Key Insights

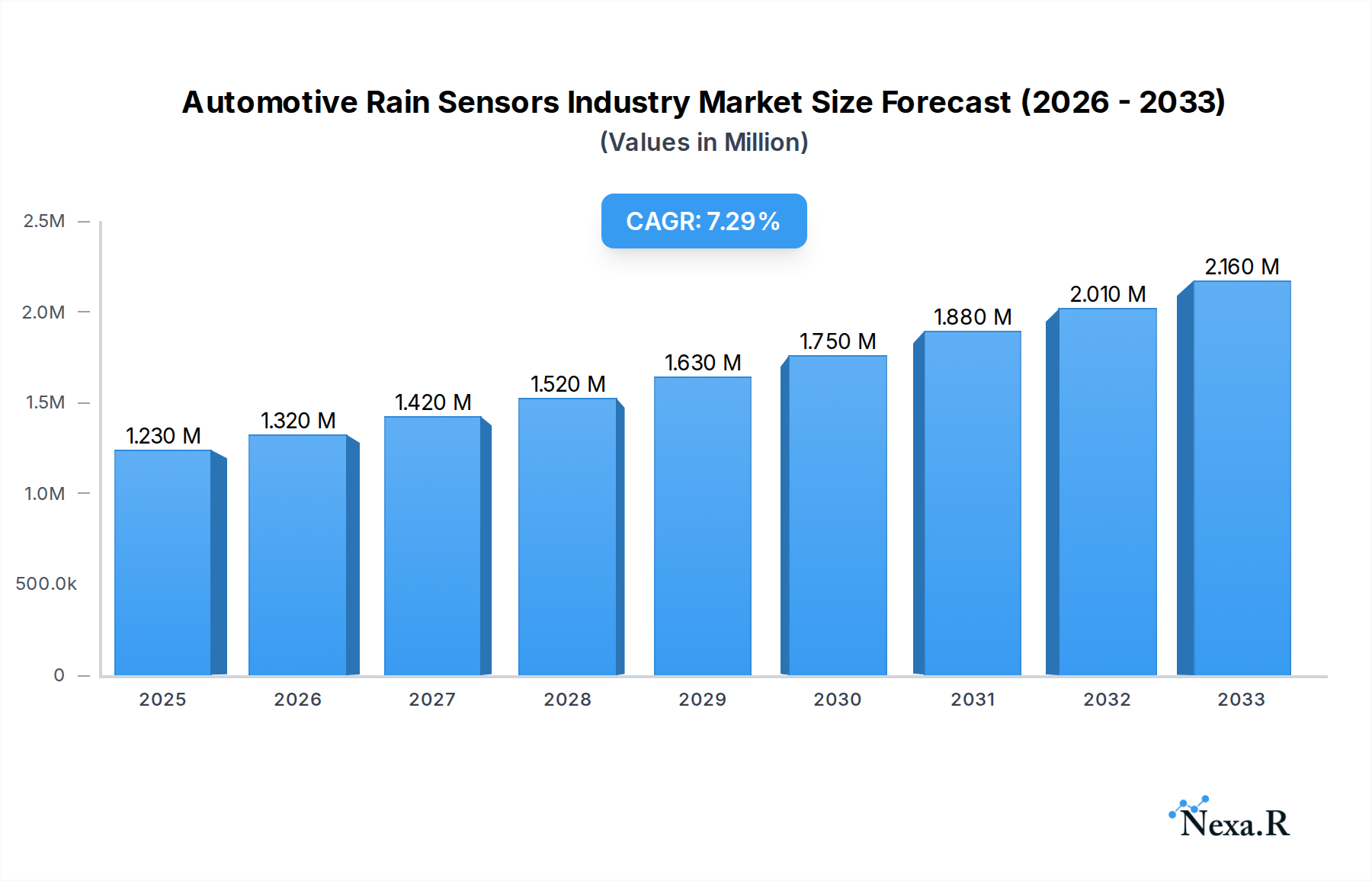

The global Automotive Rain Sensors market is poised for significant expansion, projected to reach 1.23 Million units in 2025 with a robust Compound Annual Growth Rate (CAGR) of 7.20% during the forecast period of 2025-2033. This dynamic growth is propelled by an increasing consumer demand for enhanced vehicle safety features and driver comfort. The integration of advanced driver-assistance systems (ADAS) is a primary driver, with rain sensors playing a crucial role in enabling features like automatic windshield wipers and adaptive headlights. As automotive manufacturers continue to prioritize sophisticated technology to differentiate their offerings and comply with evolving safety regulations, the adoption of rain sensor technology is expected to accelerate. Furthermore, the growing automotive production volumes worldwide, particularly in emerging economies, directly contribute to the expanding market for these essential components.

Automotive Rain Sensors Industry Market Size (In Million)

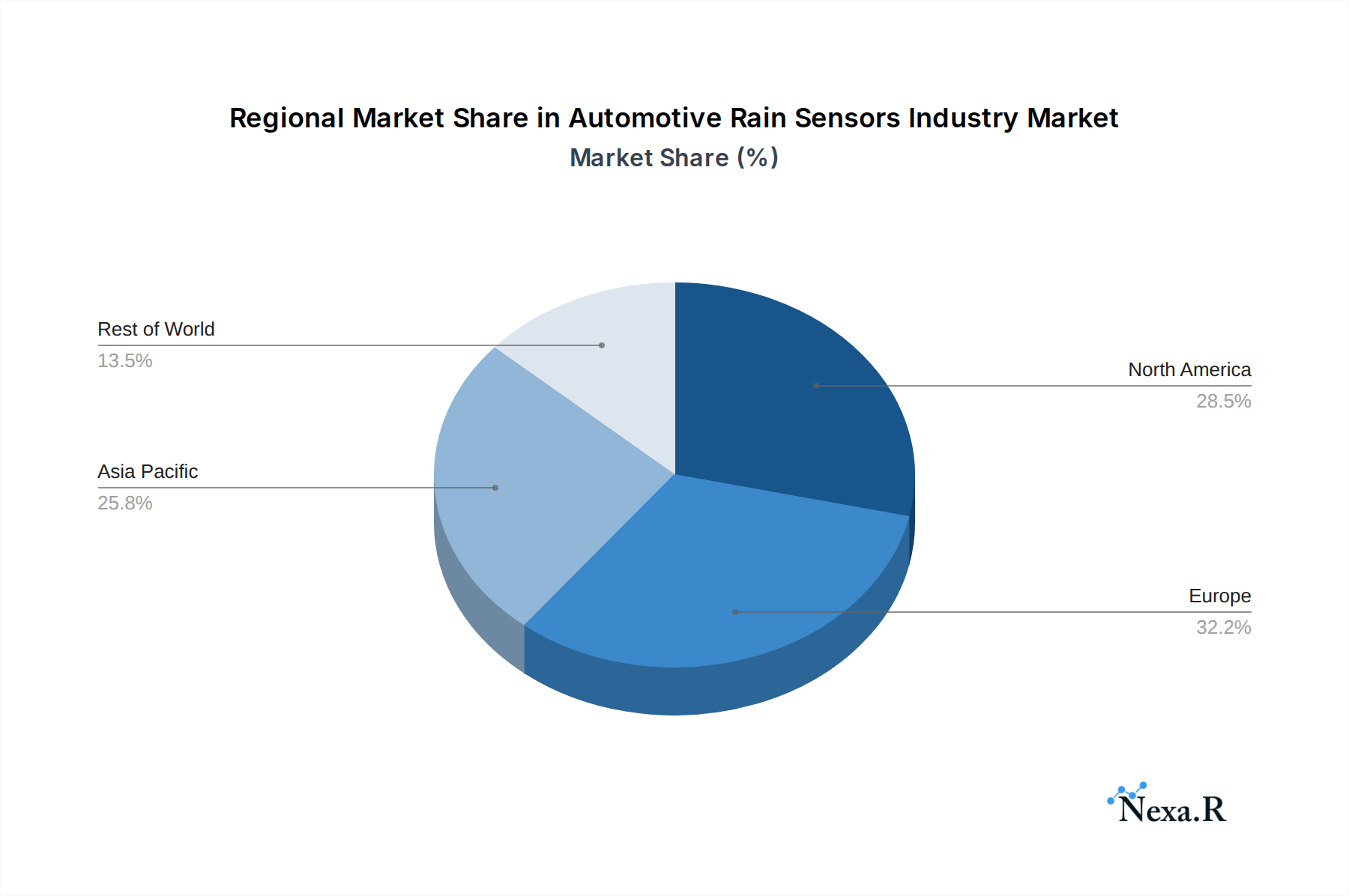

The market's trajectory is also influenced by technological advancements, leading to more accurate, reliable, and cost-effective rain sensor solutions. Innovations in optical and capacitive sensing technologies are enhancing performance and broadening application possibilities. However, challenges such as the initial cost of integration for some vehicle segments and potential competition from simpler, less integrated solutions in lower-cost vehicles could pose moderate restraints. Nevertheless, the overwhelming trend towards autonomous driving and the continuous pursuit of improved driving experiences are powerful tailwinds. Key players like Denso Corporation, Valeo Group, and ams-OSRAM International GmbH are actively investing in research and development, further stimulating innovation and market growth across major automotive hubs like North America, Europe, and the Asia Pacific region, with China and India emerging as significant growth markets.

Automotive Rain Sensors Industry Company Market Share

Automotive Rain Sensors Industry Market Dynamics & Structure

The automotive rain sensors industry is characterized by a dynamic interplay of technological innovation, evolving regulatory landscapes, and increasing demand for advanced driver-assistance systems (ADAS). Market concentration is moderately high, with key players like Denso Corporation, Valeo Group, and ams-OSRAM International GmbH holding significant shares. Technological innovation, particularly in optical and infrared sensing, is a primary driver, enabling more accurate detection in various weather conditions. Regulatory frameworks promoting vehicle safety, such as mandatory ADAS adoption in certain regions, further bolster market growth. Competitive product substitutes, including manual wiper controls and integrated camera-based systems, are present but often lack the precision and automation capabilities of dedicated rain sensors. End-user demographics are shifting towards a greater appreciation for convenience and safety features, especially among younger demographics and in regions with unpredictable weather patterns. Merger and acquisition (M&A) trends are expected to continue as larger automotive suppliers integrate specialized sensor technologies to enhance their ADAS offerings. The market is poised for robust expansion, driven by the continuous integration of intelligent sensing solutions across all vehicle types.

- Market Concentration: Moderate, with top players dominating the supply chain.

- Technological Innovation Drivers: Enhanced optical/infrared sensing, improved algorithms for adverse weather.

- Regulatory Frameworks: Mandates for ADAS features, safety standard improvements.

- Competitive Product Substitutes: Manual controls, camera-based perception systems.

- End-User Demographics: Growing demand for convenience and safety features.

- M&A Trends: Consolidation for integrated ADAS solutions.

Automotive Rain Sensors Industry Growth Trends & Insights

The automotive rain sensors market is experiencing a significant growth trajectory, projected to expand from an estimated $X,XXX million units in 2025 to $Y,YYY million units by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of Z.ZZ% during the forecast period of 2025-2033. This robust expansion is underpinned by several key trends and insights. The increasing adoption of Advanced Driver-Assistance Systems (ADAS) across all vehicle segments, including passenger cars and commercial vehicles, is a primary catalyst. As vehicles become more autonomous and intelligent, the demand for reliable environmental sensing capabilities, such as accurate rain detection, escalates. The integration of rain sensors not only enhances driver convenience by automating wiper operation but also plays a crucial role in optimizing other ADAS functions, like automatic headlamp activation and improving the performance of forward-facing cameras in wet conditions.

Technological disruptions, such as advancements in optical sensor technology, infrared sensing, and sophisticated signal processing algorithms, are enabling rain sensors to perform with greater precision and reliability, even in challenging weather scenarios like heavy rain, fog, and low-light conditions. This improved performance is crucial for the development and deployment of higher levels of automation (Level 2+ and beyond). Consumer behavior is also shifting, with a growing preference for vehicles equipped with advanced comfort and safety features. The perceived value of features that enhance driving comfort and reduce driver workload, especially during inclement weather, is directly translating into higher demand for vehicles equipped with rain sensors. Furthermore, the trend towards vehicle electrification and the integration of centralized electrical architectures in new vehicle designs create opportunities for more streamlined and efficient integration of sensor technologies. The market penetration of rain sensors, currently at approximately XX% in new vehicle production, is anticipated to climb significantly as these advanced features become standard across a wider range of vehicle models and price points. The historical period (2019-2024) has laid the groundwork for this accelerated growth, with increasing R&D investments and initial ADAS adoption paving the way for current market momentum. The base year of 2025 serves as a critical benchmark, with further analysis revealing the intricate evolution of market size and the drivers behind its projected expansion.

Dominant Regions, Countries, or Segments in Automotive Rain Sensors Industry

The Passenger Cars segment is currently the dominant force driving growth within the global Automotive Rain Sensors Industry, projected to maintain its lead throughout the forecast period (2025-2033). This dominance is attributed to several intertwined factors including the sheer volume of passenger car production worldwide, the increasing consumer demand for comfort and safety features in personal vehicles, and the faster pace of ADAS technology adoption in this segment compared to commercial vehicles.

Key Drivers for Passenger Car Dominance:

- High Production Volumes: Globally, the production of passenger cars significantly outnumbers that of commercial vehicles, naturally leading to a larger installed base for automotive rain sensors. In 2025, passenger car production is estimated to reach XX million units, compared to X million units for commercial vehicles.

- Consumer Preference for Convenience and Safety: Modern car buyers place a high premium on features that enhance driving comfort and safety. Automatic wiper and headlamp control, enabled by rain sensors, are perceived as essential convenience features, especially in regions with frequent rainfall. Surveys indicate that over XX% of new car buyers consider these features important.

- Accelerated ADAS Integration: The automotive industry's push towards advanced driver-assistance systems (ADAS) is more pronounced in passenger cars. Features like automatic emergency braking, lane keeping assist, and adaptive cruise control often rely on integrated sensor fusion, where rain sensors play a supporting role by ensuring optimal camera and LiDAR performance in adverse weather. This integration is projected to see a XX% increase in passenger cars by 2027.

- Aftermarket Opportunities: While factory-fitted sensors are the primary market, the aftermarket segment for retrofitting rain sensors into older passenger vehicles also contributes to the segment's growth, particularly in developed markets. This segment is estimated to grow at a CAGR of XX% from 2025 to 2033.

- Regulatory Push for Safety Standards: While safety regulations are impacting both segments, the accessibility and affordability of integrated safety features are driving their adoption more rapidly in the passenger car segment, influencing manufacturer focus.

Geographically, North America and Europe are leading regions in the adoption of automotive rain sensors, driven by stringent safety regulations and a high consumer demand for premium features in their passenger car fleets. In 2025, these regions are expected to account for approximately XX% and XX% of the global passenger car rain sensor market, respectively. Economic policies that support the automotive industry, coupled with robust infrastructure for vehicle manufacturing and research, further solidify their leading positions. The growth potential in emerging markets like Asia-Pacific, particularly China, is also substantial, fueled by a rapidly expanding middle class and increasing vehicle ownership.

Automotive Rain Sensors Industry Product Landscape

The product landscape of automotive rain sensors is evolving towards more sophisticated and integrated solutions. Primarily based on optical sensing technology, these sensors utilize infrared light to detect the presence and intensity of raindrops on a windshield. Innovations focus on enhancing accuracy in diverse weather conditions, reducing false positives, and integrating with other vehicle systems. Advanced algorithms allow for precise control of wiper speed and automatic headlamp activation, contributing to enhanced driver safety and comfort. The unique selling proposition lies in their ability to provide an autonomous and seamless driving experience by proactively managing visibility challenges. Technological advancements are also exploring the fusion of rain sensor data with other sensor inputs, such as cameras and LiDAR, for a more comprehensive understanding of environmental conditions.

Key Drivers, Barriers & Challenges in Automotive Rain Sensors Industry

Key Drivers:

- Increasing Adoption of ADAS: The primary growth driver is the continuous integration of Advanced Driver-Assistance Systems (ADAS) across vehicle types, necessitating reliable environmental sensing for features like automatic headlights and wipers.

- Enhanced Vehicle Safety and Comfort: Consumer demand for features that improve safety and driving comfort, especially during inclement weather, fuels market expansion.

- Technological Advancements: Ongoing improvements in optical sensing technology and signal processing lead to more accurate and reliable rain detection.

- Regulatory Push for Safety Standards: Government mandates and safety ratings increasingly favor vehicles equipped with advanced safety and convenience features.

Key Barriers & Challenges:

- Cost of Integration: The initial cost of implementing advanced rain sensor systems can be a barrier, particularly for entry-level vehicle models.

- Environmental Interference: Extreme conditions such as heavy snow, ice buildup, or dirt on the windshield can sometimes interfere with sensor performance, leading to potential inaccuracies.

- Supply Chain Disruptions: Like many industries, the automotive sensor market is susceptible to global supply chain issues impacting component availability and pricing.

- Competition from Integrated Camera Systems: While not always as precise, some camera-based ADAS systems can perform rudimentary rain detection, posing a competitive threat in certain applications. The market is projected to face a XX% impact from this competitive pressure by 2028.

Emerging Opportunities in Automotive Rain Sensors Industry

Emerging opportunities in the Automotive Rain Sensors Industry lie in the expansion of sensor capabilities beyond basic rain detection. This includes developing multi-functional sensors that can also detect fog, ice, and even road surface conditions, offering a more comprehensive environmental awareness for vehicles. The growing demand for autonomous driving at higher levels (Level 3 and above) presents a significant opportunity, as these systems require extremely reliable perception in all weather conditions. Furthermore, the integration of these sensors into vehicle-to-everything (V2X) communication systems could enable proactive safety measures by sharing real-time weather data with other vehicles and infrastructure. The development of cost-effective solutions for emerging markets and the aftermarket segment also represents a substantial untapped potential.

Growth Accelerators in the Automotive Rain Sensors Industry Industry

Several key catalysts are accelerating the long-term growth of the Automotive Rain Sensors Industry. The relentless pursuit of enhanced vehicle safety and the increasing capabilities of ADAS technologies are fundamental drivers. Strategic partnerships between sensor manufacturers and automotive OEMs are crucial for seamless integration and tailored solutions. For instance, the partnership between StradVision and ZF in March 2022, aimed at expanding automated driving perception software, highlights this trend, enabling better object detection in adverse weather. The ongoing advancements in sensor fusion, where data from rain sensors is combined with other sensor inputs, will unlock new functionalities and improve the overall performance of intelligent vehicle systems. Market expansion strategies, including penetration into new geographic regions and a focus on the rapidly growing electric vehicle (EV) segment, will further boost growth.

Key Players Shaping the Automotive Rain Sensors Industry Market

- Denso Corporation

- Valeo group

- ams-OSRAM International GmbH

- STMicroelectronics

- HELLA GmbH & Co KGaA

- HAMAMATSU PHOTONICS KK

- Semiconductor Components Industries LLC

- Analog Devices Inc

- ZF Friedrichshafen AG

Notable Milestones in Automotive Rain Sensors Industry Sector

- March 2022: StradVision and ZF announced a partnership to expand their automated driving perception software portfolio. StradVision's SVNet software could enable vehicles to detect and identify objects even in adverse weather or low-light conditions, environmental sensor fusion for shuttles, and commercial and light vehicles that could be optimized for centralized electrical architectures. This collaboration aims to enhance the perception capabilities of autonomous and advanced driver-assistance systems, directly impacting the use case and integration of environmental sensors like rain detectors.

- July 2021: After the partnership with LiDAR expert AEye, Continental could integrate the long-range LiDAR technology into its full sensor stack solution to create the first full-stack automotive-grade system for Level 2+ up to Level 4 automated and autonomous driving applications. The solution based on AEye's LiDAR technology is a substantial part of the sensor setup for high-level automation systems. This signifies a trend towards integrating multiple sensor technologies, including those for environmental sensing like rain detection, to achieve comprehensive situational awareness for autonomous driving.

In-Depth Automotive Rain Sensors Industry Market Outlook

The Automotive Rain Sensors Industry is poised for substantial growth, driven by the accelerating adoption of ADAS and the increasing demand for intelligent, safety-enhanced vehicles. The ongoing technological evolution, focusing on higher accuracy, multi-functionality, and seamless sensor fusion, will be critical in realizing the full potential of autonomous driving. Strategic collaborations between technology providers and automotive manufacturers are expected to streamline development and deployment, ensuring that advanced sensor capabilities are integrated effectively into future vehicle architectures. The market will likely see a rise in demand for integrated sensor modules that combine rain detection with other environmental sensing functions, offering a more holistic approach to vehicle perception. The expansion into emerging markets and the continued innovation in cost-effective solutions will further solidify the industry's robust future outlook, positioning rain sensors as an indispensable component of modern automotive technology.

Automotive Rain Sensors Industry Segmentation

-

1. Vehicle Type

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

Automotive Rain Sensors Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Russia

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. India

- 3.2. China

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of World

- 4.1. Brazil

- 4.2. Saudi Arabia

- 4.3. United Arab Emirates

- 4.4. South Africa

- 4.5. Rest of World

Automotive Rain Sensors Industry Regional Market Share

Geographic Coverage of Automotive Rain Sensors Industry

Automotive Rain Sensors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.20% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Rest of World

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Global Automotive Rain Sensors Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. North America Automotive Rain Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.1.1. Passenger Cars

- 7.1.2. Commercial Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8. Europe Automotive Rain Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.1.1. Passenger Cars

- 8.1.2. Commercial Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9. Asia Pacific Automotive Rain Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.1.1. Passenger Cars

- 9.1.2. Commercial Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10. Rest of World Automotive Rain Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.1.1. Passenger Cars

- 10.1.2. Commercial Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Denso Corporation

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Valeo group

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 ams-OSRAM International GmbH

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 STMicroelectronics

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 HELLA GmbH & Co KGaA

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 HAMAMATSU PHOTONICS KK*List Not Exhaustive

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Semiconductor Components Industries LLC

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Analog Devices Inc

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 ZF Friedrichshafen AG

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.1 Denso Corporation

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Automotive Rain Sensors Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Rain Sensors Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 3: North America Automotive Rain Sensors Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 4: North America Automotive Rain Sensors Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America Automotive Rain Sensors Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Automotive Rain Sensors Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 7: Europe Automotive Rain Sensors Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 8: Europe Automotive Rain Sensors Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Europe Automotive Rain Sensors Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Automotive Rain Sensors Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 11: Asia Pacific Automotive Rain Sensors Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 12: Asia Pacific Automotive Rain Sensors Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Asia Pacific Automotive Rain Sensors Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Rest of World Automotive Rain Sensors Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 15: Rest of World Automotive Rain Sensors Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 16: Rest of World Automotive Rain Sensors Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Rest of World Automotive Rain Sensors Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 2: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 4: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: United States Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Canada Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: Mexico Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Rest of North America Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 10: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Germany Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: United Kingdom Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: France Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Russia Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Spain Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Rest of Europe Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 18: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: India Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: China Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Japan Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: South Korea Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Rest of Asia Pacific Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 25: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Brazil Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Saudi Arabia Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: United Arab Emirates Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: South Africa Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of World Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Rain Sensors Industry?

The projected CAGR is approximately 7.20%.

2. Which companies are prominent players in the Automotive Rain Sensors Industry?

Key companies in the market include Denso Corporation, Valeo group, ams-OSRAM International GmbH, STMicroelectronics, HELLA GmbH & Co KGaA, HAMAMATSU PHOTONICS KK*List Not Exhaustive, Semiconductor Components Industries LLC, Analog Devices Inc, ZF Friedrichshafen AG.

3. What are the main segments of the Automotive Rain Sensors Industry?

The market segments include Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.23 Million as of 2022.

5. What are some drivers contributing to market growth?

Rapid Urbanization and Demand for Convinient Transportation.

6. What are the notable trends driving market growth?

RISING AWARENESS TOWARDS SAFETY AND COMFORT EXPECTED TO DRIVE DEMAND.

7. Are there any restraints impacting market growth?

Traffic Congestion in Major Cities.

8. Can you provide examples of recent developments in the market?

In March 2022, StradVision and ZF announced a partnership to expand their automated driving perception software portfolio. StradVision's SVNet software could enable vehicles to detect and identify objects even in adverse weather or low-light conditions, environmental sensor fusion for shuttles, and commercial and light vehicles that could be optimized for centralized electrical architectures.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Rain Sensors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Rain Sensors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Rain Sensors Industry?

To stay informed about further developments, trends, and reports in the Automotive Rain Sensors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence