Key Insights

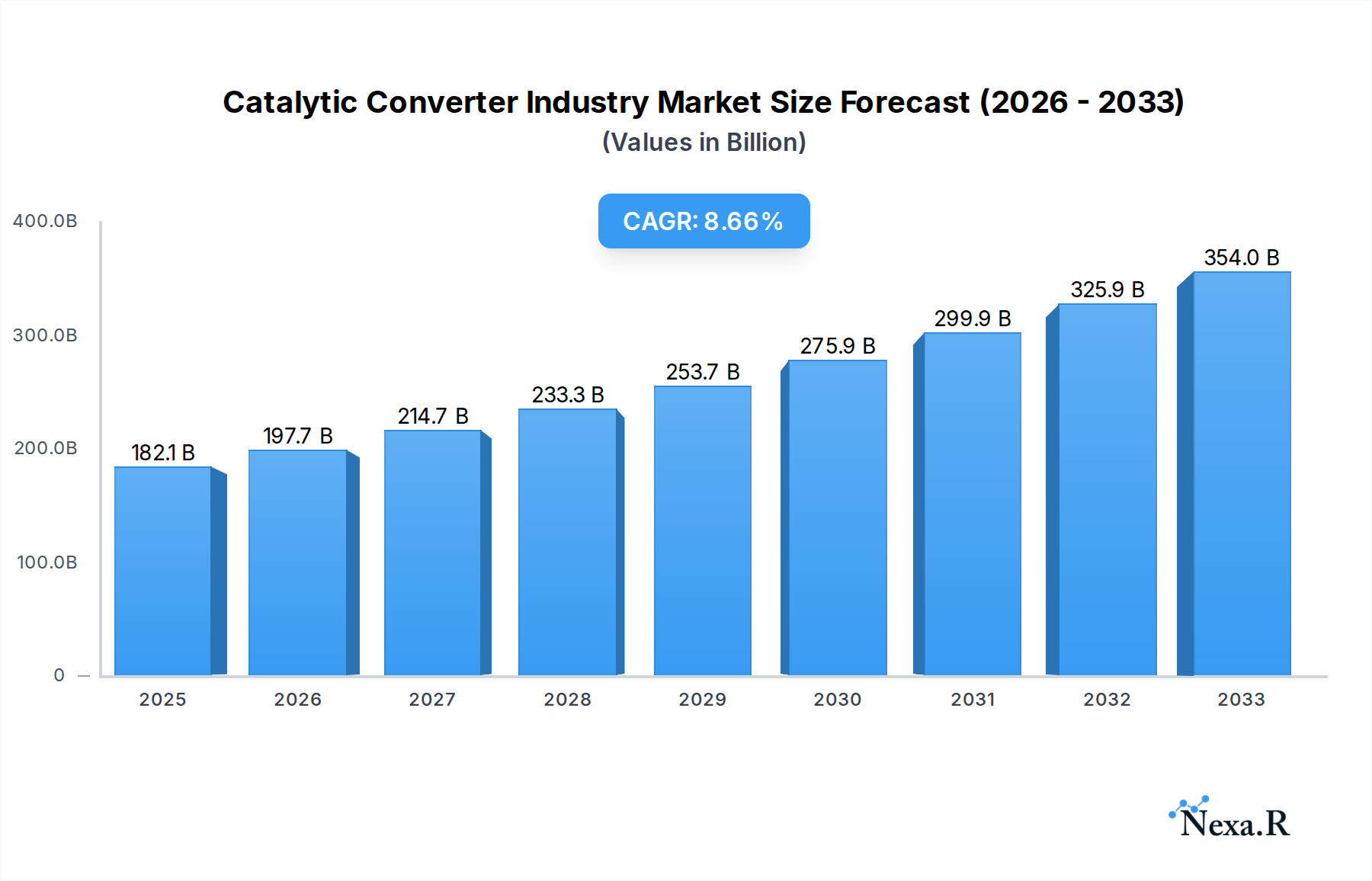

The global Catalytic Converter Industry is poised for significant expansion, projected to reach an impressive $182.1 billion in 2025 and grow at a robust Compound Annual Growth Rate (CAGR) of 8.6% throughout the forecast period. This substantial growth is primarily propelled by increasingly stringent global emission regulations, pushing automakers to adopt advanced catalytic converter technologies that effectively reduce harmful pollutants like nitrogen oxides (NOx), carbon monoxide (CO), and unburned hydrocarbons. The growing demand for cleaner transportation solutions, coupled with the surging sales of both passenger cars and commercial vehicles, especially in emerging economies, forms a powerful market driver. Furthermore, ongoing technological advancements in catalytic converter design, focusing on enhanced efficiency and durability, are contributing to this upward trajectory. The industry is witnessing a strong trend towards the adoption of three-way catalytic converters due to their superior performance in converting multiple pollutants simultaneously, while innovative materials and manufacturing processes are also being explored to optimize functionality and cost-effectiveness.

Catalytic Converter Industry Market Size (In Billion)

Despite the optimistic outlook, certain factors present challenges to sustained growth. The escalating cost of precious metals, such as platinum, palladium, and rhodium, which are crucial components of catalytic converters, poses a significant cost constraint. Fluctuations in these commodity prices directly impact manufacturing expenses and, consequently, the final product cost. Additionally, the increasing popularity of electric vehicles (EVs), which do not require catalytic converters, represents a long-term disruptive trend that could temper overall market expansion. However, the substantial installed base of internal combustion engine (ICE) vehicles and the gradual transition to EVs are expected to ensure continued demand for catalytic converters for the foreseeable future. The market is segmented by type into Two-way Catalytic Converters, Three-way Catalytic Converters, and Other Types, with Three-way Catalytic Converters expected to dominate due to their superior emission control capabilities. Vehicle types are broadly categorized into Passenger Cars and Commercial Vehicles, both contributing to the overall market volume.

Catalytic Converter Industry Company Market Share

Catalytic Converter Market: Global Industry Analysis, Size, Share, Trends, Forecast 2019–2033

This comprehensive report delves into the intricate dynamics of the global catalytic converter market, analyzing its current landscape and projecting future growth trajectories. Spanning a study period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period of 2025–2033, this report provides deep insights into market size evolution, technological advancements, regional dominance, and key player strategies. It offers a granular view of segments including Two-way Catalytic Converters and Three-way Catalytic Converters, and across Passenger Cars and Commercial Vehicles. Understand the forces shaping this vital automotive component sector, from stringent emission regulations to the rise of electric vehicles.

Catalytic Converter Industry Market Dynamics & Structure

The global catalytic converter market exhibits a moderately concentrated structure, driven by a blend of established automotive suppliers and specialized manufacturers. Technological innovation plays a pivotal role, with companies continuously investing in research and development to enhance efficiency, durability, and compliance with evolving emission standards. Regulatory frameworks, particularly stringent emission norms like Euro 7 and EPA standards, are the primary architects of market demand, compelling automakers to integrate advanced catalytic converter technologies. The competitive landscape features significant players offering robust product portfolios, while the threat of competitive product substitutes, such as alternative emission control technologies in the nascent stages of electric vehicle adoption, remains a factor. End-user demographics are predominantly tied to global automotive production and sales volumes, with a growing emphasis on sustainability and fuel efficiency influencing consumer preferences. Mergers and acquisition (M&A) trends are notable as larger entities seek to consolidate market share and acquire advanced technological capabilities, aiming to secure a competitive edge in a rapidly evolving industry.

- Market Concentration: Dominated by a few key global players with significant market share.

- Technological Innovation Drivers: Focus on reducing NOx, CO, and hydrocarbon emissions; development of cost-effective and durable materials; integration with advanced exhaust aftertreatment systems.

- Regulatory Frameworks: Stringent global emission standards (e.g., Euro 7, EPA) are the primary growth catalysts.

- Competitive Product Substitutes: Emerging alternative emission control technologies and the long-term shift towards electric vehicles pose potential future threats.

- End-User Demographics: Closely linked to global automotive sales, fleet modernization, and growing consumer awareness of environmental impact.

- M&A Trends: Strategic acquisitions to expand technological capabilities, geographical reach, and product offerings.

Catalytic Converter Industry Growth Trends & Insights

The catalytic converter industry is experiencing robust growth, underpinned by stringent global emission regulations and the persistent demand for internal combustion engine (ICE) vehicles. The market size, projected to reach an estimated $XX billion by 2025, is anticipated to witness a Compound Annual Growth Rate (CAGR) of approximately X% during the forecast period of 2025–2033. Adoption rates for advanced three-way catalytic converters, designed to abate a wider spectrum of pollutants, are steadily increasing, especially in regions with stricter environmental mandates. Technological disruptions, such as the development of electric heated catalysts (e-catalysts) by companies like Benteler, are emerging to address cold-start emission challenges and ensure compliance with the latest emission standards. These innovations are crucial for maintaining the efficacy of catalytic converters even in hybrid and advanced ICE powertrains. Consumer behavior shifts, while increasingly favoring electric mobility in the long term, still show a strong reliance on traditional vehicles for a significant portion of the global market, thus sustaining the demand for catalytic converters. The penetration of advanced emission control systems is further propelled by government incentives and the increasing corporate focus on Environmental, Social, and Governance (ESG) principles within the automotive sector. The market's evolution is also influenced by the circular economy principles, with a growing focus on recycling and recovery of precious metals from used catalytic converters.

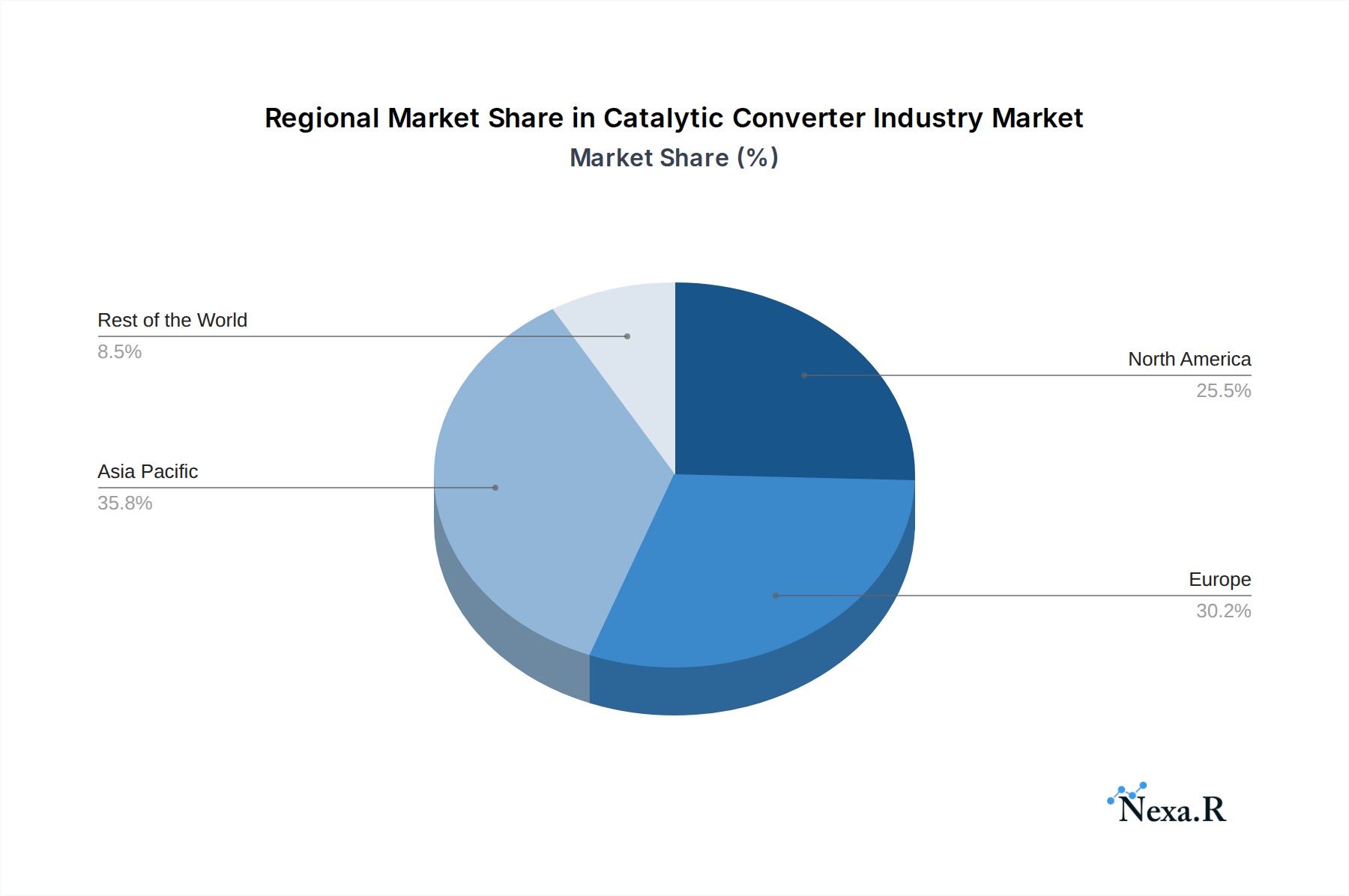

Dominant Regions, Countries, or Segments in Catalytic Converter Industry

The Three-way Catalytic Converter segment, particularly for Passenger Cars, currently dominates the global catalytic converter market. This dominance is primarily driven by the widespread adoption of gasoline-powered passenger vehicles worldwide and the stringent emission regulations that necessitate the use of three-way catalytic converters to simultaneously reduce carbon monoxide (CO), unburned hydrocarbons (HC), and nitrogen oxides (NOx).

Key Drivers for Dominance:

- Stringent Emission Standards: Regions like Europe (EU-7 standards), North America (EPA regulations), and increasingly China (National Standards VIb) mandate the use of advanced three-way catalytic converters for gasoline engines.

- High Volume of Passenger Car Production & Sales: Asia-Pacific, particularly China and India, along with North America and Europe, are massive markets for passenger cars, directly translating into high demand for catalytic converters.

- Technological Advancement: Continuous improvements in the design and material composition of three-way catalytic converters have made them highly efficient in pollutant abatement for gasoline engines.

- Regulatory Push for Cleaner Air: Growing global awareness and governmental efforts to combat air pollution have led to stricter enforcement of emission norms, reinforcing the importance of catalytic converters.

Regional Dominance:

- Asia-Pacific: This region is a major hub for automotive manufacturing and consumption. China, as the world's largest automobile market, significantly influences global demand. The rapid industrialization and expanding middle class in countries like India also contribute to substantial growth in the passenger car segment. The implementation of stricter emission standards in China has further accelerated the adoption of advanced catalytic converters.

- Europe: Europe has historically been at the forefront of stringent environmental regulations. The ongoing evolution of Euro emission standards continues to drive demand for sophisticated catalytic converter technologies. The strong presence of premium automotive manufacturers also contributes to the demand for high-performance emission control systems.

- North America: The United States, with its large passenger vehicle fleet and established automotive industry, remains a critical market. The EPA's emission standards, though sometimes evolving, consistently require the use of effective catalytic converters. The ongoing sales of gasoline-powered vehicles ensure a sustained demand.

While commercial vehicles also contribute significantly to the market, especially with advancements in diesel exhaust aftertreatment systems, the sheer volume of passenger car production and sales globally solidifies the three-way catalytic converter segment for passenger cars as the dominant force.

Catalytic Converter Industry Product Landscape

The catalytic converter industry is characterized by continuous product innovation aimed at enhancing emission control efficiency and durability. Key product developments include the evolution of Three-way Catalytic Converters (TWC) with improved washcoat formulations and optimized cell densities for greater surface area and catalytic activity, leading to near-complete conversion of CO, HC, and NOx. Innovations like electric heated catalysts (e-catalysts) are gaining traction, enabling rapid catalyst light-off during cold starts, crucial for meeting stringent emission norms like EU-7. These advanced TWCs are designed for a wide range of gasoline engines, including direct-injection and hybrid powertrains. For diesel vehicles, Diesel Oxidation Catalysts (DOC) and Diesel Particulate Filters (DPF) are integral components of the aftertreatment system, often working in conjunction with Selective Catalytic Reduction (SCR) systems for NOx control. The unique selling proposition lies in achieving compliance with ever-tightening regulations while balancing cost-effectiveness and performance.

Key Drivers, Barriers & Challenges in Catalytic Converter Industry

Key Drivers:

- Stringent Emission Regulations: Global mandates for reducing air pollutants from vehicles are the primary growth driver, forcing automakers to integrate advanced catalytic converter systems.

- Increasing Automotive Production: The continued global demand for vehicles, particularly in emerging economies, directly fuels the need for catalytic converters.

- Technological Advancements: Development of more efficient, durable, and cost-effective catalytic converter technologies, including e-catalysts, creates market opportunities.

- Focus on Air Quality: Growing public and governmental concern over air pollution necessitates cleaner exhaust emissions.

Key Barriers & Challenges:

- Transition to Electric Vehicles (EVs): The long-term shift towards EVs poses a significant challenge as they do not require catalytic converters, potentially shrinking the market in the distant future.

- Precious Metal Volatility: The reliance on precious metals like platinum, palladium, and rhodium makes production costs susceptible to price fluctuations.

- Counterfeiting and Theft: The high value of precious metals leads to increased instances of catalytic converter theft, impacting vehicle owners and necessitating new security measures.

- Supply Chain Disruptions: Global supply chain complexities can impact the availability and cost of raw materials and finished products.

- Cost Sensitivity: Automakers face pressure to minimize production costs, which can influence the selection and adoption of advanced, albeit potentially more expensive, catalytic converter technologies.

Emerging Opportunities in Catalytic Converter Industry

Emerging opportunities in the catalytic converter industry lie in the development of next-generation catalysts that can handle a wider spectrum of pollutants with even greater efficiency, especially for advanced internal combustion engine technologies and hybrid vehicles. The increasing demand for catalysts with longer lifespans and improved resistance to poisoning presents a significant avenue. Furthermore, the growing focus on the circular economy presents opportunities in efficient recycling and recovery of precious metals from end-of-life catalytic converters, creating a closed-loop system. Untapped markets in regions undergoing rapid vehicle fleet expansion and tightening emission standards also offer substantial growth potential. The development of modular catalytic converter systems that can be easily adapted to various vehicle platforms and powertrain configurations is another promising area.

Growth Accelerators in the Catalytic Converter Industry Industry

The catalytic converter industry's growth is significantly accelerated by ongoing technological breakthroughs in materials science and catalyst formulation, leading to enhanced performance and reduced precious metal loading. Strategic partnerships between catalyst manufacturers and automotive OEMs are crucial for co-developing compliant and cost-effective emission solutions for upcoming vehicle models and stringent regulations. Market expansion strategies targeting regions with rapidly growing automotive sectors and evolving environmental policies, such as parts of Southeast Asia and Africa, are vital. The increasing focus on sustainability and the growing adoption of hybrid vehicle technologies, which still rely on catalytic converters for their ICE components, act as sustained growth accelerators.

Key Players Shaping the Catalytic Converter Industry Market

- Sango Co Ltd

- Boysen

- Katcon S A de C V

- Futaba Industrial Co Ltd

- Hanwoo Industrial Co Ltd

- Eberspacher Group

- Magneti Marelli S p A

- Tenneco Inc

- Yutaka Giken Company Limited

- BOSAL International

- Faurecia SE

- Benteler International A

- Sejong Industrial Co Ltd

Notable Milestones in Catalytic Converter Industry Sector

- December 2021: Leduc RCMP, in partnership with the City of Leduc, held a Catalytic Converter Theft Prevention event, highlighting a new crime prevention strategy and demonstrating VIN etching onto vehicle catalytic converters.

- March 2021: Eberspaecher inaugurated a new 21,000 square meter plant for exhaust technology in Ramos Arizpe, Mexico, to enhance production efficiency and reduce emissions.

- July 2020: BENTELER announced readiness to offer electric heated catalysts to car manufacturers, designed to meet EU-7 standards by rapidly reaching optimal operating temperature and ensuring near 100% pollutant removal during cold starts.

- March 2020: Vitesco Technologies and Continental's Powertrain division secured a major contract from a European vehicle manufacturer for EMICAT brand e-catalyst technology, an innovative electric heating element for diesel catalytic converters, for two 48-volt hybrid van models with production scheduled for end 2022.

In-Depth Catalytic Converter Industry Market Outlook

The catalytic converter industry is poised for continued growth, driven by the unwavering need for emission control in internal combustion engine vehicles and the stringent regulatory landscape. While the long-term transition to electric mobility presents a future challenge, the near-to-medium term outlook remains robust, especially with the evolution of hybrid technologies. Strategic opportunities lie in developing advanced catalysts with reduced precious metal content and enhanced durability, catering to tightening emission standards like EU-7. Furthermore, the growing emphasis on circular economy principles will foster significant growth in the recycling and remanufacturing of catalytic converters. Companies that invest in innovation, secure stable supply chains for critical materials, and adeptly navigate evolving regulations will be well-positioned for sustained success in this dynamic market.

Catalytic Converter Industry Segmentation

-

1. Type

- 1.1. Two-way Catalytic Converter

- 1.2. Three-way Catalytic Converter

- 1.3. Other Types

-

2. Vehicle Type

- 2.1. Passenger Cars

- 2.2. Commercial Vehicles

Catalytic Converter Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Spain

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. India

- 3.2. China

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Catalytic Converter Industry Regional Market Share

Geographic Coverage of Catalytic Converter Industry

Catalytic Converter Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Two-way Catalytic Converter

- 5.1.2. Three-way Catalytic Converter

- 5.1.3. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Passenger Cars

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Catalytic Converter Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Two-way Catalytic Converter

- 6.1.2. Three-way Catalytic Converter

- 6.1.3. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.2.1. Passenger Cars

- 6.2.2. Commercial Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Catalytic Converter Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Two-way Catalytic Converter

- 7.1.2. Three-way Catalytic Converter

- 7.1.3. Other Types

- 7.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.2.1. Passenger Cars

- 7.2.2. Commercial Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Catalytic Converter Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Two-way Catalytic Converter

- 8.1.2. Three-way Catalytic Converter

- 8.1.3. Other Types

- 8.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.2.1. Passenger Cars

- 8.2.2. Commercial Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Catalytic Converter Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Two-way Catalytic Converter

- 9.1.2. Three-way Catalytic Converter

- 9.1.3. Other Types

- 9.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.2.1. Passenger Cars

- 9.2.2. Commercial Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Rest of the World Catalytic Converter Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Two-way Catalytic Converter

- 10.1.2. Three-way Catalytic Converter

- 10.1.3. Other Types

- 10.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.2.1. Passenger Cars

- 10.2.2. Commercial Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Sango Co Ltd

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Boysen

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Katcon S A de C V

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Futaba Industrial Co Ltd

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Hanwoo Industrial Co Ltd

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Eberspacher Group

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Magneti Marelli S p A

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Tenneco Inc

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Yutaka Giken Company Limited

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 BOSAL International

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Faurecia SE

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Benteler International A

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 Sejong Industrial Co Ltd

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.1 Sango Co Ltd

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Catalytic Converter Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Catalytic Converter Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Catalytic Converter Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Catalytic Converter Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 5: North America Catalytic Converter Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 6: North America Catalytic Converter Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Catalytic Converter Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Catalytic Converter Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: Europe Catalytic Converter Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Europe Catalytic Converter Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 11: Europe Catalytic Converter Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 12: Europe Catalytic Converter Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Catalytic Converter Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Catalytic Converter Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Asia Pacific Catalytic Converter Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Asia Pacific Catalytic Converter Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 17: Asia Pacific Catalytic Converter Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 18: Asia Pacific Catalytic Converter Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Catalytic Converter Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Catalytic Converter Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Rest of the World Catalytic Converter Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Rest of the World Catalytic Converter Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 23: Rest of the World Catalytic Converter Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 24: Rest of the World Catalytic Converter Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Rest of the World Catalytic Converter Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Catalytic Converter Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Catalytic Converter Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 3: Global Catalytic Converter Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Catalytic Converter Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Catalytic Converter Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 6: Global Catalytic Converter Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Catalytic Converter Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Catalytic Converter Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Rest of North America Catalytic Converter Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Catalytic Converter Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global Catalytic Converter Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 12: Global Catalytic Converter Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Germany Catalytic Converter Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Catalytic Converter Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: France Catalytic Converter Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Spain Catalytic Converter Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Rest of Europe Catalytic Converter Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Global Catalytic Converter Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 19: Global Catalytic Converter Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 20: Global Catalytic Converter Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: India Catalytic Converter Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: China Catalytic Converter Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Japan Catalytic Converter Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: South Korea Catalytic Converter Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Rest of Asia Pacific Catalytic Converter Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Global Catalytic Converter Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 27: Global Catalytic Converter Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 28: Global Catalytic Converter Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 29: South America Catalytic Converter Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Middle East and Africa Catalytic Converter Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Catalytic Converter Industry?

The projected CAGR is approximately 8.6%.

2. Which companies are prominent players in the Catalytic Converter Industry?

Key companies in the market include Sango Co Ltd, Boysen, Katcon S A de C V, Futaba Industrial Co Ltd, Hanwoo Industrial Co Ltd, Eberspacher Group, Magneti Marelli S p A, Tenneco Inc, Yutaka Giken Company Limited, BOSAL International, Faurecia SE, Benteler International A, Sejong Industrial Co Ltd.

3. What are the main segments of the Catalytic Converter Industry?

The market segments include Type, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 182.1 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Electric Vehicles; Others.

6. What are the notable trends driving market growth?

Three-way Catalytic Converters Likely to Grow Significantly During the Forecast Period.

7. Are there any restraints impacting market growth?

Product Recalls; Others.

8. Can you provide examples of recent developments in the market?

In December 2021, Leduc RCMP, in partnership with the City of Leduc, held a Catalytic Converter Theft Prevention event. This event highlighted a new crime prevention strategy and a demonstration was given of the etching of the vehicle identification number (VIN) number onto a catalytic converter of a vehicle.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Catalytic Converter Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Catalytic Converter Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Catalytic Converter Industry?

To stay informed about further developments, trends, and reports in the Catalytic Converter Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence