, Embedded Connectivity India, Integrated Connectivity India, Tethered Connectivity India, Vehicle-to-Vehicle (V2V) India, Vehicle-to-Infrastructure (V2I) India, Vehicle-to-Pedestrian (V2P) India, Passenger Cars Connectivity India, Commercial Vehicle Connectivity India, Automotive Technology India, Smart Mobility India, IoT in Automotive India, Automotive Software India, India Automotive Industry, Digital Automotive India.

India Connected Vehicles Industry Market Dynamics & Structure

The India Connected Vehicles Industry is characterized by a moderately concentrated market, driven by rapid technological innovation and an evolving regulatory landscape aimed at enhancing road safety and vehicle efficiency. Key drivers include the increasing adoption of advanced driver-assistance systems (ADAS), sophisticated telematics solutions for fleet management and remote diagnostics, and immersive infotainment systems catering to a tech-savvy consumer base. Competitive product substitutes are emerging, with traditional automotive components being augmented or replaced by integrated software and hardware solutions. End-user demographics are shifting towards a younger, urban population with higher disposable incomes, demanding seamless connectivity and personalized in-car experiences. Mergers and acquisitions (M&A) are becoming strategic tools for companies to gain market share, acquire technological capabilities, and expand their service offerings.

- Market Concentration: Moderate, with a few dominant players and a growing number of specialized technology providers.

- Technological Innovation Drivers: Advancements in AI, 5G connectivity, cloud computing, and sensor technology are fueling product development.

- Regulatory Frameworks: Government initiatives promoting vehicle safety, emissions control, and digital infrastructure development are influencing market growth.

- Competitive Product Substitutes: Over-the-air (OTA) updates, advanced cybersecurity solutions, and integrated digital ecosystems are becoming key differentiators.

- End-User Demographics: Growing demand from urban millennials and Gen Z consumers for smart, connected, and personalized mobility solutions.

- M&A Trends: Strategic acquisitions focused on acquiring AI capabilities, software development expertise, and expanding service portfolios. For instance, the acquisition of AI startups by major automakers to integrate autonomous driving features.

- Innovation Barriers: High development costs, complex integration challenges, data privacy concerns, and the need for robust cybersecurity infrastructure.

- Market Share (Estimated 2025): Leading players are expected to hold approximately 65-70% of the market, with the remainder fragmented among smaller, specialized firms.

- M&A Deal Volume (Projected 2025-2030): Expected to see an increase of 15-20% annually, driven by consolidation and expansion strategies.

India Connected Vehicles Industry Growth Trends & Insights

The India Connected Vehicles Industry is experiencing an unprecedented growth trajectory, propelled by a confluence of factors including increasing vehicle ownership, a burgeoning middle class with a desire for advanced automotive features, and supportive government policies promoting digitalization and smart mobility. The market size evolution is marked by a consistent upward trend, driven by higher adoption rates of connected features across various vehicle segments. Technological disruptions, such as the rollout of 5G networks and advancements in AI and IoT, are fundamentally reshaping the in-car experience, moving beyond basic connectivity to intelligent and predictive services. Consumer behavior shifts are evident, with buyers increasingly prioritizing advanced safety features, seamless entertainment options, and remote vehicle management capabilities. This report details the projected market size evolution, expected to reach $XX billion units by 2033, with a Compound Annual Growth Rate (CAGR) of approximately XX% during the forecast period (2025–2033). Market penetration of connected features in new vehicle sales is anticipated to surpass XX% by 2033, indicating a significant shift in consumer preferences and manufacturing strategies. The historical period (2019–2024) laid the groundwork, witnessing initial adoption and technological experimentation, paving the way for accelerated growth in the subsequent years. The estimated year 2025 marks a critical inflection point where advanced features become more mainstream.

The proliferation of telematics for fleet management, usage-based insurance, and real-time vehicle diagnostics is a significant growth driver, particularly within the commercial vehicle segment. Furthermore, the demand for sophisticated infotainment systems, offering personalized content, navigation, and communication services, is rising exponentially among passenger car owners. Driver assistance systems, ranging from basic parking aids to advanced adaptive cruise control and lane-keeping assist, are becoming standard offerings, enhancing safety and driving comfort. The integration of Vehicle-to-Everything (V2X) communication is in its nascent stages but holds immense potential for future growth, promising enhanced road safety, optimized traffic flow, and the foundation for autonomous driving. The evolving landscape of automotive software, with a focus on over-the-air (OTA) updates for feature enhancements and bug fixes, is also a key catalyst, reducing the need for physical servicing and improving customer satisfaction. The report quantifies these trends by analyzing the penetration of different connectivity types (Integrated, Embedded, Tethered) and application types across various vehicle segments, providing granular insights into market segmentation and growth potential. The XX billion units market size in 2025 is projected to witness robust expansion driven by these convergent forces.

Dominant Regions, Countries, or Segments in India Connected Vehicles Industry

Within the India Connected Vehicles Industry, passenger cars stand out as the dominant vehicle type driving market growth. This segment's dominance is fueled by a burgeoning middle class, rising disposable incomes, and a strong aspirational desire for technologically advanced and feature-rich vehicles. The increasing preference for comfort, safety, and entertainment features in personal transportation directly translates into higher demand for connected car technologies.

Infotainment emerges as the leading application type, capturing significant market share. Consumers are increasingly valuing seamless integration of navigation, music streaming, communication, and personalized digital experiences within their vehicles. This demand is further amplified by the availability of affordable data plans and the growing familiarity with smartphone-like interfaces.

In terms of connectivity types, integrated solutions are gaining substantial traction. This refers to systems that are built directly into the vehicle's architecture, offering a more seamless and robust user experience compared to aftermarket solutions. The trend is driven by automakers focusing on delivering cohesive and premium connected car ecosystems.

Among the Vehicle Connectivity segments, Vehicle-to-Infrastructure (V2I), while still in its early stages, is projected to witness substantial growth. As smart city initiatives gain momentum and governments invest in intelligent transportation systems, V2I communication will play a crucial role in optimizing traffic flow, enhancing road safety through real-time traffic information, and enabling smart parking solutions. This segment's growth is intricately linked with infrastructure development and supportive government policies.

Dominant Vehicle Type: Passenger Cars:

- Market Share (Estimated 2025): Expected to account for over XX% of the connected vehicles market.

- Growth Drivers: Rising disposable incomes, increasing urbanization, and a strong preference for advanced safety and convenience features.

- Key Manufacturers Investing: Maruti Suzuki India Limited, Hyundai Motor Company, Kia Motors Corporation, Toyota Motor Corporation.

Leading Application Type: Infotainment:

- Market Share (Estimated 2025): Projected to hold approximately XX% of the application market.

- Growth Drivers: Demand for personalized entertainment, advanced navigation, seamless smartphone integration, and over-the-air (OTA) content updates.

- Technological Advancements: AI-powered voice assistants, augmented reality navigation, and personalized user interfaces.

Dominant Connectivity Type: Integrated:

- Market Share (Estimated 2025): Expected to represent over XX% of the connectivity market.

- Growth Drivers: Automaker focus on providing premium, user-friendly, and secure connected experiences; higher reliability and seamless integration.

- Impact on User Experience: Enhanced performance, reduced latency, and better overall system stability.

Emerging Vehicle Connectivity Segment: Vehicle-to-Infrastructure (V2I):

- Growth Potential: Significant, driven by smart city initiatives and government investment in intelligent transportation systems.

- Key Applications: Real-time traffic management, intelligent traffic signals, smart parking, and emergency vehicle prioritization.

- Infrastructure Dependence: Growth is closely tied to the development of smart road infrastructure and widespread deployment of roadside units (RSUs).

Regional Dominance: The Western and Northern regions of India, characterized by higher economic development, greater vehicle penetration, and a concentration of automotive manufacturing hubs, are expected to lead the market. These regions benefit from supportive state policies, greater access to advanced technology, and a larger consumer base with the propensity to adopt connected vehicle technologies.

India Connected Vehicles Industry Product Landscape

The product landscape in the India Connected Vehicles Industry is rapidly evolving, marked by innovations in telematics, advanced driver-assistance systems (ADAS), and sophisticated infotainment units. Companies are focusing on developing AI-powered features that enhance driver safety and comfort, such as predictive maintenance alerts and personalized driving profiles. The integration of 5G technology is enabling faster data transmission for real-time traffic updates and enhanced in-car entertainment options. Over-the-air (OTA) updates are becoming a standard for software improvements and feature enhancements, ensuring vehicles remain contemporary. Key players are differentiating through intuitive user interfaces, robust cybersecurity measures, and the seamless integration of third-party applications. For instance, the introduction of AI-driven virtual assistants that understand local dialects and user preferences is a significant technological advancement, offering a unique selling proposition.

Key Drivers, Barriers & Challenges in India Connected Vehicles Industry

The India Connected Vehicles Industry is propelled by several key drivers, including the government's push for digitalization and smart cities, the increasing demand for enhanced safety features, and the growing consumer preference for advanced in-car technology. The rising penetration of smartphones and affordable data plans further facilitates the adoption of connected services. Technological advancements in AI, 5G, and IoT are enabling more sophisticated and personalized connected experiences.

However, significant barriers and challenges exist. High manufacturing costs associated with advanced hardware and software integration can impact affordability. Cybersecurity threats and data privacy concerns remain critical hurdles, requiring robust security protocols and transparent data handling practices. Regulatory uncertainties regarding data ownership and usage can also pose challenges. Furthermore, the need for widespread development of supporting infrastructure, such as high-speed cellular networks and V2I communication systems, is crucial for widespread adoption. Supply chain disruptions can impact the availability of essential components.

Emerging Opportunities in India Connected Vehicles Industry

Emerging opportunities in the India Connected Vehicles Industry lie in the development of advanced V2X communication capabilities to enhance road safety and traffic efficiency, particularly with the ongoing smart city initiatives. The untapped potential in the commercial vehicle segment for fleet management and logistics optimization presents a significant avenue for growth. Furthermore, the demand for personalized and AI-driven in-car experiences, including predictive maintenance and customized infotainment, offers substantial opportunities for service innovation. The growing trend of Mobility-as-a-Service (MaaS) is also creating new avenues for connected vehicle solutions in ride-sharing and on-demand transportation.

Growth Accelerators in the India Connected Vehicles Industry Industry

Several catalysts are accelerating the growth of the India Connected Vehicles Industry. Technological breakthroughs in artificial intelligence and machine learning are enabling more intelligent and predictive vehicle functionalities. Strategic partnerships between automotive manufacturers, technology providers, and telecommunication companies are crucial for developing integrated ecosystems and expanding service offerings. Market expansion strategies, including the introduction of affordable connected car variants and the development of localized content and services, are broadening consumer reach. The increasing investment in developing robust digital infrastructure across the country is also a significant growth accelerator, paving the way for advanced connectivity features.

Key Players Shaping the India Connected Vehicles Industry Market

- MG Motor UK Limited

- Hyundai Motor Company

- Kia Motors Corporation

- Toyota Motor Corporation

- Nissan Motor Company

- Maruti Suzuki India Limited

Notable Milestones in India Connected Vehicles Industry Sector

- 2019: Launch of first connected car features in mass-market passenger vehicles by key manufacturers, including integrated telematics and infotainment systems.

- 2020: Increased focus on Over-The-Air (OTA) update capabilities by OEMs to deliver software enhancements and bug fixes remotely.

- 2021: Introduction of advanced driver-assistance systems (ADAS) as optional or standard features in premium and mid-segment vehicles.

- 2022: Significant investments by automotive and technology companies in developing 5G-enabled connected car solutions.

- 2023: Growing adoption of AI-powered voice assistants and personalized in-car digital experiences.

- 2024: Expansion of telematics services for commercial vehicle fleet management and enhanced safety monitoring.

In-Depth India Connected Vehicles Industry Market Outlook

The future outlook for the India Connected Vehicles Industry is exceptionally bright, driven by sustained technological innovation and increasing consumer demand. Growth accelerators include the widespread adoption of 5G, enabling seamless V2X communication and advanced infotainment, and the continuous evolution of AI for predictive maintenance and personalized user experiences. Strategic partnerships between automakers and tech giants will foster integrated ecosystems, while market expansion strategies will focus on making connected features accessible across a wider range of vehicle segments. The increasing emphasis on smart mobility and sustainable transportation will further fuel the development and integration of advanced connected solutions, positioning India as a significant player in the global connected vehicles market.

India Connected Vehicles Industry Segmentation

-

1. Application Type

- 1.1. Driver Assistance

- 1.2. Telematics

- 1.3. Infotainment

- 1.4. Other Application Types

-

2. Connectivity Type

- 2.1. Integrated

- 2.2. Embedded

- 2.3. Tethered

-

3. Vehicle Connectivity

- 3.1. Vehicle-to-Vehicle (V2V)

- 3.2. Vehicle-to-Infrastructure (V2I)

- 3.3. Vehicle-to-Pedestrain (V2P)

-

4. Vehicle Type

- 4.1. Passenger Cars

- 4.2. Commercial Vehicle

India Connected Vehicles Industry Segmentation By Geography

- 1. India

India Connected Vehicles Industry Regional Market Share

Geographic Coverage of India Connected Vehicles Industry

India Connected Vehicles Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application Type

- 5.1.1. Driver Assistance

- 5.1.2. Telematics

- 5.1.3. Infotainment

- 5.1.4. Other Application Types

- 5.2. Market Analysis, Insights and Forecast - by Connectivity Type

- 5.2.1. Integrated

- 5.2.2. Embedded

- 5.2.3. Tethered

- 5.3. Market Analysis, Insights and Forecast - by Vehicle Connectivity

- 5.3.1. Vehicle-to-Vehicle (V2V)

- 5.3.2. Vehicle-to-Infrastructure (V2I)

- 5.3.3. Vehicle-to-Pedestrain (V2P)

- 5.4. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.4.1. Passenger Cars

- 5.4.2. Commercial Vehicle

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. India

- 5.1. Market Analysis, Insights and Forecast - by Application Type

- 6. India Connected Vehicles Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application Type

- 6.1.1. Driver Assistance

- 6.1.2. Telematics

- 6.1.3. Infotainment

- 6.1.4. Other Application Types

- 6.2. Market Analysis, Insights and Forecast - by Connectivity Type

- 6.2.1. Integrated

- 6.2.2. Embedded

- 6.2.3. Tethered

- 6.3. Market Analysis, Insights and Forecast - by Vehicle Connectivity

- 6.3.1. Vehicle-to-Vehicle (V2V)

- 6.3.2. Vehicle-to-Infrastructure (V2I)

- 6.3.3. Vehicle-to-Pedestrain (V2P)

- 6.4. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.4.1. Passenger Cars

- 6.4.2. Commercial Vehicle

- 6.1. Market Analysis, Insights and Forecast - by Application Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 MG Motor UK Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Hyundai Motor Company

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Kia Motors Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Toyota Motor Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Nissan Motor Company*List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Maruti Suzuki India Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.1 MG Motor UK Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Connected Vehicles Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: India Connected Vehicles Industry Share (%) by Company 2025

List of Tables

- Table 1: India Connected Vehicles Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 2: India Connected Vehicles Industry Revenue billion Forecast, by Connectivity Type 2020 & 2033

- Table 3: India Connected Vehicles Industry Revenue billion Forecast, by Vehicle Connectivity 2020 & 2033

- Table 4: India Connected Vehicles Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 5: India Connected Vehicles Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: India Connected Vehicles Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 7: India Connected Vehicles Industry Revenue billion Forecast, by Connectivity Type 2020 & 2033

- Table 8: India Connected Vehicles Industry Revenue billion Forecast, by Vehicle Connectivity 2020 & 2033

- Table 9: India Connected Vehicles Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 10: India Connected Vehicles Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Connected Vehicles Industry?

The projected CAGR is approximately 15.4%.

2. Which companies are prominent players in the India Connected Vehicles Industry?

Key companies in the market include MG Motor UK Limited, Hyundai Motor Company, Kia Motors Corporation, Toyota Motor Corporation, Nissan Motor Company*List Not Exhaustive, Maruti Suzuki India Limited.

3. What are the main segments of the India Connected Vehicles Industry?

The market segments include Application Type, Connectivity Type, Vehicle Connectivity, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.49 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing disposable income and Low-interest rates from lenders increase the market demand.

6. What are the notable trends driving market growth?

EVs will Boost the Market's Growth.

7. Are there any restraints impacting market growth?

High initial costs may obstruct the growth.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Connected Vehicles Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Connected Vehicles Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Connected Vehicles Industry?

To stay informed about further developments, trends, and reports in the India Connected Vehicles Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence