Key Insights

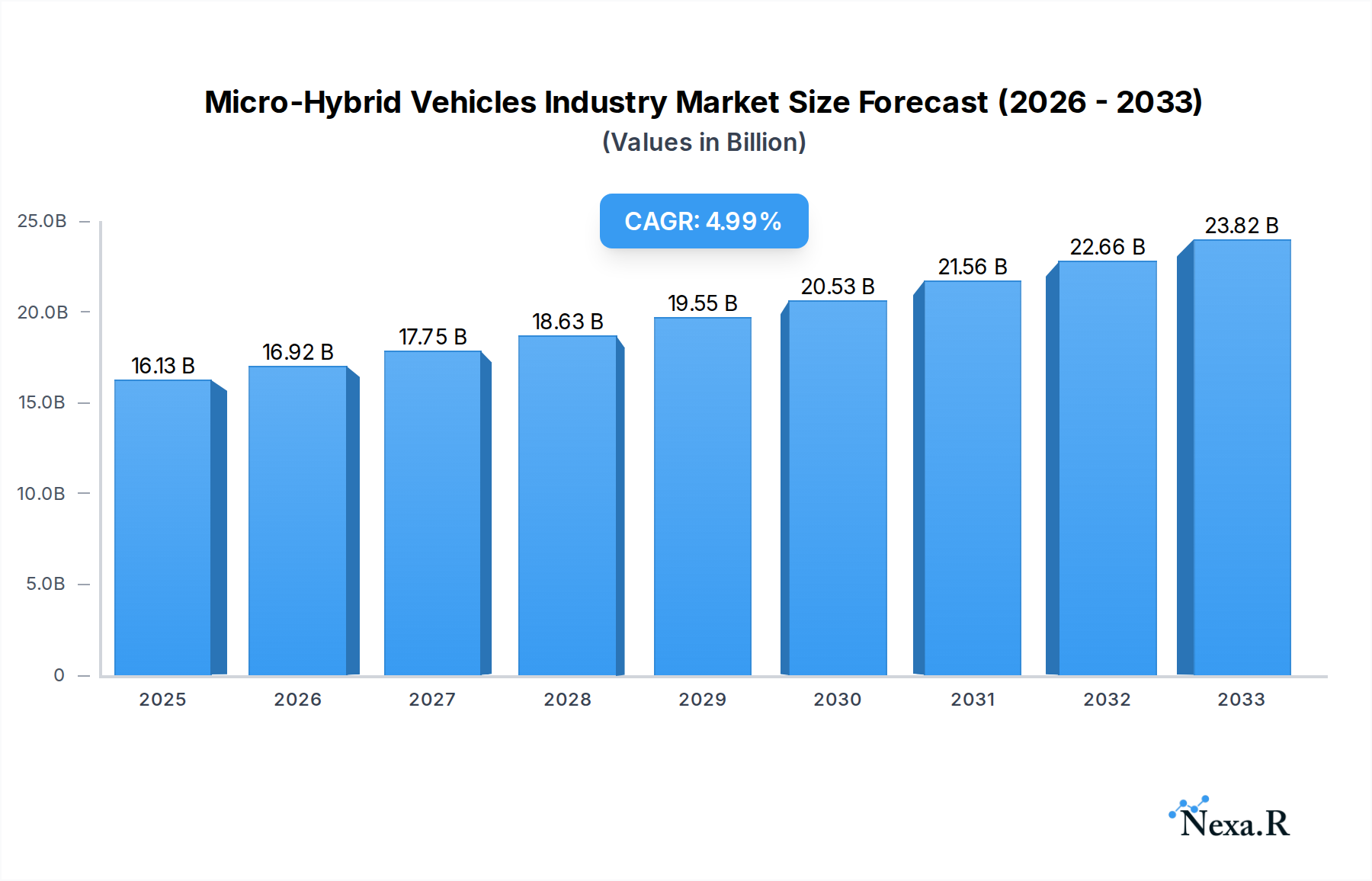

The global Micro-Hybrid Vehicles Industry is poised for substantial growth, projected to reach an impressive $16.13 billion by 2025, with an estimated Compound Annual Growth Rate (CAGR) of 4.8% extending through 2033. This robust expansion is fueled by a confluence of factors, primarily driven by increasing consumer demand for fuel-efficient vehicles, stringent government regulations aimed at reducing emissions, and the escalating adoption of advanced powertrain technologies. The industry is witnessing a significant shift towards electrification, with micro-hybrid systems serving as a crucial stepping stone towards full hybridization and electrification. Key drivers include the growing awareness of climate change, government incentives for eco-friendly vehicles, and the cost-effectiveness of micro-hybrid technology compared to more complex hybrid or electric systems. The market is segmented by capacity, with both 12V and 48V micro-hybrid systems gaining traction, catering to diverse vehicle types including passenger cars and commercial vehicles. Furthermore, advancements in battery technology, particularly the increasing adoption of Lithium-Ion batteries, are enhancing the performance and range of micro-hybrid systems.

Micro-Hybrid Vehicles Industry Market Size (In Billion)

The competitive landscape of the Micro-Hybrid Vehicles Industry is characterized by the presence of major automotive manufacturers, including General Motors, Mahindra and Mahindra, Daimler AG, Kia Motors Corporation, BMW AG, Hyundai Motors Company, Audi AG, Nissan Motors Company, Subaru, and Toyota Motors Company. These companies are heavily investing in research and development to enhance micro-hybrid functionalities, optimize energy recovery systems, and integrate these technologies seamlessly into their vehicle lineups. Emerging trends such as the development of more sophisticated regenerative braking systems, advanced start-stop technologies, and the integration of mild-hybrid powertrains are further shaping the market. While the market is experiencing strong growth, it faces certain restraints, including the initial cost of implementation for some advanced micro-hybrid systems, consumer perception regarding the benefits of mild-hybrid technology, and the ongoing evolution of fully electric vehicle technology, which may present long-term competition. Nevertheless, the compelling combination of fuel efficiency, reduced emissions, and a more accessible entry point into electrified mobility ensures a promising future for the micro-hybrid vehicle market.

Micro-Hybrid Vehicles Industry Company Market Share

Micro-Hybrid Vehicles Industry: Comprehensive Market Analysis & Forecast (2019–2033)

Unlock unparalleled insights into the rapidly evolving Micro-Hybrid Vehicles industry with this definitive market research report. Spanning the historical period of 2019–2024 and projecting growth through 2033, this analysis leverages a robust framework to dissect market dynamics, identify growth drivers, and forecast future trends. With a base year of 2025, the report provides a granular view of the global market, essential for strategists, investors, and industry professionals navigating the transition to more efficient automotive technologies. Dive deep into parent and child markets, covering crucial segments like 12V and 48V Micro Hybrid systems, and diverse vehicle types including commercial vehicles and passenger cars. Explore the impact of battery technologies, from advanced Lithium-Ion to reliable Lead Acid, and gain a competitive edge by understanding the strategies of key players such as General Motors, Mahindra and Mahindra, Daimler AG, Kia Motors Corporation, BMW AG, Hyundai Motors Company, Audi AG, Nissan Motors Company, Subaru, and Toyota Motors Company.

Micro-Hybrid Vehicles Industry Market Dynamics & Structure

The Micro-Hybrid Vehicles industry is characterized by a dynamic and evolving market structure, driven by increasing environmental regulations and a growing consumer demand for fuel-efficient and lower-emission vehicles. Market concentration varies across regions, with established automotive giants and emerging players actively vying for market share through continuous technological innovation. The primary drivers of innovation include the relentless pursuit of enhanced fuel economy, the reduction of CO2 emissions to meet stringent global standards (e.g., Euro 7, CAFE), and the development of more sophisticated start-stop systems and mild-hybrid powertrains. Regulatory frameworks, particularly those focused on emissions reduction and the promotion of electrified mobility, play a pivotal role in shaping market entry and product development strategies. Competitive product substitutes, such as fully electric vehicles (EVs) and advanced internal combustion engine (ICE) vehicles, pose a constant challenge, necessitating micro-hybrid manufacturers to continually improve performance and cost-effectiveness. End-user demographics are shifting towards environmentally conscious consumers and fleet operators seeking operational cost savings. Mergers and acquisitions (M&A) are becoming increasingly prevalent as companies aim to consolidate technological expertise, expand product portfolios, and gain a competitive advantage in this burgeoning market. For instance, strategic acquisitions of battery technology firms and powertrain component suppliers are common, reflecting the industry's focus on vertical integration and securing critical supply chains. The volume of M&A deals in the automotive sector, often involving electrification technologies, has seen a notable increase, indicating a strong consolidation trend. Barriers to innovation include the high cost of research and development, the need for standardized charging and energy management systems, and the long lead times associated with vehicle development and homologation.

- Market Concentration: Moderate to high, with key global automakers holding significant influence.

- Technological Innovation Drivers: Stringent emissions regulations (e.g., CO2 targets), rising fuel prices, consumer preference for fuel efficiency, advancement in battery and electrical component technologies.

- Regulatory Frameworks: Mandated emissions standards, government incentives for hybrid and low-emission vehicles, safety regulations for electrified powertrains.

- Competitive Product Substitutes: Fully electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), advanced internal combustion engine (ICE) vehicles.

- End-User Demographics: Environmentally aware consumers, fleet managers focused on TCO (Total Cost of Ownership), urban commuters seeking reduced running costs.

- M&A Trends: Acquisition of technology startups, strategic partnerships for component development, consolidation of powertrain expertise.

Micro-Hybrid Vehicles Industry Growth Trends & Insights

The Micro-Hybrid Vehicles industry is poised for significant expansion, driven by a confluence of technological advancements, favorable regulatory environments, and evolving consumer preferences for sustainable transportation. The market size is projected to witness a substantial Compound Annual Growth Rate (CAGR) over the forecast period, reflecting an increasing adoption rate of mild-hybrid technology as a practical and cost-effective step towards vehicle electrification. The estimated market size for micro-hybrid vehicles is projected to reach approximately $45.80 billion units by 2025, with a projected CAGR of 14.50% during the 2025-2033 forecast period, reaching an estimated $129.70 billion units by 2033. This growth trajectory is underpinned by technological disruptions, such as the continuous improvement in the performance and cost-effectiveness of 12V and 48V electrical systems, as well as advancements in battery technologies like Lithium-ion and enhanced Lead-Acid batteries that offer higher energy density and longer lifespans. Consumer behavior is shifting towards a greater appreciation for the fuel-saving benefits and reduced environmental impact offered by micro-hybrid systems, especially in urban driving conditions where frequent stop-start cycles can maximize energy recuperation. The market penetration of micro-hybrid vehicles is steadily increasing, often integrated as standard features in mainstream passenger cars and light commercial vehicles, making them accessible to a wider consumer base. This trend is further amplified by the automotive industry’s strategic focus on offering a diverse range of powertrain options that bridge the gap between traditional ICE vehicles and fully electric alternatives. The introduction of more efficient starter-generators and advanced power management systems allows for greater energy recovery during braking and deceleration, which is then used to power auxiliary systems or provide a torque assist during acceleration, thereby reducing fuel consumption and emissions without the complexity and cost of full hybrid systems. The demand for higher-performance lead-acid batteries is notably increasing, as demonstrated by industry developments like Birla Carbon's entry into the energy systems market, driven by the need to meet stringent CO2 emission requirements, particularly for start-stop or micro-hybrid vehicles. Furthermore, the expansion of hybrid lineups by major manufacturers, such as Renault’s introduction of 12V micro-hybridization solutions on petrol engines, signifies a broad industry commitment to this technology. The market is also benefiting from the increasing electrification of commercial vehicle fleets, where fuel efficiency and reduced operational costs are paramount.

Dominant Regions, Countries, or Segments in Micro-Hybrid Vehicles Industry

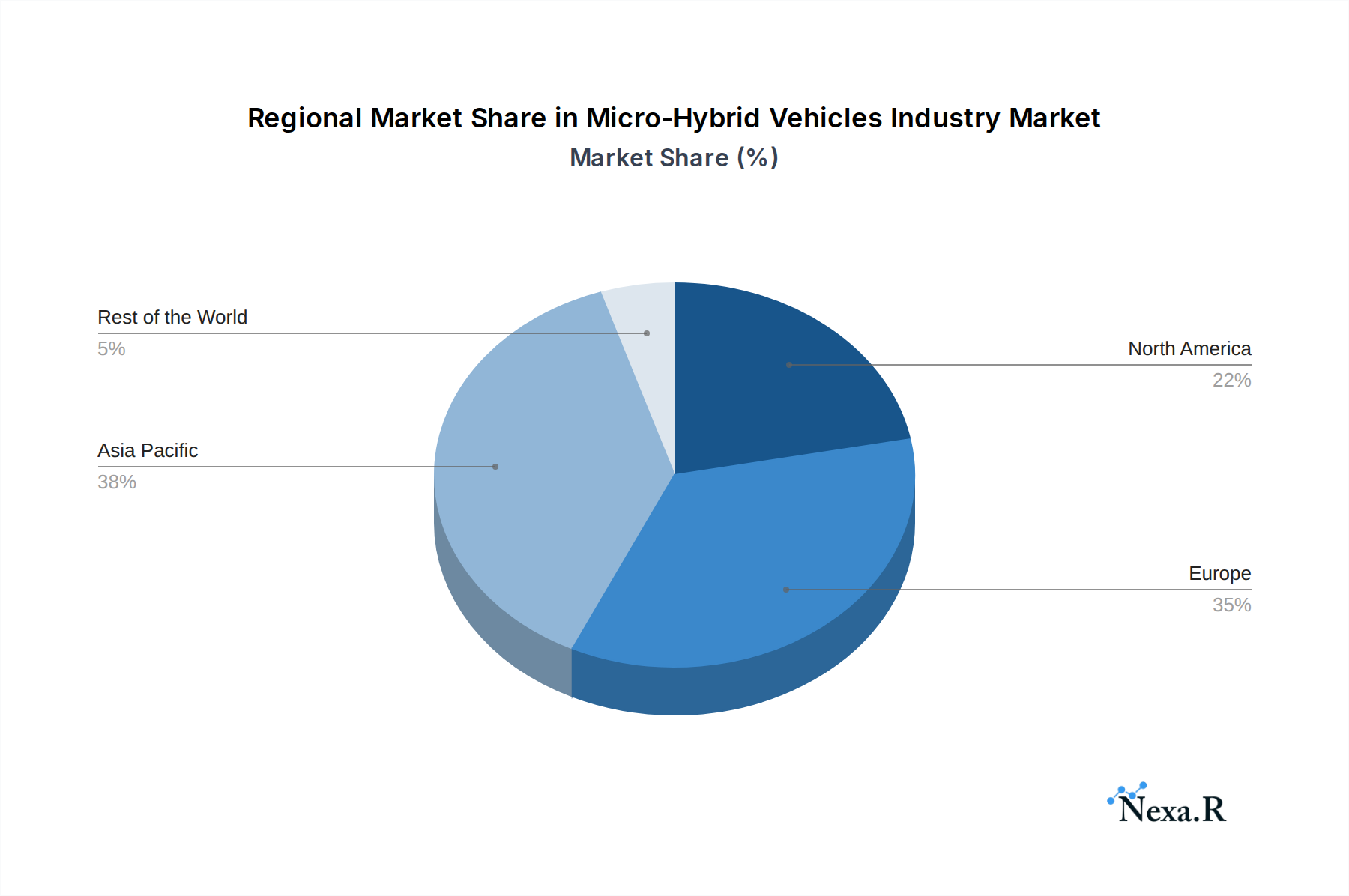

The global Micro-Hybrid Vehicles industry is experiencing robust growth across various regions and segments, with several key players driving market expansion. Among the dominant segments, Passenger Cars hold a significant market share due to widespread consumer demand for fuel-efficient and eco-friendly personal transportation. The increasing adoption of micro-hybrid technology in mainstream passenger vehicles, driven by stringent emissions regulations and rising fuel costs, positions this segment for continued dominance. Within the Capacity segment, both 12V Micro Hybrid and 48V Micro Hybrid systems are crucial. While 12V systems are prevalent in more cost-sensitive applications and basic start-stop functionalities, the 48V architecture is gaining traction for its ability to support more advanced features, including enhanced regenerative braking and mild-hybrid powertrains offering greater fuel savings and performance improvements. The Battery Type segment sees a dynamic interplay between Lead Acid and Lithium Ion batteries. Lead-acid batteries continue to be a cost-effective solution for many micro-hybrid applications, particularly for start-stop functions, with ongoing advancements improving their performance and lifespan. However, Lithium-ion batteries are increasingly being adopted for their higher energy density, faster charging capabilities, and longer cycle life, especially in more sophisticated 48V systems and premium vehicle segments. Geographically, Europe has emerged as a dominant region in the micro-hybrid vehicle market. This is primarily attributed to the European Union's aggressive emissions standards, such as the CO2 fleet targets, which have compelled automakers to accelerate the adoption of electrified powertrains, including mild-hybrid systems. Countries like Germany, France, and the UK are leading the charge, supported by strong government incentives, a well-established automotive manufacturing base, and a highly environmentally conscious consumer base. The increasing focus on reducing urban air pollution and promoting sustainable mobility further fuels demand for micro-hybrid vehicles in this region. The market share of micro-hybrid vehicles in Europe is substantial and continues to grow, often integrated into a vast array of vehicle models. The growth potential in Europe is immense, driven by the ongoing transition towards stricter emission norms and the automakers’ strategic commitment to electrify their portfolios. Other regions, such as Asia-Pacific, are also witnessing significant growth, particularly in countries like China and South Korea, where government support for new energy vehicles and the rapid expansion of the automotive industry are creating fertile ground for micro-hybrid technology. North America is also seeing an uptick in adoption, albeit at a slightly slower pace compared to Europe, with automakers responding to evolving consumer preferences and increasing regulatory pressures. The dominance of these segments and regions is a testament to the industry's response to environmental imperatives and the practical advantages offered by micro-hybrid technology in balancing performance, cost, and sustainability.

Micro-Hybrid Vehicles Industry Product Landscape

The product landscape of the Micro-Hybrid Vehicles industry is characterized by a focus on integrating advanced yet cost-effective electrical systems to enhance the efficiency of conventional internal combustion engines. Key product innovations revolve around lightweight and powerful starter-generators, advanced battery management systems, and optimized power distribution units that manage the flow of energy between the engine, battery, and auxiliary systems. These systems are designed to seamlessly enable functions like engine start-stop, regenerative braking for energy recapture, and mild torque assist. Performance metrics are typically measured by improvements in fuel economy, reductions in CO2 emissions, and enhanced drivability through smoother engine restarts and a more responsive throttle. The unique selling proposition of micro-hybrid vehicles lies in their ability to offer significant environmental and economic benefits over traditional ICE vehicles without the higher cost and infrastructure demands of full hybrids or battery-electric vehicles. Technological advancements are continuously pushing the boundaries, with a trend towards more efficient electrical components and smarter energy management algorithms to maximize the benefits of mild hybridization.

Key Drivers, Barriers & Challenges in Micro-Hybrid Vehicles Industry

The Micro-Hybrid Vehicles industry is propelled by several key drivers, primarily the stringent global emissions regulations that mandate significant reductions in CO2 output and fuel consumption. Automakers are increasingly adopting micro-hybrid technology as a cost-effective strategy to meet these targets. Consumer demand for improved fuel economy and lower running costs further fuels market growth, especially in regions with high fuel prices. Technological advancements in battery technology, particularly in lead-acid and lithium-ion chemistries, are making micro-hybrid systems more efficient and reliable.

However, the industry faces significant barriers and challenges. The primary challenge is competition from fully electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs), which offer greater electrification and zero-emission driving capabilities, albeit at a higher cost. Supply chain disruptions, particularly for critical components like semiconductors and battery materials, can impact production volumes and costs. Regulatory fragmentation across different countries and regions can create complexities for global automakers. Furthermore, consumer perception and education regarding the benefits of micro-hybrid technology compared to other electrified options remain a hurdle.

Emerging Opportunities in Micro-Hybrid Vehicles Industry

Emerging opportunities in the Micro-Hybrid Vehicles industry are centered around leveraging the technology as a transitional solution towards full electrification and capitalizing on its cost-effectiveness. A significant opportunity lies in expanding the application of micro-hybrid systems to a wider range of commercial vehicles, including light-duty trucks and vans, where fuel efficiency and reduced operational costs are critical for fleet operators. The development of more integrated and intelligent energy management systems that can further optimize fuel savings and reduce emissions presents another avenue for innovation. As battery technology continues to evolve, opportunities exist to enhance the performance and capabilities of 48V micro-hybrid systems, potentially offering a more compelling alternative to some entry-level full hybrid models. Furthermore, untapped markets in developing economies, where the adoption of more advanced vehicle technologies is gaining momentum, represent a substantial growth potential for cost-effective micro-hybrid solutions. Evolving consumer preferences towards sustainability, coupled with increasing pressure to reduce urban emissions, will continue to drive demand for these efficient vehicles.

Growth Accelerators in the Micro-Hybrid Vehicles Industry Industry

Several catalysts are accelerating the long-term growth of the Micro-Hybrid Vehicles industry. Foremost among these is the relentless pace of technological innovation, particularly in the development of more efficient and cost-effective electrical components, advanced battery chemistries, and sophisticated energy management software. Strategic partnerships between traditional automakers, component suppliers, and technology firms are crucial for co-developing and integrating these advanced systems seamlessly into vehicle platforms. Furthermore, the increasing commitment from major automotive manufacturers to electrify their entire vehicle lineups, with micro-hybrid technology serving as an accessible entry point, significantly broadens market reach. Government initiatives and regulatory mandates aimed at reducing fleet-wide emissions and promoting fuel efficiency continue to act as powerful growth accelerators, incentivizing both manufacturers and consumers. Market expansion strategies, including the introduction of more diverse vehicle models equipped with micro-hybrid technology across various segments, are also key to sustaining and amplifying growth.

Key Players Shaping the Micro-Hybrid Vehicles Industry Market

- General Motors

- Mahindra and Mahindra

- Daimler AG

- Kia Motors Corporation

- BMW AG

- Hyundai Motors Company

- Audi AG

- Nissan Motors Company

- Subaru

- Toyota Motors Company

Notable Milestones in Micro-Hybrid Vehicles Industry Sector

- September 2021: Birla Carbon announced its entry into the energy systems market by participating in The Battery Show 2021 in the United States, signaling growing interest in advanced battery solutions for vehicles. Demand for higher-performance lead acid batteries is increasing as automakers strive to meet more stringent CO2 emission requirements, particularly for start-stop or micro-hybrid vehicles.

- May 2021: Renault announced the Clio E-TECH Hybrid, Captur, and Megane Estate E-TECH Plug-in Hybrid, expanding its hybrid lineup. In addition to the full hybrid, the New Renault Arkana and New Captur introduced a 12V micro-hybridization solution on the 1.3 TCe 140 and 160 petrol engines, a first for Renault.

In-Depth Micro-Hybrid Vehicles Industry Market Outlook

The Micro-Hybrid Vehicles industry outlook is exceptionally promising, driven by its pivotal role in the automotive sector's gradual transition towards electrification. The market is expected to benefit from continued technological advancements that enhance the efficiency and cost-effectiveness of mild-hybrid systems, making them an increasingly attractive option for a wider range of vehicles. Growth accelerators, including stringent emission regulations and evolving consumer preferences for sustainable mobility, will ensure sustained demand. Strategic partnerships and the continuous expansion of micro-hybrid offerings by major automakers are poised to solidify its market position. Untapped markets in emerging economies and the potential for innovative applications in commercial fleets present significant future opportunities. The industry's ability to offer a tangible reduction in fuel consumption and emissions at a lower cost point than full hybrids or EVs positions it for robust and enduring growth in the coming years.

Micro-Hybrid Vehicles Industry Segmentation

-

1. Capacity

- 1.1. 12 V MicroHybrid

- 1.2. 48 V Micro Hybrid

-

2. Vehicle Type

- 2.1. Commercial Vehicle

- 2.2. Passenger Cars

-

3. Battery Type

- 3.1. Lithium Ion

- 3.2. Lead Acid

Micro-Hybrid Vehicles Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. India

- 3.2. China

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. Brazil

- 4.2. Mexico

- 4.3. South Africa

- 4.4. Other Countries

Micro-Hybrid Vehicles Industry Regional Market Share

Geographic Coverage of Micro-Hybrid Vehicles Industry

Micro-Hybrid Vehicles Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 5.1.1. 12 V MicroHybrid

- 5.1.2. 48 V Micro Hybrid

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Commercial Vehicle

- 5.2.2. Passenger Cars

- 5.3. Market Analysis, Insights and Forecast - by Battery Type

- 5.3.1. Lithium Ion

- 5.3.2. Lead Acid

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 6. Global Micro-Hybrid Vehicles Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 6.1.1. 12 V MicroHybrid

- 6.1.2. 48 V Micro Hybrid

- 6.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.2.1. Commercial Vehicle

- 6.2.2. Passenger Cars

- 6.3. Market Analysis, Insights and Forecast - by Battery Type

- 6.3.1. Lithium Ion

- 6.3.2. Lead Acid

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 7. North America Micro-Hybrid Vehicles Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 7.1.1. 12 V MicroHybrid

- 7.1.2. 48 V Micro Hybrid

- 7.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.2.1. Commercial Vehicle

- 7.2.2. Passenger Cars

- 7.3. Market Analysis, Insights and Forecast - by Battery Type

- 7.3.1. Lithium Ion

- 7.3.2. Lead Acid

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 8. Europe Micro-Hybrid Vehicles Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 8.1.1. 12 V MicroHybrid

- 8.1.2. 48 V Micro Hybrid

- 8.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.2.1. Commercial Vehicle

- 8.2.2. Passenger Cars

- 8.3. Market Analysis, Insights and Forecast - by Battery Type

- 8.3.1. Lithium Ion

- 8.3.2. Lead Acid

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 9. Asia Pacific Micro-Hybrid Vehicles Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 9.1.1. 12 V MicroHybrid

- 9.1.2. 48 V Micro Hybrid

- 9.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.2.1. Commercial Vehicle

- 9.2.2. Passenger Cars

- 9.3. Market Analysis, Insights and Forecast - by Battery Type

- 9.3.1. Lithium Ion

- 9.3.2. Lead Acid

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 10. Rest of the World Micro-Hybrid Vehicles Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Capacity

- 10.1.1. 12 V MicroHybrid

- 10.1.2. 48 V Micro Hybrid

- 10.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.2.1. Commercial Vehicle

- 10.2.2. Passenger Cars

- 10.3. Market Analysis, Insights and Forecast - by Battery Type

- 10.3.1. Lithium Ion

- 10.3.2. Lead Acid

- 10.1. Market Analysis, Insights and Forecast - by Capacity

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 General Motors

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Mahindra and Mahindra

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Daimler AG

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Kia Motors Corporatio

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 BMW AG

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Hyundai Motors Company

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Audi AG

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Nissan Motors Company

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Subaru

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Toyota Motors Company

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 General Motors

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Micro-Hybrid Vehicles Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Micro-Hybrid Vehicles Industry Revenue (billion), by Capacity 2025 & 2033

- Figure 3: North America Micro-Hybrid Vehicles Industry Revenue Share (%), by Capacity 2025 & 2033

- Figure 4: North America Micro-Hybrid Vehicles Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 5: North America Micro-Hybrid Vehicles Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 6: North America Micro-Hybrid Vehicles Industry Revenue (billion), by Battery Type 2025 & 2033

- Figure 7: North America Micro-Hybrid Vehicles Industry Revenue Share (%), by Battery Type 2025 & 2033

- Figure 8: North America Micro-Hybrid Vehicles Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Micro-Hybrid Vehicles Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Micro-Hybrid Vehicles Industry Revenue (billion), by Capacity 2025 & 2033

- Figure 11: Europe Micro-Hybrid Vehicles Industry Revenue Share (%), by Capacity 2025 & 2033

- Figure 12: Europe Micro-Hybrid Vehicles Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 13: Europe Micro-Hybrid Vehicles Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 14: Europe Micro-Hybrid Vehicles Industry Revenue (billion), by Battery Type 2025 & 2033

- Figure 15: Europe Micro-Hybrid Vehicles Industry Revenue Share (%), by Battery Type 2025 & 2033

- Figure 16: Europe Micro-Hybrid Vehicles Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Micro-Hybrid Vehicles Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Micro-Hybrid Vehicles Industry Revenue (billion), by Capacity 2025 & 2033

- Figure 19: Asia Pacific Micro-Hybrid Vehicles Industry Revenue Share (%), by Capacity 2025 & 2033

- Figure 20: Asia Pacific Micro-Hybrid Vehicles Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 21: Asia Pacific Micro-Hybrid Vehicles Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 22: Asia Pacific Micro-Hybrid Vehicles Industry Revenue (billion), by Battery Type 2025 & 2033

- Figure 23: Asia Pacific Micro-Hybrid Vehicles Industry Revenue Share (%), by Battery Type 2025 & 2033

- Figure 24: Asia Pacific Micro-Hybrid Vehicles Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Micro-Hybrid Vehicles Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World Micro-Hybrid Vehicles Industry Revenue (billion), by Capacity 2025 & 2033

- Figure 27: Rest of the World Micro-Hybrid Vehicles Industry Revenue Share (%), by Capacity 2025 & 2033

- Figure 28: Rest of the World Micro-Hybrid Vehicles Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 29: Rest of the World Micro-Hybrid Vehicles Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 30: Rest of the World Micro-Hybrid Vehicles Industry Revenue (billion), by Battery Type 2025 & 2033

- Figure 31: Rest of the World Micro-Hybrid Vehicles Industry Revenue Share (%), by Battery Type 2025 & 2033

- Figure 32: Rest of the World Micro-Hybrid Vehicles Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Rest of the World Micro-Hybrid Vehicles Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 2: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 3: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Battery Type 2020 & 2033

- Table 4: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 6: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 7: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Battery Type 2020 & 2033

- Table 8: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Rest of North America Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 13: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 14: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Battery Type 2020 & 2033

- Table 15: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Germany Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: France Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Italy Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 22: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 23: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Battery Type 2020 & 2033

- Table 24: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 25: India Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: China Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Japan Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: South Korea Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Rest of Asia Pacific Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 31: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 32: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Battery Type 2020 & 2033

- Table 33: Global Micro-Hybrid Vehicles Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 34: Brazil Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Mexico Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: South Africa Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Other Countries Micro-Hybrid Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Micro-Hybrid Vehicles Industry?

The projected CAGR is approximately 4.8%.

2. Which companies are prominent players in the Micro-Hybrid Vehicles Industry?

Key companies in the market include General Motors, Mahindra and Mahindra, Daimler AG, Kia Motors Corporatio, BMW AG, Hyundai Motors Company, Audi AG, Nissan Motors Company, Subaru, Toyota Motors Company.

3. What are the main segments of the Micro-Hybrid Vehicles Industry?

The market segments include Capacity, Vehicle Type, Battery Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 16.13 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Passenger Vehicle Sales Across the Globe.

6. What are the notable trends driving market growth?

Increasing Demand for Lithium-ion Batteries.

7. Are there any restraints impacting market growth?

High Cost may Restrict the Growth Potential.

8. Can you provide examples of recent developments in the market?

September 2021: Birla Carbon announced its entry into the energy systems market by participating in The Battery Show 2021 in the United States. Demand for higher-performance lead acid batteries is increasing as automakers strive to meet more stringent CO2 emission requirements, particularly for start-stop or micro-hybrid vehicles.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Micro-Hybrid Vehicles Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Micro-Hybrid Vehicles Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Micro-Hybrid Vehicles Industry?

To stay informed about further developments, trends, and reports in the Micro-Hybrid Vehicles Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence